37 mins ago

5,821

Written by: Kedar@Foresight Ventures, Alice@Foresight Ventures

Contributor: Max Hamilton @Foresight Ventures

p>PayFi: The Transformative Power of Financial TransactionsIn today's world, cross-border payments often take days, and businesses are responsible for billions of dollars in transaction fees. PayFi emerged as an innovative solution that combines the advantages of decentralized finance (DeFi) with the immediacy of modern payment systems, and is expected to reshape the future of transactions.

As the global financial landscape continues to evolve, PayFi has emerged at the intersection of blockchain technology and payment systems, committed to combining the efficiency of DeFi with modern payment solutions The combination of immediacy and convenience changes the way of transactions. This article will delve into the reasons for the rise of PayFi, outline the current status of the industry in which it operates, list key cases, and explore its potential application scenarios.

1. The birth background and advantages of PayFi (1) Filling the gap between DeFi and paymentThe traditional financial system has long-term problems of low settlement efficiency, such as settlement time The length, high transaction costs, and limited accessibility were all exposed during the 2008 financial crisis. Although DeFi has introduced innovative financial services through decentralized platforms, it falls short in terms of real-time processing capabilities for daily transactions.

PayFi uses blockchain technology to achieve real-time settlement of transactions. Based on the time value of money (TVM) theory, that is, money currently available is more valuable than the same amount of money in the future because of its potential earning power. PayFi maximizes financial efficiency through instant, safe and low-cost transactions.

(2) PayFi’s unique advantagesReal-time settlement: transactions are completed instantly, eliminating the delay problem of the traditional banking system.

Safe and reliable: The non-tamperable ledger feature of the blockchain ensures safe and transparent transactions and provides protection for users.

Cost reduction: eliminate intermediate links, significantly reduce transaction costs, and save user expenses.

Globally accessible: Its decentralized platform reaches markets not fully covered by traditional financial services, including people without bank accounts, achieving inclusive financial services.

Innovative products: giving rise to novel financial service models such as "buy now, pay never", as well as innovative applications such as providing advanced monetization channels for creators.

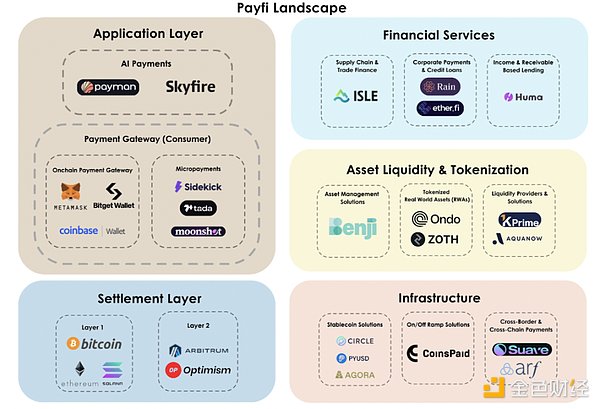

2. PayFi industry panorama and insights into subdivisionsThe PayFi ecosystem is booming, and various industries are actively innovating to respond to financial challenges. The following is an analysis of its key segments and examples of innovative companies in each field.

(1) Cross-chain and cross-border paymentStubborn problems of traditional cross-border payment

p>Slow speed and high latency: Traditional payment channels are inefficient, settlement often takes several days, and the settlement process across time zones and bank business hours is complex, exacerbating payment sluggishness.

Inefficiency of funds and constraints of pre-deposited funds: Pre-deposited funds require financial institutions to maintain foreign currency funds in current accounts, resulting in a global liquidity gap of US$4 trillion. , idle funds cannot generate income and become hidden costs for financial institutions and are passed on to end users, causing users to pay higher fees.

High transaction costs: Involving layers of fees from multiple intermediaries, including pre-deposited funds fees, currency exchange fees, etc., the average transaction cost of global cross-border remittances As high as 6.35% (World Bank statistics).

