29 mins ago

2,069

Author: Lian Ping Source: Wall Street Insights

Today’s Central Bureau meeting pointed out that moderately loose policies should be implemented currency.

In September, Lian Ping, chief economist of the Guangkai Chief Industry Research Institute and chairman of the Chief Economist Forum, issued a report entitled "Recommended adjustment of the monetary tone to" "Moderately Loose" article. Lian Ping suggested that the monetary tone should be defined more scientifically and rationally. The monetary tone will be adjusted to "moderately loose" to create a suitable environment for the implementation of greater RRR cuts and interest rate cuts.

Lian Ping reviewed my country's currency practice in the past 30 years in the article. The central bank only implemented "moderately loose" currency during 2009-2010.

The following is the full text of Lian Ping’s article:

Since 2011, my country has implemented a "stable" monetary tone for 14 years. The current foreign economic situation has undergone major changes, especially facing severe insufficient demand, deflation and downward pressure, while the currencies of the United States and Europe are turning to easing in an all-round way. Against this background, should my country's currency continue to maintain a "stable" tone? Or should it be adjusted in a timely manner to send a more positive and clear signal to the market, so that the currency can better perform its countercyclical adjustment function? This article will start a discussion and put forward opinions.

1. Flexible currency adjustment should be the norm

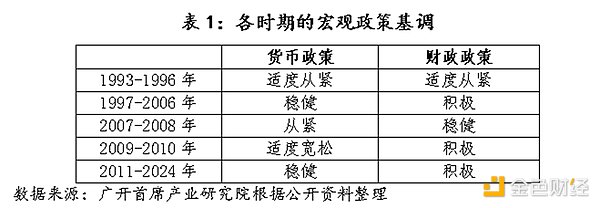

Reviewing my country’s currency practice in the past 30 years , the monetary tone can be divided into "tight", "moderately tight", "stable", "moderately loose" and "easy" ranges from tight to loose. Based on changes in the objective situation, the monetary authorities take "stability" as the core and flexibly adjust between "tightening" and "easing" to achieve the purpose of stabilizing the economy and making counter-cyclical adjustments.

In 1993, my country experienced economic overheating and serious inflation. The central government adopted a moderately tight monetary policy. By the end of 1996, the inflation that had lasted for three years had dropped sharply. fall back. In 1997, my country faced sluggish domestic demand, coupled with the severe external shocks caused by the outbreak of the Asian financial crisis, resulting in a deflationary situation. In response to internal and external pressures, the monetary tone shifted from "moderately tight" to "stable", and through appropriate Increase money supply to maintain RMBThe currency value is stable, and credit leverage is used to promote the expansion of domestic demand and increase exports. At the end of 2007, in order to prevent economic growth from turning too fast into overheating, the Central Economic Work Conference set the monetary tone for 2008 as "tight." In September 2008, marked by the bankruptcy of Lehman Brothers, the U.S. subprime mortgage crisis accelerated and our country's economy was also affected by a financial crisis that had not been seen in a century. The central government decided to implement proactive fiscal measures and moderately loose money, which continued until 2010. Since 2011, in order to prevent inflation, asset price bubbles, "hot money" changes and financial risks, my country has returned to a "stable" monetary tone. In the approximately 14 years since then, the tone of my country's currency has not changed significantly, but it has tended to be looser or tighter in actual operation. Among them, the sound money from 2011 to 2013 was generally tight, emphasizing the prevention of inflation; the sound money from 2014 to 2019 returned to "sound neutrality", emphasizing neither looseness nor tightness; the sound money from 2020 to 2024 In essence, it is on the loose side, which highlights the flexibility, appropriateness, precision and power of the currency.

Looking back on the past, there are several points worth paying attention to in my country's monetary tone:

p>First, when the economy faces a serious impact, the monetary tone will often make directional or larger adjustments. Judging from historical experience, under the threat of economic overheating or inflation, the monetary tone will usually quickly adjust in a tight direction. For example, "moderate tightening" in 1993, "tightening" in 2008, etc.; in the context of contractionary shocks, the monetary tone will be adjusted in a loose direction in time. This adjustment may be across one gear, or it may be It's two gears. For example, in 1997, the monetary tone shifted from "moderately tight" to "moderately tight". In 2009, the monetary tone skipped from "moderately tight" to "moderately tight" and "moderately loose", and directly crossed over from "moderately tight" to "moderately loose."

Second, the monetary tone sometimes appears to be “unworthy of its name” in actual operation. Among the five major keynotes, "tight", "moderately tight", "stable" and "moderately loose" have all appeared at different times, with the exception of "easy". But this does not mean that the "loose" tone is truly absent. During 2009-2010, my country's money and credit grew rapidly. Especially from the end of 2009 to the beginning of 2010, the year-on-year growth rate of M1 reached 38.96%, the growth rate of M2 was close to 30%, and the growth rate of various RMB loan balances exceeded 34% for many consecutive months. ; Matching the rapid growth of credit, local financing platforms have sprung up, and some regions have even established more than ten financing platforms in a short period of time. It can be seen that the currency tone at that time was far fromIt is "moderately loose" in name, but "easy" in real terms. Similarly, sometimes the true meaning of "stable" is "moderately loose" (such as 1997), and sometimes it means "moderately tight" (such as 2011-2013). Often its expression changes in the opposite direction from the previous tone, and it needs to be based on the actual situation. Set out to grasp its relative tightness changes.

