29 mins ago

987

Author: Paul Timofeev, Sitesh Kumar Sahoo, and Gabe Tramble

Source: Shoal Research Translation: Shanou Ba, Golden Finance

IntroductionThe rapid development of the Web3 field stems from its open source and decentralized characteristics. This characteristic brings about hyper-growth and scaling, what many refer to as cryptographic composability. This composability allows for the creation of modular technology stacks where components can be seamlessly inserted or removed, driving unprecedented innovation. At the core of this innovation is the basic process of blockchain transactions, whose core value depends on the distributed network's ability to coordinate and achieve a consistent system state.

When a transaction is sent on the blockchain, a distributed network of nodes must first verify the contents of the transaction and then vote on the order of the transactions to form the The next block in the chain. When these nodes reach an agreement, a state called "consensus" is reached. Blockchain initially achieved consensus using a Proof-of-Work (PoW) mechanism, which involved professional nodes called miners competing to solve cryptographic puzzles in order to add new transactions and blocks to the chain.

Although Bitcoin and many blockchains still use PoW consensus, most blockchains today have moved to Proof-of-Stake (PoS) ), ensuring security through economic incentives rather than computing power. The concept was first proposed in the 2012 Peercoin white paper, which proposed a deterministic algorithm that selects nodes based on the number of local network tokens pledged by node operators, favoring nodes with more capital.

Subsequently, Jae Kwon wrote the Tendermint BFT white paper in 2014, introducing a new consensus mechanism that requires less than one-third of the nodes to Failure, a consensus can be reached, and it will be put into use with the launch of the Cosmos Hub mainnet in 2019. In addition to consuming significantly less energy than PoW, a key advantage of PoS is that, like PoW, staking cannot be easily faked. Additionally, PoS incentivizes honest behavior through a process called slashing, whereby validators will suffer financial losses if they behave maliciously.

With the widespread adoption of PoS blockchains, participation in staking has given rise to new ideas for maximizing the utility of pledged capital, such as making pledged capital more liquid to provide security for new products and ecosystems.

Staking Design OverviewOriginal StakingStaking is a mechanism in which token holders deposit tokens into a staking contract to participate in the security maintenance of the underlying protocol and receive rewards for their contributions. In this article, this mechanism can be called "original" Staking” as its core utility is limited to remaining idle in a smart contract, while other forms of staking provide additional utility, which will be expanded upon further below. The stake size of a validator determines the likelihood of being selected to produce a block. The more capital staked, the greater the likelihood of being selected. Technically, anyone can participate as an independent staker, but the blockchain is generally limited. Stakeholders impose certain financial and hardware requirements that may not be easily achieved by regular users or token holders. For example, participating Ethereum validators require deposits. 32 ETH and comes with at least 16GB RAM, multi-core CPU and 1TB SSD, while Solana requires paying 1.1 SOL per day to vote and comes with at least 256GB RAM, fast multi-core CPU and high-speed SSD storage

Therefore, in order to lower the participation threshold, a delegation mechanism was formed, allowing token holders to participate in staking with less capital and without any hardware, while allowing node operators running validators to expand their staking allocation, thereby Increase its block reward. The pledge can be delegated directly to the validator, or through a pledge pool, which is a smart contract that centrally entrusts funds to multiple validators. The pledge pool can be delegated by a third party, such as one that provides pledge services. Centralized exchange (CEX) custody, can also be hosted on Ethereum such as Decentralized on-chain protocols such as Rocket Pool or Jito on Solana perform non-custodial operations

Staking also exists at the application level, i.e. the application's token holdings. Stakeholders can lock their tokens to secure the protocol (for example, to provide liquidity in the event of a deficit event on the lending protocol), often resulting in rewards for the staker, as well as additional utility such as governance rights or revenue sharing. This has even given rise to bribery markets in DeFi (such as Curve Wars), protocols compete to accumulate more governance tokens and thereby obtain a higher proportion of reward returns.

Nonetheless, the original pledge due to its design. Simplicity, with one key limitation: the capital locked up in the smart contract is illiquid, reducing the liquidity of the token and its ecosystem. The lack of underlying staking utility hinders the adoption of staking services, as the rewards distributed to token holders need to compensate for the price exposure risk of locked tokens. A large amount of network activity may generate enough fees to provide natural rewards to stakers, but this is often unsustainable and has not historically been the case in most PoS chains. Distributing rewards through native token issuance is a common alternative, but this is equally unsustainable in the longer term. This problem prompted the development of liquidity staking protocols.

