55 mins ago

8,290

Author: Delphi Digital; Compiler: 0xxz@金财经

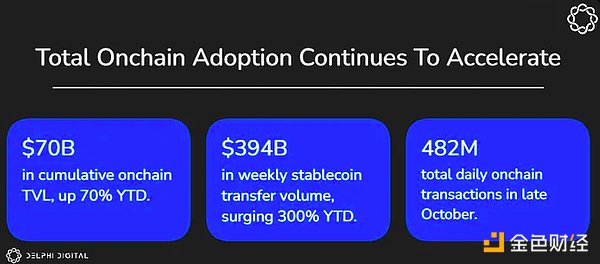

IntroductionIn 2024, the on-chain economy has grown significantly, with daily transaction volume increasing by more than 50% year-to-date, and the total value locked on the chain (TVL) With a growth of 70%, the total TVL of all major networks exceeds US$70 billion. These major networks include Bitcoin, Ethereum, Solana, Arbitrum, Avax, Base, Binance Smart Chain, Cosmos, Optimism, Polygon, Sei, and Sui. The World Economic Forum predicts that 10% of global GDP will be on-chain by 2027, a prediction further confirmed by reports from the International Monetary Fund and the World Bank on the global shift to digital infrastructure.

This report delves into the recent growth of the on-chain economy through October 2024 and analyzes several use cases behind this growth, including stablecoins, L2 , collectibles, social media, gaming, DeFi and institutional adoption. Overall, the data is clear: the on-chain economy is growing rapidly.

This report also provides an in-depth look at Base’s recent developments. Base is an Ethereum L2 incubated by Coinbase that has experienced significant growth since launching its mainnet on August 9, 2023.

“Base is a secure, low-cost, developer-friendly Ethereum L2 designed to serve one billion users and one million chains ”

In the approximately one year since Base was launched, it has positioned itself at the forefront of the L2 field. During this time, the Base team has contributed to progress on multiple chains: reducing rollup transaction fees to less than 10 cents via EIP-4844, creating smart wallets to simplify account abstraction, contributing to the hyperchain stack, and more. Daily transaction volume on Base has grown 1,600% since early January, from 372,000 to more than 6.63 million in October. Of the many metrics analyzed, Base is growing faster relative to the overall on-chain economy (such as TVL, active addresses, and transactions).

The growth of the on-chain economy is not limited to financial speculation. 66% of all active on-chain applications are non-DeFi, such as gaming, social, and digital collectibles. DeFi applications account for 33% of on-chain applications on major networks.

As new use cases continue to emerge and developers and users continue to get on-chain, the on-chain economy will accelerate in the coming months and years.

Overview of the overall economy on the chainOn-chain indicators

Total TVL on the chain

Total locked value(TVL) is a metric used to evaluate the amount of capital allocated to smart contracts on a specific network. Year-to-date, cumulative TVL across networks has grown from $41 billion to more than $70 billion, a 70% increase. TVL grew 110% to $87.9 billion as of November 19.

As the total TVL on the chain surges, Base’s growth is particularly prominent. TVL on the Base chain increased from $439 million in January 2024 to $2.51 billion at the end of October 2024, an increase of 470%. As a result, Base’s market share increased from 1.07% of total on-chain TVL to 3.59%.

It is worth noting that although on-chain growth is driven by Base, this is mainly reflected in active addresses and stablecoin transaction volume. This is because on-chain TVL on Base is still relatively low compared to other major networks - reflecting the greater mix of non-monetary use cases on Base.

This significant rise stems from increased usage of Base in general and, more specifically, the rising popularity of Aerodrome, which currently accounts for over 40% of Base TVL.

Total number of active addresses on-chain

Year-to-date, the total number of weekly active addresses on-chain has increased from 19.3 million to approximately 60 million, a 210% increase. Weekly active addresses grew 240% to 65.6 million as of November 19.

Note: As a reminder, the active address refers to the active interaction address of the project's revenue-generating smart contract within a given time period. Active addresses are not equivalent to weekly active users, as users may create and operate multiple wallet addresses.

Meanwhile, Base’s weekly active addresses increased from 300,000 in January to 6.61 million at the end of October, a 2,100% increase. This increased Base’s market share of the total weekly active addresses on the chain from 1.6% to 11%.

Note: Daily new addresses refer to newly created interactive addresses within the 24 rolling cycle, which interact with smart contracts that generate revenue. These addresses have not previously indicated any on-chain activity on the network.

So far this year, the total number of new daily active addresses has increased from 710,000 to 6.95 million, an increase of 879%.

