7 mins ago

8,880

Core points

The twists and turns and impact of Trump’s election as Treasury Secretary. Trump has gone through a lot of speculation and weighing on the choice of Treasury Secretary. On November 19, Trump nominated Howard Lutnick as Secretary of Commerce. On November 22, Trump nominated Scott Bessant as Secretary of the Treasury. Trump’s appointments as Minister of Finance and Minister of Commerce correspond to a combination of “radical trade + moderate finance”. On trade, Lutnick, as a trade hawk, may promote a tougher trade protectionist stance. In terms of finance, although Bessant supports Trump's "reducing regulations and tax cuts", he also attaches importance to controlling inflation and balancing the deficit. Bessant proposed an economic proposal known as the "333 Plan", which is to reduce the budget deficit to 3% of GDP by 2028, achieve 3% GDP growth through deregulation, and increase oil production by 3 million barrels per day or the equivalent. energy. In the short term, investors' attention may shift from trade protection risks to a more sustainable U.S. economic and debt outlook, and both U.S. stocks and U.S. bonds are expected to receive a boost.

Overseas economy. 1) United States: New housing starts and building permits in the United States in October were lower than expected; the NAHB housing market index rose in November. The U.S. Markit manufacturing and services PMIs both rose in November. The final reading of U.S. consumer sentiment in Michigan for November was unexpectedly revised downward. The latest number of initial jobless claims in the United States fell, but the number of continuing claims hit a new high in nearly a year. Market expectations for interest rate cuts have been thwarted again. CME data shows that as of November 22, the market expected a 52.7% probability of a 25BP interest rate cut in December, down from 61.9% the previous week. 2) Europe: ECB officials said that they will almost certainly cut interest rates by 25 basis points in December; the final HICP value of the Eurozone in October rose by 2% year-on-year, while the manufacturing and service industries in November were weaker than expected and in the contraction range. UK CPI in October was higher than expected year-on-year, while both manufacturing and services PMI were weaker than expected. 3) Japan: Japanese Prime Minister Shigeru Ishiba launched a 21.9 trillion yen economic stimulus plan, which is expected to boost GDP growth by 1.2 percentage points; Bank of Japan Governor Kazuo Ueda’s speech was hawkish, and Japan’s core CPI was 2.3% year-on-year, higher than expected. Pay attention to the possibility of Japan raising interest rates in December.

Global major asset classes. 1) Stock markets: U.S. and European stock markets are recovering, while some Asian stock markets continue to be under pressure. The S&P 500, Dow Jones Industrial Average and Nasdaq Composite Index rose 1.7%, 2.0% and 1.7% respectively for the week. The Philadelphia Semiconductor Index rose 2.5% for the week; the Russell 2000 Index rose 4.5%. The European STOXX600 index rose 1.1% for the week, and the Nikkei 225 index fell 0.9%. 2) Bond market: U.S. bond interest rates with maturities of 3 years and belowInterest rates on U.S. Treasury bonds with maturities of five years and above stabilized or fell slightly. The 10-year U.S. Treasury yield fell 2 BP throughout the week to 4.42%. Total foreign holdings of U.S. Treasury securities rose for the fifth straight month. 3) Commodities: Oil prices and gold prices rebounded sharply, while copper prices stopped falling. Brent and WTI crude oil rose 5.8% and 6.3% respectively throughout the week, closing at US$75.2 and US$71.2/barrel respectively. Gold spot prices rose 4.8% throughout the week, rising back to around the $2,700/ounce mark. The escalation of the conflict between Russia and Ukraine, coupled with Trump's appointment of hawkish official Lutnick as Commerce Secretary, triggered an increase in demand for safe havens; the slight decline in the real interest rate on the 10-year U.S. Treasury bond also helped release the potential for rising gold prices. 4) Foreign exchange: The U.S. dollar index rose 0.76% for the whole week, closing at 107.49, and exceeded the high in October 2023, setting a new high since November 2022. The euro and pound depreciated significantly, and the yen showed some resilience.

Risk warning: U.S. inflation has risen beyond expectations, global financial markets have been more volatile than expected, and international geopolitical situations have exceeded expectations.

