13 mins ago

1,455

Author: Andy (Twitter/X @hoidya_); Eureka Partners

TL;DR

1. What is the end of Defi, and why some projects are heading to a dead end?

The ending essence of Defi is the beginning of the next Defi. The ending of most projects towards a dead end is only in line with the natural life cycle of the plate, achieving their respective main factors of collapse, and other projects undertake their liquidity. From a high-dimensional perspective, the entire Web3 industry is still "permanent", which shows that the relationship between disks and disks built by the Web3 ecosystem is in line with a healthy ecosystem. By observing various ecology, projects, and protocols with this logic, we can find that their life cycle will become shorter and shorter as the dimension is lower, which is a reasonable phenomenon. Therefore, the "turnover rate" of the plate represents the health of the project, and the "turnover rate" of the project represents the health of the ecosystem. Next time, don’t say “no one takes over” hastily. You should take a closer look at every project’s reverse card, and abstractly decouple business logic, and no longer be fooled by those seemingly high-end concepts.

2. Can Berachain achieve "never end"?

Berachain's main collapse point is: BGT pledge income

3. Defi liquidity game: Does Berachain essentially change anything?

Is Berachain a technical bottleneck that essentially breaks through the liquidity market? The answer is obvious, no, it is just a part of the improvement. But Berachain chose the right application scenario - public chain. If we only focus on the mechanism, it will be wrong. The judgment of this potential is only at the agreement level, but the actual bribery reward of the BGT token is to revitalize other ecological projects, and can even be regarded as a big narrative of the same level of Restaking.

4. What is happening with Berachain and what is the best way for users to participate?

The author observed 103 projects and summarized the following characteristics of Berachain:

Project native Strong, GTM strategies are different: most projects deployed in Bera are not multi-chain compatible, but are native to Berachain. The ratio of native projects to non-native projects is about 10:1 (Note: It is not ruled out that some products are the same Team origin). Contrary to intuition, not all non-NFT native projects tend to issue NFTs as cold starts, and most of them are still halal.

Economic flywheels are all different, and they will never leave their roots: Most of the projects deployed in Berachain realize economic flywheels through Infrared, and at the same time, projects further build multi-layer VE (3,3) based on the original BEX , for example, Berodrome. But the core idea remains unchanged, and any incentive is a currency-based one, so users only need to clarify the fundamentals of the project behind the token + market-making capabilities. The flywheel between the project should be coupled, but not The flywheel effect representing the project will collapse due to the collapse of a single project. As long as the ceded tokens are ensured to exchange for excess returns, the user is willing to continue to protect the plate and allow other projects to fill the gap in the flywheel.

Most high-financing projects issue NFT: Among the top 10 financing projects, 7 are Community/NFT/Gamefi, and all issue NFTs.

Community hot spots, but hot to each other: the average number of viewers on the native Berachain ecological project is 1,000 -2000+ people, some project parties are underestimated in the number of readers (number of followers/number of readings for draws < ecological average). For example, Infrared has 7,000+ followers, and the average number of post viewers is 10,000+; many native ecological projects will cooperate with each other, and the cooperation forms are relatively diverse, such as participating in economic flywheels, ceding tokens, etc.

The project is still innovating, but it is not a subversive narrative: in the NFT track, some project parties choose to use BD capabilities In exchange for user attention, rather than brag about the effectiveness, such as HoneyComb, Booga Beras. In the Defi track, some project parties continue to study liquidity solutions, such as Aori, and some project parties try to optimize past VE(3,3) models, such as Beradrome. In the Social track, some project parties try to review the quality of ecological projects through Peer to peer, such as Standard & Paws. In the Launchpad track, some project parties try to implement Fair Launch in the form of token equity cutting and LP allocation, such as Ramen and Honeypot. In the Ponzi/Meme track, some projects tried to achieve a "sustainable economy" by Floor price pool, such as Goldilocks.

5. Where should Berachain's explosion point be? What ecosystem is potential stock?

The author believes that LSDFI and Ticoin assets are the outbreak of Berachain point. The former builds more diverse economic flywheels, creating a larger economic bubble & seat belt for Berachain. The latter splits more liquidity for the project party and gains more users by participating in the ecological flywheel.

#1 Introduction

After experiencing Berachain's products some time ago, I communicated with several friends about product experience and project development judgments. The following are a few core views heard:

Berachain POL mechanism is strictly not innovative, but will also improve The threshold for user participation, but it does not affect the mood of early users.

Berachain's rise and fall is reflected in single currency, not the "three currency model".

Berachain's NFT is the shovel, not the currency.

Berachain is the end of Defi.

The views of the first three are not painful, but only the fourth point I have reserved, and I hope to leave more for Defi Imagine space, not bound by an ecological prosperous Tang Dynasty. The author does not want to be groundless, so he wrote this article and left it to the readers to decide.

#2 What is the ending of Defi?

Why do some projects go to a dead end?

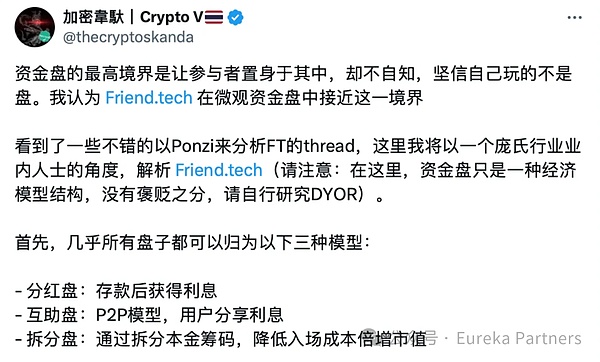

First of all, we need to reach a consensus on the nature of Defi, that is, Defi is a plate - a plate that repeats itself over and over again. If the plate is only roughly understood as "new money is covered with old money", some of the hubs that Defi has really started will be ignored. The author believes that the understanding of the plate @thecryptoskanda's three-plate theory has good reference value.

https://x.com/thecryptoskanda/status/ 1702031541302706539

Three plates refer to:

Diployment plate: Obtained after depositing Interest, such as Bitcoin mining, Ethereum POS, and LP income.

