43 mins ago

2,269

Author: Victor Ramirez Source: coinmetrics Translation: Shan Oppa, Golden Finance

Key takeaways:In South Korea During the brief period of turbulence, the phenomenon of "kimchi premium" re-emerged, which is the common name for the price misalignment between the Korean market and the global market. As a result, Bitcoin is trading close to $115,000.

Cryptocurrency trading exhibits strong seasonal market and on-chain activity across exchanges and assets.

On-chain activity has grown significantly since the start of the year, especially for currencies traded primarily in Asia and which have been the target of U.S. Securities and Exchange Commission enforcement actions.

IntroductionBroadly speaking, cryptocurrencies are touted as a borderless, 24/7/365 market. While the underlying technology is indeed independent of where you are in the world, individual markets are sensitive to seasonal patterns, idiosyncrasies of regulatory regimes, and various human preferences around the world.

In this article we explore seasonal and geographical patterns in cryptocurrency trading activity. We will take the Korean market as an example. Using time zone data, we can observe localized effects across multiple cryptocurrency exchanges and assets. Finally, we will provide the latest news on activity on various altcoin chains.

Capital controls lead to pickle premiumAn interesting case study is the special market behavior that occurs in a specific region, which is widely known as the "pickle premium". The kimchi premium refers to the difference between the price of a digital asset traded in the Korean market and the global “reference” price. The pickle premium is primarily due to high demand for crypto-assets in closed market environments, as well as years of strict regulation that have made these markets less efficient due to difficulties in international arbitrage.

While this may represent an obvious arbitrage trade, local regulations make it difficult for foreigners and institutional investors to profit from it. Capital controls on the South Korean won limit the movement of fiat currency into and out of South Korean exchanges. By law, only Korean or foreign residents holding a resident registration card can trade through Korean exchanges. At the same time, compared with exchanges, South Korea's foreign exchange exchanges face stricter controls. In order for Koreans to trade cryptocurrency on a foreign exchange exchange, they must first buy it from the exchange and then transfer it out to the foreign exchange exchange. Together, these constraints limit the paths through which capital can move through the system.

Finally, bank channels make for a slow response to any arbitrage opportunities. Moving funds from a bank to an exchange can take hours, sometimes up to a day, at which point the arbitrage opportunity disappears.

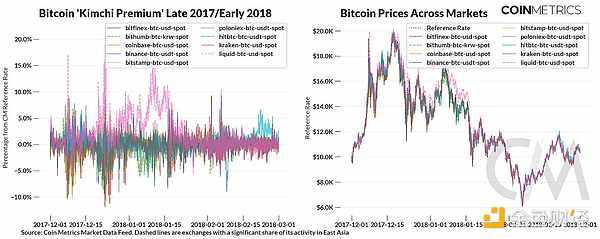

The pickle premium is well documented in the history of cryptocurrencies and began to gain traction in late 2017.

Source: Coin Metrics market data p>

The pickle premium persisted during the peak of the 2017-2018 bull market. The market volume was very thin at the time, resulting in wide spreads. Notably, FTX's sister. Trading firm Alameda Research from 2017 began exploiting this regulatory arbitrage and became one of the largest cryptocurrency trading companies at its peak

Source: Coin Metrics market data

in 2021 During the bull market of 2020, we were again able to observe persistence of the kimchi premium, albeit to a lesser extent and with less frequency. Korean exchange Upbit’s KRW-Bitcoin market fluctuated frequently, culminating in a flash crash of 12.5 in May 2021. %.

Source: Coin Metrics Market Data

As the market has generally grown over time, the pickle premium phenomenon has Basically gone, with some exceptions. The kimchi premium phenomenon even pushed Bitcoin prices above $100,000 in some Korean markets, less than two weeks after global prices converged to $100,000.At 1:27 pm UTC on the 3rd, South Korean President Yoon Seok-yeol declared martial law, resuming the premium phenomenon again. According to Coin Metrics’ 1-minute reference rate, premiums have increased by up to 20%. At its peak, the premium pushed Bitcoin’s price to nearly $115,000.

Although the "kimchi premium" phenomenon is now well-known, strict capital controls make it difficult for overseas investors to participate in the Korean market. This leaves the market vulnerable to liquidity shocks, which can trigger price instability.

Cryptocurrency trading exhibits strong seasonal behavior Seasonality of cryptocurrency exchangesDespite the fact that the blockchain itself is permissionless, cryptocurrency exchanges are still the vast majority A necessary intermediary for most market participants. Although the cryptocurrency market is global, each exchange must comply with local regulations in order to serve a given user base. Given the varying levels of regulation around the world, it’s common for cryptocurrency exchanges to have trading activity concentrated in a few geographical areas. Few exchanges are truly borderless.

We can use this knowledge of local legal restrictions, as well as known user preferences in specific regions and metrics derived from market data, to understand where trading activity is Distribution around the world. The chart below shows the share of trading activity on specific exchanges in different time zones.