Industry Innovation Cases

Arf: Build a regulated global settlement banking platform to provide financial services Institutions provide on-chain liquidity solutions. Realize the instant and low-cost advantages of cross-border settlement with the help of stable currencies such as USDC, provide real-time liquidity for cross-border transactions on demand through the blockchain, and eliminate the dependence of current account accounts on large cash reserves; provide instant credit lines based on USDC , allowing financial institutions to temporarily borrow funds during transactions and repay them after payment is settled. Arf abandons the pre-deposited fund account model and uses USDC-based short-term liquidity solutions to effectively reduce capital requirements and settlement time, significantly reducing the operating costs of financial institutions engaged in global transactions. Pay attention to transparency and create complete traceable loan records. With the help of blockchain, all loan, repayment and receivable information can be easily traced. Adhere to the strict compliance concept as VQF financial services standardMembers of the association follow international standards on anti-money laundering and financial supervision and set an example for the industry. To date, more than $1.6 billion in on-chain transactions have been successfully processed, maintaining a zero-default record.

suave.money: Create a cross-chain payment solution that enables enterprises to receive cryptocurrency payments from any blockchain network, and enterprises can seamlessly connect with various agents. Pay with tokens and flexibly choose to receive your favorite tokens according to your own needs, improving payment flexibility in the blockchain ecosystem. suave.money's platform simplifies cross-chain transactions. Enterprises do not need to manage multiple wallets or rewrite decentralized applications (DApps), so they can attract user groups from different blockchain ecosystems and broaden their customer sources. By promoting payment convenience from more than 10 blockchain networks and enhancing liquidity acquisition capabilities, it provides strong support for the expansion of DeFi and Web3 projects and expands market coverage. Simplifying the cross-chain transaction process and reducing the complexity of enterprise operations enables enterprises to attract more customers in the blockchain ecosystem without relying on professional infrastructure construction, creating more opportunities for enterprise development. With its innovative capabilities, it helps companies tap into the trillion-dollar cross-chain capital potential, occupies an important position in the rapidly developing DeFi and crypto payment fields, and provides users with unparalleled flexibility and convenience.

(2) Lending based on income and receivablesThe dilemma of the traditional lending model: Traditional lending business relies on collateral and will lack the potential of large assets or credit records The exclusion of borrowers limits the inclusiveness and fairness of financial services.

The emergence of innovative solutions: Platforms such as Huma Finance allow users to borrow against future income or receivables, using blockchain technology to implement the lending process Transparency and efficiency.

Positive benefits: This innovative model significantly improves financial inclusion, provides new access to capital for underserved markets ignored by traditional financial institutions, and promotes Balanced economic development and social fairness and justice.

Huma Finance’s practical case: building a decentralized lending protocol to provide businesses and individuals with lending services based on future income and receivables. Connecting borrowers with global investors through an on-chain platform creates an income-supported lending model that is different from the traditional DeFi over-collateralization model. Partnering with Circle, Request Network, Superfluid and other platforms to launch the world’s first on-chain factoring market on Ethereum and Polygon, allowing users to tokenize invoices or payments for the first timeUse flows as collateral to broaden the scope and form of collateral. With the efficiency of blockchain, the on-chain processing time of the factoring process is shortened to less than one minute, providing users with a convenient experience. Huma Finance’s technical architecture consists of several key components. The decentralized income portfolio layer converts income sources such as invoices, payroll, and pledge income into tokenizable assets, providing a rich asset base for the lending business. The assessment agency framework is responsible for conducting accurate risk assessments of various types of lending needs to ensure that the credit quality on the chain is reliable and stable. The smart contract suite implements diversified lending use cases from invoice factoring to universal credit lines through configurable smart contracts to meet the personalized needs of different users. Huma Finance focuses on providing much-needed liquidity support to small and medium-sized enterprises and people without bank accounts. Through innovative lending models, it helps these groups break through traditional financial restrictions, obtain financial resources that are otherwise difficult to reach, promote their economic development and social integration, and build a Make positive contributions to a more equitable and inclusive financial ecosystem.

(3) Tokenization of real-world assetsDifficulties in traditional asset transactions: The transaction process of real-world assets such as real estate is cumbersome, the intermediate costs are high, and the transaction speed is slow. It brings inconvenience and financial burden to both buyers and sellers.

Innovative breakthrough in tokenization: Tokenize real estate and other real-world assets. Through smart contract technology, asset ownership can be divided into multiple parts. Realize partial ownership transactions while significantly accelerating transaction speed and processes, injecting new vitality into the asset trading market.

Significant advantages: This tokenization model significantly lowers the threshold for investors to enter the market, allowing more investors to participate in real-world asset investment, At the same time, it greatly improves asset liquidity, accelerates the asset buying and selling process, and enables market resources to be allocated and circulated more efficiently.