Mutual aid disk: P2P model, the focus is on flow mismatch, such as meme.

Split the plate: reduce entry costs and double the market value by splitting principal chips, such as Ethereum ICO.

The following sorts out the main factors of crashing in different plates:

p>

The life cycle of an ordinary plate is inevitably a death spiral and does not take over, but the life cycle of a good plate is repeated, and may be caused by different plates Combined and serialized together, like an Ourobosnake. Therefore, understanding a project should be a "modular" understanding and disassembled according to the category of the plate. Otherwise, after the narrative period Fomo ends, the future trend of the project may be misunderstood.

The so-called one gives birth to two, two gives birth to three, and three gives birth to all things. The three-disk theory does not limit the "three-disk", but the coupling relationship between disks, which truly achieves endless vitality.

The author briefly explains what cases will be found in different combination disks:

Dip first-then dividends: LRT. The user's ETH will be pledged to POS (get the first layer dividend income), and then authorized to AVS (get the second layer dividend income).

Divid first-and-mutual assistance: point-to-pool lending agreement. Users first pledge tokens to obtain initial collateral income, and then other Borrowers lend out collateral to increase the user's collateral income.

Divid dividends first-split later: ICO on the POS chain. Participate in the P2P network with native tokens, receive block rewards, and deploy non-native/copy token contracts on the network , capture the liquidity of other users.

Mutual assistance first-and then dividends: OHM/Reserve Currency. OHM theory anchoring At $1, after purchasing at a premium, the remaining pledges can get more dividends.

Mutual assistance first-after Mutual assistance: mixed lending. Borrowers can prioritize point-to-point Lenders, if liquidity is insufficient, then point-to-pool Lenders.

Mutual assistance first - then split: Runestone. Users hype Runestone first, and then Runestone holders can get airdrops for each project.

Split first - then dividends: Non-native interest-generated assets on the chain. Non-native assets are generated from ICO and dividends are paid in other tokens/native tokens.

Split first-and then mutual assistance: frend.tech. Users can set up new targets with low thresholds, and then they will still meet the new money and cover old money.

Split first-split later: Bong Bears. Bong Bears is an NFT that continues to re-base multiple rounds. Bong Bears is born Bond Bears, Bond Bears is born Boo Bears …. Then there are Baby Bears and Band Bears.

Yes It is obvious that the above combination and judgment of different disks are relatively subjective. From the actual situation, a project may containThe plate combination is not limited to 1-2 types, but may be as many as 4-5 types. But is it certainly better if there is too much? This is related to the allocation resources of a project, or to be straightforward - trading ability. The allocable resources also determine how the relationship between disks can be handled, that is, parallel or serial (referring to the concept of computer thread processing here).

Parallel: The relationship between different disks in a project's business does not conflict with each other, and multiple logics can be implemented separately. For example, there are no necessary business coupling between the protocols in which the public chain ecosystem is flourishing.

Serial: The relationship between different disks in a project's business may conflict, and the business logic needs to be sequenced. For example, the LRT protocol logic is used in serial processing, and the user's ETH will be pledged to POS first, and then authorized to AVS to obtain two layers of profits.

After understanding the essence of Defi, let's return to the question: What is the end of Defi, and why some projects are heading to a dead end?

The ending essence of Defi is the beginning of the next Defi. The ending of most projects towards a dead end is only in line with the natural life cycle of the plate, achieving their respective main factors of collapse, and other projects undertake their liquidity. From a high-dimensional perspective, the entire Web3 industry is still "permanent", which shows that the relationship between disks and disks built by the Web3 ecosystem is in line with a healthy ecosystem. By observing various ecology, projects, and protocols with this logic, we can find that their life cycle will become shorter and shorter as the dimension is lower, which is a reasonable phenomenon. Therefore, the "turnover rate" of the plate represents the health of the project, and the "turnover rate" of the project represents the health of the ecosystem. Next time, don’t say “no one takes over” hastily. You should take a closer look at every project’s reverse card, and abstractly decouple business logic, and no longer be fooled by those seemingly high-end concepts.

Does this mean that Meme is the healthiest? After all, the starting price is low and the project turnover rate is also high. From this understanding, technological breakthroughs are not important. As long as someone recognizes this narrative, they can continue. Is this really the case?

If the dimension is placed only in the Meme track, then the continuous stream of new and old plates can be understood as healthy operation But if we mention the dimension to the entire public chain ecosystem, only the Meme track can continue to grow, this is trueCan this public chain be healthy? I believe you also find it a little weird. Although in a practical sense, we often see the popularity of a certain track, and we jokingly say that the xx chain is about to rise and regard its popularity as a sufficient and unnecessary condition, but with a little thought, This kind of explosion may usher in a sudden drop in other ecological liquidity of a chain, and even strongly bound the fate of the native chain coin price to a certain track. This is not what most chain-making projects hope to see一 (Appchain is not considered here), so in most cases, the popularity of a certain track should be a necessary and insufficient condition, that is, the traffic of a certain track cannot infer the development of the entire chain, and the trend of the chain should be reversed. Promote its ecological traffic.

#3 Can Berachain achieve "never end"?

After reading the above article, I believe many readers have begun a preliminary interpretation of Berachain. Let’s not rush to interpret the project first. Let’s take a step back and think about what is the core as a chain?

Right, liquidity. Mobility, as the nutrient for all things, determines the subsequent development of the ecology and also represents the degree of heat of the chain. In the past, the public chains of the halal factions ignored this focus and just engaged in marketing, trying to "take away liquidity" from other chains. What about? Without it, they are not prepared to consider how to better manage users' funds.

