31 mins ago

4,777

Author: Austin Weiler, MESSARI Agreement Research Analyst; Compilation: 0xjs@<<

The main points of this articlePayfi Extended solution.

The adoption of stablecoins is surging, with a total market value increased from $ 130 billion to US $ 204 billion, and the monthly transfer volume increases from 148% to US $ 26 trillion in 2024 The solid foundation of the chain payment solution.

The financial layer in Payfi is rapidly mature; in 2024, the monthly payment amount funded by HUMA and ARF increased from $ 63 million to US $ 136 million, highlighting its important growth to global companies around the world sex.

T+0 settlement and DEPIN Financial and other emerging PayFi use cases have changed the method of improving cash flow and reducing settlement delays in traditional industries, and opened new opportunities for enterprises of various scale.

The combined regulatory clarity and DEFI are essential for PayFi's expansion in 2025, because the ecosystem meets global standards to release liquidity and promote the participation of institutions.

ForewordPayfi follows the principle of currency time value, that is, today's dollars are more valuable than the future dollars. The money received today can be invested in enterprises or markets, and additional value is generated over time. Payfi has become the cornerstone of the traditional financial system. It is essential for global economic growth to be rooted in daily life.

Examples of the existing PayFi market include credit cards (the global trading market size in 2023 is $ 16 trillion) and trade finance (global enterprises supporting $ 89 trillion in enterprise payment markets). Remittance is another important example. One of the seven people around the world depends on cross -border payment remittances, whether it is sending or receiving. However, the realization of prepaid funds for remittances requires $ 4 trillion to support settlement, which indicates that the capital efficiency of the current system is low.

Although the traditional PayFi system is very important, it also faces major challenges:

Slow: cross -border payment may take several working days to settle.

Elegant: remittances may generate high costs (the average global average of 7%).

It is difficult to obtain: Many people who want to get these services, including 1.4 billion people around the world without bank accounts, are rejected due to geographical restrictions, lack of identity or insufficient income.

These inefficient problems highlight the demand for more effective solutions.

Payfi is the abbreviation of Payment Financing. It makes basic financial use cases such as credit, trade finance, and remittances easier to access, safer, safer, and more secure, safer, and more secure, safer, safer, and saferMore efficient. By leveraging blockchain technology and stablecoins, PayFi reduces settlement times and transaction costs. Solutions related to PayFi provide businesses and individuals in global markets with greater access to payments finance.

In addition to improving existing systems, PayFi creates new markets, allowing for entirely new financial use cases that were previously impossible. This enables developers to design innovative financial solutions that simplify the exchange of value and reduce settlement delays.

Real-world assets (RWA), such as stablecoins and tokenized invoices, are the medium of exchange in the PayFi ecosystem. These assets enable businesses to access liquidity, trade efficiently, and take advantage of opportunities in ways that traditional systems cannot match.

The PayFi ecosystem provides technical infrastructure for building financial primitives to solve the long-standing inefficiencies of traditional payment financial systems. By enabling old and new use cases, PayFi expands financial access and drives economic growth around the world.

PayFi use casesPayFi applications solve the inefficiencies of the traditional financial system and unlock new opportunities. From enabling T+0 settlement to facilitating DePIN finance, the following use cases demonstrate PayFi’s transformative potential across industries.

Credit/Debit Cards Backed by Digital AssetsCredit Cards Backed by Digital Assets are a prime example of how PayFi applications can enable innovative financial solutions. Rain is one such application that provides a customized USDC-backed enterprise card for Web3 native teams. In Rain’s model, a corporate finance department deposits its USDC into a vault to determine its credit limit. At the end of each settlement cycle, balances are automatically settled via on-chain clearing, ensuring transparency and efficiency. While Rain relies on USDC and vault-based operations, other solutions can be collateralized via any stablecoin supported by the currency layer or even blue-chip crypto assets like Bitcoin or Ethereum.

Furthermore, not all payment solutions require a vault-based mechanism. Some systems, such as Kulipa, integrate directly with self-hosted wallets, allowing users to maintain control of their funds while accessing Web2 debit card functionality. The adoption of low-latency blockchain enhances these processes, in many cases allowing funds to be locked upon card authorization while maintaining a self-hosted environment. The Solana protocol enables the use of Program Derived Addresses (PDAs) to support this use case, allowing programs to sign for users in real time. These flexible models address a variety of business needs and reduce reliance on traditional banking infrastructure.

Digital asset-backed credit and debit cards are a growing use case in PayFi, which combines financial inclusion with cutting-edge payments technology. The cards leverage blockchain for settlement liquidity and include multiple collateral options.

Cross-border PayFiCross-border PayFi is a transformative solutionIt aims to solve the problem of low efficiency of traditional banking channels (such as agent banks and SWIFT), which usually delay transactions for several days. In order to meet the needs of the day of settlement, payment companies usually deposit funds in advance in their destinations. This process is called prepaid funds. Although the prepaid funds can effectively ensure liquidity, it will occupy operating funds, restrict business growth and bring financial risks. It is estimated that the funds locked in global prepaid funds accounts are as high as $ 4 trillion.

Payfi application provides modern alternatives by providing a liquidity solution on the chain to achieve real -time and economical and efficient settlement. Using USDC and other stablecoins, these solutions allow licensed financial institutions to bypass the needs of prepaid funds by setting up payment on the blockchain nearly realized on the blockchain. This model reduces operating costs and releases capital, so that the company can invest in growth and expand the scale of operation without additional operating capital.

For example, ARF provides a licensed financial institution with short -term, circular and USDC -based cross -border payment credit lines. This enables them to settle with international partners in real time while avoiding the challenges of prepaid funds. Cross -border PayFi shows how the PayFi solution uses blockchain to simplify liquidity management, improve operating efficiency, and provide faster and more flexible financial services.