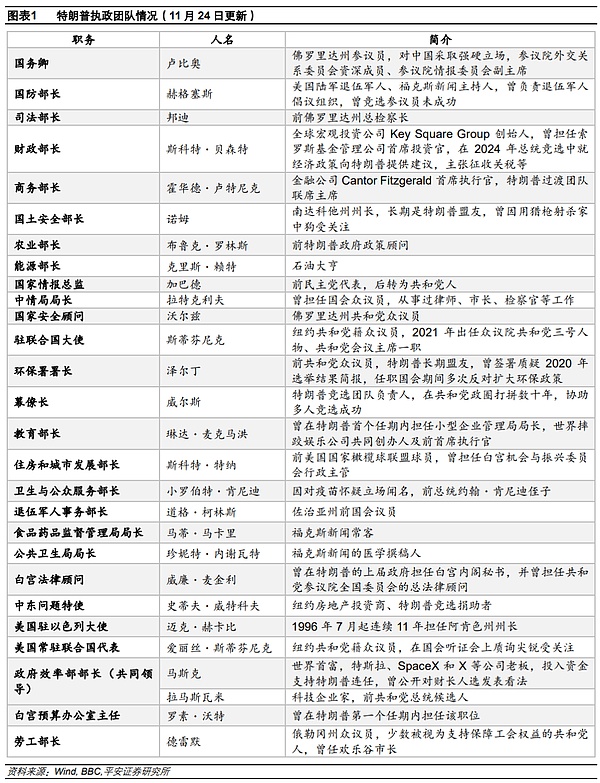

01 The twists and turns and impact of Trump’s election as Treasury Secretary

In the past week, the market has paid close attention to the appointments of the U.S. Secretary of the Treasury and the Secretary of Commerce. Trump has experienced many speculations and trade-offs on the selection of the Secretary of the Treasury. Initially, Howard Lutnick, CEO of Cantor Fitzgerald, Scott Bessant, founder of global macro investment firm Key Square Group, and Lighthizer, Trump’s first-term trade representative, all On the short list for finance minister. On November 16, Musk publicly expressed his support for Howard Lutnick as Secretary of the Treasury. This behavior was interpreted as "public pressure on Trump" and caused dissatisfaction with the Trump transition team. According to a report by the New York Times on November 17, Trump is reconsidering candidates for U.S. Treasury Secretary after he takes office, including former Federal Reserve Governor Kevin Warsh and Wall Street billionaire Mark Rowan. On November 19, Trump announced his nomination of Lutnick as U.S. Secretary of Commerce. On November 21, the Wall Street Journal quoted people familiar with the matter as saying that Trump has proposed to choose Kevin Warsh as Treasury Secretary, and revealed that Warsh may be nominated after the current Federal Reserve Chairman Powell ends his term in 2026. Takes over as chairman of the Federal Reserve. Finally, on November 22, Trump nominated Scott Bessant as Treasury Secretary.

On November 19, Trump nominated Howard Lutnick as Secretary of Commerce. Lutnick is a long-time friend of Trump and a clear supporter of Trump's relationshipTariffs, which is in line with Trump’s philosophy of using tariffs as an important economic tool. He has worked for the financial services company Jianda Company since 1983 and rose to the position of CEO. He has strong control and operational experience in the business field. Trump said in a statement that Lutnick would "lead our tariff and trade agenda and be directly responsible for the Office of the United States Trade Representative." It is worth mentioning that Lighthizer, the top US foreign trade official who has been hotly discussed by the outside world, has not been appointed. The possible reason is that in addition to being consistent with Trump on tariffs, Lutnick also served as a co-director of the Trump transition team, participated in the selection and review of cabinet candidates, and was deeply integrated into Trump in terms of personnel operations. camp, in contrast, Lighthizer may not be as good as Trump in terms of overall role fit.

On November 22, Trump nominated Scott Bessant as Secretary of the Treasury. Bessant, 62, is the founder of global macro investment firm Key Square Group and served as chief investment officer of Soros Fund Management. He advised Trump on the economy during the presidential campaign. Trump said Bessant has long been a staunch advocate of "America First" and will help him usher in a new golden era for the United States. Bessant's appointment may be due to his high degree of agreement with Trump in terms of economic philosophy. His experience in the investment field can provide a unique perspective on U.S. economic development, and he has shown loyalty and support for Trump during the election campaign. , although they support tariffs, they advocate a gradual and relatively balanced approach. In addition, Bessant has long been a strong critic of the Federal Reserve. He once advocated the appointment of a "shadow Fed Chairman" and the latest suggestion is that the Fed should "nominate the next Fed Chairman as soon as possible."