"Retain liquidity, isn't this the job of the project party? What should the public chain party do? We can only provide the best Develop a three-piece set, and the others must be created by the heavenly public beauty. "

Under the ideal state, public chains can also create some narratives , let the ecology take over these liquidity, but the magnitude is never the public chain level. At present, the most ideal liquidity narrative that can carry the public chain level is LRT+AVS, while other chains are always difficult to get out of the track-level narrative, and they will only Due to the development of a certain target, such as BTCL2 is limited by the outbreak of inscriptions and runes.

From this moment, we can reposition Berachain. The author believes that the best understanding of Berachain should be the "navigator of liquidity". Readers who are not familiar with Berachain can find many three-coin models + POL interpretations written by many colleagues on the Internet. The author will not bother to give it a brief introduction to Berachain's token model:

Three coins: BGT (governance), Bera (Gas), Honey (calculated stable)

Key process: BGT can be obtained in Berachain native applications (the main network may be released on more protocols in the future), BGT can be used to "boot" the BGT release amount of different LP pools; BGT is not transferable , but can be 1:1 to be used as Bera. Friends who are familiar with Defi can basically understand it as a variant of ve(3,3).

Note: BGT can only be obtained from the officially deployed protocols (BEX, BERPS, BEND), but after the main network is online, it will be open to all protocols deployed on Berachain.

The author believes that Berachain's token model should be viewed in combination with ecology, rather than hasty viewing as a product. Here, the author uses Berachain to explain the correct way with the three-disk theory. The process of developing towards the ecology:

Digital plate: User/ecological project party mortgages assets as LP, obtains BGT release income .

Split disk: BGT can be used to pledge it to become a governor, or authorize it to other governors; BGT governors Can determine the amount of BGT releases in different LP pools.

Mutual assistance disk: Ecological project parties provide bribery rewards to attract BGT governors , the ecological project party obtains potential more liquidity from higher BGT releases.

Split the disk: Users purchase tokens from different project parties from the LP pool.

Digital disk/split disk/mutual aid disk: Users The assets inflow and outflow from different ecological projects.

So the main collapse point of Berachain is: BGT pledge incomeIt is not difficult to find that this is a seesaw mechanism. When Bera/BGT has high implicit value, the potential anti-reform pressure of BGT will be very high. Once There are fewer BGT pledges, and the absolute return of BGT pledges should be higher at this time, which will push up the willingness of BGT pledges. The implicit value of Bera/BGT becomes lower, but when there are more pledges, the profit space will also be reduced, and Bera/ The implicit value of BGT has become higher again... After repeated cycles, the healthy Berachain ecosystem should maintain a positive premium for a long time, which means that the ecosystem has more transaction volume and should "be" be willing to pay more bribe rewards to give back to BGT pledgers. However, considering the actual situation, the amount of bribery reward for purchasing liquidity is not "dark forest". Rational project parties can refer to the bids of friendly competitors to set prices, or conspire to set prices to re-determine the attractiveness of liquidity by the free market. Finally, It will only return to a "market equilibrium" return average.

In addition, another hidden collapse point of Berachain is that the LP staking income is lower than that of other DEX self-organized LPs in the ecosystem, which means that users will do so due to "Vampire Attack" is lost. If you look at the actual situation, this problem is not big. There are two reasons:

Berachain Native DEX should have the most transactions Yes, it is also a small project that should choose cold start/IDO DEX, so in terms of user experience, it can provide the widest trading route without huge liquidity outflow.

Berachain The native DEX has the strongest brand power, and other DEXs are difficult to match. You can refer to Uniswap's rapid rebound after being attacked by Sushiswap's vampire, which shows the important impact of brand power on users' trading minds.

#4 Defi Liquidity Game

Did Berachain essentially change anything?

For Defi, even though the shapes are different, the core elements are still liquidity, so how to attract and distribute liquidity in the product structure becomes The measurement criteria for sustainable development are especially true for public chains. Below, the author will briefly review some liquidity solutions that have appeared in the past few years and compare whether Berachain's solution has essentially solved the liquidity problem.

Scheme 1: Liquidity mining

Subsidize only LPs with fee income with project native tokens. Suitable for early Defi, users have not been affected by the dazzling product model, this simple and effective subsidy helps quickly capture liquidity. The most classic case is Sushiswap's vampire attack on Uniswap, using LP mining subsidies $SUSHI tokens to capture $1.4 Billion liquidity in the short term. But the problem is also obvious. This dividend is not U-based, and the more liquidity, the less dividends it pays. Therefore, the tokens mined by early users will only quickly exit at the secondary level, which accelerates the possibility of the project collapse. Nansen's 2021 report has long pointed out that 42% of the LPs entered on the day of liquidity mining start-up withdrawal within 24 hours. About 16% of LPs exit within 48 hours, and by day three, 70% of users will exit. If it were today, this data would not be surprising. If it weren’t for a diamond player or a believer in the project party, who would be willing to run away?

Scheme 2: CLMM/Other AMM variants

Liquidity aggregation is carried out by changing the normal AMM (i.e. CPMM, constant product market maker) model. The most famous algorithm is CLMM, which is actually more similar toIt is a liquidity pool with countless independent different price ranges, which is seamless from the user experience. This approach is to achieve a balance between the order book and the CPMM, and to improve capital efficiency while ensuring sufficient liquidity to take over. For further explanation, readers can just look at Uniswap V3 or the V3 fork on the market. I won’t explain too much here. This kind of solution iteration will not harm the platform tokens, so basically everyone has one set.