Trade financeTrade finance is the cornerstone of global commerce, enabling enterprises to obtain short -term funds to support operations and growth. Traditionally, these services depend on financial institutions. These institutions may refuse to provide services due to limited credit records or insufficient financial infrastructure, especially in underdeveloped areas. Payfi allows enterprises to obtain instant funds by allowing companies to invoices invoices or future income, and use them as mortgages, thereby solving these obstacles. This method makes acquiring capital democratization, while reducing dependence on traditional loan systems.

An example of blockchain -based trade and financial innovation is Tether's trade and financial plan. Recently, Tether provides finance for a $ 45 million crude oil transaction in the Middle East, using USDT to speed up the settlement and reduce costs. This shows that the blockchain can modernize the global trade flow by reducing costs, accelerating payment time, and increasing transparency. Payfi uses tokenized assets and blockchain infrastructure to create a more easy to access and more efficient trade and financial ecosystem, release new opportunities for enterprises of various scale, and position the industry.

T+0 FinanceDue to the delay in the liquidation of basic assets, even risk -weighted assets (such as national debt) may take two to three days to settle. Payfi applications can be used to solve this inefficient problem by using the liquidity pool to redeem this inefficient problem, thereby achieving the settlement of the day (T+0). Once the basic assets are completely settled, the liquidity pool will be compensated to provide fast and transparent solutions for these transactions.

This function can change the global payment process.For example, companies with complex international supply chains (such as Amazon) often encounter delays when they transfer funds across multiple jurisdictions (that is, from the United States to Britain to Hong Kong). The PayFi solution eliminates these bottlenecks, so that suppliers can receive payment without multiple delays. Similarly, the conversion from the legal currency to stable currency on the exchange and payment platforms can also benefit from the settlement of T+0, which significantly improves the payment experience of enterprises and institutions.

DEPIN FinancialDEPIN project's operating principles are that the cost of building large infrastructure can be distributed to individuals in exchange for future value re -distribution. These projects usually need to contribute bandwidth or hardware such as the network or hardware to compensate the participants with high micro -transaction volume. Payfi products can simplify the financial process behind the DEPIN project by providing financial selection and fast and low -cost micro -diplomatic settlement.

For example, items such as ROAM focusing on the decentralized Wi-Fi network can benefit from it. Users can use the Roam loan to plan to buy the Roam Wi-Fi router mining machine and use mining to reward the loan balance. This process is implemented in two ways: through a 30% stable currency down payment, the remaining 70% of the Huma Finance loans, or 100% loan funded by ROAM or Huma through 4Sol deposit requirements. The user then repays the principal and interest through the Roam airdrop and mining reward. Once the loan is repaid, the user will obtain all the ownership of the router and can start to get all the rewards by providing DEPIN services.

These loans are repaid through mining rewards and Roam airdrops, making participation easier and inspired the contributors. By promoting timely repayment and realizing the complete ownership of hardware after paying off the loan, Payfi plays a key role in supporting the growth and sustainability of supporting the DEPIN ecosystem.

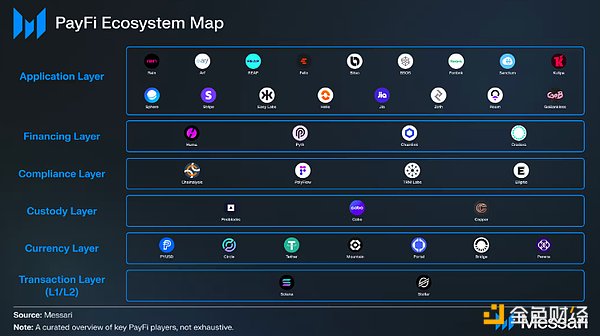

Payfi stack X Payfi ecosystem

Payfi ecosystem can be regarded as a six -layer technology stack. It was originally proposed by Huma Finance that each layer plays a different role to promote to promote to promote Efficient and compliant payment financial solution. The Open Payfi stack provides a blueprint for collaborative layers of clear definition, while maintaining openness and flexibility.

This method is inspired by the early Internet. At that time, the Internet was isolated, closed and unpredictable. The introduction of the OSI model (seven -layer framework) has achieved combined and interoperability, paving the way for countless innovations that can be accessed worldwide today. Similarly, the Open Payfi stack aims to establish a modular and open network architecture for payment finance, accelerate and implement new use cases without the need for each ecosystem participant to operate under the same infrastructure.

Payfi Six -layer stack and project detailed explanation of the project 1.The foundation of the easy layerPayFi stack ensures high throughput, low transaction costs, and rapid settlement -this is the basic attribute of effective payment processing. Blockchain platforms such as Solana and Stellar optimized these requirements and provided solutions such as Solana Pay and Stellar payment platforms to improve payment efficiency.

Solana

The high -performance and high scalability architecture of Solana makes it very suitable for Payfi. The network can handle up to 65,000 transactions (TPS) per second, and the cost of each transaction is usually 0.0024 to 0.048 US dollars. This efficiency can achieve nearly real -time settlement time, which is essential for high -frequency use cases such as retail payment, e -commerce transactions and real -time cash flow management. Solana achieves this performance through its unique parallel transaction processing, which allows the processing to verify multiple transactions at the same time -eliminating the network bottleneck and ensuring that the use rate is consistent with the increase.

Solana also supports infrastructure without licenses and borderlessness, allowing developers to build and deploy payment applications without centralized approval. This promotes the innovation of the global market, eliminates the demand for intermediaries, reduces costs and improves accessibility of enterprises and individuals. Solana provides an ideal framework for the global PayFi solution by supporting cross -border payment.

