21 mins ago

7,233

Author: Michael Nadeau, The DeFi Report; Compiled by: Wu Baht, Golden Finance

We have said it many times: if you don’t understand macroeconomic trends, you don’t understand cryptocurrency. Of course, the same is true for on-chain data.

This week, we explore how macroeconomic trends will impact the cryptocurrency market in 2025.

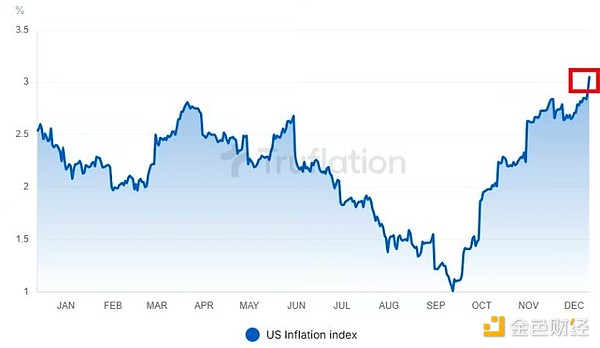

InflationInflation data are rising. After bottoming at 1% in September, we have accelerated our recovery to over 3% on a Truflation basis.

Data: Truflation

We like Truflation's data because it uses real-time data from a variety of online sources Web scraping data. Additionally, it is updated more frequently than traditional indicators such as PCE.

However. The Fed's focus is on PCE. Therefore, we use PCE as a way to forecast the Fed and Truflation to get a more real-time view of the economy.

This is personal consumption expenditures:

Data: FRED database

Currently 2.3% (October data). is also rising – which is hard to see in the chart (2.1% in September). We will have November data on December 20th.

Views on Inflation

Energy costs and housing costs are the main drivers of growth. However, crude oil prices are at cycle lows.

Data:: Trading Economics

The question is whether they are here to stay, or whether they may fall further.

Given seasonal effects + Trump’s plans to increase supply through US deregulation, it’s hard to see why oil prices would surge any time soon.

On the other hand, geopolitical conflicts, unforeseen natural disasters, or OPEC production cuts in anticipation of increased U.S. supply could cause oil prices to rise.

We have not seen these events occur.

Furthermore, our position is that inflation in the 21st century has been driven primarily by supply shocks + fiscal spending and stimulus checks - which we do not view as a threat today.

As a result, we expect oil prices to be range-bound and inflation/growth to fall.

USDData: Trading View

Since OctoberBitcoin is up 58% since the 1st. Meanwhile, the U.S. dollar index rose from 100 to nearly 108. Today's ranking is 107.

This is a special behavior. Typically, a stronger dollar is detrimental to risk assets like Bitcoin (see 2022). But we now see a strong correlation between the two.

So what's going on? Should we be worried?

We believe the U.S. dollar is showing strength as global markets price in a Trump victory. Trump is good for business. This means they are good for the market.

We saw the same dynamic after Trump’s victory in 2016. The dollar rose. Why? We believe foreigners are digesting the impact of the “Trump Rump” and buying USD-denominated assets as a result.

Views on USD

We believe growth is slowing/normalising. This is lowering inflation, albeit with a delay. Interest rates may fall.

As a result, we expect the dollar to be range-bound over the medium term, possibly back towards 100.

ISM data (economic cycle)Data: MacroMicro

From the perspective of the economic cycle, we can see The blue line (manufacturing) appears to be bottoming out. Historically, a reading below 50 indicates the economy is in contraction. A sustained reading below 50 signals a slowdown.

This is where we are now - service (red line) is doing slightly better.

These levels tend to coincide with rising unemployment rates. This usually results in the Fed adopting easy money.

Again. That's exactly what we're seeing today.

Views on the economic cycle

We believe growth is slowing, leading to rising unemployment. This could ultimately manifest as downward pressure on inflation.

This leads to interest rate cuts. This puts downward pressure on the US dollar.

In the medium term, we believe these dynamics should support risk assets/cryptocurrencies.

Credit MarketsData: FRED

Credit spreads continue to be at historically low levels, suggesting investors are investing in additional Risk units have lower compensation requirements.

This could mean two things: 1) The market is complacent and risk is mispriced. Or 2) market participants are optimistic about the economy and the Fed and fiscal easing.

We think it is the latter.

Next let’s look at the trend of bank loans.

Data: Fred Database

Tightening lending standards since peaking at the end of 2023The proportion of banks has been declining. Ideally, this KPI will remain stable as the Fed cuts interest rates.

Having said that, historically we have seen an inverse correlation between interest rate cuts and the proportion of banks tightening lending standards. Why? Rate cuts often signal an economic slowdown or recession - making it harder for banks to lend.

Views on credit markets

No signs of stress. At least not yet.

Labor MarketThe unemployment rate rose to 4.2% in November (previously 4.1%). Below we can see the recent rise in jobless claims.

Data: Forex Factory

We believe that the weakness in the labor market has now captured the Fed's full attention. The continued rise in unemployment claims data tells us that for those who are out of work, finding work is becoming increasingly difficult.

This is another sign of slowing/normalizing growth. That being said, the stock market remains at all-time highs. Corporate profits are strong. This is what keeps the labor market intact.

But my sense is that the Fed is watching this like a hawk. After all, Sam's Rule was triggered in July.