Scheme 3: Dynamic distribution AMM

The liquidity range adjustment is carried out through passive/active methods, but its core idea is to ensure that liquidity reaches the highest capital efficiency. For more detailed contents of the plan, please refer to Maverick Protocol. It is similar to manually re-deployment of CLMM intervals. This approach allows users to experience lower slippage transactions, but the trade-off is to establish a "price buffer zone", and the potential cost of the project party in market value management will be higher (for example, it is more difficult to pull the market), so this Token pairs using dynamically distributed AMMs have high correlation, such as LST/ETH.

Scheme 4: VE model

Compare The classic VE model is proposed by Curve. After the user pledged the governance token, he can obtain some credentials, the masterpiece VE token, which can be used to determine the proportion of liquidity mining in different LP pools, that is, the dividend income of the governance token. In short, governance tokens can be used to determine the distribution of governance token releases in the LP pool. Because governance tokens can determine the allocation amount of liquidity mining, it has extended a project-guided liquidity, aiming to provide a deeper transaction depth to ensure sufficient liquidity to undertake it. Therefore, the project party is willing to provide more rewards for "election bribery". Most of the governors related to the project are rewarded with the project's native tokens. Early projects will choose to outsource bribery platforms, but more new solutions will now adopt built-in bribery modules.

Scheme 5: Reserve Currency/OHM imitation disk

Sell bonds at a discount to collect liquidity and issue stablecoins with this liquidity, because stablecoins should be anchored to US$1. Once there is an over-purchase, the remaining liquidity will be regarded as profit and distributed to the The pledger of stablecoins. In theory, this method can operate sustainably, but in realityInstead of treating these tokens as stablecoins, users choose to over-purchase the stablecoin and pledge it to obtain the treasury surplus income. Under the combination of pledge, securitization, and secondary market purchases, the value of the stablecoin will be pushed to a level far from reaching. If a huge profit-taking position is closed, there will only be further runs, and finally even return to a water level below US$1. The game situation of OHM is also called the (3,3) model. From the above, it can be found that users have chosen to stake, so it is expressed in a 3x3 matrix, which is (3,3).

Scheme VI: VE(3,3) model p>

Different from ordinary VE models, VE(3,3) pays more attention to local optimal consensus. Therefore, the project will create an environment to guide the coin holders who govern tokens to choose in the local optimal direction. The LP handling fee of the VE model mentioned above is actually a global dividend, that is, all governance token stakers have benefits. However, most of the LP fees of VE(3,3) only appear in the governors who vote for the pool. The pledgee needs to estimate the subsequent share of different LP fees before choosing to vote. So in a sense, the bribery platform also provides a local consensus that users can actively obtain the most profits. Therefore, whether it is the LP fee isolation or the bribery market, it further allows internal competition in the liquidity market and tries to attract liquidity in a "single-blind" situation, that is, it is impossible to determine how much liquidity the liquidity provider will provide. , this part is always opaque. In addition, the biggest difference between the bribery market and LP handling fee is the income pricing method. The former is denominated by the project token, while the latter is more common in the U-standard pricing. Therefore, the former can be used as a buffer zone for the entire DEX, and can still be used before the return bubble ends. Maintain the price of governance tokens.

Scheme VII: Reverse VE(3,3) Model

Forward (3,3) attaches importance to the global optimal solution of returns, while reverse (3,3) increases through the loss mechanism User de-pled cost/coin holding cost. Readers may understand that traders hold tokens with risk of depreciation, but such projects are often in group members' trading, called native deflation mechanism. The practice of using this model on conventional projects on the market is slightly conservative. For example, GMX does not mean that the principal depreciation will be caused by not pledging, but that the deprivation may lead to part of the matter.Red is lost, readers can watch GMX interpretation online. Using this model requires the project party to fully understand its business and understand the life cycle & design logic, otherwise it will only accelerate the death of the project. Whether it is the token value too high or the rapid depreciation, it is not a long-term project hope. See.

Scheme 8: Liquidity guidance

Liquidity guidance generally has two roles, LP & LD (Liquidity Director). LP still provides liquidity, while LD is responsible for determining where the liquidity will go. Tokemak is one of the few liquidity solutions that use this solution on the market. V2 has also iterated and used internal algorithms to obtain the liquidity guidance route to obtain the optimal solution, so that LP can obtain the optimal mortgage income, while liquidity purchase The user can clearly know how much money can be "leased" and how much liquidity can be "leased". The liquidity marketplace has not yet been launched, but it has accumulated more than 8M of liquidity. Judging from the past performance of currency prices, this narrative has only received attention in the previous round of Defi Summer. There is not much performance in the bear market and this bull market. Whether the liquidity market needs market transparency is still needed to be verified later. The author believes that a certain degree of "clear price marking" is needed in the liquidity market, because there are blind spots, bidding will be inefficient, and there are many potential idle rewards that cannot be correctly distributed to incremental funds. This kind of solution will be in the market liquidity. It acts as a terminator during gameplay, just like MEV-boost in MEV dark forest.

Scheme 9: VE-LP / Proof of Bond (POB)

I finally came to the highlight of this chapter, which is why I think Berachain POL is not the core reason for innovation.

VE-LP/POB's core idea is to introduce liquidity as an entry ticket & defense line for projects. The former can be seen in Balancer, and the latter can be seen in THORchain. Balancer allows users to LP in BPL/WETH, and the LP credentials they obtain can be further pledged to obtain veBAL for handling fee sharing and governance. THORChain POB requires node operators to pledge their native tokens as underwriting funds, and deduct 1.5 times of collateral assets after LP loss as compensation. The liquidity carried by the entire network is hardCap will be 1/3 of the governance tokens. When the network becomes insecure/inefficient, a balance point will be sought through liquidity mining<>node operator income distribution. For example, when the network node's mortgage assets are not enough to repay the on-chain liquidity loss, the next one will be added Release of period node income (governance tokens). No matter how the details of these plans change, there will be entry barriers for the core issues, so how to set a reasonable entry difficulty to maintain sufficient liquidity is the key.