Each row represents an exchange, and each column represents that exchange's spot trading volume during peak hours in a certain time zone: 9 a.m. to 5 p.m. The value of each cell is the ratio of the exchange's average trading volume in a given time zone to its average hourly trading volume. The last column is the average hourly trading volume for each exchange. For example, Binance’s trading volume during the East Asian session was 12.1% lower than its average of $802 million, but its trading volume during the European session increased by 19.4%.

Source: Coin Metrics Market Data

As expected, we see Korean exchanges Bithumb and Volume indices for Upbit and Japanese exchanges Bitbank and Bitflyer trend toward the East Asian session. Upbit is only available in East Asian markets such as South Korea and Singapore. In fact, in the United States, anyIt is illegal for anyone to trade on Upbit. Assuming that trading activity from Upbit users from outside East Asia is negligible, we can use trading activity occurring outside of East Asia hours as a baseline for off-peak trading activity.

Due to overlapping European and US time zones, it is difficult to distinguish activity in specific regions, but there are still clearly observable patterns in trading activity. Even though Kraken is a US exchange, it sees slightly more activity during the EU session than the US session.

Overall, we do still see an over-reliance on U.S. trading hours on most exchanges. Coinbase, Gemini, and Crypto.com have the largest preference for U.S. trading hours, at 36.1%, 57.3%, and 37.1%, respectively. Interestingly, Bullish is not legal in the US but shows a strong preference for US/ET (38.6%).

Seasonality of asset transactions< p style="text-align: center;">Source: Coin Metrics market dataWe can analyze the assets of all exchanges The same approach applies to trading volume. Similar to the exchange segment, most asset trading activity still occurs during the EU/US session. Bitcoin, ETH and USDC special indices are aligned with the US session.

Ripple, Tron, Stellar, and Cardano performed better during the East Asian session compared to other currencies. South Koreans have shown strong interest in XRP, while Tether on Tron is the most widely used stablecoin in Asia.

Time zone analysis is obviously limited by longitude, so we can't rely solely on it. This is when we rely on known user preferences. Bitso’s “Latin America’s Cryptocurrency Landscape” and “Stablecoins: Stories from Emerging Markets” show that Latin Americans have a strong preference for stablecoins, especially Tether, which provides an attractive and stable alternative to inflationary monetary systems plan. Tether, on the other hand, has come under scrutiny from U.S. regulators for its solvency, although it remains compliant and still serving U.S. users. While we see USDT activity concentrated during the US session,Its trading volume in the region may come more from South America than North America.

We can go one step further and view the transfer value of the asset directly on the chain.

Source: Coin Metrics Network Data Pro

The results in the above table are consistent with what we know from SOTN #165 to the same situation as in SOTN #165 , we see that the on-chain activities of several assets show different bands. On-chain transfer values for Bitcoin, Ethereum and USDC are skewed towards the EU/US session, consistent with trading volume.

Tether's on-chain activity is slightly different from its off-chain activity. USDT’s on-chain activity peaked significantly during the EU session at +46.4%, while exchange off-chain activity was at +17.8%. During the US session, Tether saw a +15.5% deviation when trading on exchanges, but a -5.6% deviation when it came to on-chain activity.

This is consistent with the regional differences in stablecoin preference we observed in SOTN #220. A similar heat map broken down by hour can be found on our stablecoin dashboard stablecoins.coinmetrics.io.

Party Like 2017/21The 2017 and 2021 “dinosaur” coins have seen significant price increases in recent weeks. XRP, TRX, ADA, and XLM prices have performed quite well, with the former rising 278% in the past month. But does the price increase correspond to more on-chain activity?

We examined the on-chain metrics of these chains and compared them across different networks. Different blockchains account for transactions differently, so we normalized the on-chain metric using percentage growth through early 2024.

Source: Coin Metrics Network Data Pro

Overall, network activity is increasing across several chains. When measuring the number of transactions and active addresses, the Ripple (XRP) ledger saw the largest increase in activity. We also saw an increase in trading volume for Cardano (ADA) and Tron (TRX). It follows that there are some notable similarities between the assets with the largest increases in price and on-chain activity:

As we saw above, these tokens have experienced the largest increases in price and on-chain activity compared to Bitcoin and Ethereum. East Asia has strong regional preferences.

These tokens are called securities by the current U.S. Securities and Exchange Commission (SEC).

Traders may be pushing for Trump's blanket tolerance of cryptocurrencies, with recently appointed SEC commissioner Paul Atkins considered to be "short on cryptocurrencies." Friendly" attitude. Of course, the cryptocurrency industry viewed Gensler positively when he was first appointed.

ConclusionIn this issue, we highlighted how cryptocurrency markets perform differently around the world. Local regulations, such as those we see in South Korea, tightly control capital flows in the market, leading to price distortions. Time zone analysis can illuminate how markets express a preference for certain trading channels or assets in specific regions. Overall, the preferences shown by global market participants make up the global cryptocurrency economy. Understanding the nuances of each market around the world will help guide the continued global adoption of cryptocurrencies.