Solana Pay is a common commercial payment open source framework that promotes direct transactions between merchants and consumers. It is also the core component of the Solana ecosystem to contribute to PayFi. Solana Pay supports stable coins such as USDC and other Solana native SPL tokens, which can achieve low -cost and real -time payment, eliminating delay and high costs brought by traditional credit card systems. The functions of Solana Pay include:

Direct and transparent payment: Merchants can receive payment almost immediately, no third -party participation, and can track all transactions.

Integration with e -commerce: Solana Pay is integrated through platforms such as Helio and Shopify, allowing enterprises to receive online purchase with the least settings.

Wallet interoperability: It supports various walrana -based wallets (that is, Phantom, Solflare, etc.) to ensure that users can use their favorite tools for transactions.

In addition to the convenience of payment, major financial institutions such as VISA, PayPal, Stripe, and Circle have also established Solana integration to strengthen the liquidity in the PayFi ecosystem and ensure that merchants and consumers can obtain stable coins. The integration of Solana and PayPal is to improve the speed, scalability, accessability and cost of PYUSD transactions. This setThe efficiency of PYUSD transactions is to expand its adoption on various platforms and promote the development of the Solana ecosystem. All these Pagrants use the low transaction costs and scalability of Solana to laid the foundation for the new financial model, including the credit system on the chain and programmable payment.

Other innovations related to payment in the ecosystem of Solana include blockchain links (Blinks). Blinks is a feature introduced by Solana that converts the operation on the chain into shared links, so that users can perform blockchain transactions directly from various platforms without leaving the current application or webpage. This innovation is part of Solana Actions, which can promote transactions on the Solana blockchain. Blinks has been integrated into various platforms, including social media and e -commerce websites, which can realize activities such as NFT, exchange tokens and pledge SOL directly from social media timelines.

Solana's infrastructure has improved the existing system and implemented new cases that could not be achieved before. By supporting innovative innovations such as programmable credit, micro -friendship and value exchange, Solana enables developers to create the original financial language, thereby expanding capital acquisition channels, reducing settlement delays, and promoting digital payment in various industries.

In short, Solana's high throughput, scalability and low -cost transactions make it a pillar of payment solutions in the Payfi ecosystem. Its decentralized and friendly infrastructure of developers has promoted innovation, making Solana a natural choice for the future of scalable global payment applications and promoting the future of finance on the chain.

Stellar

Stellar Established in 2014. It is a verified blockchain that is optimized for global payment and is very suitable for the trading layer in the Payfi ecosystem. Stellar's transaction speed is fast (proceed within 5 seconds), low transaction costs (average 0.00005 US dollars), making it an economical high -efficiency and scalable cross -border payment solution. Stellar supports direct point -to -point transactions, while simplifying currency exchange, which is particularly effective in traditional systems with high cost and inefficient remittances and emerging markets.

Stellar's main advantage is its asset tokenization function, which allows users to digitize assets from currency to precious metals and other products. This enables all parties to transfer fast and cheap asset transfer, even across national or currencies. Anchors (Anchors) is a specific term of Stellar, which refers to connecting the Stellar network to the entry/gold channel of traditional financial systems (such as financial institutions or financial technology companies). Accessability.

and Stellar phaseSupplemented by the Stellar Disbursement Platform (SDP), which is an open source batch payment solution. The SDP supports a single operation up to 10,000 transactions, almost instant settlement funds, and operates around the clock. It also invited the creation of wallets through SMS to simplify the entry process of the payee. Through the integration of companies such as MoneyGram, SDP associates digital assets to legal currencies to achieve real -time wages, humanitarian assistance and supplier payment payment.

Soroban, a Stellar smart contract platform launched in March 2024, is another progress of the network, so that it can host smart contracts on the Payfi stack. SOROBAN has added programming to Stellar, allowing developers to build scalable DAPPs to automate and complex financial processes. With the help of Soroban, Stellar now supports the DEFI protocol, decentralized exchanges (DEX) and other financial products. These products used to restrict the functions of the network. These tools allow developers to create DAPP on the application layer of the PayFi stack.

By combining its recognition role as a blockchain centered on payment, the batch payment function of smart contracts and SDP, Stellar has unique advantages and can become a key basic contributor to the PayFi ecosystem trading layer. Essence Stellar infrastructure provides a safer, more efficient, and cost -effective solution for global payment finance. At the same time, it has paved the way for innovative financial primitives to make up for the defects of traditional systems.

2. The currency layer of the currency layerPayfi Dapps is mainly based on USDC, and Pyusd and USDP are also used in some cases. The new PayFi Dapps can integrate other main stablecoins, such as USDT and USDM. In the future, it is expected to integrate other non -US dollars options, such as EURC, XSGD, GYEN, and HKDR. The availability of a variety of stablecoins linked to different currencies enhance the accessability of the entry -exit gold channel, thereby achieving more flexible payment options in addition to the exchange of exchange support from the US dollar. This supports the settlement of international transactions and cryptocurrencies to legal currencies, and improves the realization of global blockchain transactions.

In 2024, the total market value of stablecoin increased by 57%, from $ 130 billion to $ 204 billion. This growth is mainly due to the dominant position of the two major stablecoins. USDT accounts for 68% of the market value share, and USDC accounts for 22%. With the expansion of the stabilized currency market, the scope of use in use based on stable currency construction may increase withdrawal, including PayFi applications. Stablecoin as value storage and exchange mediaThe adoption of intermediaries continues to increase, laying the foundation for applications that leverage these assets.

