23 mins ago

2,318

Article author: nic carterArticle compilation: Block unicorn

Venture capitalist Marc Andreessen Appearing on Joe Rogan’s podcast made some explosive claims claiming there is a systemic “de-banking” of unpopular companies and individuals, particularly in the crypto industry. At the beginning of the video, he pointed to the Consumer Financial Protection Bureau (CFPB), which was created under the leadership of Elizabeth Warren, as the main culprit in causing crypto startups to be debanked. However, some critics counter that not only has this “de-banking” not happened, but that the CFPB’s actual goal is to end it.

The problem is that there are several different issues to discuss here. First, what is Marc Andreessen complaining about, and are his concerns justified? Second, what role, if any, did the CFPB play in the debanking process—was it an instigator or a curb?

Many on the left are unaware of the crypto industry and the right’s concerns about debanking in general, and therefore reacted to Mark’s remarks and Elon’s repost on social platform Feeling confused or disbelieving. First of all, I think it's worth reading Mark and Joe's conversation in its entirety because many people are reacting based only on snippets when this is actually an in-depth review that includes many independent points. Next, let’s dig a little deeper.

What is Marc Andreessen complaining about?

Mark makes some clear and interconnected points on the show. He began by criticizing the Consumer Financial Protection Bureau (CFPB), arguing that it is an "independent" federal agency with little oversight and is able to "intimidate financial institutions and prevent new competition and new startups that try to compete with the big banks." .

He then mentioned debanking as a specific hazard, which he defined as “when you as an individual or your company are completely removed from banks removed from the system." Mark noted that this phenomenon occurs through banks acting as agents (similar to the censorship implemented through big tech companies), but in an indirect way that shields them from direct liability.

According to Mark, debanking “has been happening in all Canadian banks over the past four years.Cryptocurrency entrepreneurs. This also happens to many fintech entrepreneurs, and anyone trying to launch any new banking services, because they () are trying to protect the big banks. Among other things, Mark mentioned a number of businesses that were not favored by the government during the Obama administration - legal marijuana, the escort business, and gun stores and manufacturing. It was called Operation Choke Point, created by Obama's Justice Department) and "Operation Kill 2.0" (named after the crypto industry) targets "enemies" and those "undesirable tech startups" Mark added, "This has a huge impact on the technology sector. . We've had about 30 founders go bankrupt in the last four years. ”

Victims "basically include every crypto founder, every crypto startup, who have either been personally debanked and forced out of the industry, or Their companies were debanked, unable to continue operating, or they were sued by the SEC or threatened with charges. ”

Mark also mentioned that he understands that some people have been debanked because they "held wrong views or made unacceptable comments."< /p>

To summarize, Mark makes the following claim:

Debanking means individuals or companies Being deprived of banking services either because your industry is not favored by the government or because you hold dissident political views

The CFPB bears at least some responsibility, as do other unnamed federal agencies

This is accomplished by having regulators outsource financial repression to banks, which insulates them from direct liability

The main victims of debanking during the Obama administration were legal but unpopular industries — marijuana companies, adult businesses, gun stores and gun manufacturers

Crypto companies and entrepreneurs, as well as fintech companies, are the main victims of debanking under Biden. Conservatives are also sometimes debanked simply because of their views

30 in a16z portfolio A technology entrepreneur encountered a dilemmaConsumer banking services.

We will evaluate these points at the end of the article.

What do critics say about Marc Andreessen's remarks?

I'm simplifying, but left-liberals are unhappy with Marc Andreessen's comments because they believe he is using the debanking narrative to satisfy himself purpose (supporting cryptocurrencies and fintech), while ignoring the more “legitimate” victims of debanking — such as the Palestinians who were kicked off Gofundme for funding Gaza. As for the mainstream left, they are generally vocal in their support of debanking their enemies, so they would rather ignore the whole thing.

