55 mins ago

8,121

Author: Felix Jauvin, Blockworks; Compiled by: Whitewater, Golden Finance

As early as September, the market predicted one of the most aggressive interest rate cutting cycles I have ever seen, with multiple cuts of 50 basis points, which will quickly bring the federal funds rate to 3% in 2025. Fast forward to today and the picture is completely different, with only one or two rate cuts expected in 2025 at most.

Let’s take a deeper look at what’s driving this change and what to expect.

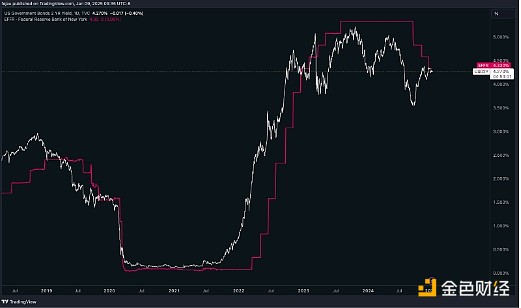

The chart below compares the effective federal funds rate (EFFR) to the two-year U.S. Treasury note.

By comparing these two yields, we can draw some conclusions:

In the past two years, we have seen many times that the two-year Rates are already pricing in an upcoming cycle of aggressive rate cuts (such as two-year rates falling below the EFFR).

For the first time since mid-2022, we see these two yields flat. That means the market is pricing in a rate-cutting cycle that's largely over, but it also doesn't see any possibility of a rate hike.

One of the drivers of talk of a quick end to this brief rate-cutting cycle is surprisingly stubborn inflation. As we saw in the December summary of economic forecasts, FOMC members have moved from a broadly balanced outlook on inflation to seeing risks skewed to the upside.

Coupled with the fact that the labor market is now proving to be more resilient and robust than when the FOMC began cutting interest rates in September, these factors are making the distribution of possible outcomes even more A hawkish-leaning monetary reaction function.

Put these factors together and you can see why there is growing confidence that the rate-cutting cycle is over.

Having said that, there are still dovish voices within the FOMC.

In his speech this week, Governor Waller mentioned that he still believes that a rate cut will occur this year: "So what is my view? If the outlook develops as I have described here, I will support a rate cut in Continue to lower our interest rates in 2025. The pace of rate cuts will depend on the progress we make on inflation while preventing a weakening of the labor market. ”

As in the past two years, the pace of rate cuts will depend on the progress we make on inflation. This year is shaping up to be another extreme year, with the market shifting from aggressive hawkish pricing to aggressive dovish pricing.

Investors need to decide quickly whether to try to ride these sentiment changes or ignore them as noise.