During the same period, Base’s daily new active addresses increased from 8,320 at the beginning of the year to 450,000 at the end of October, an increase of 5,300%. This increased Base's market share from 1.2% to 6.5%.

Total number of transactions on the chain

The number of transactions is determined byQuantified by evaluating the number of trades made within a given time frame.

So far this year, the cumulative number of weekly transactions has increased from 315 million at the beginning of the year to 482 million, an increase of more than 50%. As of November 19, the number of weekly on-chain transactions so far this year has increased by more than 60% to 531 million.

During the same period, Base’s daily trading volume increased from 2.1 million at the beginning of the year to 42.34 million at the end of October, an increase of more than 1,900%. This increased Base's market share from 0.67% to 9%.

Base's huge increase in daily transaction volume shows that the network's popularity and affordability are rising, but the broader trend also highlights that Base can succeed while enabling other networks to succeed ( For example, other networks in the hyperchain).

Total deduplication of stablecoins

A key area of on-chain economic growth is stablecoins, which enable on-chain assets to be moved seamlessly around the world at a fraction of the cost of traditional finance flow. Year-to-date, total deduplicated on-chain stablecoin weekly trading volume has increased from $89.7 billion to $249 billion, an increase of more than 177%.

As of November 11, weekly stablecoin transfer volume was 302 billion, up more than 235% year-to-date.

Note: Deduplicated stablecoin trading volume is quantified by evaluating the cumulative sum of stablecoin transfer values while removing duplicates. Removing duplicates is critical to analyzing accurate volume numbers. Duplicates are transfers that are considered uneconomic activities, such as CEX transfers, bot activity, fake transactions, and non-payment wallet transfers.

Stablecoin growth on Base has also accelerated rapidly: During the same time period, Base’s cumulative weekly stablecoin trading volume increased from $620 million in early January to 10 US$62 billion at the end of the month, an increase of more than 9,800%. This increased Base's market share from 0.7% to 33%, a 47-fold increase.

As of November 11, Base’s cumulative weekly stablecoin trading volume increased from $620 million in early January to $55 billion in November, an increase of more than 8,800%. This increased Base's market share from 0.7% to 18%.

The increase in Base stablecoin transaction volume reflects Base’s efforts to reduce costs while increasing network capacity. As a result, Base can leverage stablecoins as a universal medium of exchange to process large-scale payments between consumers and merchants.

Institutional Adoption

Institutional adoption of on-chain public permissionless networks is critical to the long-term success of the broader crypto ecosystem and is currently in its early stages. bitsThe Coin and Ethereum spot ETFs were approved in January and June 2024 respectively, but have already seen massive adoption - with total net flows exceeding $24 billion. While we expect the ETF trend to grow significantly from here on out, this is just Web2 wrapping Web3 products. Tokenization can be considered as the native transfer of traditional web2 assets to the chain, which is the future of institutions and is receiving great attention from countries around the world and the private sector. To access all of web3, organizations need a scalable, secure, and appropriately licensed marketplace infrastructure.

Total RWA ValueReal World Assets (RWA) are digital tokens that represent physical assets or financial instruments on the blockchain. This includes real estate, art, merchandise, etc. Tokenizing RWA on-chain allows for fractional ownership and opens up new possibilities for trading, investing, and ownership. The growth of RWA is a key driver of on-chain economic growth.

A number of different metrics can be evaluated to determine growth in institutional adoption. Currently, the best metric is total RWA growth, as it describes the actual capital on the chain.

The total RWA value of the entire network (excluding private credit and stablecoins) is $3.92 billion, of which tokenized treasuries account for 62%.

Total risk-weighted assets are up more than 50% year-to-date, from $8.3 billion to $13.25 billion.

Ethereum has received over $3 billion in RWA.

Data from RWA.xyz shows that RWA is achieving considerable growth and will continue to grow as more institutions join the chain.

Tokenized value growth broken down by category

With the successful approval of the Bitcoin spot ETF, institutional focus has turned to the tokenization of RWA.

A quote from BlackRock CEO and founder Larry Fink sums up institutional sentiment well:

“ ETFs is the first step in the technological revolution of financial markets, and the second step is the tokenization of all financial assets. There is a strong push to tokenize financial assets to enable them. Benefit from unrestricted on-chain economies. As seen by major traditional financial institutions such as BlackRock and Franklin Templeton, they have begun issuing RWA on-chain.

Tokenized Treasury bonds currently account for the majority of issued RWA, with commodities ranking second:

As of November 19, the total RWA value across all blockchain networks ( Excluding private credit) was US$3.92 billion, of which tokenized government bonds accounted for 62%.