Third, the monetary tone has lacked flexibility in recent years. Before 2011, the monetary tone switched between "tight", "moderately tight", "stable" and "moderately loose" in a timely manner according to changes in the objective situation and the needs of regulatory objectives; after 2011, although the economic operation has also undergone stages Although there have been significant changes and fluctuations in nature, the flexibility of the monetary tone is obviously insufficient, and the "stable" tone has been continuously used for 14 years. In fact, over the past 14 years, the economy has experienced a series of fluctuations. Such as the economic downturn and capital outflow in 2015-2016; the US trade war against China in 2018-2019; the impact of the epidemic in 2020-2022, etc. But the overall tone of the currency has not changed. This is obviously not conducive to the currency's countercyclical adjustment based on the needs of the real economy. Of course, the spillover effect of the Fed's currency has brought certain constraints to our country's currency, but the Fed's currency has gone through several rounds of major adjustments in the past 14 years.

2. It is necessary and feasible to adjust the current monetary tone to "moderately loose"

First of all , from an environmental perspective, macroeconomic and financial indicators are relatively weak, and further monetary support is urgently needed. In August 2024, my country's manufacturing purchasing managers' index (PMI) was 49.1%, down 0.3 percentage points from the previous month. The prosperity of the manufacturing industry continued to decline, and it was below the boom-bust line for the fourth consecutive month. Since the beginning of this year, the manufacturing PMI has only briefly stood on the boom-bust line in March and April, and the remaining six months have been less than 50%. In 2023, there will only be 4 months above the boom-bust line, and 8 months below 50%. %. In other words, my country's manufacturing industry has been in a sluggish state for most of the past two years. Looking at financial data, the balance of broad money (M2) increased by 6.3% year-on-year in August, which has been below 8% for five consecutive months; the balance of narrow money (M1) fell by 7.3% year-on-year. In July, new RMB loans only increased by 260 billion yuan. If the 558.6 billion bill financing is excluded, the actual new loans were negative; although new RMB loans in August rebounded to 900 billion yuan, they were 12200 billion yuan in the same period from 2021 to 2023. Compared with 1.36 trillion yuan, there is still a big gap. Judging from the breakdown of data, the scale of short-term, medium- and long-term loans to residents and enterprises has declined significantly, and the factors leading to credit decline due to insufficient demand may exceed seasonal factors. In addition, price, real estate, consumption and other indicators are also in a continued downturn.

Secondly, there is a clear gap between the existing "stable" monetary tone and market psychological expectations. So far in 2020, even in the face of the new crown epidemic Such as major external shocks and insufficient domestic demand, the monetary tone will only shift from a "stable and neutral" tone to one that maintains a stable currency. "Flexible and appropriate", "flexible, accurate, reasonable and appropriate" and "precise and effective" have been adjusted in loose directions, but the overall tone is still "stable". Since 2023, the central bank has made multiple adjustments to the LPR interest rate, such as the 1-year LPR. Interest rates were lowered in June 2023, August 2023 and July 2024 10 basis points, the 5-year LPR interest rate was lowered by 10, 25 and 10 basis points respectively in June 2023, February 2024 and July 2024, except that the 5-year LPR interest rate was reduced from 4.2% in February 2024. Except for the slightly larger rate cut to 3.95%, the other rate cuts are very small. This is different from that in Europe and the United States. Continuous interest rate cuts of 25-50 basis points, or even a single maximum reduction of 100 basis points, have more symbolic meaning than practical significance, and there is a clear gap between them and market expectations. Therefore, small interest rate cuts are difficult to have a significant impact on the market. From the perspective of strengthening expectation management and effectively guiding market expectations, making reasonable and appropriate adjustments to the monetary tone as soon as possible will help boost market confidence and change the current situation of generally weak market expectations.

Thirdly, from a collaborative perspective, in order to enhance the effect of countercyclical adjustment, currency must better coordinate with fiscal , implement the "double easing" combination. In the process of counter-cyclical adjustment, expansionary finance is usually used to stimulate aggregate social demand through measures such as borrowing, deficit, tax cuts, and expansion of expenditure. However, due to the "crowding out" of expansionary finance itself. "effect" side effects, that is, when When spending increases, money demand will increase accordingly. With a given money supply, interest rates will rise, causing private sector investment to be suppressed. At this time, expansionary money is often needed to restrain the rise in interest rates by increasing the money supply. my country’s fiscal tone is clearly set at “positive fiscal ", and proposed to "increase efforts to improve efficiency", and the overall bias is towards expansion. The national fiscal budget deficit in 2023 was initially set at 3%. The budget was adjusted in October 2023, adding 1 trillion yuan of ultra-long-term government bonds. The final fiscal The deficit rate will reach 3.8%. In 2024, our country’s budget deficit rate will continue to be set at 3%. The quota for special bonds is 3.9 trillion, a further increase from last year. It has also been decided to issue large-scale ultra-long-term special government bonds for several consecutive years starting this year. While the fiscal tone is obviously expanding, the currency is bound to provide active cooperation, including increasing liquidity. Supply, further lowering interest rates, etc. At this time, the monetary tone is very strong.It is necessary to make corresponding adjustments from "stable" to substantive "moderately loose".