Views on the labor market

It is softening. But it's not fast. We expect the Fed to (try to) act before the data weakens (as they already cut rates by 50 basis points in September after the July SAM data).

Treasury and fiscal expendituresData: U.S. Treasury

The United States spent 1.83 more than tax revenue this year Trillions of dollars. In November alone, it spent more than double its revenue.

The $1.83 trillion that has been printed and pushed into the economy/Americans has been a major driver of financial markets this year (and a major driver of inflation in our opinion).

Now. Trump is coming. We also have a new agency called DOGE, the Department of Efficiency, headed by Elon Musk.

Some believe excessive spending will be reduced as a result. Maybe it will. But which departments will be cut? Medicare/Social Security? army? interest?

That’s 65% of the budget – which seems untouchable.

Meanwhile, the Treasury must refinance more than a third of its debt next year. We don't think they can do that by raising interest rates.

Views on treasury/fiscal spending

We believe that significant cuts in fiscal spending are unlikely in the short term. DOGE could cut $10 billion in spending. But it won’t change the reality in a substantial wayshape. This will take some time.

Meanwhile, the Treasury will need to refinance a third of all outstanding debt next year. We think they'll do it at lower interest rates.

Combining these views, we are optimistic about the outlook for risk assets/cryptocurrencies.

FedThe next FOMC meeting will be held on December 18, and the market currently predicts a 97% chance of a rate cut. We think this may also give a green light for easing.

Why?

We believe that we hope to continue to implement easing. But when the Fed doesn't cut rates, it will be difficult for them to do so because the yuan will weaken against the dollar, making imported goods more expensive.

Views on the Federal Reserve

Raising interest rates in the short term seems unlikely. A rate cut in December is almost a certainty, with markets pricing in a pause at 76% in January. There is no FOMC meeting in February.

As a result, the next decision will not be made until March. We believe the labor market is now likely to show more signs of weakness, with the Fed likely to cut rates further in mid-to-late 2025 - ultimately to around 3.5%.

Will interest rate cuts increase inflation? We don’t think so – it’s a non-consensus view. In fact, we think rising interest rates are causing inflation (and other fiscal spending) to rise.

Why?

Because interest payments now exceed $1 trillion. The money is printed and passed on to Americans who hold bonds, and the money appears to be pumped into the economy. Of course, rising interest rates have not caused banks to stop lending (see chart above).

As a result, we believe inflation is likely to decline as the Fed cuts interest rates (assuming oil prices remain low and we do not see further increases in fiscal spending). Remember, we had zero interest rates for 10 years with low inflation. Japan has had 0% interest rates for 30 years and has a low inflation rate.

TrumpThe market knows what a Trump presidency will bring:

Lower taxes. This should boost corporate profits and potentially lead to a rise in share prices. It could also lead to increased income inequality and larger deficits. More deficits = more dollars in the hands of Americans.

Tariffs/"America First." This may lead to price increases. We think AI/automation may actually offset this to some extent.

Deregulation. This is good for business as it could lead to higher profits in the energy, technology and financial sectors.

Stronger borders. This can lead to labor shortages and rising wages (inflation).

Thoughts on TrumpWe think Trump is generally good for business, free markets and asset prices. The trade-off is that we may see some inflationary impulses. This is where things get interesting, because ifIf inflation returns, the Fed will seek to pause interest rate increases or tighten monetary policy.

Of course, we think Trump will try to impose his will on Jerome Powell. Ultimately, we think Trump wants to boost the economy and eliminate some of the debt through inflation over the next four years. This means that inflation must exceed nominal interest rates, but that is not the case today.

Finally, given Trump’s support for the digital asset industry (and the incoming SEC chairman), we think cryptocurrencies will benefit from his .

Not to mention the potential for favorable legislation from Congress and the strategic reserve of Bitcoin in the coming years.

Views on Trump

We believe that Trump will be beneficial to cryptocurrencies from a market and regulatory perspective.

Dan Tapiero (one of my favorite macro investors) says we are experiencing deflation (negative real interest rates).

Negative interest rates have dampened inflation concerns in the United States. This makes the dollar stronger (as we are seeing today).

A U.S. interest rate cut may make the U.S. also cut interest rates.

Ultimately, it will lead to more global liquidity.

Speaking of global liquidity.

Global LiquidityWith 1/3 of US debt needing to be refinanced over the next year, we believe the Fed may have to step in as the buyer of last resort (QE).

Lower interest rates in the United States will allow China and Europe to ease conditions in some coordinated way.

We believe this will result in ample liquidity/collateral within financial markets – with cryptocurrencies/risk assets being one of the biggest beneficiaries.

These dynamics are consistent with the fourth year of the crypto cycle—the most volatile upcycle in history.

SummaryGrowth is slowing.

This is causing labor market turmoil (and the Fed is watching).

This leads to interest rate cuts (as we are seeing today).

This allows China and Europe to ease conditions without sacrificing currency/imports.

This brings favorable liquidity conditions for risk assets.

This is the future we see.

Think of fiscal spending, an incoming Trump, and the fourth year of the cryptocurrency cycle, and you can predict explosive bull market conditions in 2025 (expect volatility).

Of course, we will continue to monitor the market and provide you with the latest information from an on-chain data + macroeconomic perspective.

After all, if you don’t understand the macroeconomic situation, you don’t understand your cryptocurrency.