The growth in tokenized Treasuries has primarily occurred on Ethereum L1, exceeding $1.5 billion. Only $4.5 million in tokenized Treasury bonds have been issued on Base, but this area is already ripe for growth. As the network matures and decentralizes further by achieving the next stage, which is the level of decentralization, Base will be ready for the influx of on-chain assets.

On-chain developersOn-chain developers are an important part of the on-chain ecosystem - an active developer ecosystem promotes the creation of innovative applications that attract users to join the network and stay Live them.

Generally, the number of full-time developers on each chain is considered the most important metric for measuring developer activity. As of the latest developer report on June 24, Base ranks second with more than 900 active full-time developers, behind Ethereum (about 2,800).

Note: A full-time developer is defined as a developer who commits code for more than 10 days per month.

On-chain NFT transaction volumeNFT transaction volume is quantified by calculating the sum of NFT transaction volume within a given time frame. Cumulative weekly NFT trading volume has dropped from 309 million to 59 million so far this year, a drop of approximately 80%.

During the same time period, Base’s cumulative NFT trading volume increased from approximately 100,000 in early January to 7.66 million, an increase of more than 7,500%. This increased Base's market share from 0.003% to 13%. NFT growth on Base has been driven primarily by the promotion of free or low-cost NFTs rather than speculative NFT trading activity, indicating a shift in NFT market focus in recent years.

While NFT trading volume on major networks has been trending downward due to market conditions and many high-profile NFT values falling by approximately 80%, NFT trading volume on Base has increased significantly. This is largely because Base NFTs were virtually non-existent at the beginning of the year, and now their trading volumes are more in line with the overall market for NFTs.

Deep Dig into BaseIn general, while the entire on-chain field continues to grow, Base has also achieved accelerated growth. What's more, Base's market share across all analyzed metrics has grown multiple times year-to-date, demonstrating Base's clear relative strength and outperformance in terms of economic growth and user adoption.

For example:

The number of daily transactions has increased 1,600% since the beginning of January, from 372,000 to more than 6.63 million in October.

Daily transaction volume has increased by more than 50% year-to-date.

Year-to-date, weekly active addresses have increased by more than 2,100%.

Total value locked year-to-date is up over 70%.

This also proves that Base and otherHe develops the team’s efforts to build beneficial applications and networks that promote economic growth throughout the chain.

While Base is growing faster than other networks in all of the following metrics, it's worth noting that usage is up on most major networks so far this year, suggesting that bringing people to The joint effort to get on-chain is benefiting all networks.

Base user activity increased so far this yearData from January 2024 to October 2024 tells a unique story: Base adoption is soaring.

Weekly active addresses and transaction volume on Base have increased steadily, increasing by more than 2,100% and 1,600% respectively from January to October 2024. The impressive progress shows that Base is effectively attracting users and expanding on-chain adoption globally.

It should be noted that weekly active addresses are not equivalent to weekly active users, because users may create and operate multiple wallet addresses, which means that the correspondence relationship is not 1:1. Nonetheless, it is still a useful metric for assessing overall activity levels on the chain, especially when filtering addresses that interact with revenue-generating smart contracts, as is done in this report.

In 2024, weekly active addresses on Base surged from 300,000 in January to 6.61 million at the end of October, reaching an all-time high of 7.19 million on September 16. The increase represents a year-to-date increase of more than 2,100%.

Note: Base Weekly active addresses refer to the number of unique addresses that have interacted with revenue-generating smart contracts deployed on Base . A person may be active at multiple addresses.

As of November 19, Base’s weekly active addresses increased by 2,000% to more than 6.5 million.

These initiatives have successfully fostered a growing ecosystem. Coupled with the significant reduction in transaction fees after EIP-4844 (typical fees are now less than 1 cent), Base has become a very attractive chain to work with from both a user and developer perspective interactive.

So far this year, Base's daily new addresses have grown from 9,300 in January to 670,000 at the end of October, hitting an all-time high of 867,700 on September 20. The increase marks more than 7,100% growth since the start of the year.

Note: The daily new addresses of Base refer to the number of new addresses that interact with the revenue-generating smart contracts deployed on Base for the first time (does not mean < em> Base any previous on-chain activity).

Meanwhile, Base's daily return addresses increased from 59,000 in January to more than 1 million in October, peaking at 1.23 million on October 3. That equates to more than 1,600% year-to-date growth, a strong indication that user retention remains strong despite a surge in activity.

Note: Base Daily return address refers to the number of interactive addresses that have previously interacted with revenue-generating smart contracts deployed on Base .