But there is a segment of the left that is at least ideologically consistent and skeptical of corporations and the power of speech and finance. (This group may be growing now that the right has regained control of some tech platforms and regained power). They have been fighting against debanking. They recognize that while right-wing dissidents are the primary victims of debanking (think Kanye, Alex Jones, Nick Fuentes, etc.), the left could just as easily suffer if the reverse were true. They define debanking more narrowly: “Debanking, or as some financial institutions prefer to say, de-risking, is when banks interact with customers who are deemed politically incorrect, extreme, dangerous or out of bounds Cut ties.” (Excerpted from this article by TFP). Upa Subramanya mentioned in this article that banks have the power to completely ruin a person's financial life if they consider that person a risk to reputation and unable to do business. Individuals on both the left and right have been affected - Melania Trump, Mike Lindell, Trump himself, Christian charities, January 6th attendees, Muslim crowdfunding organizations and charities Institutions etc.

Yet many on the left remain critical or confused by Anderson's comments, especially regarding the Consumer Financial Protection Bureau. Here are a few examples:

Lee Fang: The CFPB has always been strongly opposed to debanking. Why did Anderson say that? Where is the evidence? What's not mentioned in this long article is that the CFPB investigated Anderson-backed startups for fraud, not speech. Debanking comes from the FBI and Department of Homeland Security (DHS), not the CFPB.

Lee Fang: Debanking is indeed a big problem. We’ve seen truckers who oppose mandatory vaccines lose their bank accounts for protesting, pro-Palestinian groups losing access to their Venmo accounts, and more. But now, predatory lenders and fraudsters are conflating consumer protection with “de-banking” and calling for deregulation.

Jarod Facundo: I really don’t understand what @pmarca is talking about because just a few months ago, at a FedSoc event, CFPB Director Chopra (Chopra) warned viewers that Wall Street was "debanking" but gave no explanation.

Jon Schweppe: I agree with @dorajfacundo. Have no idea what @pmarca is talking about. The CFPB has been leading the charge against discriminatory debanking. What does this mean?

Ryan Grim: The CFPB issued a legally good rule targeting banks that debank users based on their opinions. Yes, a populist left-wing CFPB chief is standing up for conservatives. Now, venture capitalists and Musk don't like the CFPB for other reasons, and they're lying, inflaming people's emotions, and weakening the CFPB.

Overall, this group is hostile to cryptocurrencies and fintech and does not view companies in these industries as victims of "debanking," at least They are not considered ethically equivalent to crowdfunding platforms that send money to Gaza. According to left-liberals, crypto practitioners are “bringing it to their own devices.” They argue that cryptocurrency practitioners issue tokens, scam and commit fraud, and therefore they should be looked down upon by banks. “If crypto founders are debanked, that’s a problem for bank regulation, not our fight.”

Furthermore, according to these critics, Mark's mistake was blaming the Consumer Financial Protection Bureau. They tell us that the CFPB is an agency fighting "debanking." Mark is only upset with the Consumer Financial Protection Bureau because he invested in fintech platforms and the Consumer Financial Protection Bureau is responsible for making sure they don't defraud customers.

Since Mark’s appearance on Rogen’s show, dozens of tech and cryptocurrency founders have spoken out about their experiences of being unilaterally stripped of access to their banks. Many in the cryptocurrency industry see light at the end of the tunnel and believe that the unconstitutional assault on the cryptocurrency space by banking regulators through banks is nearing its end. Calls for an investigation into Operation Kill 2.0 are growing. So who is right? Anderson or his critics? Is the CFPB really guilty? Is debanking really as serious as Mark says? Let’s start our investigation with the CFPB.

What is CFPB?

The Consumer Financial Protection Bureau (CFPB) is an "independent" agency established in 2011 by the Dodd-Frank Act ) was established after the financial crisis. It has broad remit and is authorized to oversee banks, credit card companies, fintech companies, loan sharks, debt collection agencies and student loan companies. As an independent agency, its funding comes from outside Congress (and therefore is not subject to congressional funding review). The president cannot easily remove the director, it can directly write rules and bring enforcement and legal proceedings in his own name. It has considerable power. The CFPB was formed essentially at the exclusive behest of Senator Elizabeth Warren.