Liquidity stakingThe emergence of liquidity staking stems from the need to develop a new mechanism that allows stakers to maintain security without affecting the security of the underlying protocol. maintain the liquidity of its pledged assets. The process is largely similar to base staking, where stakers deposit assets into smart contracts and receive base returns for their contributions to the underlying system. Liquidity staking, however, goes a step further by distributing to stakers a voucher token called a Liquid Staking Token (LST) that is worth the same amount as the original deposit. This innovation demonstrates the importance of composability in the DeFi space, as LST can be used in a variety of applications (e.g. liquidity provision, lending), ultimately enabling stakers to earn higher returns on top of their pledged assets , while increasing the overall liquidity of the underlying network ecosystem.

Since the emergence of the first batch of liquidity staking protocols at the end of 2020, liquidity staking has become the fastest growing area in DeFi. As of this writing, there are over $42.3 billion in assets in the space, about 60% of which belongs to Lido Finance’s stETH contract. Ethereum currently accounts for nearly 85% of the liquidity staking in the DeFi space, while Solana is relatively small with less than $4 billion locked in the liquidity staking protocol, 45% of which comes from Jito.

Overall, liquidity staking brings great flexibility and capital efficiency to stakers, which in turn benefits the underlying layers they support Blockchain and the ecosystem built on it. However, as blockchain evolves, the uses for pledged assets continue to evolve. The rise of modular infrastructure and services has given rise to a plethora of new application-specific blockchains, which often face difficulties in building their own validator networks due to a lack of activity and economic incentives. Therefore, new mechanisms are designed to expand the use of pledged assets to help secure and launch new blockchains. This mechanism is “Restaking”.

Pledge againRe-staking refers to the expansion of one blockchain’s staking and validator network to provide security for any number of other blockchains. From a more formal perspective, restaking can be defined as a variant of security-enabled Proof-of-Stake (PoS) blockchain environments, where a security-providing chain services a security-consuming chain, typically through a Intermediary implementation of the re-pledge agreement.

This mechanism enables new blockchains (whether application-specific or general-purpose chains) to leverage the economic and computational resources of large base layers such as Ethereum or Solana to activate its security. Stakeholders can also increase capital efficiency by securing multiple blockchains rather than a single chain, thereby increasing returns on their pledged assets. However, it is important to note that securing multiple blockchains increases the risk of slashing of staked assets – a concept that will be explored further below.

Just like running a validator node directly on a proof-of-stake blockchain or depositing funds into a staking pool, anyone can participate in re-staking. Users can choose native restaking, which is running a validator node that promises to participate in the restaking module, or liquid restaking, which is staking through a protocol or service provider, who restakes on behalf of the user. Pledge. In addition, re-hypothecation can be limited to native layer 1 (L1) assets, or can be extended to support almost any asset. This approach is called "universal re-hypothecation" or "universal re-hypothecation".

Early implementation

Although restaking is commonly associated with Eigenlayer today, the concept has Tested and implemented in application-specific blockchains, where startup security is often one of the biggest challenges. Several different ecosystems and networks have implemented some form of shared security at different times, and while the specifics may vary, the core concept is often the same - enabling smaller protocols to leverage existing economies and computing resource pool to facilitate its early development while improving capital efficiency and returns for stakers.

•In the Polkadot ecosystem, validators participate in the security of the relay chain (Relay Chain) by pledging DOT, and the relay chain is an approved Parachains provide security.

•In the Avalanche network, validators that protect the C chain (the main center of economic activity) can participate in subnets (Subnets), a subnet is a dynamic collection of validators that cooperate to protect multiple chains or reach consensus on their status. A subnet can secure multiple chains, but each chain can only be verified by one subnet.

•Cosmos takes a different approach. The first 95% of the pledge weights and validator sets of its ecological center Cosmos Hub are actually copied to all consumer chains. This One mechanism is called "Replicated Security". Cosmos Hub validators must run nodes on all consumer chains, although different software and/or hardware can be used. If the validator performs poorly on the consumption chain (such as downtime or double signing), the Cosmos Hub validator will be punished.