An example of an on-chain event driving Base is the Onchain Summer program, which celebrates and showcases on-chain innovation - including music, art, food and games. The program encourages participation by showcasing compelling on-chain projects in the Base ecosystem. This effort has helped bring users on-chain, as evidenced by the surge in on-chain activity.

Another factor supporting Base’s success is the diverse marketing campaigns that reach a wide target audience, such as advertising on Liquid Death boxes to promote on-chain activity.

Separately, Coinbase launched cbBTC, a wrapped Bitcoin token, on Base. By prioritizing cbBTC adoption on Base, they help solidify Base’s position as the leading ecosystem for the most secure on-chain wrapped Bitcoin.

Programs like cbBTC and Onchain Summer help bring the masses on-chain. Once they're here, they're here to stay, as the active addresses returned indicate.

Falling fees drive Base transaction growthNot surprisingly, as active addresses increase, daily on-chain transaction volume also soars.

As of November 19 , the number of daily transactions increased by 1,900% to 770 em>More than ten thousand pens.

In particular, the number of daily transactions has increased by 1,600% since the beginning of January, from 372,000 to more than 6.63 million in October. Both active addresses and transaction volume show similar trends, which proves that the Base economy is becoming an on-chain hub in the Rollup field.

Contrary to web2 dynamics, the cost of doing business on Base has fallen despite soaring demand. The average transaction fee on Base dropped from $0.44 in the first quarter to $0.019 on October 17, a drop of more than 95%. While this is partly due to EIP-4844, Base has been working on the expansionWork such as increasing the gas limit has played an important role in reducing costs.

Specifically, average transaction fees have dropped by more than 95% so far this year, while average daily transaction volume has surged 800%, from 615,000 transactions in the first quarter to 5.6 million transactions in October. These low fees make on-chain technology more popular and encourage more developers and users to join the chain.

Base, on the other hand, is currently the largest gas consumer among rollups using blobs, continuously processing >50 transactions per second, consuming >13 mgas/s.

Base commits over 29% of all blobs, indicating a huge demand for Base block space as a result of the explosive growth of the Base chain.

However, this may cause problems in the future. If the maximum number of blobs is not increased in future upgrades, the current cap may hinder Base growth.

Year-to-date growth in base economic value and total locked value

Year-to-date, Base’s total economic value has increased from $900 million in January to $8.03 billion at the end of October. Reached 792%. This number makes Base the second largest L2 in this metric, behind Arbitrum.

Note: Total economic value refers to the sum of all canonical bridged, externally bridged, and locally minted tokens

It is worth noting that this growth is unparalleled and is the reason why the network is Fastest growth rate ever (in just 16 months!) in terms of total economic value amassing over $8 billion. We expect this economic value chart to maintain its trend as heavy inflows are expected to continue over the next few years.

Additionally, Base ranks third in terms of net traffic (nominal traffic, not %), with $1.6 billion in net traffic across all networks so far this year, while Ethereum’s net outflows are 65 billion dollars. It must be admitted that most of the outflows experienced by Ethereum are mainly the migration of capital into rollups, which indicates that capital flows mainly stay within the EVM ecosystem rather than moving out of the ecosystem.

So far this year, the Base protocol’s TVL has risen from $439 million in January to $2.52 billion at the end of October, an increase of 470%. As of November 8, Base’s TVL has exceeded $2.77 billion, making it the leading L2 by total value locked.

The ratio to monitor is TVL/Total Economic Value, since a healthy ecosystem will have both metrics growing at a similar rate.

By directly comparing each metric, we can gain a deeper understanding of the on-chainOverall distribution of activity. The similarity between TVL and total economic value shows that most capital is locked in protocols and smart contracts, indicating active DeFi activity. On the other hand, if the total economic value significantly exceeds TVL, it would indicate on-chain activity beyond the scope of DeFi, highlighting a more diverse distribution — which is the case with Base.

Growing Stablecoin Market Cap on BaseBased on all of the above metrics and many others, Base is the fastest growing L2.

Another interesting way to quantify the "success" of a network is to track the overall market cap of stablecoins on the network.

So far this year, the market value of stablecoins on Base has risen from US$170 million in January to US$3.53 billion at the end of October, an increase of more than 1,900%. This represents a significant increase in both nominal value and percentage.

As of November 19, the market value of stablecoins on Base was US$3.3 billion (an increase of more than 1800% from US$170 million in January), while the market value of all network stablecoins was US$186 billion ( A 38% increase from $134 billion in January).

It is worth noting that this percentage increase exceeds the increase in economic value during the same period, indicating that the Base ecosystem is not only growing, but also beginning to mature.