The CFPB is often targeted by conservatives and libertarians alike because it is another federal agency, and a largely unaccountable one at that. It was set up by Elizabeth Warren, a frequent target of right-wing attacks, to effectively harass fintech companies and banks. Of course, most of these companies are already heavily regulated. Banks are subject to state or federal supervision (OCC) and, if they are public companies, accountable to the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve, and the Securities and Exchange Commission. Credit unions, mortgage lenders, etc. all have their own regulatory agencies. Before the creation of the CFPB, federal financial regulation was not sorely lacking. The United States has more financial regulatory agencies than any other in the world. It’s understandable, then, that conservatives will question why Elizabeth Warren, who appears to be motivated solely by revenge, has been given an exclusive agency she can use to harass her opponents at will.

Now let’s talk about the CFPB’s responsibilities.

As for the functions of the Consumer Financial Protection Bureau (CFPB), it does have some specific regulations, usually against discrimination in bank access. In particular, the Equal Credit Opportunity Act (ECOA) and the "Fraudulent, Unjust, or Abusive Practices" section (UDAAP) of the Dodd-Frank Act are relevant legal frameworks. ECOA prohibits discrimination based on certain protected categories, including race, color, national origin, gender, marital status, age, or receipt of public assistance.

As far as the issue of "Operation Stifling" mentioned by Marc Anderson is concerned, these regulations do not apply. Under the law, “cryptopreneur” or “conservative” are not protected categories. Therefore, this part of the CFPB’s functions does not theoretically involve the issue we are discussing: targeted suppression of specific unpopular industries. Furthermore, this provision applies to credit access, not banking in general.

The UDAAP portion of the Dodd-Frank Act is another regulation that may be relevant to debanking. It gives the CFPB broad authority to pursue conduct it deems unfair, deceptive or abusive. Their massive settlement with Wells Fargo falls under UDAAP. In theory, if the CFPB were to take action against debanking, they should do so under UDAAP. But so far, the response has been loud but little rain, and they have not taken any substantive action.

What the CFPB is doing

Recently, the CFPB finalized a rule that would Wallets and payment apps are included in its regulatory scope, making it more like a bank. The rule requires large digital payment apps, such as Cash App, PayPal, Apple Pay and Google Wallet, to provide transparent explanations for account closures. They specifically mentioned "de-banking" in their rule release. Keep in mind that this rule does not apply to banks, but to “big tech companies” or p2p payment apps. In any case, as of now, this rule has not been implemented in practice, so we will need to see how it is implemented in the real world.

Will this rule inhibit something like Operation Kill 2.0? Almost impossible. First, it covers the behavior of technology companies, not banks. Second, the stranglehold-style behavior was not optional behavior at the bank level, but the result of federal regulators cracking down on the entire industry through the banks. For example, if the CFPB noticed that cryptocurrency startups were being systematically cut off from banking operations, they would have to confront the Federal Deposit Insurance Corporation (FDIC), the Federal Reserve, and the Office of the Comptroller of the Currency (OCC) (and eventually the White House) to End this practice. Given Elizabeth Warren’s staunch anti-crypto sentiments, one can’t help but wonder if the CFPB will do the same. More importantly, killing the lineThe dynamic concerns bank regulators overstepping legal boundaries to remove banking services from entire industries. This has nothing to do with malfeasance on the part of individual banks (the banks were simply helplessly complying with the regulators' orders).

Under UDAAP, the CFPB could theoretically review systemic account closures targeting an industry, such as cryptocurrency. But this recent payment application rulemaking does not apply to banks, and some critics of Marc Andreessen have cited the rule to illustrate the CFPB's opposition to debanking. Moreover, the CFPB has so far been silent on debanking in its actual enforcement actions.

What are the main enforcement contents of the CFPB?