Ondo Finance’s successful practice: launching tokenized U.S. Treasury bonds and other income-generating products on the blockchain platform, opening up new investment channels for investors, This enables them to conveniently obtain short-term U.S. Treasury bonds and other fixed-income assets through decentralized finance (DeFi), achieving an organic integration of traditional financial markets and DeFi. Ondo Finance's innovative products provide investors with stable, profitable, liquid and safe investment options, breaking the barriers between traditional financial markets and DeFi, allowing more investors to share the dividends of the originally relatively closed capital market. , enrich investors’ asset allocation portfolios, and enhance the efficiency and vitality of the entire financial market. As of September 2024, Ondo Finance has achieved outstanding results in the field of tokenized U.S. Treasury bond products, with its total locked position value (TVL) has crossed the $600 million mark. Among them, the locked amount of USDY (interest-bearing stablecoin) reached US$384 million, and the locked amount of OUSG (tokenized US Treasury bonds) was US$221 million. These data fully prove the market's high recognition and widespread acceptance of its innovative products, highlighting its Leading position and strong influence in the field of real-world asset tokenization.

Zoth’s innovative contribution: building a market platform specifically for tokenized trade finance assets, providing investors with convenient access to U.S. dollar-denominated fixed income products way. By tokenizing assets in traditional financial fields such as trade receivables and corporate bonds, we build a bridge between traditional finance and decentralized finance (DeFi), creating high-yield, low-risk investment opportunities for investors, and at the same time Enterprises provide new financing channels and fund management methods. Zoth's platform plays an important role in the market, not only bringing high-quality investment options to investors, helping them achieve asset appreciation and preservation, but also providing strong support for corporate development. By tokenizing trade financing assets, companies can unlock working capital more efficiently, optimize capital structure, and improve their competitiveness and risk resistance. At the same time, this will help promote the optimal allocation of global market capital, promote a more reasonable flow of financial resources to companies and projects in need, further improve the on-chain trade finance ecosystem, and make a positive contribution to the stability and development of the entire financial market.

(4) Enterprise payment and credit solutionsConsumers’ new needs and limitations of traditional credit: In today’s consumer market, consumers require flexibility in payment methods They expect to enjoy a more convenient and diversified payment experience without shouldering a heavy debt burden. However, traditional credit models are often unable to meet this demand, causing inconvenience and economic pressure to consumers.

PayFi's innovative model: In response to this market demand, PayFi innovatively introduces unique payment models such as "Buy Now, Pay Never", through clever use of The interest income obtained from the DeFi lending platform offsets the purchase cost, providing consumers with a new, more flexible and debt-free payment solution, greatly enhancing consumer purchasing power and shopping experience.

Industry Innovation Case

Rain: Launching an enterprise card supported by USDC, targeting the Web3 team (Such as decentralized autonomous organization DAO and various protocol projects, etc.) Design of daily business payment requirements. With the help of this enterprise card, the Web3 team can easily use its on-chain assets (such as USDC) to pay for daily business expenses such as travel expenses and office supplies purchase expenses, without anyIt requires cumbersome conversion operations between cryptocurrency and legal currency, which greatly simplifies corporate payment processes and improves financial management efficiency. As an important part of its expenditure management platform, Rain's corporate card makes full use of the advantages of blockchain technology to achieve seamless integration of digital assets and traditional payment systems. Through this innovative payment method, enterprises can manage their finances more efficiently, reduce the cost and time consumption of intermediate links, and at the same time provide more convenient and secure payment solutions for enterprises in the blockchain and encryption fields, effectively promoting the development of the Web3 industry and the popularization of applications. .

Ether.fi: The launch of "Ether.fi Cash" product has attracted widespread attention in the market. This is a credit card that cooperates with Visa and has unique innovations. Function. After users hold the card, they can easily obtain a borrowing limit with their crypto assets (including various assets based on Ethereum) as collateral, so that they can consume legal currency without selling crypto assets, providing users with more flexible funds. Management style and consumption experience. In addition, the "Ether.fi Cash" credit card is deeply integrated with Ethereum's Layer 2 network Scroll. This technical advantage significantly reduces transaction costs and further improves user cost-effectiveness. At the same time, the card supports point-to-point USDC transfer functions, allowing users to transfer and manage funds more conveniently, meet payment needs in different scenarios, and bypass traditional bank intermediate links, saving users additional expenses. In addition, in order to improve users' enthusiasm and satisfaction, "Ether.fi Cash" credit card also provides an attractive cashback reward mechanism, which brings real economic benefits to users' consumption process and further enhances product market competitiveness and user satisfaction. viscosity.