Monthly stablecoin transfer volume increased by 148% in 2024, from $1 trillion to $2.6 trillion. In December 2024, transfer volume shares were inverse to the stablecoin market capitalization distribution, with USDC accounting for 55% of transfer volumes and USDT at 39%. While the increase in stablecoin transfer volume can be attributed to a variety of factors, USDC’s larger share of transfer volume relative to its market capitalization suggests that it is used more frequently in dapps that require heavy transfer activity. Conversely, USDT has a low share of transfer volume relative to its market capitalization, which may indicate that it is primarily used as a store of value. These trends highlight USDC’s potential as a foundational stablecoin for applications requiring heavy microtransactions. This aligns with the needs of PayFi applications that rely heavily on this type of transaction model, highlighting USDC’s suitability as a currency layer in the PayFi infrastructure stack.

In addition to stablecoins providing a medium of exchange for PayFi dapps, infrastructure providers such as Portal and Perena also ensure the management of stablecoin assets. Portal focuses on infrastructure that helps users transact by connecting traditional and decentralized financial systems using blockchain-based assets.

Portal

Portal provides wallet infrastructure and Web3 interface to help partners enable Web3 functions on their applications. Its SDK allows partners to connect to the protocol and decentralized applications through a mobile or desktop browser. Portal uses multi-party computation (MPC) encryption technology to provide an embedded wallet that does not require a mnemonic phrase, thereby enhancing security and user accessibility.

Portal also supports stablecoin infrastructure and supports the creation of USD stablecoin accounts. These accounts allow users to receive, store and spend wealth in the form of digital dollars, especially in emerging markets. Portal’s infrastructure supports features such as Visa-backed physical and virtual credit cards for local spending of stablecoins, as well as over-the-counter solutions that facilitate the exchange of digital dollars into local currencies. Portal supports use cases such as DeFi swaps, NFT games, and cross-border payments. Portal has partnered with exchanges, fintechs, and developers to facilitate Web3 onboarding and integration while expanding stablecoin accessibility to users around the world.

Perena

Perena is a stablecoin infrastructure provider on the Solana blockchain, dedicated to creating a unified and liquid ecosystem for stablecoins. It solves challenges such as fragmented liquidity in the stablecoin market and inefficient use of capital. At the heart of Perena’s offering is Numéraire, a platform integrated with major stablecoinsof multi-exchange stablecoins, including USDT, USDC and PYUSD. Numéraire (Beta) is an automated market maker (AMM) that creates and exchanges stablecoins, designed to maximize capital efficiency while protecting users from MEV attacks.

Perena innovatively uses a layered Collateralized Debt Position (CDP) system to mint synthetic stablecoins backed by the proceeds from tokenized real-world assets. This approach aims to bridge the gap between DeFi principles and traditional financial systems by converting stablecoin swaps into liquid synthetic dollars. Perena is committed to building a scalable, liquid stablecoin ecosystem on the Solana network.

3. Custody layerThis layer solves the problem of secure storage and management of digital assets, which is crucial to PayFi. Institutional-grade hosting solutions are provided by companies such as Fireblocks, Cobo, and Copper. Features provided by these platforms include multi-party control of assets, secure protocols for asset liquidation in the event of default, and fine-grained account management controls. This sophisticated custody solution is critical for institutional users and is increasingly becoming available to retail and small business users as self-hosted wallet technology advances.

4. Compliance LayerA key challenge in using stablecoins in real-world payments is ensuring compliance with regulations, particularly anti-money laundering (AML) practices. The permissionless nature of assets moving between wallets and blockchains complicates tracking illegal activity, creating blind spots that are difficult for regulators to navigate. Additionally, the centralized structure of many cryptocurrency payment systems introduces custody risks, inefficient fiat settlement integration, and limited service capabilities.

To address these challenges, companies such as Chainalysis, Elliptic, and TRM Labs offer advanced anti-money laundering solutions to improve monitoring and tracking capabilities. Likewise, PolyFlow provides an innovative compliance infrastructure layer tailored for PayFi. PolyFlow provides a modern framework that addresses inefficiencies and risks in traditional cryptocurrency payment systems by decentralizing transaction processing, employing privacy-preserving technologies, and ensuring custodial-free operation.

PolyFlow

PolyFlow is an infrastructure layer designed to enable the direct purchase of goods and services using cryptocurrencies. It focuses on the settlement of funds (whether crypto or fiat) between wallets without relying on bank accounts. It decentralizes real-world transaction processing to reduce centralized custody risks and regulatory blind spots, providing a custody-free model that meets compliance standards.

Key to PolyFlow’s value proposition is its Payment Identity (PID) layer, a decentralized ID linked to encrypted user privacy-preserving KYC/KYB information. This can be done without damagingIn cases of user privacy enhance regulatory compliance. PID helps to establish a credit framework for small and medium -sized enterprises. The strategy is aimed at industries that investors can support, usually insufficient service, and promote financial inclusiveness and growth. Polyflow also solves the inefficient problem in the traditional encrypted payment model by reducing the dependence of the opaque centralized system and minimizing the dependence of traditional legal settlement.

Polyflow has a payment liquidity pool (PLP) for settlement execution, which simplifies the large -scale use of cryptocurrencies, which is suitable for multiple use cases, such as supply chain finance on the Stellar network. By using the tokenization, Polyflow is the liquidity on the "account receivable" assets of "receivables" as the tokenization, and effectively transferred the credit of the business buyer to the upstream supplier, thereby increasing capital availability. By integrating DEFI compatibility, Poyflow generates benefits by providing liquidity for payment transactions, which is a key requirement for using Payfi. PLP combines the multifunctional compliance, privacy protection and service of innovation, and positions itself as a basic compliance protocol in the PayFi ecosystem.