So when we look back at Berachain's POL+Three Coin model, it is essentially a VE(3,3)+VE-LP model. Variant. According to the above introduction, the market for BGT bribery is an application of VE(3,3) model, while POL is an application of VE-LP. The core of the former lies in the management of the market value of the governance token, while the core of the latter lies in the entry threshold. Generally, the governance tokens of VE model on the market are traded randomly in the secondary market, so for ecological projects, liquidity purchases can be carried out at will, but for the VE model project, they face the risk of token fluctuations. , but the POL method has slowed down the acquisition of governance tokens (BGT), giving more time and space to control the market to a certain extent. At the same time, POL allows multiple types of tokens to be collateralized, lowering some entry thresholds in exchange for more More potential liquidity.

Liquidity can be summarized from the above series of liquidity solutions The impossible triangle of game: security, high liquidity, and market transparency.

Safety: refers to whether the solution can provide a back-end defense line for the project party's liquidity, such as the VE(3,3) model Only when the bubble bursts in the bribery proceeds will the VE project party have a possibility of collapse.

High liquidity: refers to whether the plan can attract absolutely high-value liquidity, such as the project party is willing to cede most of the governance agents If you have a currency, then this income will attract a batch of short-term liquidity.

Market transparency: refers to whether the solution can transparent the market demand for liquidity, such as the POB project can carry The liquidity determines the total amount of assets in the node.

Back to the question itself: Does Berachain have any technical bottlenecks that essentially break through the liquidity market?The answer is obvious, nothing, just part of the improvement. But Berachain chose the right application scenario - public chain. If we only focus on the mechanism, we will misjudgment that this potential is only at the protocol level. However, the actual bribery reward of BGT token can also be used to promote other ecological projects. Revitalization can even be regarded as a big narrative of the same level as Restaking. Just imagine, now you are the project party, and you do not have enough capital reserves as liquidity mining as an early reward, but you still form a trading pair in BEX (Berachain native DEX) and have a certain amount of liquidity. At this time, the project It is convenient to obtain BGT returns from the liquidity of these pledges, and BGT can determine the subsequent release of the pool. Since the pool is small, even the small amount of BGT release is more profitable than other blue chip tokens. High, thereby indirectly attracting liquidity. Thinking from this logic, Berachain's POL mechanism is actually a bit like the Restaking track. Because the AVS integrated the security of ETH in the Restaking track, Berachain's small project is also integrating the "security" of part BGT, providing more sufficient liquidity for the project party's subsequent development.

#5 What is happening with Berachain?

What is the best way for users to participate?

As of May 3, 2024, according to Beraland and According to the author, there are currently about 103 projects, among which Defi and NFT account for the majority. Since the project may have multiple businesses, the author also divides such projects into the categories of business. The specific ecological distribution is as follows:

Defi: 36

Gamefi: 15

Meme: 4

Infra: 18

Community: 13

NFT: 24

Most of the current projects are Defi and NFT products. Berachain's ecology is relatively complicated, and the author only selects some key projects to introduce (relatively subjective).

1. The Honey Jar (THJ)

"The Honey Jar is an unofficial community NFT project, situationed at the heart of the Berachain ecosystem, which hosts a number of games."

The above is the official positioning, which can basically be understood as a hodgepodge project of NFT+Gamefi+Community+Gateway+Incubator. Its NFT is called Honeycomb and can be used for governance within projects. Currently all Honeycombs have been cast, with a floor price of 0.446ETH and an initial cast price of 0.099ETH. NFT holders can participate in the platform's game and receive some mysterious rewards from potential Berachain's other project ecosystem (as of February 22, 2024, HJ has accumulated 33 projects cooperation, and about 10 projects provide airdrop rewards), Berachain's ecosystem can "position" to valuable high-net-worth users through these NFT holders and potentially improve the future participation of the project (high-net-worth users may be willing to invest more). In short, this is an NFT that requires "the project party to do things".

In addition, every quarter, The Honey Jar releases new mini-games and allows users to perform a new round of NFT casting, a total of There are 6 rounds. These NFTs are different from Honeycomb, called Honey Jar (Gen 1-6), and the Gen serial number of this round is determined by the order. Users who purchase these NFTs can participate in the tourThe game can be understood as an NFT lottery game, and a lottery will be performed after all the current NFTs are cast. The winner can receive the rewards in the prize pool (NFT+ bonus). There are currently two rounds of games, and the remaining four rounds will be announced in 2024Q2 and deployed on 4 different EVM chains.

THJ incubated 6 tissues:

First, Standard and Paws. The project is a rating system designed to avoid ecological waste projects.

Second, Berainfinity, can be understood as Berachain's Gitcoin, helping developers/projects develop sustainably.

Third, ApiologyDAO. Positioning is the investment DAO of the Berachain ecosystem.

Fourth, Mibera Maker. Positioned as Milady of Berachain ecosystem.

Fifth, The Apiculture Jar. Positioned is the Meme/Artist department of THJ.

Sixth, Bera Baddies. Positioning is the female community on Berachain.

Evaluation: The author believes that the early participation of this project is relatively valuable, and no one will dislike the "shovel". But this kind of narrative generally has the opportunity to price in early, so we must be clear about other core collapses/risk points besides systemic risks (the subsequent performance of Berachain mainnet has been broken):

First, the project party has sufficient bargaining power and BD capabilities, and can "use OG to make the project party". If this narrative is proven that Honeycomb cannot truly capture high-net-worth users, then it will also be No follow-up project party is willing to provide high-value benefits to NFT holders.