Finally, changes in the external environment provide a time window for my country’s currency tone adjustment. On August 23, Federal Reserve Chairman Powell delivered a speech at the global central bank governors’ meeting, officially confirming that “the time for adjustment has arrived.” The market generally believes that the Fed's announcement of an interest rate cut in September is a foregone conclusion. We estimate that this round of Fed interest rate cutting cycles may last 14-16 months, with 6-8 interest rate cuts, and a cumulative rate cut of 150-200 basis points. It is undeniable that in recent years, as the downward pressure on the economy and deflationary pressure have continued to increase, my country's monetary tone has still not been adjusted. A very important reason is the constraints imposed by the high interest rates implemented by the Federal Reserve on my country's economy and finance. At present, a new round of interest rate cuts by the Federal Reserve is imminent. Against this background, my country's monetary tone has gained a rare time window for adjustment, giving it room to promote a new round of reserve requirement ratio and interest rate cuts.

The "moderately loose" monetary tone is between "stable" and "loose" time, its implementation under the current circumstances has three positive significances: First, it is more proactive than the "stable" monetary tone, which can match the greater use space of total volume, price and structural monetary tools, and inject sufficient space into the market. liquidity and pushed real interest rates significantly lower. Second, the monetary tone is relatively more prudent than the "loose" monetary tone. Since the easing efforts are relatively moderate, it can avoid sequelae such as "flooding" and severe inflation. Third, compared with the current monetary tone that is called "stable" but is actually loose, its greatest positive significance is that it can send a clearer and clearer signal to the market, allowing all market parties to better understand the easing intentions. It also formed consistent positive expectations for the follow-up and enhanced confidence in the economic recovery. Since RRR cuts, interest rate cuts and structural tools have been frequently adjusted in the direction of easing in recent years, and the direction of continued countercyclical adjustment will not change in the future, why can't we realistically adjust the "stable" tone to a "moderately loose" tone in a timely manner? Judging from all aspects of the situation, the current monetary conditions are ripe for implementing a truly "moderately loose" tone.

3. Related Suggestions

Suggestion 1: Conduct a more scientific and reasonable adjustment of the monetary tone define. Formulators should comprehensively sort out and standardize the monetary tone system and related definitions, especially the boundaries between “loose” and “moderately loose”, “tight” and “moderately tight”, and explain the differences betweenUnder the keynote, what specific changes will occur to the monetary targets and operating tools, how to refine the triggering conditions for the entry and exit of each keynote, how to match the monetary keynote and the fiscal keynote, etc.

Recommendation 2: Further strengthen expectation management and send clear monetary signals to the market. While the monetary tone system is being standardized, it is recommended that the monetary authorities adopt a more rigorous and accurate tone that better reflects current needs, so that all market parties can better understand the direction of the currency and form a positive feedback that resonates at the same frequency. As the leaders of the central bank pointed out, "When the transparency of currency is improved, the understandability and authority of currency will be enhanced, and the market will spontaneously form stable expectations for future currency trends, rationally optimize its own decision-making, and monetary regulation will be more effective with half the effort."

Recommendation 3: Adjust the monetary tone to "moderately loose" to create a suitable environment for implementing greater RRR cuts and interest rate cuts. Judging from the possibility of lowering the reserve requirement ratio, the weighted average deposit reserve ratio of my country's small banks is currently as low as about 5.0%. There is relatively little room in the short term, but it does not mean that it cannot be further reduced; the weighted average deposit reserve ratio of medium-sized banks is 6.5%, and the weighted average deposit reserve ratio of large banks is 8.5%. If the monetary authorities implement a new round of RRR cuts, they may consider targeting large state-owned commercial banks and national joint-stock commercial banks to focus on targeted RRR cuts. Given that relevant banking institutions account for 60% of deposits in my country's banking industry, a targeted reduction of 0.5 percentage points in the reserve requirement ratio is expected to release more than 600 billion yuan of liquidity to the market. Given that current real interest rates are still relatively high, further interest rate cuts are necessary. It is recommended to concentrate resources and implement a single larger interest rate cut of about 50 basis points at the end of this year or early next year. At the same time, considering that among the structural monetary instruments, the carbon emission reduction support instrument, the inclusive small and micro loan support instrument, and the inclusive pension special re-loan will all expire at the end of this year, it is also possible to further strengthen the relevant structural monetary instruments at the beginning of next year. New quotas will be added, and re-loans to support agriculture, re-loans to support small businesses, and rediscount rates will be lowered by 0.5 percentage points each to facilitate cooperation in green finance, inclusive finance, pension finance and other issues.