5. The capital layerThe capital layer includes an agreement that enables the borrowing pool to enable the Payfi application by connecting the fund supply and demand. It focuses on management risks, asset pricing, structured, standardization and distribution, making it an important part of the PayFi infrastructure. Humafinance is the leading decentralized lending infrastructure agreement to coordinate the operation of these pools in the PayFi ecosystem. Huma enables the loan to provide capital within a fixed period (such as three or six months). The liquidity provider can obtain a return ranging from 10% to 20%, as shown in the ARF pool on Solana. These income provides funds from the lending costs charged from the Payfi application users. The loan is mortgaged with assets such as future profit and loss sheets, and credit evaluation services such as Credora are verified. Prophecy machines such as ChainLink and Pyth integrate the data on the chain and linked data, support accurate credit assessment and further strengthen this growth cycle.

Huma

The core function of Huma is to allow liquidity provider (LP) to deposit, earn and extract funds, and provide credit services to borrowers. This protocol is different from the traditional DEFI lending platform in several key terms:

Tailoring for Payfi: HUMA focuses on Payfi, provides credit options for credit limit and account receivable support, To meet the demand for specific liquidity in this field.

Modular structured finance: Huma's structured financial module can flexibly adapt to different financial environments, allowing custom repayment plans, cost structure and installment payment. This adaptability makes HUMA applicable to various uses of cross -industryexample.

Advanced Risk Management: Huma’s risk management framework incorporates dynamic valuation agents for evaluating credit. These agents review and approve credit requests, determine credit terms (e.g., limits, terms, interest rates), declare defaults when necessary, and restructure credit terms. The system is designed to effectively reduce risk and maintain borrower accountability throughout the loan process.

Instant Liquidity: Huma provides instant access to funds through efficient liquidity solutions, allowing borrowers to quickly deploy capital.

Compliance and open architecture: Huma works with licensed partners to perform KYC/KYB processes and investor checks to ensure compliance. Its open, modular architecture also enables cross-layer interoperability, facilitating the creation of innovative financial solutions.

For lenders, funding the PayFi app can yield higher yields on users’ USDC than other alternatives such as Ondo, although it carries higher risks due to the possibility of loan defaults on repayments. . Ondo offers an alternative to typical DeFi yield opportunities by introducing tokens collateralized by U.S. Treasury RWAs. For example, OUSG is a tokenized security backed by BlackRock’s U.S. Treasury Bond ETF (SHV), which tracks the performance of short-term U.S. Treasuries maturing within one year. Historically, these yields have been reliable but low and can fluctuate with market conditions, often reflecting broader economic trends such as inflation and changes in Federal Reserve interest rates. This could compress returns during periods of monetary easing.

PayFi dapps generate revenue from PayFi primitives that are essential for many businesses, such as international payments. These primitives play a key role in day-to-day business operations, ensuring demand is stable, supporting sustained returns and reducing exposure to broader economic fluctuations.

These funding tiers allow for real-time evaluation of lenders. This transparency builds lender confidence and attracts institutional participation. This can create a positive flywheel: as more borrowers successfully repay their loans, the credibility of the system increases, thereby increasing liquidity from larger providers.

Huma also supports the application layer of the PayFi stack, including applications that provide a range of PayFi services. One example is Arf, which specializes in cross-border payments. Huma& Arf Financial's monthly payments grew 116% in 2024, from $63 million in January to $136 million in December. Monthly payments in 2024 also increased 108%, from $63 million in January to $131 million in December. Huma’s total on-chain transaction volume has exceeded $2.9 billion.

Rain is a digital asset-backed credit card platform that embodies the PayFi industryHow to use the infrastructure of the PayFi stack, such as the liquidity pool and financial protocol provided by platforms such as Huma. In addition to RAIN, Huma also operates a variety of loan pools tailored for various financial needs, supports small enterprises such as DAPP, JIA and other small enterprises such as DAPP, and ROAM (a decentralized global Wi-Fi roaming network To.

Roam uses Huma to operate the DEPIN hardware financial plan on Stellar to allow users to use the cash flow generated by the Roam product (ie, the Roam Rainier Max 60 router). Users can use the Roam tokens or NFT as a mortgage to obtain loans from Huma, and then use it to buy Wi-Fi hardware. Operators can manage the equipment, make money by rewarding through Roampoints, and repay loans.

In order to give priority to risk management, HUMA focuses on launching low -risk pools to ensure stability and security, rather than increasing the number of available options without distinction.

At present, seven active pools on the blockchain compatible with EVM support the above applications. ARF cooperates with Huma, and their pools are active on Solana and Stellar. Stellar also supports Roam's financial pool, which indicates that the network has increased Payfi in the ecosystem.

6. Application layerPayfi ecosystem is huge scale, and mainly participants have promoted their basic layers of innovation and adoption, such as Stellar, Solana, and Huma. Although the key layer (such as transactions and finance) of Open Payfi stack provides infrastructure for safe and efficient operations, the most critical layer for user participation is the application layer. This layer enables end users to interact with PayFi solutions in various cases, including cross -border payment, remittances, DEPIN finance, trade finance, etc.

This section focuses on some major participants of the Payfi application layer today. The impact of these innovations is the most obvious on users. Although it is not detailed, this overview shows the breadth of the continuous development and evolution of the PayFi ecosystem.