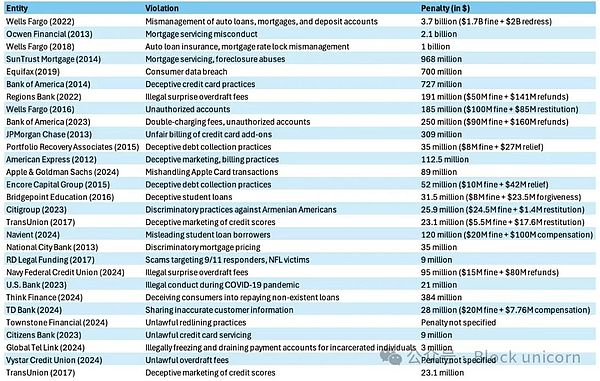

I couldn't find any CFPB settlements related to "debanking." Here are the CFPB’s 30 largest settlements, sorted by dollar amount:

I can The closest or related case found was the 2023 Citibank case, which exposed their discrimination against Armenian-Americans in credit card applications. ((The bank ostensibly did this because California’s Armenian community had experienced higher fraud rates, largely due to fraud syndicates.) Citibank paid a $25.9 million fine.

In 2020, the CFPB found that Townestone Financial used its marketing to prevent African Americans from applying for mortgages. The company paid a $105,000 fine.

Both nationality and race are considered protected groups under U.S. law, so neither case is purely red-lining, as critics of cryptocurrency debanking have complained. p>

Furthermore, I looked at 50 recent CFPB settlements since March 2016, and none of them involved arbitrary deprivation of access to banking services in the most recent. Of the 50 cases, 15 involved UDAAP violations (such as the infamous Wells Fargo case), 8 related to fair lending violations, 5 related to student loan servicing, 5 related to credit reporting inaccuracies, 5 related to mortgage loan servicing, 4 related to auto loan discrimination, 3 cases involving illegal overdrafts: None./p>

What is the substance of Mark’s criticism of crypto/fintech companies and conservatives being debanked?

At this point, there is no real ambiguity. I have documented in detail the phenomenon known as "Operation Kill 2.0," in which Biden reinstates the financial redlining practices that Obama began implementing around 2013. At that time, Obama's Justice Department launched "Operation Kill," an official DOJ program designed to target legal but politically unpopular industries such as loan sharks, marijuana, adult care, and gun manufacturers through the banking industry. Iain Murray's article Operation Stifle: What it is and why it matters provides a good discussion of this. Under Marty Gruenberg, Obama's FDIC used hints and threats to persuade banks to "de-risk" companies in more than a dozen industries. Conservatives expressed displeasure, with members led by House Rep. Luetkemeyer exposing the practice. Critics argue the approach is unconstitutional because it involves secret regulation through persuasion rather than official rulemaking or legislation.

In 2014, a DOJ memo about the practice was leaked, and the House Oversight and Reform Committee released a key staff memo about the practice. The Federal Deposit Insurance Corporation issued new guidance to banks, encouraging them to assess risks on a case-by-case basis rather than redlining entire industries. In August 2017, Trump’s Justice Department officially ended the practice. In 2020, Trump’s comptroller, Brian Brooks, issued “fair access” rules aimed at ending debanking based on reputational risk.

However, in May 2021, Biden's acting comptroller, Michael Hsu, revoked the rule. In early 2023, following the FTX crash, people in the cryptocurrency industry, myself included, noticed that similar strangulation tactics were being used against cryptocurrency founders and companies. In March 2023, I published “Operation Strangle 2.0 is underway and cryptocurrencies are becoming its target,” followed by another article in May detailing the new findings.

Specifically, I discovered that the FDIC and other financial regulators have secretly set a 15% limit on bank deposits for cryptocurrency-related companies upper limit. Furthermore, ICryptocurrency-focused banks Silvergate and Signature were unfairly forced to go bankrupt or close due to anti-crypto sentiment. Cryptocurrency companies have struggled to access banking services since then – although there are no official public regulations mandating banking restrictions on crypto companies, nor any related legislation. Law firm Cooper and Kirk has once again accused Operation Strangler 2.0 of being unconstitutional.