Bitget Card: The launched Visa card serves as an important bridge between cryptocurrency and traditional payment systems, providing users with convenient and efficient payment solutions. The card is closely connected to the multi-currency wallet. Enterprise or individual users can conveniently hold, convert and use various mainstream cryptocurrencies in the wallet, such as USDT, BTC, ETH, USDC, BGB, etc. (Currently, fund accounts are mainly in USDT Mainly recharge, with plans to gradually introduce more cryptocurrencies in the future). During the actual payment process, Bitget Card can automatically convert cryptocurrency into legal currency based on real-time exchange rates, ensuring that users can successfully complete payments when spending money at any merchant that accepts Visa cards around the world, without having to worry about cumbersome currency exchange procedures and exchange rate fluctuations. Risk, truly realize the seamless connection between cryptocurrency and legal currency payment, providing users with great convenience. The emergence of Bitget Card has had an important impact on the corporate payment field. It not only simplifies the corporate payment process, but also eliminates the need for companies to manually handle complex cryptocurrencies and legal currencies.Through the conversion operation, traditional currency consumption can be used in real time, greatly improving payment efficiency and fund utilization efficiency. At the same time, its strong cross-border payment capabilities make it easier for companies to expand and operate international business without having to worry about opening and managing foreign currency accounts, effectively reducing corporate operating costs and financial risks. Currently, Bitget Card has been widely accepted and recognized in more than 180 countries and regions around the world, providing strong support for the global development of enterprises. In addition, Bitget Card also has rich potential DeFi Use cases, such as supplier payment, companies can directly use the card to pay suppliers in fiat currency, avoiding the tedious process of manually converting cryptocurrencies, improving supply chain payment efficiency and stability; in terms of travel expense reimbursement, employees can rely on this card The card can easily make business-related consumption payments during cross-border travel, such as air ticket bookings, hotel accommodations, etc., without worrying about payment restrictions and handling fees, and provides a more convenient payment solution for corporate cross-border business activities; in terms of corporate reward mechanisms, companies You can also use Bitget Card The cryptocurrency payment function provided provides employees with cryptocurrency-based rewards. Employees can convert cryptocurrency into legal currency for consumption according to their own needs, or directly use it in scenarios that support cryptocurrency payment, creating an incentive and welfare system for corporate employees. Bring more innovation and flexibility, further enhance the competitiveness and attractiveness of enterprises.

(5) Supply chain and trade financeThe dilemma of traditional supply chain finance: In the traditional supply chain finance system, suppliers often face long and complex payment cycles. A large amount of funds are locked up for a long time, which seriously restricts its operational efficiency and capital turnover capabilities, making it difficult to maintain normal production and operation activities and business expansion. According to statistics, global enterprises have up to US$2.5 trillion in trade financing needs that cannot be effectively met every year due to the limitations of traditional financial institutions. This has become a bottleneck for global trade development and hinders the coordinated development of industrial chains and stable economic growth.

PayFi's solution: PayFi provides innovative solutions to the invoice financing problem in supply chain finance by introducing a decentralized platform. Under this model, suppliers can use the advantages of blockchain technology to tokenize their invoices and quickly achieve financing on a decentralized platform, obtain immediate financial support, and greatly improve capital liquidity. At the same time, buyers can continue to settle according to the original payment plan without changing traditional payment habits and financial processes, achieving a balanced and coordinated development of interests between buyers and sellers, and providing a strong guarantee for the efficient operation of supply chain finance.

Industry Innovation Cases

Isle Finance: Deeply engaged in the field of supply chain finance on the chainThe credit market has built a platform that can accurately connect high-credit buyers with liquidity providers, thereby helping companies obtain financing faster. It cleverly uses blockchain technology to greatly enhance the liquidity of the entire supply chain through rigorous verification of real-world assets (RWAs) and implementation of early payment strategies for buyers, especially those suppliers with low credit ratings. and security, laying a solid foundation for the stable development of supply chain finance. Isle Finance uses its own platform to vigorously promote the development of reverse factoring business, which not only significantly speeds up the company's payment speed, but also greatly optimizes the cash flow situation. This innovative solution based on blockchain allows companies to flexibly provide early payment discounts, creating extremely stable and considerable returns in the field of supply chain finance. It also broadens the channels for companies to obtain liquidity and provides them with sustainable Inject strong impetus into development.

(6) Stable currency payment platformExample: Agora

Business content: carefully built The U.S. Digital Dollar (AUSD) is fully backed by cash, U.S. Treasuries, and overnight repurchase agreements. The platform is dedicated to using blockchain technology to enable broader and more convenient circulation of U.S. dollars around the world, with a special focus on areas underserved by the traditional financial system. It fully implements the concept of financial inclusion and opens up a path for the public. A new way to gain easier access to stable, globally recognized currencies.