Base on-chain application ecosystemMultiple use cases beyond DeFi

With the rapid growth of users and transaction volume, the number of projects launched on Base is also steadily increasing. A thriving ecosystem is a sign of a healthy network, and it's clearly driven by Base's commitment to delivering an unparalleled developer experience. As of October 17, 2024, there are 85 active applications on Base and more than 100 daily active wallets.

More than 60% of on-chain applications on Base have nothing to do with DeFi: gaming applications account for 20%, collectibles account for 18.8%, social applications account for 15.3%, and "other" accounts for 5.9%.

As shown above, while DeFi applications lead as a single category, areas such as games and collectibles also have high usage, accounting for 54% of all active applications on Base above.

The diversity of applications on the chain shows that Base is more than just a DeFi hub. It is a space where all types of on-chain applications can flourish and form a real economy. This is further supported by the growth of apps like FrenPet, which focus on gameplay rather than monetary gain.

The diversity of applications on Base is roughly similar to the cumulative application diversity of the major networks supported by DappRadar.

These useful features provided by dApps show that users are beginning to accept all types of on-chain applications. This is a healthy sign for the on-chain ecosystem, which is growing in diversity beyond currency-centric applications.

Supporting ease of use and cost-effectivenessDividing the year into post-EIP-4844 and pre-EIP-4844 periods, average transaction fees for users dropped 70% from $0.422 post-EIP-4844 to $0.097.

As mentioned earlier, after the implementation of EIP-4844, transaction fees on Base dropped by 70%, which promoted the rapid growth of transaction volume. Continued improvements in cost efficiency will unlock significant expansion of on-chain use cases and help attract new users to the chain.

As transaction costs decrease, it becomes more feasible for on-chain applications to completely eliminate gas fees. With the payer bearing minimal transaction fees, users do not need to consider paying gas fees with ETH.

Base is not the only L2 where users are seeing fee reductions, however. Development work made by Base outside of its own rollup (especially EIP-4844) benefits all rollups. The biggest advantage of cheap transactions is that on-chain applications can provide gas fees through paymaster. By paying transaction fees themselves through the application (the lowest cost per transaction), users don’t need to think about paying gas fees with ETH.

This simplifies the entry barrier for new users. If full abstraction does become possible in the future - where the on-chain user experience is very similar to web2, by being streamlined to the point where users don't know they are interacting with the blockchain - then applications will be able to absorb the gas fee costs without compromising on Significant impact on profitability.

As Base fees continue to drop and approach the cheapest, economically viable cost, the possibilities for on-chain exploration are nearly endless.

Adoption of Coinbase Smart Wallet continues to grow since launch (June 2024)Launched in June 2024, Coinbase Smart Wallet is an advanced wallet designed to optimize the user experience and simplify onboarding process. There are no extensions/installations required, passwords are used instead of complex mnemonics, and the wallet works on most major networks. Smart wallets shorten the user on-chain process to just a few seconds and clicks.

After hitting an all-time high of 21,660 in August, the number of Coinbase Smart Wallet monthly active wallets has surged 168% since launch in June - from 5,700 to 15,280.

Additionally, the number of monthly wallet operations using the Coinbase Smart Wallet surged from 31,200 to 70,320, an increase of 125% and hit an all-time high in October 2024.

Note: Data refers to on-chain interactions using the Coinbase smart wallet.

Incentives for DevelopersThere are four main factors in creating a developer-friendly environment on Base:

Base is built as a standardized EVM, This means developers can write applications using Solidity, the most popular blockchain programming language.

Base is part of Superchain, a rollup network using OP Stack, allowing Base to share security and communication layers with other rollups. As a result, Base is more attractive to developers due to increased interoperability between Superchain rollups and the support it receives from other Superchain developers.

The Coinbase Developer Platform and Onchainkit provide ready-to-use components and tools to make developing on Base easier.

Transactions are very cheap compared to other Rollups, and application fees are significantly lower than their Web2 competitors, resulting in a large user base.

On-chain use cases proliferateProjects are broken down by innovation and utility

As Base continues to see an influx of activity so far this year, different areas have seen varying success.

Here is a summary of some of the standout protocols in each area and their performance this year.

Social – Farcaster Frames

Launched in March, Farcaster Frames is a tool that allows interactive experiences to be embedded into casts on Farcaster.

Frames are easy to find, Warpcast (the largest Farcaster client) has a subpage to view popular Frames. They are similar to Blinks on Solana and Slinks on Starknet, allowing tweets to embed interactive on-chain content.

Frames unlock internal composability between clients, networks, and users. Many frameworks are built on Base, allowing for many different on-chain interactions, such as minting NFTs in the feed, making on-chain payments, and playing games. These on-chain tasks can be completed with just a click of the frame.