Recently, as the cryptocurrency industry remains shackled by this secretive regulation, I took another look at the practice and uncovered new evidence that Silvergate Bank was Execution rather than natural death.

Today, crypto-focused banks still impose a 15% deposit cap, which Stifling the development of the industry. Every U.S. crypto entrepreneur has suffered from this—and I can attest to it, as do about 80 of our portfolio companies. My firm, Castle Island, a general venture capital fund that only handles fiat currencies, also experienced the sudden closure of some of its bank accounts.

After Mark’s appearance on Rogen’s show, many cryptocurrency executives also weighed in. David Marcus explains how Facebook’s Libra project was killed by Janet Yellen. Kraken CEO Jesse Powell, Joey Krug, Gemini CEO Cameron Winklevoss, Visa’s Terry Angelos, and Coinfund’s Jake Brukhman also shared their stories. Caitlin Long has long campaigned against Stifle 2.0 and even founded her own bank, Custodia, which was stripped of its main account by the Fed. Critics may not be sympathetic to the crypto industry, but the fact is that it is a perfectly legal industry that has been silenced by secret letters and insinuations from banking regulators. As a result, the United States has launched a broad crackdown on crypto banking, which has been implemented not through legislation or rulemaking in a democratic process, but entirely through administrative agencies.

Besides cryptocurrencies, similar actions against financial technology are also quietly unfolding. Since the start of 2023, one in four FDICEnforcement actions targeted banks that partnered with fintech companies (the proportion of banks that did not partner with fintech companies was only 1.8%). . As an investor in the fintech space, I can attest that finding banking partners for fintech companies has become a huge challenge, comparable to the difficulty cryptocurrency companies face in obtaining banking services. The Wall Street Journal criticized the constitutionality of the FDIC's action, saying the agency "actually engaged in rulemaking while bypassing the notice and public comment periods required by the Administrative Procedure Act."

As for Anderson’s comments about conservatives being disconnected from their bank accounts, we have ample anecdotal evidence that this is happening. Melania Trump mentioned in her recent memoir that she was disconnected from her bank account. The same thing happened to the right-wing speech platform Gab.ai. In 2021, JPMorgan Chase canceled General Michael Flynn's bank account, citing reputational risks. In 2020, Bank of America canceled the account of the Christian nonprofit Timothy II Project International, and in 2023 froze the account of Christian missionary Lance Varnau. In the UK, Nigel Farage caused a minor scandal when he was debanked by Coutts/NatWest Bank. These are just a few of many examples. Under current law, Bank of America can close an account for any reason without giving an explanation. So, in essence, Anderson is right.

Why are critics trying to limit discussion of "debanking"?

What critics have in common is that Anderson has somehow used the term "debanking" to advance his own economic agenda. Writer Lee Fang said:

"The issues around debanking are very serious. We've seen truck drivers who oppose mandatory vaccines lose their bank accounts in protest, and supporters of Palestinian Organizations lose access to Venmo, etc. But now predatory lenders and fraudsters are conflating consumer protection with 'debanking' and calling for deregulation. ”

Axios author hints that Anderson worries CFPB because his firm invested in dubious neobanks like Synapse, which collapsed earlier this year. It became a common theme in the comments that Anderson only cares about “debanking” because he wants to deregulate the cryptocurrency and fintech industries and move away from the CFPB’s attempts to protect customers.

This sounds true, so itThis resonated with many on the left who were unwilling to believe that an entire industry would be unlawfully deprived of banking services. Unfortunately, this is certainly true for them. Obama did develop a strategy of using bank regulations to unconstitutionally crackdown on industries like gun manufacturing and loan sharking. Biden has once again refined these strategies and used them very effectively in the cryptocurrency space. They are now going after fintech companies by harassing partner banks. These things did happen, and in both cases they were widespread (and unconstitutional) overuses of executive power that will now be exposed and reversed under Trump.