Trump’s appointments as Finance Minister and Commerce Minister correspond to the combination of “radical trade + moderate finance”. In terms of trade, Lutnick, as a trade hawk, may naturally help Trump adopt a tougher trade protectionist stance. Lutnick holds a radical concept of tariffs. He believes that tariffs are an effective tool to protect the interests of American workers, and even advocates that the United States "should return to 125 years ago", that is, the era of only tariffs and no income tax. In terms of finance, although Bessant supports Trump's "reducing regulations and tax cuts", he also attaches importance to controlling inflation and balancing the deficit. Bessant proposed an economic proposal known as the "333 Plan", which is to reduce the budget deficit to 3% of GDP by 2028, achieve 3% GDP growth through deregulation, and increase oil production by 3 million barrels per day or the equivalent. energy. He sees room for further reductions in the federal budget deficit, which averaged 4% of GDP during Trump's first term.

In the short term, investor attention may shift from trade protection risks to a more sustainable U.S. economy and debtU.S. stocks and U.S. bonds are expected to be boosted by the U.S. financial outlook. After Lutnick was elected as Secretary of Commerce on November 19, European stock markets fell collectively, the Nasdaq Golden Dragon Index plunged during the session, and the prices of gold and Bitcoin rose, reflecting the market's fear of U.S. trade risks and risk aversion. of heating. On the other hand, Bessant is called "one of the smartest people on Wall Street" by Trump and is also regarded by the market as a "safety solution" and "an adult in the room." After he is nominated as Treasury Secretary, the market may The outlook for the U.S. economy and debt is expected to be more robust and predictable, which may boost the performance of both U.S. stocks and U.S. bonds in the short term.

02 Overseas Economy

2.1 United States: Expectations for interest rate cuts have been frustrated again

U.S. housing starts and construction permits in October were lower than expected; NAHB in November Housing market index rose. The annualized total number of new housing starts in the United States in October was 1.311 million units, compared with the expected 1.33 million units. The previous value was revised from 1.354 million units to 1.353 million units. The initial annualized total number of construction permits in October was 1.416 million households, compared with the expected 1.43 million households, and the final value in September was 1.425 million households. The NAHB housing market index in the United States rose 3 points to 46 in November, reaching the highest point since April this year, benefiting from rising sales expectations and optimism that Trump will reduce regulatory burdens.

US Markit manufacturing and service PMIs both rose in November. The initial value of the S&P Global (Markit) manufacturing PMI in the United States in November was 48.8, a four-month high, in line with expectations, and the previous value was 48.5; the initial service PMI value was 57, a 32-month high, and the expected 55.2, the previous value was 55; comprehensive The initial PMI value was 55.3, a 31-month high, compared with the expected 54.3 and the previous value of 54.1.

The final value of U.S. consumer confidence in Michigan in November was unexpectedly revised downward. The final value of the University of Michigan Consumer Confidence Index in the United States in November was 71.8, which was expected to be 73.7. The initial value was 73, and the final value in October was 70.5. The one-year inflation rate is expected to have a final value of 2.6%, an expected value of 2.7%, an initial value of 2.6%, and a final value of 2.7% in October.

The latest number of initial jobless claims in the United States fell, but the number of continuing claims hit nearly One-year high.In the week ending November 16, the number of initial claims for unemployment benefits in the United States fell by 6,000 to 213,000, the lowest level since April. Market expectations were for an increase to 220,000. In the week ending November 9, the number of people continuing to apply for unemployment benefits increased by 36,000 to 1.908 million, exceeding the high in February this year and setting a new high since November 2023.

Market expectations of interest rate cuts have been frustrated again. CME data shows that as of November 22, the market expects the probability of a 25BP interest rate cut in December to be 52.7%, lower than the previous week's 61.9%; the weighted average expectation of interest rates at the end of 2025 is 3.84%, higher than the previous week's 3.75%.