They also create convenience between consumers and merchants, allowing for seamless transactions within the Farcaster client. This increases purchases because it reduces the steps to complete a purchase.

Game – Frenpet

Frenpet is an idle game on Base that has quietly become a huge success over the past year. The app is built on the browser and the creation process is completely abstracted through Privy and the payment system.

The game has been growing steadily, with over 2.25 million plays so far this year.

The gaming scene on Base is just getting started, and as Base continues to attract more users to its network, there is a chance that fun little games like Frenpet will start to become popular.

NFT/Digital Collectibles

NFT trading volume across networks, including Base, had been trending downward for most of the year, but bottomed out (at least temporarily) in August ).

As of the end of the first quarter of 2024, we are seeing an upward trend in transaction volume. This excludes the outlier in late October, which returned to the mean the next day.

NFT transaction volume on Base corresponds to peak activity in different periods, and there is a lack of consistency within quarters. The most likely reason is that specific NFT initiatives have temporarily boosted NFT trading volumes.

Interestingly, so far this year, the weekly NFT minting volume on Base has increased from a peak of 17.12 million in the first week of June to 832,000 at the end of October, an increase of 5 million. This indicator shows a counter-trend of increased NFT activity.

That number has grown 500% so far this year, demonstrating that Base is becoming a hub for non-monetary use cases for NFTs.

Based on NFT activity on Base and other networks, NFT behavior appears to be shifting away from trading/speculation toward non-monetary use cases for NFTs. This is illustrated by a 500% increase in weekly NFT minting volume on Base between January and October 2024, followed by a significant drop in NFT trading volume between March and October 2024.

Beyond art, the true value of NFTs, such as Bored Apes, is their ability to be tied to real-world utility. Examples of this real-world utility include NFTs representing membership in a coveted group or a deed to real estate.

Minting has been trending upward since Coinbase launched its Onchain Summer program, which encourages participants to mint NFTs—often at little or no cost (via gasless transactions). This demonstrates that Onchain Summer has a lasting impact on user engagement, as users remain active after the program ends.

DeFi on BaseDecentralized Finance (DeFi)An intermediary that provides financial products and services at an institutional scale without absorbing value. With DeFi, value can be redistributed to participants. Like most networks, DeFi remains dominant on Base and takes advantage of transaction fees below one cent. The following sections cover four different embedded areas: DEX/Derivatives, Money Markets, Telegram Bots, and Liquidity Staking/Yield Farming.

Trading platform

Base has become an important area of spot asset trading, and daily trading volume continues to grow. Year-to-date, Base DEX trading volume has grown 3,900% from $22 million in January to $880 million by the end of October 2024.

Combining these two metrics, Aerodrome is the clear winner. Aerodrome’s total TVL has exceeded $1 billion, accounting for approximately 40% of Base’s total TVL, and facilitates the highest on-chain volume pools among ETH, BTC, USDC, and EURC. The protocol is a fork of velodrome, a Curve-inspired automated market maker (AMM) that aims to serve as a liquidity center on Optimism.

Aerodrome plays the same role on Base and has been hugely successful so far - accounting for the majority (~50-60%) of DeFi trading volume on Base.

Aerodrome is particularly attractive for financial transactions. Users can redeem USDC and EURC within 1-5 seconds at a fee of 0.05%, 24/7 with no delays and virtually no slippage. By comparison, traditional financial transfers can take 1-5 business days and have fees ranging from 0.3% (Wise, on the low end, which charges 6 times as much as Aerodrome) to 3% (Wells Fargo, which charges 60 times as much as Aerodrome). Additionally, international transactions on Aerodrome are available 24/7 and take only 1-5 seconds, compared to 1-5 business days for traditional financial transactions.

Users prefer a familiar structure so that they can truly benefit from the protocol. This is why in the early stages of most networks outside of Ethereum, Uniswap did not hold the majority of the market share, but rather the native AMM.

Most alternative network-native AMMs have traditionally had complex user incentives centered around staking tokens to earn emissions or protocol fees. Once this happens, the flywheel kicks into gear and native AMMs attract all the liquidity. Uniswap usually doesn’t become a market leader right away. This was obtained in several rollupsEmbodiments: Base (Aerodrome), Optimism (Velodrome), and zkSync (Maverick).

What needs to be noted here is: as rollup matures, this flywheel will often break, and Uniswap liquidity on the network will continue to grow and seize market share. Aerodrome's incentive structure makes it the clear leader on Base in terms of TVL and transaction volume, however, this may change as the rollup ecosystem matures.