Impact: Powerful push to democratize access to U.S. dollars, highly aligned with PayFi’s ambitious vision to expand financial inclusion. It gives full play to the technical advantages of blockchain and builds a decentralized and easy-to-access financial system, allowing individuals and enterprises to benefit from U.S. dollar-backed financial instruments. The results are particularly significant in Argentina, Southeast Asia and other regions. It provides strong support for local economic development and financial stability.

Achievements: Successfully brought the stablecoin AUSD to the market, initially issued on Ethereum and later expanded to the Avalanche network. Remarkably, mintage surpassed $20 million within just a few weeks of release. Today, the platform is steadily advancing the global layout of its digital dollar, continuing to expand the international market, while always adhering to the development strategy of financial inclusion and regulatory compliance, and gradually establishing a good reputation and influence in the stablecoin field.

Example: PayPal

Business content: In August 2024PayPal USD (PYUSD) was officially launched, first launched on the Ethereum blockchain, and then successfully expanded to Solana in May 2024. The original design intention of this stablecoin is to fully integrate the advantages of the two blockchains and strive to achieve a fast and low-cost digital payment experience. Especially after expanding to Solana, with its excellent transaction speed and low fee advantages, the usability of PYUSD in various commercial and DeFi application scenarios has been greatly improved, providing users with more efficient and convenient payment options.

Impact: It is expected to become a powerful alternative to traditional payment systems with its fast and cost-effective characteristics, thereby significantly improving global payment efficiency. It successfully implements seamless transfer functions across different platforms (covering PayPal and Venmo, etc.), allowing users to easily hold and transfer stablecoins, and fully utilizes the technical advantages of blockchain to manage and pay transactions for users’ digital assets Bringing more convenience and innovative experience.

Achievements: After expanding to Solana, PYUSD's market adoption has shown rapid growth, with its market value rising rapidly and successfully surpassing the $500 million mark. This remarkable achievement fully demonstrates its deep integration and widespread recognition in centralized and decentralized platforms. It also marks a major victory for PayPal in its exploration of stablecoins, setting the stage for its future development in the field of digital payments. A solid foundation has been laid for further development.

Example: Bridge (acquired by Stripe)

Business content: Bridge as a company focused on The stablecoin payment platform always takes simplifying cross-border digital payments as its core goal. Through convenient API interfaces, it can easily realize stablecoin-based payment integration and provide global users with low-cost and efficient cross-border transaction solutions. Before being acquired by Stripe, Bridge had already achieved remarkable results in e-commerce platform integration, successfully helping merchants to seamlessly connect and efficiently process stablecoin payment services in any corner of the world, greatly expanding the use of stablecoins in the commercial field. Application scope.

Impact: Recently acquired by the US payment giant Stripe, this major event is undoubtedly a key milestone for the integration of stablecoins into mainstream financial services. With the help of Stripe's powerful infrastructure and extensive market network, Bridge can further expand its business coverage and comprehensively improve its capabilities, committed to providing global enterprises with more convenient, efficient and stable services.Fixed currency payment and settlement services. This move is highly consistent with PayFi’s grand vision to promote the global adoption of digital currencies by promoting financial inclusion and seamless cross-border transactions. It is expected to leverage Stripe’s existing advantages and Bridge’s stablecoin technology expertise to accelerate blockchain-supported payments. The widespread application and deep integration of payment methods in mainstream financial channels has injected new vitality into the innovative development of global financial payment fields.

Achievements: In August 2024, Bridge's payment volume annualized run rate successfully exceeded US$5 billion, a remarkable achievement. During its development, Bridge has established close cooperative relationships with many industry-leading companies, such as Coinbase and SpaceX, and is still providing high-quality payment services to these companies today, and has accumulated rich practical experience and experience in the field of stable currency payment. A good market reputation has become one of the important forces driving the development of the industry.

ConclusionOverall, PayFi is not a new concept. The problems it aims to solve already exist in the traditional financial system, and there are corresponding solutions. But that doesn’t mean PayFi is worthless, as traditional solutions still fall short. By solving core inefficiencies in the global payments system and harnessing the transformative potential of blockchain, PayFi has the potential to unlock unprecedented liquidity and drive financial inclusion. As more and more companies innovate in this space, the vision of a fully decentralized financial ecosystem where payments are instant, secure, and borderless is getting closer to reality. Now is the time to embrace PayFi’s transformation and shape the future of global finance.