50 mins ago

7,593

In traditional finance, the lending market provides short-term lending opportunities, usually for highly liquid and low-risk assets, aiming to provide safety and the highest possible returns. In decentralized finance (DeFi), this concept has evolved to mainly refer to the ability to lend and borrow various digital assets in a decentralized and permissionless environment without specific time limits. These platforms allow users to deposit cryptocurrencies into the protocol, with borrowers paying interest to depositors in exchange for providing sufficient collateral.

The lending market uses a dynamic interest rate model to automatically adjust lending rates based on the liquidity utilization of a certain market or pool. These models ensure efficient allocation of capital while incentivizing borrowers to return borrowed assets when liquidity is tight. A key feature of this interest rate model is the "kink point", where when utilization reaches a certain critical value, interest rates begin to rise significantly to control the leverage in the system: as utilization rises, interest rates may It increases gradually, but once the inflection point is exceeded, interest rates spike rapidly, causing borrowing costs to rise significantly.

It should be noted that the lending market is different from unsecured loans: the lending market requires borrowers to provide collateral to secure the loan to ensure that the loan can be obtained at any time during the loan term. Repayment; while unsecured loans (usually referred to as traditional loans) allow customers to borrow money without providing collateral (or only providing part of the collateral or other guarantees), and the repayment of the borrowed money relies on credit scores and legal channels to guarantee it.

Lending market: the basic "Lego" in the DeFi ecosystem

Lending market in DeFi The importance is mainly reflected in its ability to help users earn income from idle assets and unlock liquidity without selling the assets they hold. This feature plays a crucial role in DeFi capital efficiency. The ability to borrow against a specific token is one of the most sought-after features in the industry, and is often an important criterion in determining whether a crypto asset is a “blue chip” asset.

This feature allows users to obtain leverage at a low cost, helping high net worth individuals (HNWIs) incorporate assets into tax planning, while also allowing those with abundant but liquid assets to Teams with insufficient liquidity are able to borrow against their treasury and holding assets to support operating capital, and in the process earn interest on the collateral (for example, Curve and Maker are two typical cases in the past few years) ).

In addition, the lending market serves as the backbone for other DeFi instruments such as Collateralized Debt Positions (CDPs), yield farming strategies (supporting many near-"delta neutral" strategies), and on-chain margin trading. Therefore, lending and borrowing The market is one of the most important building blocks of DeFi, also known as the "funding building block"

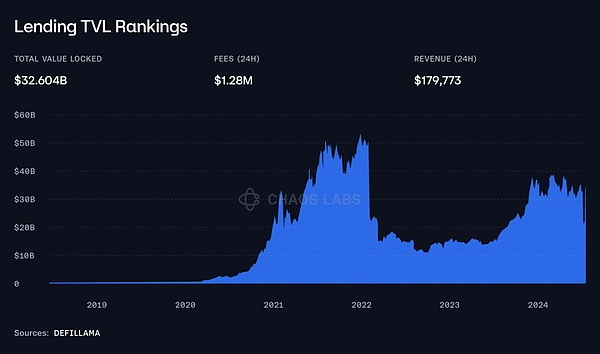

To give everyone a clearer understanding of the size of these lending markets, the total value locked (TVL) in crypto lending protocols currently exceeds $32.6 billion, as shown in the figure below.

Source: Devillama

Design decisions for the crypto lending market : Shared liquidity pool and isolated liquidity pool

While cryptocurrency lending markets all serve the same basic purpose, there are significant differences in the design of liquidity structures. The biggest difference is between markets that use a single shared liquidity pool (like @Aave) vs. segregated liquidity Each model has its own trade-offs, including liquidity depth, asset flexibility and risk management.

Isolated liquidity pools: flexibility and risk isolation

In the segregated liquidity pool model, each market or asset operates within its own independent liquidity pool. This approach is adopted by protocols like Compound v3 and even more extreme ones. Examples are platforms such as Rari Capital (before its collapse)

The main advantage of segregated liquidity pools is their flexibility in building sub-markets. This flexibility enables protocols to create markets tailored to specific asset classes or user needs. For example, segregated liquidity pools can Specifically designed to support a specific asset group, such as meme tokens, or only allowing the existence of certain types of tokens due to unique risk characteristics or needs

This kind of customization is one of the biggest advantages of segregated liquidity systems, as it allows projects to be tailored to specific communities or circuits that may not fit within the broader shared liquidity pool. Framework. With LRTs (Liquidity Return Tools) and tokenized underlying transactions likeThis advantage has been particularly demonstrated with the rise of USDe): many users want to take advantage of the high yields, but are unwilling to take on the risks associated with new assets.

In addition to flexibility, segregated liquidity pools also provide better risk isolation. By isolating each market, the risk of any particular asset is limited to its corresponding liquidity pool. This means that if the price of a certain token drops sharply or becomes too volatile, the potential impact is limited to that market and does not ripple to other parts of the protocol.