Second, provided by other project partiesThe total value of the potential reward to the NFT holder needs to be greater than or equal to the floor price of the NFT. Let's conservatively estimate the price of Honeycomb:

1) Honeycomb cost price: 0.099ETH is approximately equal to 300U

2) Forecast return: The risk-free return on the chain is about 5% (POS); currently 10 projects are willing to pay for airdrops, and each project airdrop is about 6. Monthly distribution, with an initial value of 30U (10% Expected rate), and a total theoretical value of 300U (30U*10), which means 50U per month; assuming there are 3 new projects willing to airdrop to NFT holders each month.

3) Return growth rate: Assume that the project party is washing the market in the first three months, waiting for the low purchase and then pulling the market, and the next three months Pull the market by 1 times, 1.25 times and 1.25 times respectively; assuming that the institutional price returns at 5-10 times the price point on the day of TGE, the release period is 12 months, which means that the project party needs to pull 2.5-5 times within 6 months (about 10 times). The same is true for pulling the market in the next three months by 1 times, 1.25 times, and 1.25 times).

The estimated net NFT value of the final result is 367U. If estimated at the current floor price (0.446ETH), the market forecasts the return value of a single project needs to be maintained at 20%. The above estimate is for fun, but the actual reference value is not high.

2. Build a bera

"Build-a-Bera is a results-driven partner with the Berachain Foundation designed to provide Bera-oriented founders with the tools, mentorship, and re sources needed to thrive in a competitive market."

According to the official definition, Build-a-Bera is a partner of the foundation and helps the project parties of the ecosystem develop, which is commonly referred to as an incubator. Each period recruits 5 project parties for a period of 12 months. Currently, the five projects on the official website are: Infrared, Gummi, Kodiak, Shogun, Beratone.

Evaluation: The author believes that these are selected The project party has a high probability that it will receive more Berachain support, and that the various projects in the incubator will be easier to form cooperation (in fact, the same is true). Therefore, the author will introduce the selected projects mentioned above.

3. Infrared Finance

Friends who are familiar with Defi can regard it as a combination of Frax (frxeth+sfrxeth) and Convex. In short, Infrared Finance is an LSD project designed to solve BGT Liquidity issues.

Basic process: Users pledge tokens in Infrared Finance, and these tokens will be pledged in BEX by Infrared Finance In the sex pool, the BGT income received at the same time will be authorized to the Infrared validator. The Infrared validator returns the subsequent BGT release income + other income (block rewards, bribes, MEVs, etc.) to the Infrared Vault. Infrared will partially Other income is regarded as treasury income, and the accumulated BGT income in the pool is minted as iBGT+ iRED to return to the user.

Token model: iBGT is 1:1 pledge by BGT; users can use iBGT in other products on Berachain; users can pledge iBGT to obtain siBGT, siBGT can obtain BGT benefits from Infrared validator, such as bribery, block yield, etc.; iRED can be used on the platform Governance, such as guiding the Infrared validator to increase the release of BGT to a certain LP.

CommentPrice: Another project of "using the emperor to command the world". On the surface, it solved the problem of BGT liquidity, but in fact it moved the battle for election bribery from BGT to iRED. For example, Infrared Finance accounts for 51% of LP, which means it has an absolute voice in the release distribution of BGT. Naturally, iRED is the "National Jade Seal" that will make the world. Under this basis, if the liquidity needs of the project party remain unchanged, Infrared receives more bribes than other validators, further aggravating Infrared's control over Berachain. In fact, this may be more like a fact. Taking Convex's voice over Curve in the past was once approaching 50% as an example, and Berachain currently does not have other LSD projects with Build-a-Bera support, and currently ecological cooperation There are also many. If the user's needs are relatively stable BGT returns + some excess returns, it can be expected that after going online, the priority portal for users to pledge tokens is Infrared. In addition, the dual token "seesaw" mechanism adopted by the project further amplifies the returns of siBGT holders, because not all users want to sacrifice liquidity, so the benefits of this pledge should be higher than those of ordinary BGT LSD products. And the sources are all "real income". It seems like a win-win product between multiple parties, we also need to understand some of its collapse points/core risks:

First, the depreciation of iRED risk. Each iRED release will increase the total circulation, thereby indirectly reducing the value of iRED. The implicit value of iRED represents the benefits of bribery. If potential projects are more willing to directly provide high bribery in Berachain BGT Station for some reasons (such as the pursuit of decentralization), then the implicit value of iRED will become lower, and in turn, Accelerate the depreciation of iRED. If Infrared can master most liquidity, then it will essentially return to Berachain's POL mechanism. Strictly speaking, this is considered a systemic risk.

Second, the centralized risk of Infrared. Although Infrared currently has multiple support, including incubators that the foundation cooperates with, their potential risks of doing evil cannot be ignored. At present, Infrared does not explicitly specify the threshold for their validator participation. If it is run completely by its own, it will have a higher risk of single point of failure than Lido.

4. Kodiak

"an innovative DEX that brings concentrated liquidity and automated liquidity management to Berachain. ”

Kodiak Positioning is a DEX and provides services that automatically manage liquidity (see the dynamic AMM list in the liquidity solution above), and also provides one-click coin issuance function. According to the official, Kodiak is not a direct competitor of BEX, but a niche replenishment, because BEX does not provide the function of aggregating liquidity. In addition, it is worth noting that Kodiak cooperated with Infrared and proposed two economies Flywheel:

First, the Treasury flywheel. Kodiak will first bribe Infrared, thereby increasing the BGT release of Kodiak LP. Kodiak then treasury Liquidity staked in Kodiak LP pool and LP tokens are staked to Infrared, Infrared thus gains control of the LP and is subsequently staked in Kodiak LP pool to obtain Infrared's iBGT+iRED income.

Second, community flywheel. Users can use stake their Kodiak LP tokens and get the iRED+iBGT returns from Kodiak.