In March 2023, replication security will be officially launched through the Prop 187 V9 Lambda upgrade. However, the trend is gradually towards providing greater flexibility to stakers and validators. ICS v2 introduces “opt-in security” that allows validators to choose whether to secure a specific consumption chain. Additionally, a proposal was made in early May 2024 that, if passed, would allow Cosmos Hub validators to receive BTC pledges through the Babylon Staking Protocol, allowing any asset to be used for economic security on Cosmos.

Mesh Security will eventually allow chains to provide and use security at the same time, rather than using the provider chain's validator set to protect the consumer chain. Operators can choose whether to run a Cosmos chain, and stakers can choose to re-stake their staked assets to secure another Cosmos chain. Finally, a proposal was released in early May 2024 that, if passed, would allow Cosmos Hub validators to receive BTC staking through the Babylon Staking Protocol, paving the way for economic security with any asset on Cosmos.

In June 2023, the Eigenlayer protocol introduced the heavy pledge function to Ethereum. The Eigenlayer protocol is a set of middleware smart contracts on Ethereum that supports the consensus layer ETH is heavily staked to provide security for the consumer chain called Active Validation Service (AVS). Eigenlayer ultimately serves as an open marketplace designed to connect AVS looking to lease security (validator sets and/or staked assets) with stakers and node operators that provide said security. ETH and supported ETH LST can be staked through a set of smart contracts thatEnergy contracts represent AVS extensions orheavy-collateralized economic security.

By leasing security assets to AVS, operators and stakers can expand the utility of their assets, thereby increasing returns. However, this comes with risks, as their staking is now subject to any slashing conditions that AVS may impose, in addition to being slashed by the underlying chain Ethereum. Eigenlayer is an off-protocol solution on Ethereum, meaning Beacon Chain validators can choose to participate as Eigenlayer node operators.

Currently, there are no slashing conditions or re-staking rewards enforced on Eigenlayer, but this will change once EIGEN tokens become transferable in late September 2024 . Additionally, Eigenlayer recently announced permissionless token support to enable any ERC-20 token to be used as a re-staking asset.

Universal RestakingUniversal Restaking, or "Universal Restaking", uses an asset- and chain-independent method to combine security resources Assigned from a set of providers to a set of consumers. This approach allows for the pooling of various staking assets across multiple chains, increasing participant accessibility and reducing reliance on a single base layer. Similar to Eigenlayer, the Universal Redemption Protocol acts as an intermediary between the security providing chain and the consuming chain (AVS).

Liquidity re-pledgeLiquidity re-pledge enables re-pledged assets to be expressed in the form of Liquid Restaking Tokens (LRT). The end goals of liquidity staking and liquidity re-pledge protocols are similar: to provide re-stakers and stakers with a liquidity representation of their underlying positions. Therefore, LRT can be formally defined as a derivative asset that replenishes positions. The LRT provider is ultimately responsible for portfolio management on behalf of re-hypothecaters, managing the allocation of pledges across various yield positions to maximize returns and minimize risk to depositors. For a more detailed breakdown of LRT, see Shoal Research’s previous report.

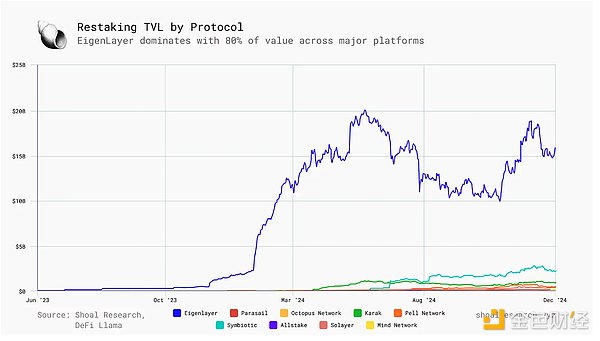

The current state of re-hypothecationAs of this writing, the total number of actively re-hypothecated assets has reached $28.14 billion. Among them, Eigenlayer accounts for 60% of the total, and Ethereum as a whole accounts for about 80% of the total TVL (total locked value) of re-pledges. So far, only EigenlayeThe TVL of four rehypothecation protocols, r, Babylon, Symbiotic, and Karak, exceeded $1 billion.

At the same time, the liquidity re-pledge agreement has also evolved with the development of re-pledge. Growing rapidly, its total TVL reached approximately US$15.62 billion, accounting for approximately 57% of the total re-pledged TVL.