However, these benefits also come with costs, as isolating liquidity is a double-edged sword, which also means fragmentation of liquidity pools.

For isolated markets, every market must face the "cold start" problem - this is not just a one-time challenge, but every time These are all faced when creating a new market. Each market can only rely on its own participants, and liquidity may not be enough to support large-scale lending activities.

Source: Solend — limited liquidity available on isolated markets

As mentioned earlier, some protocols have taken the concept of segregated lending markets to the extreme, enabling permissionless market creation.

In these cases, such as Rari or @Solendprotocol, users can create their own permissionless markets, decide on whitelisted assets, and set risk parameters (such as loan value than LTV and mortgage ratio CR), and manage the corresponding incentive mechanism.

Shared Liquidity Pools: Deep Liquidity from Day One

Another On the other hand, a single shared liquidity pool provides deep, ready-to-use liquidity from the start. By integrating all assets into a unified pool, the shared liquidity system is able to support large-scale lending activities with fewer liquidity constraints, even for newly added assets.

Lenders also benefit from the shared pool: a larger liquidity base attracts more borrowers, thereby generating higher yields, which Earnings are also generally more stable because theySupported by diversified borrowing needs.

This is the main advantage of the shared liquidity model, and although it is the only advantage, the importance of this cannot be overemphasized. In every market, liquidity is king, but it is even more important in crypto markets.

However, the main disadvantage of shared liquidity pools is systemic risk. Since all assets are tied into the same pool, a problem with one asset (such as a sudden devaluation) could trigger a cascade of liquidations, which could affect the entire system if bad debts arose.

Thus, these pools are less suitable for niche or more experimental assets, especially compared to liquid, mature tokens .

Finally, governance and risk monitoring of shared liquidity systems are often more complex, as any changes to the protocol involve greater risks.

Model combination: exploring hybrid models

Between isolated liquidity pools and shared liquidity pools The trade-offs vary significantly, and no one approach is perfect. This is why, as the market matures, the lending market is gradually moving towards hybrid models (or at least introducing hybrid features) to balance the liquidity advantages of shared pools with the customization and risk isolation provided by segregated markets.

A typical example of hybridization is the customized isolation market introduced by Aave, which cooperates with platforms such as @LidoFinance and @Ether_Fi. Aave's systems typically use a single shared liquidity pool to provide deep liquidity for major assets. However, Aave also recognizes the need for greater flexibility when supporting assets with different risk characteristics or application scenarios, thus creating markets for specific tokens or collaborative projects.

Another key feature of @Aave that fits this trend is the eMode design. eMode is designed to optimize capital efficiency when trading with underlying assets. Specifically, eMode allows users to unlock higher leverage and borrowing capabilities on assets with higher price correlations (thus, the liquidation risk of these assets is significantly reduced), significantly improving capital efficiency by isolating specific positions.

Other protocols like @BenqiFinance and @VenusProtocol,Traditionally in the shared liquidity category, it has taken a significant step forward by introducing segregated pools for specific sub-tracks. In these cases, segregated markets are tailored for niche areas such as GameFi, Real World Assets (RWA), or “ecosystem tokens” without impacting the operations of mainstream pools.

At the same time, segregated market lending platforms like Compound or Solend usually have a "main pool" as a shared liquidity pool, or in Compound's Case in point, they have recently started adding more assets to the most liquid pools and are actually moving towards a hybrid model.

Note: Solend initially adopted a shared liquidity model and later changed its design.

The business model of the cryptocurrency lending market

The core business model of the crypto lending market revolves around Generate income through multiple mechanisms related to lending, collateralized debt positions (CDPs).

1. Interest rate difference: The main source of income in the lending market is the difference between lending rates. Users can earn interest by depositing their assets into the protocol, while borrowers pay interest to obtain liquidity. The protocol makes money from the difference between the interest rate borrowers pay to borrow and the interest rate depositors receive on deposits. This spread is usually small, but the benefits accumulate as more users participate in the protocol. For example, in the Ethereum market of Aave v3, the deposit rate for $ETH is 1.99%, while the borrowing rate is 2.67%, resulting in a 0.68% spread.

2. Liquidation fees: The lending market also generates additional income through liquidation fees. When a borrower's collateral falls below required thresholds due to market volatility, the protocol initiates a liquidation process to maintain the solvency of the system. The liquidator pays off part of the borrower's debt in exchange for discounted collateral. Typically, the protocol receives a portion of this reward, and in some cases, the protocol itself runs a liquidation bot to ensure timely liquidation and generate additional revenue.

3.CDP related fees: Some protocols charge specific fees for their CDP (Collateralized Debt Position) products. These fees come from the interest on borrowed CDP assets. It may be a time-based fee or a one-time fee (or both).