Evaluation: It is suitable for interest-generating assets and native asset trading pairs, but it may not be suitable for siBGT&iBGT scenarios. At the same time, the flywheel has high requirements for the mid- and late-stage control capabilities of the project. The above article is also It is mentioned that dynamic distribution AMM is suitable for token pairs with high correlation. For example, LST/ETH, LST (non-rebasing token) will accumulate the validator's returns, which should be higher than the price of iBGT, but because the returns are stable returns , there will be no extreme volatility, so dynamic AMM will be more likely to form a price buffer zone, so that it will not appear between the two. However, the native returns of siBGT are different from POS, with relatively diverse sources and not low volatility. , so the price buffer zone actually makes the price discovery efficiency less efficient, potentially underestimating the real market return value of siBGT. In addition, the core collapse point of the project is: bribery income (iBGT+iRED+liquidity stability)This is basically a common problem for all bribery options, which also implies that the implicit value of Kodiak tokens should be lower than or equal to the bribery income, otherwise the project party will have a deficit. (Similar to the current situation of lido), but on the other hand, if the value of Kodiak native tokens is not high enough to attract enough liquidity, that is, there is not enough BGT release. *In the early days, most LP thinking should be currency-based, which is a bullish signal. *The cost of bribery is greater than or equal to the profit of bribery, but in the middle and late stages, the ecology is weak, and LP naturally needs to think from the U-based position. At that time, Kodiak will only There are two options left: maintain the bribery volume on the U standard, or continue the bribery on the currency standard. The former accelerates the potential selling pressure in the market, while the latter reduces the platform's liquidity attraction, which are both at the critical point of collapse. If there is no other narrative, it will come to the end of the life cycle.

5. Gummi

"A sweet treat for those sers interested in something a little stronger than honey."

According to the official description, Gummi positioning is mainly a money market. There is not much information at present, but it is likely to be a lending agreement and supports leveraged lending.

Their cooperation with Infrared is similar to Kodiak. Although Gummi did not explicitly say that he would bribe Infrared validators or all validators, it is highly likely that it is the former.

Evaluation: There is not much room for discussion for this project at present because the product details are still unclear. But because it is a Build-a-bera incubation product + Infrared ecological partner, it is mentioned here.

6. BeraBorrow

"Beraborrow is a decentralised protocol at the forefront of the Berachain ecosystem, providing int erest-free loans using the iBGT token as collateral. ”

Friends who are familiar with Defi can understand it as Liquity's imitation disk. According to official description, BeraBorrow is a collateralized debt agreement (CDP) that allows users to lend NECT stablecoins with iBGT at 0 interest + 110% collateral rate, which is anchored at USD 1.

Why interest-free: It is impossible to have a truly "interest-free" agreement. So our focus should be where the agreement is pumping from. BeraBorrow charges fees every time the user lends NECT and redemption. The redemption fee is dynamically adjusted according to the redemption frequency within 12 hours. The more redeemed (meaning that the value of NECT is overestimated), the more fees are charged.

Anchoring mechanism: divided into hard anchoring and soft anchoring. The former provides a 1:1 redemption mechanism between iBGT and NECT. When NECT is overvalued (greater than US$1.1), you can exchange NECT worth 1 BGTi at a 110% mortgage rate on the platform, and then sell NECT to obtain the difference as Return; when undervalued (less than US$0.9), it can be purchased in the secondary market and redeem iBGT 1:1 on the platform, and the difference in the middle is the return. The latter refers to the value of NECT theoretical anchoring, that is, it is equal to US$1. The platform adjusts the overestimated NECT through dynamic redemption fees.

Maximum leverage: 11 times. Because the platform mortgage rate is 110%, theories can open 11 times of leverage (1+1/0.1=11).

Other risk control: A stable pool will be launched for platform liquidation in the future, and the profits of the liquidation will be given to the LP of the stable pool.

Evaluation: Stablecoin projects are essentially bonds, and users care about APY, not the use scenarios of stablecoin (More trading pairs). If you really want to use stablecoins, why not use Honey? Judging from the current product revenue sources, only stable pools are the potential source of revenue, but it is not ruled out that iBGT mortgaged on the platform may be further mortgaged on Infrared vault in the future to obtain potential revenue. Then for users, if they are bearish on iBGT in the short term, they can amplify the leverage and wait for the bottom position to be liquidated to obtain potential liquidation spreads.

Liquity's highest liquidation value = debt value - (the current price of the number of collateral assets is <10%* the proportion of users in the stable pool).

Simply estimate it with an example. Suppose a position has 500iBGT and 10000 NECT debt, the current mortgage rate is 109%, that is, the iBGT price is 21.8 U (109%10000/500). If the user accounts for 50% in the stable pool, it means that the user can obtain a profit of 450U (50050%21.8-1000050%). According to the above example, the key profit point of the user lies in the current proportion of the stable pool + the liquidation frequency.

In addition, if users are bullish on iBGT in the medium and long term, they may obtain up to 11 times the siBGT revenue by amplifying leverage, but the current business Not specified in the official BeraBorrow document. For such users, the key risk is the downward fluctuation risk of BGT.

7. Beratone

"BeraTone offers an intricate life-sim and farming system, reminiscent of beloved classes like Stardew Valley, allowing players to cultivate and manage their dre am farmstead."

According to the official introduction, Beratone belongs to MMORPG, players will play the role of bears and farm with various bears in the simulation world. Friends who are familiar with the game can refer to the Stardew Valley Story. One of the creators of BeratoneIt is PixelBera and the art of Bit Bears (the fifth generation of Bong Bears NFT) Thanks to the popularity of Bit Bears, PixelBera hopes to introduce some "utility" to Bit Bears, and Beratone was born. The game Demo is expected to be launched in Q2 24 and will be launched in Q1 2025. NFT is being sold in 24Q3, and Founder’s Sailcloth NFT has been sold, which will provide a variety of buffs in the game, such as increasing backpack space. It is worth noting that the game will be available to everyone, and there are no threshold restrictions, so the NFT sold in Q3 is not an entry ticket, but may also be similar to Founder’s Sailcloth NFT.