Compared with re-staking, the competition for liquidity re-staking is more intense, and since June 2023, different protocols have taken turns to occupy the leading position in the market. As of this writing, EtherFi accounts for ~50% of all liquidity restaking deposits, and the majority of liquidity restaking TVL is concentrated in Ethereum, consistent with the overall trend of restaking.

Restaking is slower to develop on Solana: Picasso Network in 2024 The re-pledge vault was first launched on Solana at the end of January and has attracted deposits of 3,507 SOL (approximately US$729,000) so far. As of now, the total TVL restaking on Solana is approximately $371 million, with the majority of that added in the past few months with the launch of Solayer.

Currently, restaking on Solana is starting to heat up as Jito enters the market with its Jito (Re)staking protocol.

Re-staking on SolanaSolana is built from scratch with a unique architecture and optimization Provides fast execution speeds and low-cost transactions with high transaction volumes. Solana is designed to maximize the developer and user experience by taking full advantage of hardware performance capabilities, ultimately making hardware the only long-term limiting factor in network performance. As the chain with the second highest TVL (Total Locked Value), the re-staking ecosystem on Solana has the potential for growth and change in the medium to long term. Jito is one of the teams looking to introduce restaking into the Solana ecosystem and leverage its history of successful product development.

Jito IntroductionJito LabsFounded in 2021 by Lucas Bruder and Zano Sherwani, Solana is a US-based infrastructure company that offers a suite of MEV (Maximum Extractable Value) products and services. Jito Labs is the core development team focused on product development and deployment, while Jito Foundation is responsible for JTO token governance and strategic oversight of Jito network products and services such as the JitoSOL liquidity staking token and the Jito (Re)staking protocol.

In July 2022, Jito Labs first launched the MEV dashboard to help reveal the MEV ecosystem on Solana that had not yet been deeply explored at the time. A few months later, the team open-sourced Jito-Solana, the first validator client on Solana designed to capture and redistribute MEV profits to validators and stakers. Jito-Solana was ultimately forked from the Solana Labs client, adding about 1,000 lines of code to enable validators to earn MEV rebates. Its broader goals are to combat spam on the network and optimize Solana’s performance.

Working with the client, Jito Block Engine supports off-chain block space auctions, and searchers submit transaction lists (i.e. transaction packages) that are executed sequentially and atomically. After simulating each transaction combination in the submitted package, the engine forwards the highest paying transaction package to the leader for inclusion in the block. Jito Relayer acts as a transaction processing unit (TPU) agent, filtering and validating transactions off-chain, and submitting verified transactions to the block engine and validator.

It should be noted that in March 2024, Jito Labs announced the suspension of the memory pool function of Jito Block Engine because the Solana ecosystem has restricted some users running MEV robots. Concerns were expressed about exploiting memory pools for sandwich attacks. Currently, the Block Engine is still running and continues to process and forward transactions while conducting transaction package simulation, but the memory pool component has been removed.

This mechanism ultimately imposes costs on the network for transaction spam and performance impediments. Validators running Jito-Solana capture MEV profits generated in transaction packages during their leadership period. The launch of JitoSOL’s liquid staking token enables stakers to delegate their pledgesTo validators running the Jito-Solana client, thereby increasing the validator's stake amount and allowing stakers to earn MEV rewards while receiving basic staking benefits. In December 2023, the Jito Foundation also launched StakeNet, a network composed of on-chain guardians and managers that provides two core functions:

1. Validator history program: stores the 3-year history of each validator in the entire network;

2. Guardian program: Calculate scores based on validator performance and manage pledge distribution to ensure that pledges are delegated to the best-performing validators.

Building on its experience with MEV and liquidity staking infrastructure services, Jito is introducing a new framework that enables applications and networks to leverage any SPL token for security.

Jito (Re)stakingOn July 25, 2024, the Jito Foundation released the Jito (Re)staking code, which is a hybrid multi-staking token on Solana. An asset staking protocol that allows any new network or application to bootstrap its economic security. The protocol consists of two main components:

•Vault Program: used to create and manage pledged assets;

•(Re)staking Program: Coordinates activities and incentives among network participants.

Together, these two core programs provide developers with a modular, extensible framework for simplifying the staking mechanism of any SPL asset, becoming the best solution on Solana. The first agreement of its kind.