2.2 Europe: There is no problem with the European Central Bank cutting interest rates

ECB officials said that they will almost certainly cut interest rates by 25 basis points in December; the final HICP value of the Eurozone in October rose by 2% year-on-year, while the manufacturing and service industries in November were weaker than expected and at shrinkage range. European Central Bank Governing Council member Stunaras believes that the European Central Bank will almost certainly cut interest rates by 25 basis points in December. He stressed that tariffs could have a negative impact on Europe and could trigger a recession in the medium term. ECB Vice President Guindos said that inflation will fall back to the target level next year; risks to the economic outlook have increased and are biased to the downside; it is "very clear" that interest rates will be cut further, but due to rising trade tensions and global conflicts Officials should not act hastily due to uncertainties. The European Central Bank released a "Financial Stability Report" stating that although the debt-to-GDP ratio of most euro zones has declined, some sovereign debt burdens are still heavy and there are high risks to sustainability. European Central Bank President Christine Lagarde said the European Central Bank needs to pay more attention to financial stability and long-term economic growth in Europe. The final HICP value in the Eurozone rose by 2% year-on-year in October, in line with market expectations and returning to the European Central Bank's target level, paving the way for an interest rate cut in December. The initial value of the manufacturing PMI in the Eurozone in November was 45.2, which was expected to be 46, and the final value in October was 46; the initial value of the service PMI was 49.2, which was expected to be 51.6, and the final value in October was 51.6; the initial value of the comprehensive PMI was 48.1, a ten-month low, and the final value in October was 50. , with a final value of 50 in October.

UK's October CPI was higher than expected year-on-year, while the manufacturing and service PMIs were both weaker than expected. The British CPI rose by 2.3% year-on-year in October, a significant increase from the previous value of 1.7%, and higher than market expectations of 2.2%. The core CPI in October rose to 3.3% year-on-year from 3.2% in September, and the service CPI rose from 4.9% to 5% year-on-year. A higher-than-expected rise in inflation weighs on traders' expectations for the Bank of England's futureBets on rate cuts in a few months. The initial value of the UK manufacturing PMI in November was 48.6, 50 expected, and the final value in October was 49.9; the initial service PMI value in November was 50, 52 expected, and the final value in October was 52; the comprehensive PMI initial value in November was 49.9, 51.8 expected, and the final value in October The final value is 51.8.

2.3 Japan: Shigeru Ishiba announces economic stimulus plan

Japanese Prime Minister Shigeru Ishiba launched a 21.9 trillion yen economic stimulus plan, which is expected to boost GDP growth by 1.2 percentage points; Bank of Japan Governor Kazuo Ueda’s speech was hawkish, and Japan’s core CPI was 2.3% year-on-year, higher than expected. Pay attention to the possibility of Japan raising interest rates in December. Japanese Prime Minister Shigeru Ishiba launched a 21.9 trillion yen (approximately US$140 billion) economic stimulus plan, which includes subsidies for low-income families, stimulating investment in semiconductors and artificial intelligence, and restarting electricity and gas subsidies to solve the problem. Inflation, wage growth and a series of challenges. Including private funds, the total economic stimulus package is 39 trillion yen. According to estimates by the Japanese Cabinet Office, these measures will boost GDP growth by 1.2 percentage points. Bank of Japan Governor Kazuo Ueda said Japan's economy is heading towards sustained wage-driven inflation and warned against keeping borrowing costs too low; the central bank will carefully review various data before next month's interest rate review and will "seriously "Consider the impact of yen exchange rate fluctuations on the economic and price outlook. Japan's October core CPI rose 2.3% year-on-year, expected to rise 2.2%, the previous value rose 2.4%; October CPI rose 2.3% year-on-year, expected to rise 2.3%, the previous value rose 2.5%; month-on-month rose 0.6%, the previous value fell 0.3% . Japan's November service PMI initial value was 50.2, the previous value was 49.7; the manufacturing PMI initial value was 49, the previous value was 49.2; the comprehensive PMI initial value was 49.8, the previous value was 49.6.

03 Global Major Assets

3.1 Stock Market: U.S. and European stock markets are picking up

In the past week (as of November 22), U.S. and European stock markets have recovered, while some Asian stock markets continue to be under pressure. In the United States, the S&P 500 Index, Dow Jones Industrial Index and Nasdaq Composite Index rose 1.7%, 2.0% and 1.7% respectively for the whole week. At the macro level, the disturbance caused by the appointment of Trump's new team has weakened, mid- and long-term U.S. bond interest rates have stabilized, and market risk appetite has recovered. At the industry level, among the 11 industries in the S&P 500 Index, daily consumption, materials, real estate and utilities performed better, while communication services, information technology, consumer discretionary and medical care performed better.Health care and other performance lagged behind. The Philadelphia Semiconductor Index rose 2.5% for the week; the Nasdaq Golden Dragon Index was flat; the Russell 2000 Index rose 4.5%. In Europe, the European STOXX600 index rose 1.1% for the whole week, and the German DAX, French CAC40 and British FT100 indexes rose 0.6%, fell 0.2% and rose 2.5% respectively for the whole week. In Asia, the Nikkei 225 Index fell 0.9%, while the South Korea Composite Index rose 3.5%. Hong Kong stocks and A-shares continued to be under pressure.