ARF

ARF is a global liquidity platform that provides short -term financing solutions for cross -border payment and focuses on licensed financial institutions. ARF provides liquidity on the chain, which can realize USDC -based settlement based on real -time, low -cost, and no pre -injection accounts. Traditional cross -border payment requires financial institutions to maintain a large amount of capital injection capital in multiple accounts. This is a model of capital dense and inefficient, which hinders scalability and innovation. ARF solves by launching the world's first short -term, cycle, and cross -border payment liquidity solutions based on USDCThis problem eliminates pre-funding and counterparty risk.The protocol has become one of the fastest-growing stablecoin use cases, with over $2.9 billion in on-chain transaction volume and no credit defaults to date. Arf ensures a faster, cheaper and more reliable payment process with fully traceable same-day settlement through on-chain transparency. Arf’s liquidity pool currently offers annual interest rates of 10% to 20% while maintaining healthy gross margins. Backed by prominent investors such as Circle Ventures and Stellar Development Foundation, Arf aims to democratize access to liquidity and promote financial inclusion globally.

Arf has demonstrated strong capital efficiency, achieving rapid turnaround of 50 cycles per year and processing $1.5 billion in loan volume. It had average liquidity of $30 million in December 2024 and plans to expand this to $200 million to $250 million in 2025.

Bitso x Felix

Felix, a payments platform based on WhatsApp, and Bitso, a cryptocurrency exchange with more than 5 million users, have partnered to revolutionize remittance payments in Latin America. The traditional money transfer process is slow and costly, often requiring users to travel to a physical location, pay high transaction fees ($10 for an average transfer of $300), and handle cash, which can pose security risks. Felix provides a safe and affordable remittance solution by integrating Stellar payment channels, USDC and Bitso’s inward/outward channels.

Using Felix, US users can send money directly through WhatsApp by interacting with an AI bot that collects transaction details and provides a secure payment link. Payments are made using a debit card, and once completed, funds are collected in U.S. dollars, converted to USDC in Felix’s Bitso account, and then converted to local currencies such as Mexican pesos. These funds are sent through local banking channels (such as SPEI in Mexico or other/region-specific systems) and deposited into the recipient's bank account.

This solution significantly reduces the time and cost of cross-border payments, allowing funds to arrive within seconds. With a user-friendly platform and extensive local bank integrations, Felix and Bitso ensure widespread access to remittances across Latin America, increasing financial inclusion and creating a faster and easier cross-border payments experience for senders and recipients.

Airtm x Bridge

Paying workers in areas with volatile currencies and high inflation is a huge challenge for both employers and employees. Employers need a reliable, efficient way to meet global payroll requirementsdemand, while workers need to be paid promptly to preserve value and be able to withstand the effects of local currency instability. Traditional cross-border payment systems are slow, costly and often unable to penetrate emerging markets. They also involve complex compliance processes, expensive currency conversions, and technical barriers to integrating with modern payment networks.

To address these challenges, Airtm and Bridge have developed a cross-border payments platform powered by the Stellar network. Airtm is a fintech company that provides users with globally connected digital dollar accounts, enabling them to receive payments, access funds in e-wallets and convert funds into local currencies. Users can deposit funds through more than 400 methods, withdraw funds almost instantly, and send or request payments from other Airtm users. By integrating Bridge’s stablecoin orchestration services, the platform ensures efficient currency conversion between fiat currencies and stablecoins such as USDC or USDP, providing secure and inflation-proof payment options.

The platform leverages Stellar’s low-cost and instant payments infrastructure and is powered by the power of Airtm. Users can withdraw funds peer-to-peer to digital wallets, cryptocurrencies, and more. They can also transfer funds directly to local bank accounts in 15 countries including Argentina, Brazil and Mexico. By combining Airtm's global financial instruments, Bridge's stablecoin services and the Stellar network, the solution enables individuals and businesses in emerging markets to earn money quickly, affordably and reliably.

BSOS

Founded in 2018, BSOS is committed to driving the growth of the supply chain of fintech solutions and providing liquidity to startups through blockchain and DeFi. BSOS’s green finance pool allows qualified investors to finance projects such as ChargeSmith, Taiwan’s electric vehicle charging station network, using short-term credit loans backed by projected revenues. ChargeSmith, which aims to have 1,500 charging stations by 2025, relies on BSOS and Huma to secure the credit it needs to expand. The green finance pool provides monthly interest, with collateral backed by charging stations and management revenue. BSOS also combines enterprise resource planning with on-chain liquidity to enable short-term trade finance.

Easy Labs

Easy Labs is a Web3 financial contract automation platform that helps teams build and manage complex payment processes. The platform helps Web2 and Web3 teams reduce transaction costs, scale operations, earn passive income on assets, accelerate payment settlement, and facilitate cross-border transactions while gaining greater visibility into the flow of funds across the organization. Easy Labs aims to bring Web3 efficiency to traditional Web2 enterprises.

Fonbnk

FONBNK is a global market that allows users to convert mobile call time into digital currencies, combine Web3 technology with super local payment methods to achieve fast, safe and US dollars. FonbNK is supported by Nigeria, Kenya and South Africa, and operates on Payfi blockchain pillars such as Stellar, Solana, and Celo, aiming to completely change cross -border payment and promote financial inclusiveness. The platform enables users to exchange call time with trusted city merchants, convert it to stablecoin, can deposit into digital wallets, exchange for local currency or to access DEFI services.

FonbNK's gold -entry process allows users to transfer funds to agents and receive stablecoins in their wallets. At the same time, its gold -out function allows cryptocurrencies to be exchanged back to the legal currency co -deposited into bank accounts or other specified methods. With its fast and safe mobile recharge service and the integration of stable coins, FonbNK enables individuals in emerging markets to easily access digital and traditional financial systems to promote financial inclusiveness and innovation.