Before we dive in, here is a brief explanation of some important terms:

Node (Node): refers to software that runs according to its associated network specifications.

•Node Consensus Network (NCN): a group of distributed nodes that jointly achieve consensus and provide services for specific protocols or networks, including L1 public chains and application chains , cross-chain bridge, co-processor network, DeFi applications, solver networks, and oracle networks.

•Operator: An entity that manages one or more nodes in the node consensus network.

•Vault Receipt Token (VRT): A derivative token that represents the underlying recollateralized position, similar to LRT (Liquidity Recollateralized Token).

In short, Jito (Re)staking provides NCN with economic security and improves liquidity and Composability. NCN is able to configure staking parameters, penalty conditions, and other economic incentives according to its needs.

Vault ProgramThe Vault Program is responsible for managing the creation and operation of Vault Receipt Tokens (VRT). The core logic is: stake a token and obtain derivative tokens representing the pledged liquidity position, which can be used to protect the underlying NCN. Jito (Re)staking allows any SPL asset or a combination of multiple SPL assets to serve as the underlying asset, enabling stakers to more effectively diversify their VRT holdings, create a more balanced risk-reward portfolio, and use a wider range of assets within the Solana ecosystem. assets.

Vault Program allows NCN to manage VRT operations (casting, destruction, delegation), and Enforce your own penalty conditions and deposit/withdrawal caps. This is particularly important because not all SPL assets are equally secure, and the security requirements and conditions of different NCNs can vary significantly due to differences in underlying functionality. Additionally, the Vault Program allows NCN to implement custom VRT delegation strategies across multiple operators, DAOs, multi-signatures, or on-chain automation protocols such as the StakeNet Guardian Program.

Restaking ProgramWhile the Vault program is responsible for managing VRT, the Restaking Program is responsible for managing NCN and its corresponding operators. This includes implementing various opt-in mechanisms, as well as managing the distribution and enforcement of reduction conditions.

The Vault program and the re-pledge program together create a modular framework that enablesStart economic security with any SPL asset. Jito (Re)staking further simplifies the process for developers and NCNs, providing a simple and customizable interface to manage VRTs and operators.

The main advantages of Jito (Re)stakingJito (Re)staking aims to achieve consensus and gain by providing a modular, asset-agnostic framework for NCN Economic security, thereby alleviating the cold start problem prevalent in the current on-chain economy.

First of all, Jito (Re)staking allows anyone to create VRT using any SPL asset, simplifying the design process of token economics and token utility; any Tokens can all become liquid pledged or re-staking assets while maintaining governance compatibility and enforcing necessary security parameters. Additionally, Jito (Re)staking allows for multi-asset staking, meaning NCN can also leverage existing assets with deeper liquidity and wider token distribution, as well as its native token, to achieve wider market accessibility.

Another core advantage is that Jito (Re)staking allows NCN to configure and fine-tune risk parameters. NCNs built on Jito (Re)staking can implement more complex risk management and security models to meet their specific needs, such as multi-layer slashing penalties or multi-asset slashing to achieve deeper economic security.

At the same time, treasury, operators and NCN can choose who they integrate based on risk tolerance; treasury can choose which operators and NCN to entrust, and Operators and NCNs can choose which vaults and assets they want to support. Vaults can also choose to join specific haircut conditions determined by the NCN to better manage the amount of assets at risk at a given time. To ensure the safety of users and assets, all program funds are securely stored in the Vault program and can only be withdrawn through user actions or slash events.

Roadmap and AdoptionSince the launch of Jito (Re)staking, multiple teams and protocols have announced cooperation and integration plans:

•Switchboard - A decentralized oracle network on Solana, Switchboard plans to enhance its capabilities with multi-layer slashing and customizable staking parameters.economic security, thereby improving the quality and performance of their data feeds. This will make Switchboard the first Node Consensus Network (NCN) to integrate Jito (Re)staking.

•Squads - Decentralized treasury management protocol on Solana Squads Protocol is integrating Jito (Re)staking into its upcoming Squads Policy Network (SPN) to coordinate and incentivize activity among network participants and improve reliability and performance. SPN will provide more advanced digital asset management security and flexibility by enabling granular and versatile trading strategies for smart accounts.