3.2 Bond market: Mid- and long-term U.S. bond interest rates stabilize

In the past week (as of November 22), interest rates on U.S. bonds with maturities of three years and below have increased, while interest rates on U.S. bonds with maturities of five years and above have stabilized or fallen slightly. The market further evaluated the prospect of a rate cut in December, causing short-term U.S. bond rates to rise, but the uncertain economic outlook did not continue to drive upwards in mid- and long-term U.S. bond rates. The 2-year U.S. Treasury bond rate rose 6BP for the whole week to 4.37%. The 10-year U.S. Treasury yield fell 2 BP for the whole week to 4.42%, breaking away from the highest level since July; the 10-year TIPS interest rate (real interest rate) fell 3 BP for the whole week to 2.07%, and the implied inflation expectation rose 1 BP for the whole week to 2.34%. The latest data released by the U.S. Treasury Department showed that the total amount of U.S. Treasury debt held by foreign countries rose to $8.6729 trillion in September from $8.5034 trillion in August. This is the highest level on record and the fifth consecutive month of increase. . However, Japan continues to reduce its holdings of U.S. debt. In the non-U.S. region, the 10-year German government bond yield fell 1 BP to 2.32% throughout the week.

3.3 Commodities: Oil and gold surge

In the past week (as of November 22), oil prices and gold prices rebounded sharply, while copper prices stopped falling. In terms of crude oil, Brent and WTI crude oil rose 5.8% and 6.3% respectively throughout the week, closing at US$75.2 and US$71.2/barrel respectively. At the macro level, tensions between Russia and Ukraine have escalated rapidly, with the two countries launching missiles at each other. The market is worried that the expansion of the conflict may affect crude oil supply, triggering a rise in oil prices. In terms of inventories, in the week ending November 15, U.S. EIA crude oil inventories increased by 545,000 barrels, which is expected to increase by 138,000 barrels, and the previous value increased by 2.089 million barrels. In terms of precious metals, the spot price of gold rose 4.8% throughout the week, rising back to around the $2,700/ounce mark. Silver spot prices rose 1.9% for the week. The escalation of the conflict between Russia and Ukraine, coupled with Trump's appointment of hawkish official Lutnick as Commerce Secretary, triggered a rise in demand for safe havens; the actual interest rate of 10-year U.S. Treasury bondsThe slight drop in the rate also helped release the potential for gold prices to rise. In terms of metals, LME copper and aluminum were flat and fell 1.0% respectively throughout the week. In terms of agricultural products, CBOT soybeans, corn and wheat fell by 1.4%, rose by 0.5% and rose by 1.2% respectively.

3.4 Foreign Exchange: The U.S. Dollar Index rose above 107

In the past week (as of November 22), the U.S. dollar index rose 0.76% for the whole week, closing at 107.49, and exceeded the high in October 2023, setting a new high since November 2022. The euro and pound depreciated significantly, and the yen showed some resilience. In the United States, the appointment of hawkish officials in the United States has further raised expectations for U.S. interest rates, while the prospect of interest rate cuts in Europe has become more certain, further boosting the dollar. In the Eurozone, the latest inflation data in the Eurozone were in line with expectations, the PMI was weak, and an interest rate cut in December is more certain. The euro fell 1.18% against the dollar for the week, the largest depreciation among major currencies. In the UK, British inflation and PMI data were both stronger than those in the euro zone, and the pound fell even more. GBP/USD fell 0.69% for the week. In Japan, the Bank of Japan's stance was hawkish, inflation data was strong, and investors focused on the possibility of raising interest rates in December, which limited the decline of the yen. The yen fell 0.25% against the US dollar for the week, with USD/JPY closing at 154.77. On the other hand, the RMB fell 0.20% against the US dollar for the whole week, with the US dollar closing at 7.2452 against the RMB.

Risk warning: U.S. inflation rises more than expected, and global financial markets fluctuate beyond expectations As expected, the international geopolitical situation exceeded expectations, etc.