Currency Market

Three major currency markets account for most of Base’s market share: Morpho Blue ($220 million), Aave ($150 million) and Moonwell ($146 million) . These numbers represent active deposits on the platform.

Morpho Blue is a trustless platform containing an immutable, independent lending market. MetaMorpho allows third parties to offer their own customized vaults on Morpho Blue. Morpho Blue automatically handles the maintenance of structural forces on market parameters to ensure the market remains solvent.

Isolated lending markets are powerful because they isolate the risk of each collateral asset. This means that Morpho Blue could technically add "riskier" collateral (e.g. less liquid and more volatile assets like uSUI) and increase its revenue without increasing the amount offered in the market. External risks with “stronger” collateral (e.g. ETH). The disadvantage of this is that the borrower cannot benefit from large deposits in other vaults.

Aave, on the other hand, is a traditional DeFi lending marketplace where all pools are tied together, allowing users to submit any collateral selection and borrow any enabled asset. Due to its resiliency and long-term reputation, Aave is the “de facto” lending marketplace for most networks.

Moonwell offers users a combination of both. Moonwell is a fork of Aave that can take deposits using collateral from any acceptable asset. They also have core vaults built on top of Morpho for a more independent lending pool. The combined offering allows users to choose the infrastructure they want to use, managed by the Moonwell DAO.

Having three competitive lending markets on Base is a healthy sign of decentralization and competition and helps promote user innovation and choice. While many networks with Aave as the dominant currency market suffer from SPF (single point of failure), this will not be the case with Base as funds are spread across multiple protocols.

ThisOptimal for long-term growth, although it requires more total liquidity to reduce the impact of fragmentation. More choice and competition are good for users, and the growth of Base DeFi allows every lending market to build enough liquidity to meet the needs of almost all users. The continued growth of the ecosystem will benefit all lending markets and reduce the impact of liquidity fragmentation, thereby benefiting users.

Telegram Bots

Telegram bots have gained momentum across most networks, driven by a dramatic increase in on-chain transactions and a simplified user experience, resulting in a major shift in retail investor behavior this year .

Telegram bots function to snipe and efficiently trade on-chain assets for users, giving it an advantage over users who trade manually using self-hosted wallets. Most bots charge around 1% on trades.

Using Telegram bots for on-chain asset transactions has significant user experience advantages. As a result, Telegram bot adoption continues to grow, with daily revenue consistently exceeding $1 million.

Contrary to other networks, the number of Telegram bots on Base is not high, indicating a lack of adoption.

The low number of Telegram bots coupled with the rising number of DEXs on Base seems to indicate that Base has attracted a large number of actual users, and that there is also migration activity from other networks to Base.

Yield Activities

Decentralized yield farming of cryptocurrencies is very popular. Since almost all cryptocurrencies are financial in nature, a tool to maximize returns without centralized risk is very attractive to many users, driving adoption.

However, Base is not a chain built for profit, but to create an on-chain global economy. Only a small portion of the assets on Base are actively leveraged income activity, as most capital from institutions is risk-averse and prefers to hold these assets, or in some cases, from licensed participants Borrow there.

Base's top yield platform (provided by TVL) is Extra Finance, which offers a range of leveraged yield products.

They have amassed over $150 million in TVL (while significant, it is a small fraction of the $8 billion in assets on Base), and their user trading volume is approaching May 2024 highs Points - Daily trading volume regularly exceeds 2,000 transactions.

Extra’s leveraged return design is a streamlined but smart design that maximizes returns for all participants. The process follows the following structure:

Providing collateral -> Borrowing different assets from the lending pool -> Automatically convert assets into equal proportions -> Provide liquidity -> Compound rewards

Don’t want to Users taking advantage of the proceeds can lend their assets to mining pools to earn interest rates, similar to any other lending market.

Weekly Base contracts deployed so far this yearBase can prioritize work on the decentralized stack (such as failure proofing) and help the broader Ethereum ecosystem because there is ample developer activity on Base .

We are seeing this in action today - weekly contract volumes are significantly higher than at the beginning of the year, increasing from 5,400 in early January to 72,300 in October, a 1,200% increase.

Note: The number of contracts deployed per week refers to the number of unique on-chain contracts deployed on Base every week.

Weekly Base contracts deployed by unique addresses so far this year p>

In addition, Base also found that the number of contracts deployed through unique addresses is increasing rapidly. Since January, the number of contracts deployed via unique addresses per week has increased from 3,700 to 32,500, a 778% increase.

Note: The number of contracts deployed by unique addresses each week refers to the number of on-chain contracts deployed on Base by developers who have not deployed contracts that week.