•Renzo - The leading liquid re-staking protocol policy manager on Ethereum Renzo will launch its ezSOL as a VRT leveraging Jito (Re)staking. Anyone can mint ezSOL by staking JitoSOL and earn from a combination of staking rewards, re-staking rewards, and MEV tip income.

•Sonic - The first game SVM on Solana Sonic will integrate Jito (Re)staking in its upcoming HyperGrid shared state network and HyperGrid bridge. Jito (Re)staking’s NCN model will add an economic security layer for validators to securely prevent state conflicts in HSSN and enhance the core bridging infrastructure with multi-layer slashing and customizable staking parameters to enable atomic ized SVM ↔ Solana exchange.

•Fragmetric - Fragmetric launches FragSOL, the first liquid re-staking token native on Solana, as a VRT for Jito (Re)staking. FragSOL will leverage Solana’s token scaling capabilities to accurately distribute NCN rewards and introduce a standardized token process to efficiently manage multi-asset staking and slashing.

•Ping Network (formerly Twilight) - Twilight, the upcoming privacy DePIN project on Solana, will leverage Jito (Re)stakingEnhance the decentralization and economic security of its validator network. Twilight will utilize multi-level slashing and customizable staking parameters to ensure strong protection of its privacy infrastructure.

•Kyros - kySOL combines staking, MEV and re-staking rewards into one token to optimize returns. Users can cast kySOL using JitoSOL or SOL. Kyros is also partnering with Jito, Kamino, and Raydium to launch an incentivized liquidity pool, which will enhance kySOL’s liquidity and open up more opportunities for the DeFi ecosystem.

Key Risks and ConsiderationsBefore explaining the reasons for restaking on Solana and assessing Jito’s positioning, it is worth reviewing the key risks involved. Both re-staking and liquidity re-staking introduce a set of interrelated risks that impact different participants in the ecosystem.

Core risks of staking blockchain

Proof-of-Stake, PoS ) The core of the blockchain is to provide security through the slashing mechanism. The reduction mechanism uses a penalty mechanism to penalize validators that violate protocol rules (such as censoring blocks) or perform poorly over a period of time (such as excessive downtime), confiscating part of their pledged assets. When this mechanism is applied to restaking protocols, the risk is further amplified, as operators bear the additional risk of slashing any application or Node Consensus Network (NCN) they protect.

Although this risk is compensated by providing higher rewards to stakers and operators, the economic impact cannot be tolerated under the larger scale of federated security adoption. ignore. Slashing not only penalizes validators, but also affects stakers who delegate capital to them, resulting in less rewards due to less staking. In a re-hypothecation protocol, the more concentrated the staking distribution is (i.e., the majority of the staking is held by a small number of operators), the greater the overall haircut risk.

This situation may affect the security of the underlying chain used to protect NCN, especially if a large number of pledges in the network are re-staked and slashed, controlling The cost of staking a majority on the network may therefore be reduced. The price fluctuation of the underlying asset also plays an important role, the greater the price fluctuation, the higher the risk faced by the underlying protocol or NCN.

Currently trimmedLack of reduction mechanism

It is worth noting that most (if not all) re-staking protocols have not yet implemented reduction mechanisms. Therefore, the lack of deterrence against malicious behavior or poor performance by operators instead poses greater risks to stakers and NCNs, especially those with fewer capital resources and greater impact of financial losses.

For example, some restaking protocols (such as Eigenlayer) have developed frameworks to solve subjective failures—that is, problems that cannot be easily verified on-chain. Objective failures apply to violations that are mathematically and cryptographically provable on-chain (such as double-signing or lengthy outages), while subjective failures must be resolved off-chain through some kind of social consensus among network participants.

Transparency and trust issues

This raises questions about transparency and trust in these systems Hypothetical issues, off-chain resolution can be complex and time-consuming processes, and may even lead to a base layer fork if there is enough controversy and disagreement surrounding the correct state of NCN. Eigenlayer plans to mitigate this risk by using the EIGEN token, which enables validators to enforce slashing penalties for subjective failures, performing slashing by forking the token rather than the base layer.

The impact of market-driven incentives

Need to consider the impact of market-driven incentives on operators and pledges influence of the person. In order to enhance the economic security of NCN, pledged capital must be sticky, that is, remain stable over the long term. However, without some kind of long-term commitment enforced through mechanisms such as lock-up periods (which in turn poses risks to operators and stakers), operators may move their stake at any time in pursuit of the highest possible returns.

