2 mins ago

1,408

Author: NingNing

In early February, altcoins in CEX and AI Agent/MeMe on the chain The currency experienced a terrible pullback. Everyone has a question in their minds: Where has liquidity (AKA, money) gone?

The answer may be simpler than you think - chasing certain benefits .

When the high FDV/low market value altcoins in CEX keep unlocking and smashing the market or shipping OTC, and when the P player on the chain is rolled into a red ocean, the funds are I am tired of the stupid game with high odds and low winning rates, and start looking for passive returns with certainty and compound interest effects.

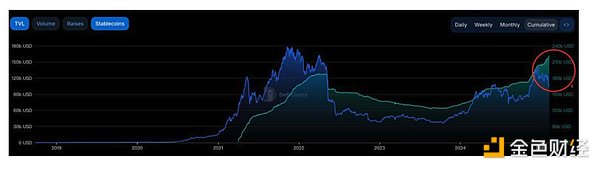

In the past 25 years, the growth slope of stablecoin scale has become steep, but the TVL in the entire market has As a result, the PayFi track raised its head in the winter dullness (Winter Mute).

Like other cutting-edge narratives, the conceptual extension of PayFi is in rheological iteration, from the original "Buy First, Never Pay" payment process paradigm, Evolved into a solution to the payment financing scenario defined by Messari. Behind this change is the evolution of industry strategy thinking from narrative to majorism to cost reduction and efficiency pragmatism.

Let's first look at a set of cross-border payment industry data:

Global prepaid accounts lock funds :$4 trillion

Cross-border payment fee: average 7%

Closing cycle: 2 -3 days

Population without bank account: 1.4 billion

It can be seen that cross-border The payment industry has serious problems with high costs and inefficiency. The root of the problem is the structural flaw of the traditional financial system.

In the past decade, we have witnessed three waves of decentralized financial innovation in the ICO, DeFi, and http://Pump.fun paradigm launch platforms, each wave is subverting the asset issuance and trading paradigm of traditional finance.

PayFi is doing something similar, trying to restructure the entire infrastructure for payment financing. This includes:

Real-time settlement (T+0) instead of T+2

Program How to use credit instead of manual review

Composibility instead of closed systems

PayFi What about achieving the above goals?

Huma Finance, a pioneer in PayFi track, gives a transaction layer, currency layer, custody layer, compliance layer, financing layer, and application layer. Standard paradigm:

1. Transaction Layer

This is the foundation of the entire system. Mainly dominated by two public chains:

Solana: 65,000 TPS, sub-second confirmation, the fee is as low as USD 0.0024

Stellar: 5 seconds confirmation, the fee is about 0.00005 USD

Why do these two chains dominate PayFi? Because they solve the three payments Core requirements: high throughput, low latency, and controllable costs.

2. Currency Layer

This layer is mainly composed of stablecoins. USDC plays a central role here. Interestingly, USDC's market value accounts for 22%, and transaction volume accounts for 55%. USDC is becoming a "payment-level" stablecoin, while USDT is more of a "store-value-level" stablecoin.

3. Custody Layer

This is probably the most underestimated layer. It solves a key problem: how to be safe

Main players include: Fireblocks, Copper, Cobo.

What they provide is not only "custody", but a complete fund operation framework.

4. Compliance Layer

Talking about compliance in the crypto world seems to be It's a bit out of place, but this is precisely the key to distinguish PayFi from traditional DeFi. The core functions include: KYC/AML integration, transaction monitoring, risk assessment, and compliance reporting.

5. Financing Layer

This is the most innovative in the entire architecture The sexual part. It realizes things that are impossible in traditional finance:

Programmed Credit Evaluation

Real-time risk pricing

Automatic clearing

Huma's innovation at this level is particularly worthy of attention:

Income pledge model

Dynamic credit limit

Intelligent fund pool management

6. Application layer

This is a layer that is directly targeted to users, including:

Payment applications (Helio, etc.)

Cross-border remittance (Bitso x Felix)

Enterprise payment (Rain)

Small WeChat Credit (Jia)< /p>

The market value of stablecoins increased by 57% in 2024 to US$204 billion. Meanwhile, Huma and Arf's monthly payment financing increased from $63 million to $136 million, showing a strong growth trend related to market volatility.

I personally have an optimistic accelerator attitude towards PayFi. It is neither the End Game of Finance nor the short-lived narrative, but a " Destructive innovation experiment.

And history tells us: those who bet on "destructive innovation" and insist on long-termism often win more than band masters and on-chain bet dogs.

Which from what I have learned, Huma Finance will be TGE this year. Before that, the only way for ordinary investors to bet on PayFi's "destructive innovation" was to deposit money from the payment financing lending pool deployed by Huma Finance on the Solana chain.

In order to lower the threshold for user participation, Huma Finance lowered the minimum deposit amount from 1000U to 100U and introduced a maximum of 7 times the points Boost mechanism. Currently, the stablecoin income in the second phase of the activity is 13% to 20%. Adding the potential points airdrop reward, the APY will be higher. If you participate now, you can get an OG LP Status reward and enjoy a permanent APY Boost benefit.

The current 6-month lock-up period is full, and there are 3 lock-up periods There are still a few vacancies in the month. If you miss this wealth train, don’t worry, Huma Finance will open a new quota in late February.

In the current market environment full of uncertainty, Bitcoin options worth $10 billion (maximum pain point $85,000) expire on March 28. Embrace stablecoin financial management with real income + potential airdrop increaseInvestment opportunities that rate critical hits may be one of the best strategies.