Gobankless

Gobankless is a digital bank platform that uses blockchain technology to realize the point -to -point payment and stable currency transactions from all over Africa. The platform provides instant cross -border payment, USDC to cash exchange and cash delivery services, which has functions such as real -time capital, prepaid digital cards, and customs clearance integration. Through the maximum reduction of expenses and providing tailor -made solutions, Gobankless enables enterprises and individuals to obtain efficient and affordable financial services.

For Africa's financial ecosystem, Gobankless plays a vital role in promoting financial tolerance by providing convenient tools for banks and without bank services. In fact, time and low -cost payment solutions support SMEs, improve cash flow management and improve operating efficiency. In addition, the application also promotes economic growth by empowering the informal economy and the realization of the interoperability between different financial platforms. Gobankless promotes the innovation and accessibility of the African financial sector, while promoting wider economic activities.

Helio

Helio is a self -service platform that allows merchants, creators and developers to receive USDC and hundreds of digital currencies. And high -end Web3 features and other characteristics. HelioPay supports integration into the e -commerce system to provide chain checkout and custom transaction infrastructure for markets, DEX and high -traffic applications. Helio supports Solana, Bitcoin, Ethereum and Polygon, providing real -time payment, with a transaction fee of 1%, eliminating the risk of refund. The platform runs the official Solana Pay plugin that runs SHOPIFY, and integrated supporting merchants through non -code -free integration to make more than 6,000Name sellers benefited, with annual sales reaching $1.5 billion. Helio’s funding includes a $3 million seed round in April 2023, and its NFT subscription HelioX reduces transaction fees for merchants.

Jia

Jia is a blockchain-based microfinance platform that provides small business loans to businesses in emerging markets, with a focus on Kenya and the Philippines. Jia provides income support loans to help businesses grow or stay afloat, serving the medical clinics, consumer goods, food and beverage, and transportation industries. An example client might include a medical clinic that needs short-term capital to purchase supplies, which can be a challenge without affordable financing. Borrowers who repay their loans will be rewarded with Jia tokens to incentivize timely repayment while promoting community ownership in the lending ecosystem.

Rain

Rain provides a digital asset-backed credit card solution that allows businesses (primarily Web3 companies and DAOs) to leverage Polygon to use stablecoins such as USDC wherever Visa is accepted. The cards provide quick, low-cost payment for things like corporate travel and are integrated into mobile wallets like Apple Pay and Google Pay. Rain reinvents spend management for the Web3 team by offering a USDC-backed corporate card, where corporate funds are collateralized by assets to set credit lines and liquidated on-chain at the end of each settlement period. Rain has partnered with Huma Finance as a liquidity provider to provide an accessible solution for crypto-native organizations that require fiat transactions without relying on traditional credit card assets.

Reap

Reap is a Hong Kong-based financial management platform that provides businesses with a set of tools to streamline payments, expense management and cash flow operations. By connecting traditional banking and digital assets, Reap provides enterprises with solutions tailored for Web2 and Web3.

Their main product is the Reap Card, a secured Visa business credit card that is collateralized by fiat currency or stablecoins such as USDC, providing businesses with access to credit without relying on traditional banks. The card supports flexible repayment in fiat currency or digital currency, which can meet diverse operational needs. With Reap Pay, businesses can make global payments (such as rent or wages) without a bank account, using stablecoins to reduce reliance on the traditional banking system. The platform’s Reap Treasury integrates fund management through different balances in Reap Card, Reap Pay and general funds to enable seamless transfers to optimize liquidity and payment capabilities. Reap supports transferring USDC and USDT on Solana, Ethereum, Polygon, and transferring U on TronSDT.

Reap combines innovative payment infrastructure with strong security and privacy functions to provide enterprises with comprehensive financial management solutions in the traditional and blockchain financial environment.

Sanctum

Sanctum is a platform that supports the issuance and transaction mobile pledged token (LST) on the SOLANA blockchain. Its functions include zero -slip point transactions and revenue through the deposits of LST. The platform integrates with Jupiter and Solflare. It allows teams, creators, and DAO to create LST and get pledge rewards from token holders to provide innovative tools for monetization and community participation.

In the PayFi ecosystem, SANCTUM's Creator Coins provides a sustainable and non -licensed way for creators. Essence This ensures stability and reliability, while allowing creators to obtain predictable returns from pledge income. Supporters holding these tokens can get exclusive content, benefits and experiences, thereby promoting a deeper connection between creators and fans. Creator Coins also creates tangible value through surpassed speculative transactions, highlighting the practicality of cryptocurrencies in the real world.

For example, HealthSol, this is a healthy charitable plan that allows users to hold HealthSol and donate pledge rewards to public health programs for emerging markets, and Flojo. This is a healthy beverage brand that uses Creator Coins Establish a loyal community while bypassing traditional advertisements. By using its unified liquidity layer, Sanctum guarantees 1: 1 tokens to support SOL.

Sphere

Sphere is a blockchain -based payment platform. It is based on the Solana blockchain and aims to promote the commercial transactions of cryptocurrencies and legal currencies. It provides legal currency entrances, regular subscriptions and API integration to support the payment of cryptocurrencies and legal currencies. Sphere focuses on simplify cross -border transactions and reduce TRADFI's high costs and processing time. Sphere initially supported the HELIUM and other DEPIN networks, allowing users to conduct legal currency transactions without holding native token. It also aims to extend its services to other depins, including HiveMapper and Render, and also become a comprehensive API for currency swap and cross -chain payment. Sphere supports more than 120 major credit cards (VISA, MasterCard, American Express, Discover), bank transfer and electricity exchange, focusing on the development of the developing economies.