Incentivizing NCNs to compete for operators by offering higher returns (usually inflationary token issuance) does not benefit the broader ecosystem in the long run , but may repeat past mistakes in the design of encryption protocol incentive mechanisms (such as the imbalance between protocol income and expenditure in liquidity mining).

Key considerations for liquidity re-hypothecation

Shoal Research explored this in a previous report Some key risks in liquidity re-hypothecation include:

•Supported Deposit Asset Risks - Vault Receipt Tokens (VRT) are subject to the risks of their underlying assets. Native Redemption Tokens face different risks than Liquidity Staked Tokens (LST).

•Liquidity acquisition risk - some re-hypothecation protocols have a custody period when the pledged assets are canceled (such as Eigenlayer's 7 days). This mechanism raises concerns about term risk and potential liquidity issues. If there is insufficient liquidity in the secondary market, investors may have difficulty selling VRT at a fair market price. The cooling-off period for Jito (Re)staking is approximately 4. -5 days (two epochs). Asset redemption time and the liquidity of the VRT provider play a key role in this risk

•Smart contract risk. ——Need to evaluate VRT Risks of the protocol architecture, including reward distribution mechanism, fee structure and multi-signature permissions, etc. These factors may affect asset transfer and withdrawal

•Oracle risk—— Reliable price data is critical to maintaining VRT pricing. Inaccurate oracle data may lead to VRT mispricing, thereby creating systemic risks during redemptions or liquidations.

•Governance Risk – Choosing How to Protect NCN The mechanism is crucial in ensuring its long-term stability. There must be a trade-off between granting power to a large number of stakeholders (time-consuming) and granting power to a small number of actors (such as 5/3 multisig).

•Cross-chain bridging security risks - For cross-chain VRT, the risks introduced by the basic bridging mechanism need to be considered. There are different trade-offs and risks for both native bridges and third-party bridges.

•Cyclic risk – in lending markets, using VRT Carrying out recursive borrowing (looping) may lead to cascading liquidations in periods of high volatility, similar to the stETH depeg event in 2022. However, this risk is mainly targeted at the lending market and does not pose a significant risk without large-scale adoption.

Reasons for re-stakingSince the launch of Eigenlayer on Ethereum, research and development work in the field of re-staking has accelerated significantly. Currently, Eigenlayer has accelerated. Ranking third in total volume locked (TVL) on the Ethereum network, Solana has re-established its leadership as the foundation layer for application development, second only to Ethereum’s TVL despite a large increase in Q4 2023. Partial growth momentum (mainlyFueled by a surge in meme coin trading activity) has gradually slowed down, but many new products and services are being developed on Solana, including several key infrastructure projects. In addition, the new SVM API launched by Anza enables developers to build SVM-based projects on the Solana mainnet beta, paving the way for a new era of SVM L2 and application chains. These L2 and application chains may become important sources of demand for Jito (Re)staking.

Comparison of Ethereum and Solana re-staking

1. Liquidity gap

Ethereum's liquidity is far greater than Solana's (TVL is about 9-10 times that of Solana), making it a powerful base layer with greater economic security.

2. Growth space

Solana’s current development potential and growth space are greater. The staking incentive mechanism can play an important role in improving the TVL of the network.

3. Capital efficiency

Liquidity re-pledge strategy management requires constant reallocation of capital. And continue to incur gas costs. The cost of managing re-staking on Solana is significantly lower than on Ethereum, making it more capital efficient.

4. Differences in ecological needs

More teams in the Solana ecosystem focus on applications Development, not infrastructure building. This raises questions about the origin of the requirements for the restaking protocol, as the application's requirements structure may be different from NCN. For example, AMMs like Raydium do not need to launch their own set of validators in their current state.

Nonetheless, the rise of SVM-L2 and application chains has brought a new flow of economic security requirements, providing re-staking solutions to meet this demand. Important opportunity.

Jito’s roleAs of now, about 93% of Solana validators are running the Jito-Solana client, with a total of 2.5k SOL tokens distributedfees, involving 6.5 million transaction packages.

JitoSOL’s deposits have grown to 14.5 million SOL (approximately US$3.14 billion), $644 million in charges have been incurred to date. JitoSOL has steadily grown its position in the Solana liquidity staking space and currently accounts for approximately 45% of total TVL.