Whether or not writers like Fang believe that Biden’s strategy of debanking crypto companies mitigates his own moral views on groups sympathetic to debanking, that’s It's all irrelevant. It happened, it was debanking, and it was illegal. Whether Mark has some financial motive for criticizing the CFPB is not that important. (I checked and the CFPB has not taken any enforcement action against a16z’s investment companies to date). Bank regulators (Mark did mention multiple agencies, not just the CFPB) do use a highly regulated financial system to achieve their ends. It doesn’t matter whether the motivations of the messenger are pure or not. The key is whether federal agencies dangerously abuse executive power and go far beyond their authority to harass legitimate industries. In fact, they did.

Ruling on Anderson's Charge

So, based on a thorough analysis, let's evaluate Mark Remarks at Rogan Conference:

Debanking means being debanked as a person or company, either because your industry is not favored by the government , or because you hold a different political opinion

In my opinion, this is an accurate description. Being "debanked" does not differ based on whether the victim is sympathetic to you.

The CFPB bears at least some responsibility, as do various other unnamed federal agencies

The CFPB does habitually harass fintech companies and banks, and it probably doesn’t need to exist. But based on what we know about Operation Stifle 2.0, they don't bear primary responsibility. More directly involved are the FDIC (Federal Deposit Insurance Corporation), OCC (Office of the Comptroller of the Currency), and the Federal Reserve, with Biden's coordination. Contrary to what critics say, CFBP is not a real mitigationsolution forces, as they have so far not brought any cases against “de-banking”, although there has been some noise about it recently.

De-banking works by having regulators outsource financial repression to banks so they are not directly responsible

This is an accurate description. Just like using big tech companies to censor dissidents, using banks or fintech platforms to kick out tech founders is an effective way to financially silence a regime's enemies without subjecting them to too much scrutiny. .

The main victims of debanking during the Obama administration were legal but unpopular industries — marijuana companies, adult shops, gun shops and gun manufacturing Commerce

This is an accurate description of how Operation Stifle, the official Obama-era Justice Department program, works. It actually started with loan sharking, but Mark doesn't mention that.

Cryptocurrency companies and entrepreneurs, as well as fintech companies, are the main victims of bank decentralization during the Biden administration. Conservatives are sometimes debanked for their views

These claims are all true, although we have more evidence of a coordinated crackdown on cryptocurrencies than The anti-fintech movement is even greater (although we know the FDIC is holding fintech companies accountable through enforcement actions against partner banks). Regarding the de-banking of conservatives, we have plenty of anecdotal evidence that this is happening, but there is currently no evidence that banks have active internal banks. This appears to be done on a case-by-case basis, with "reputational risk" as the reason. The bottom line is that banks are completely opaque and they are not required to provide justification for their de-risking decisions.

30 tech founders in a16z’s portfolio have been debanked

Yes Possible, and very likely. a16z is a very active cryptocurrency investor, and almost every local cryptocurrency startup has faced banking issues at some point.

Where did Marc make a mistake?

What is Mark's mistake?

He somewhat exaggerated the role of the CFPB, as their sister regulators, the FDIC, OCC, and the Federal Reserve, bear greater responsibility for the recent series of crackdowns on cryptocurrency and fintech companies. However, he did note that others The unnamed "agency" was behind debanking (although he didn't mention the FDIC, OCC, or Federal Reserve). Additionally, in the case of the CFPB, Elizabeth Warren was the founder of the agency and she was most responsible for killing the action. people (especially in Biden (Bharat Ramamurthy, her appointee to the National Economic Council), so I can understand Mark giving the CFPB disproportionate responsibility. style="text-align: left;">His discussion of sensitive persons (PEPs) is somewhat simplistic. Doesn't result in automatic loss of banking services, but generally makes you subject to more due diligence Mark is probably referring to the Nigel Farage/Coutts/Natwest incident, which was indeed the case when Nigel was considered a PEP. A factor in his being debanked by Coutts

Overall, Mark is right and the critics are wrong. The CFPB has yet to become any strong anti-debanking force. Debanking is real and it clearly applies to crypto and fintech area, more evidence will come to light as Republicans take control and the investigation unfolds.