Evaluation: The art style is closely related to Web2 games, but TBH and Web3 users still pursue APY, and the game is essentially a huge Defi. However, as a Gamefi project party, one of the rare advantages is that the economic model can be designed as a single-blind model, that is, the user is not clear about the benefits, and is equipped with an appropriate long-term economic system, plus an in-app purchase system, the life of a game The cycle will be longer than we think. In addition, Gamefi's revenue is calculated based on the NFT standard, so it can also create an inflated market value through a lower turnover rate to attract users to participate in the gold-making volume, but it is more difficult to control the market compared to the U/coin standard. In short, if you are a Bera enthusiast, you can consider running with the game. The odds in the game are relatively high, and you need to estimate the turnover rate in the secondary market. If necessary, you can use pre-market trading and OTC to avoid risks.

The above-mentioned project introduction is relatively introductory and is not enough to bring ecological insight to readers, so the author will give the above-mentioned ecological map All projects have done some research, ranging from 1 hour to 5-10 minutes. Here are some of my summary:

Projects are highly native and have different GTM strategies: Most projects deployed in Bera are not multi-chain Compatible, but native to Berachain, the ratio of native projects to non-native projects is about 10:1 (Note: It is not ruled out that some products are from the same team). Contrary to intuition, not all non-NFT native projects tend to issue NFTs as a cold start, and most of them are still halal.

Economic flywheels are all different, and they are still in the essence: most of the projects deployed in Berachain are made through Infrared realizes economic flywheel, and at the same time, there are projects that further build multi-layer VE(3,3) based on the original BEX, such as Berodrome. But the core idea remains unchanged, and any incentive is the currency standard, so users only need to clarify the fundamentals of the projects behind the token + market-making capabilities. The flywheel between projects should be coupled, but it does not mean that the flywheel effect of the project will collapse due to the collapse of a single project. As long as the ceased tokens can be exchanged for excess returns, the user is willing to continue to protect the market and allow others to The project fills the gap in the flywheel.

Most high-financing projects issue NFT: 7 of the top 10 financing projects are Community/NFT/Gamefi, and all issue NFTs. .

Community hot spots, but hot to each other: the average number of viewers on the native Berachain ecological project is 1,000-2,000+ people. Some project parties are underestimated in the number of readers (number of followers/number of readings for draws < ecological average). For example, Infrared has 7,000+ followers, and the average number of post viewers is 10,000+; many native ecological projects will cooperate with each other, and the cooperation forms are relatively diverse, such as participating in economic flywheels, ceding tokens, etc.

The project is still innovating, but it is not a subversive narrative: in the NFT track, some project parties choose to use BD capabilities in exchange for user attention. Instead of just bragging about the effects, such as HoneyComb, Booga Beras. In the Defi track, some project parties continue to study liquidity solutions, such as Aori, and some project parties try to optimize past VE(3,3) models, such as Beradrome. In the Social track, some project parties try to review the quality of ecological projects through Peer to peer, such as Standard & Paws. In the Launchpad track, some project parties try to implement Fair Launch in the form of token equity cutting and LP allocation, such as Ramen and Honeypot. In the Ponzi/Meme track, some projects tried to achieve a "sustainable economy" by Floor price pool, such as Goldilocks.

#6 Where should Berachain's explosion point be? What ecosystem is potential stock?

I believe that all readers may also know Berachain after reading thisWith a relatively comprehensive understanding, it is not difficult to imagine that there are two potential development paths: LSDFI and Ticoin Assets.

First, LSDFI refers to all economic flywheels related to Infrared, which are essentially the economic moat of Berachain. As can be seen from the above, many projects have established cooperation with the Infrared Finance ecosystem and entrust the LP to Infrared to obtain excess returns. Therefore, the subsequent ecosystem is likely to replicate the old path of Ethereum, such as using siBGT as collateral assets stablecoins, interest rate swap agreements, etc. But unlike the Ethereum pledge threshold, Berachain's threshold lies in the liquidity. Therefore, LSD protocols such as pump finance that lower the threshold for staking participation can also be reproduced on Berachain in another form - amplifying liquidity, such as leverage. Borrowing and other methods.

Second, the graph coin assets do not necessarily refer to a certain protocol, such as ERC404, but all potential NFT assets and NFTs Fragmented solutions. The reason why the Tucoin assets are suitable is that Berachain natively provides liquid bribes, which is the lifeblood of all ecological projects to issue coins, and it is also Berachain's own defense line. NFT project parties can attract a new wave of buying through the method of converting coins, which is also a rebasing thinking (split plate), and participate in the economic flywheel of other project parties at the same time, such as the Infrared finance mentioned above.

In fact, readers can explore the above two directions by themselves. The author has found individual cases during the research process, but because this article is only used as Research and analysis are not used as investment advice, so it is not mentioned here.

#7 Postscript

The author talked to a friend about Berachain, and Talk about whether the project will be successful?

Some people say: "Berachain's community support is very high, and the data is not bad now. Many NFTs are sold. It should be It can run out."

Another person said: "Berachain is just a huge Defi. After this narrative ends, it is soonYou will not be able to run away, and it is impossible to run away without fundamental ecological-level narratives. ”

The author has always believed that the definition of "successful project" is very complicated, which is different from "Defi/What is the end of the project", and he Not a single measure.

If the community responds well but VCs don't make money, is this a good project?

If VCs make money and the community is crying, is this a good project?

If everyone is happy together, some people become cannon fodder, is this a good project?

If you are a landlord, everyone becomes Is this a good project for your crops?

The project talks to you about the future, and you talks to him about the present, and is this a good project?

The project talks to you about technology and narrative with him. Is this a good project?