On the basis of its core products, Sphere launchedSpherenet, a permissioned blockchain solution built on the Solana Virtual Machine (SVM) and designed for regulated financial entities. Spherenet is a trust-neutral, privacy-preserving, and natively compliant shared account ledger. Spherenet facilitates the discovery, verification and universal settlement of licensed counterparties at near-instantaneous speeds. Developed by a global consortium of regulated institutions and fintechs, Spherenet provides a secure, compliant infrastructure for cross-border trade finance and emerging market transactions. With advanced features like confidentiality transfer and delegated authority, Spherenet ensures privacy while ensuring judicial compliance. Spherenet currently operates in 14 emerging and developed jurisdictions, underscoring Sphere’s mission to connect traditional finance and blockchain to enable regulated institutions to integrate into PayFi.

Zoth

Zoth is a blockchain-based platform that connects TradFi and DeFi by tokenizing RWA to provide liquidity solutions and high-yield investment opportunities. Founded in 2023, Zoth provides institutional and accredited investors with secure fixed income products such as trade finance receivables, U.S. Treasuries and corporate bonds. Zoth’s products include ZeUSD, a stablecoin backed by high-quality RWA, and a $100 million tokenized liquidity note (ZTLN) backed by U.S. Treasuries and corporate bonds. With $106 million in assets, a 91% reinvestment rate and a 0% default rate, Zoth aims to create safe and efficient financial products integrated into the blockchain ecosystem.

The future of PayFiAs the variety of products increases and user adoption increases, the scale of PayFi will continue to expand. This section highlights the specific use cases and applications expected to make significant progress in 2025, as well as the key ecosystem developments that will drive and support this growth.

T+0 settlement

PayFi’s future may involve transforming cross-border transactions through T+0 settlement. Currently, cross-border payments take two to three days to settle, causing inefficiencies and cash flow challenges. Protocols that leverage PayFi’s six-layer infrastructure stack directly address these issues by enabling same-day settlement. This could streamline global payments processes in a way that today’s financial system cannot.

This feature is particularly useful for multinational companies operating complex supply chains across multiple jurisdictions. For example, businesses like Amazon often handle multi-step payment processes, which can lead to operational delays due to settlement bottlenecks. T+0 Finance removes these barriers, ensuring seamless, real-time transactions and improving operational efficiency at scale.

As the T+0 settlement solution develops, it may set a new benchmark for financial innovation and become theKey differentiation factor of FI ecosystem. By providing the speed of settlement that cannot be compared with traditional finance, T+0 Finance makes PayFi a leader who promotes the innovation of global payment systems. Its success may catalyze a wider range of adoption, showing the potential for changing financial solutions based on blockchain.

Market Education

Many protocols in the Payfi ecosystem use the technology of Tradfi, DEFI, and RWA to create favorable interoperability for building an innovative solution. However, this overlapping may be blurred, and it is difficult for users to distinguish Payfi's specific products and products rooted in other industries. A typical example is the comparison between AAVE's DEFI borrowing agreement and JIA. JIA is a small enterprise financing platform focusing on PayFi. It provides funds for the loan with the assets of tokenized "accounts receivable" as mortgage. Payfi needs to coordinate and work hard to educate the market's unique cases to establish a clear identity. Payfi infrastructure stacks and industry conference tools are essential for improving popularity and promoting the industry's growth.

In 2025, multiple agreements/chains participating in the PayFi ecosystem will focus on increasing popularity and conveying the value proposition of the industry by actively participating in the major industry conferences. These include Huma, Solana Foundation and Stellar Development Foundation. They plan to host PayFi activities in the near future:

February 2025: Hong Kong Consensus

May 2025: Dubai token 2049

September 2025: Singapore token 2049

November 2025: Meridian

December 2025: Abu Dhabi Breakpoint

These activities will provide the opportunity to show Payfi sustainable development and interact with major stakeholders.

Regulatory development

One of the focus of 2025 will be the supervision and development of monitoring and adapting to the jurisdiction area. Payfi's most important regulatory changes will be concentrated in the application of stable currency supervision and the application of cryptocurrency travel rules in cross -judicial jurisdictions. These frameworks are essential to allow financial institutions to be able to use stablecoins comply with stablecoins for payment. Clear supervision and guidance will accelerate the use of stable coins, especially in the UAE and other regions. The progress of these regions has encouraged agencies to participate in the Payfi and RWA fields. This clarity is expected to promote the growth of ecosystems by expanding its participation in Payfi to provide Payfi.

In addition, the recent regulatory framework (such as the EU's MICA regulations) has created a more fit for RWARegular environment. Switzerland, Luxembourg, Liechtenstein, and Singapore have launched eye -catching compliance megacities. In October 2024, the World Economic Forum (WeF) announced that Australia, Britain, Brazil and South Korea have promised to launch new regulatory frameworks. In addition, Trump may adopt the approach that is conducive to innovation may bring stable currency legislation, provide clarity and enhance institutional trust. If this is implemented, it may greatly improve the US regulatory framework and create a more favorable environment for blockchain -based payment systems.

Projects in the field of Payfi will give priority to maintaining agility and compliance to cope with these continuous development frameworks. This includes a standardized legal agreement for the establishment of assets of tokens to simplify transactions and enhance investor confidence.

End languagePayfi represents a changeable payment financial method, which not only solves the inefficient problem in traditional systems, but also achieves new use cases. With the continuous improvement of stable currency, the increasingly mature blockchain infrastructure, and the continuous improvement of regulatory transparency, Payfi is expected to promote major innovation in the global market.

With the basic support of main participants such as Huma, Solana, and Stellar, and a good indicator adopted quickly, PayFi is expected to expand its influence in 2025 to provide global enterprises and individuals with scalable, efficient and accessible access to access. Financial solutions.