4. FlashFlash loan fees: Most protocols allow users to make flash loans for a small but very lucrative fee. Flash loans are essentially loans that need to be paid back in the same transaction, allowing users to instantly access the capital they need to perform specific operations (such as liquidation).

5. Treasury income: The protocol sometimes uses its treasury to earn income, usually choosing the safest method of return.

It is these mechanisms that make the lending market one of the most profitable protocols.

These fees are sometimes shared with governance tokens or redistributed through incentive mechanisms , or used to cover operating expenses.

Risk<> Lending Market

As mentioned earlier, the business of operating the crypto lending market Can be one of the most profitable, but also one of the riskiest businesses.

One of the first problems facing the emerging lending market is the "cold start" problem.

The cold start problem refers to the difficulty in initiating liquidity in a new protocol or market. Early adopters are often reluctant to put money into pools that are not yet large enough due to concerns about illiquidity, limited borrowing opportunities, and potential security breaches. Without sufficient initial deposits, interest rates may be too low to attract borrowers, and borrowers may find it impossible to obtain the loans they need, or face interest rates that are too volatile due to changes in liquidity.

Protocols usually solve the cold start problem through liquidity mining incentives. Users receive native tokens as rewards for providing liquidity or borrowing liquidity (one of the parties’ Incentives affect the other party indirectly, especially where revolving lending is possible). However, if these incentives are not effectively managed, it can lead to unsustainable token issuance, which is a trade-off that protocols need to consider when designing their launch strategy.

Timely liquidation is another key element in maintaining the solvency of the agreement. When the value of a borrower’s collateral falls below a certain threshold, the protocol must liquidate it to prevent further losses. This mainly faces two problems:

First of all, this processThe success of the process relies heavily on liquidators – whether operated by the parties to the agreement or managed by a third party – who need to monitor the agreement in real time and execute liquidations quickly.

Source: Chaos Labs Benqi Risk Dashboard

In order to ensure that liquidation can proceed smoothly, liquidators need to receive sufficient incentives through liquidation rewards, and these rewards must be balanced with the income of the protocol.

Second, the liquidation process must be triggered when it is financially safe to liquidate: if the value of the seized collateral is comparable to, or nearly equal to, the outstanding debt , then the risk of the position slipping into the bad debt area will increase. In this process, it is crucial to define safe and up-to-date risk parameters such as loan-to-value ratio (LTV), collateralization ratio (CR), and set liquidation buffers between these parameters and liquidation thresholds. At the same time, the asset whitelist on the platform needs to go through a strict selection process.

In addition, in order to ensure the smooth operation of the protocol, ensure that liquidations occur in a timely manner, and prevent users from abusing functions, the lending market relies heavily on functional oracles , provides real-time valuation of collateral and indirectly reflects the health and liquidability of loan positions.

Oracle manipulation is an important risk, especially in less liquid assets or protocols that rely on single-source oracles, where attackers can distort price to trigger liquidations or borrowing with incorrect collateral levels. Several similar incidents have occurred in the past, with the most famous example being Eisenberg's exploit of the Mango Markets vulnerability.

Latency and latency are also key factors; during times of market volatility or network congestion, delays in price updates can lead to inaccurate valuations of collateral, causing lags or The liquidation of mispricing ultimately resulted in bad debts. To deal with this problem, protocols often adopt a multi-oracle strategy, aggregating information from multiple data sources to improve accuracy, or setting up backup oracles in case the primary data source fails, while also using time-weighted prices to feed prices. Filter out sudden changes in asset value caused by manipulation or outliers.

Finally, we also need to consider security risks: among projects that suffer attacks, the currency market is usually the main victim, second only to cross-chain bridges.

The code that governs the lending market is extremely complex, and only a few protocols can proudly claim to have an impeccable background in this area. At the same time, we have seen many protocols, especially forks of some complex lending products, encounter multiple security vulnerabilities when modifying or processing the original code. In order to reduce these risks, protocols usually take measures such as bug bounties and regular code audits, and use strict processes to approve protocol modifications. However, no security measure can be foolproof, and the potential for vulnerability attacks is always an ongoing risk factor that a team needs to be careful about.

How to deal with losses?

When a protocol encounters a loss, whether due to bad debts due to liquidation failure or emergencies such as hacker attacks, there is usually a set of standard mechanisms to Share losses. Aave’s approach can be used as a typical example.

Aave's Safety Module serves as a reserve mechanism to make up for possible funding gaps in the protocol. Users can stake AAVE tokens in the security module and receive rewards, but these staked tokens may be slashed by up to 30% to cover shortfalls if needed. This acts as an insurance mechanism and has recently been further enhanced with the introduction of stkGHO.

These mechanisms essentially provide users with "high-risk, high-reward" opportunities and align the interests of users with the interests of the protocol as a whole.