Although this metric has declined slightly since April, the overall trend is still increasing, which is a strong indication that Base on-chain applications The developer ecosystem is booming. Additionally, it shows that the team’s development efforts to make Base a developer-friendly chain are succeeding.

Onchain Job Market InsightsFor the portion involving non-public information, we interviewed recruiters from different headhunting firms.

The number of companies hiring engineers with smart contract expertise has increased so far this year

In the first two years of 2024, according to our sources Quarterly, the number of companies recruiting engineers to work on on-chain development has increased dramatically. After EthCC, this growth slowed somewhat as the traditional “summer slowdown” occurred and prices fell. Even during this period, however, there was a clear uptick in hiring relative to other periods of declining prices.

Our sources noticed an interesting trend: during bear markets, there is a greater focus on infrastructure, leading to more developers working on infrastructure-related issues. MutuallyConversely, in a bull market, people actively optimize for mass adoption, which results in more consumer apps being funded and therefore more developers working on developing consumer apps.

More job opportunities for crypto-savvy applicants

According to our sources, demand for crypto-native job seekers is increasing across industries. Crypto-native talent understands how blockchain projects market to users because the candidate was/still is a user—a clear advantage over candidates who don’t understand crypto. One source added that crypto-native employees who are familiar with niche marketing structures that appeal to the crypto community are key to a successful marketing strategy.

Interestingly, demand for networking events for crypto-native talent surged in Q1 and Q2, coinciding with protocols launching their products and tokens. However, our sources note that companies in the cryptocurrency industry still place a high value on prestige. Even for crypto-native candidates, factors like attending an Ivy League school are often highly valued in the hiring process.

According to our sources, the demand for cryptocurrency natives and candidates with prestigious backgrounds has resulted in many positions within the industry being restricted to a limited number of applicants.

On what builders/protocols/founders think about the talent pool

Our sources indicate that before the collapse of FTX, Luna and Three Arrows Capital, the industry’s talent pool was much better Broader and more diverse, with candidates coming from a variety of fields outside of computer science. Clearly, the impact of these events on the crypto industry extends far beyond a decline in market valuations. General reputation issues remain, reducing the number of applicants willing to work in an industry they view as unstable.

This bias against cryptocurrencies is also reflected in the declining interest of students in joining university blockchain clubs, according to one source. Prior to the aforementioned crash, there was a significant increase in demand for club memberships. Given the current competitive landscape for computer science and engineering internships, waning interest in an industry where opportunities are abundant is particularly concerning.

That said, the crypto industry will benefit from a stronger attraction to young builders for on-chain development — targeting interns and recent graduates.

Talent demand strong, talent shortage

Despite poor market conditions, recruiters are seeing continued demand for engineering talent as venture capital-backed projects have limited access to There is fierce competition for technical engineer resources.

As a result, there is a clear shortage of crypto developers as demand continues to exceed available talent. Interestingly, three sources added that many traditional developers are reluctant to pursue positions in crypto because they view the industry as unstable.

Three results from a recent Coinbase survey of on-chain and mainstream developers corroborate this statement, underscoring concerns about onboarding new developmentLack of confidence in personnel capabilities.

Half (49%) of mainstream developers believe that “encryption and blockchain are important areas of innovation in the future.”

78% of on-chain developers agreed that “it used to be difficult to get new users started using cryptocurrencies and blockchain applications.”

73% of on-chain developers said “ The lack of clarity in crypto regulations makes it more difficult to innovate in the space."

Coinbase is actively seeking clearer regulation globally on behalf of the industry. Progress in this area may help remove barriers to innovation for developers and promote the overall development of the on-chain economy.

ConclusionIn 2024, the on-chain economy will undoubtedly usher in explosive growth. Much of this growth has been driven by activities other than financial speculation and trading. Stablecoins have found product-market fit and are driving a more global digital economy. L2 reduces on-chain costs, making on-chain construction easier, faster, and cheaper.

In just over a year, Base has solidified its position as the L2 leader. By building an ecosystem that attracts developers with minimal transaction fees, Base creates an environment that not only attracts developers and users, but also has high retention rates.

DeFi remains the core of on-chain economic activity. DeFi provides financial products and services at an institutional scale, but without intermediaries who absorb value. Instead, this value can be redistributed to participants.

At the same time, new use cases and applications are becoming an important part of the on-chain economy. Facilitating diverse on-chain application development and creating infrastructure to support various industries (such as gaming and SocialFi) means that on-chain experiences are constantly expanding, which is a major driver of the growing global on-chain economy.

Lower fees, more use cases, easier-to-use technology and innovative products have all contributed to the booming development of the on-chain economy.