Demand for lending JitoSOL on Kamino Finance continues to grow, with utilization rates approaching 100%.

The competitive landscape of Jito (Re)stakingAlthough Jito is widely present in Solana, There are still a number of key catalysts and protocols that pose credible challenges to the adoption of Jito (Re) staking. First, there is already another re-staking protocol on Solana, Solayer, which launched in June 2024 and has amassed a whopping $168 million in deposits. Solayer features a re-staking architecture and shared validator network designed to provide Solana applications with enhanced capabilities to protect block space and prioritize transaction inclusion.

Secondly, Solana also faces competition from other native teams, especially liquidity staking protocols, which may be well-positioned and motivated to build their own Pledge products. For example, Sanctum positions itself as the unified liquidity layer for Solana LSTs, enabling all LSTs (regardless of size) to share a deep liquidity pool and operate with minimal liquidity constraints. To date, Sanctum’s Reserve, Infinity and Validator LSTs have attracted over $1 billion in TVL. Helius, the core RPC provider on Solana, launched their hSOL LST with Sanctum, with over 13 million SOL currently staked. Binance’s BNSOL currently leads the way with 6.77 million SOL staked on the platform. Another notable Solana native competitor is Marinade Finance. Marinade back in 2021Its liquidity staking protocol, which launched in 2017, currently has a TVL of just over $1.8 billion and lifetime fees of $181 million. While neither team has mentioned re-staking at the moment, it’s not far-fetched to imagine these teams developing their own competitive re-staking products. The launch of Karak appears to have opened the floodgates for restaking competitors on Ethereum, and a similar effect will likely play out on Solana.

Finally, universal recollateralization protocols such as Symbiotic and Karak will face competition if they choose to adopt a chain-neutral approach that supports SOL and SPL/Token2022 assets. Even Eigenlayer is starting to change tack, launching permissionless token support that will make any ERC-20 asset available for rehypothecation. Thinking beyond Ethereum, though, Eigenlayer ultimately positions itself as an “innovative orchestration engine.” If application development and value accumulation on Solana one day exceeds that of Ethereum, there is no reason for Eigenlayer not to adapt to the demand and set up shop on Solana in that case. However, this is a long-term hypothetical scenario and there is no guarantee that Eigenlayer will always be the leading restaking protocol, so it is unclear how much of a threat it would pose to Jito (re)staking.

In this context, Jito needs to rely on its successful record in the Solana ecosystem and ensure that the Jito Foundation continues to optimize the re-staking protocol and respond to NCN and operators in a timely manner and other protocol participants’ needs and feedback.

Jito (Re)staking application scenariosRe-staking protocols benefit from the increase in middleware solutions that require coordination mechanisms to meet business needs. The development of NCN is still in its early stages and may span multiple areas. The following are potential application scenarios for Jito (Re)staking:

•Decentralized solver network:

DEX and liquidity platforms that adopt solver architecture can launch their own decentralized solver network, distribute revenue and impose cut penalties on solvers to incentivize them to execute transactions at the best price.

•SVM L2:

With SolanaSVM L2 is emerging as applications increase demand for faster block confirmation times and customized economic incentives, driving the need for economic security, where Jito (Re)staking can meet the demand.

•Order flow auction and MEV redistribution protocol:

Solana DEX can implement order flow Auction and distribute the value obtained through MEV to traders or token holders, similar to CoWSwap on Ethereum.

ConclusionAlthough there are still significant gaps in the field of re-staking from conception to reality, it is generally believed that re-staking will be the driving force behind the vigorous development of on-chain applications Key development directions that help enhance its economic security and capital efficiency. This can be compared to the impact of Amazon Cloud Service (AWS): by providing a cloud computing platform that rents computing resources on demand, AWS has promoted the rapid rise of web application development.

By outsourcing computing resources and infrastructure construction, web developers can devote more time and resources to creating valuable products and services, and more Understand user needs well. Likewise, the Re-Staking Protocol enables blockchain-native applications and networks to outsource economic security concerns to focus on developing valuable products and services while inheriting the key features and benefits of blockchain.

Re-staking on Solana is on the rise, and Jito (Re)staking is well-positioned to become the protocol of choice to drive the launch of new innovative products and services.