55 mins ago

2,486

Author: Guosheng Communication Team

AbstractStanding at the current point in time, we re-evaluate the development trend and development trend of AGI investor expectations. The market starts with computing power, extends to GPU, optical modules, switches, storage and other tracks, and leverages overseas mapping to eagerly look forward to AI applications, but ignores the pull on upstream infrastructure when computing power increases. If applications are the most explosive direction, then the infrastructure will take a long time to develop. Not only liquid cooling, but also the demand for energy is fundamental. This is also the starting point of this article.

Marginal changes: One of the biggest differences between AIDC and traditional data centers is that the level of electricity consumption has increased significantly. AIDC has the characteristics of large data volume, complex algorithms and 24/7 instant response, so compared with traditional data centers, AIDC consumes a lot of power. With the rapid development of AI, it is expected that AI software integrating large language models will develop rapidly, and training needs and inference needs will resonate. In the future, the power consumption of data centers will increase significantly. AIDC will become a new generation of "electric tigers", and data center consumption will The proportion of electricity will further increase. SemiAnalysis predicts that global data center critical IT power demand will surge from 49GW in 2023 to 96GW in 2026, of which AI will consume approximately 40GW. Vertiv predicts that data center power consumption will increase by 100GW over the next five years, with global data center power demand rising to 140GW by 2029.

Dilemma: The U.S. power grid is unable to support the development of AI computing power. Compared with the construction speed of data centers, the current construction speed of the U.S. power grid is relatively slow and the power generation capacity is limited. Therefore, in the short term, the United States will face a power demand dilemma due to the development of AI. Currently, U.S. power supply faces obstacles such as long infrastructure construction cycles, shortage of infrastructure facilities, labor shortages, lack of experience among practitioners, and the need to coordinate multiple stakeholders when building a power grid. The rapid development of AI has caused power supply shortages in some areas. North American utility Dominion Energy said it may not be able to meet the power demand in Virginia, leading to multi-year delays in the construction of the world's fastest-growing data center hub.

Solutions: short term - natural gas, medium term - SMR nuclear power, long term - controlled nuclear fusion. The rise of AI is leading resource competition to computing power + energy. In the AI-driven digital world, computing power is the basis for iteration and innovation, and energy is the key to supporting the operation of these computing powers.key. In the short term, natural gas combined with fuel cells will provide flexible and efficient power generation solutions for data centers to meet the current rapid expansion needs. In the medium term, small modular reactors (SMRs) will become a key path to address power bottlenecks in data centers due to their stability and adaptability to distributed deployment. In the long term, controllable nuclear fusion is expected to completely break through energy supply constraints and provide unlimited and clean power support for the future computing power ecosystem. In this process, from the continuous innovation of energy technology to the efficient collaboration of computing power ecology, it not only promotes the leap of AI technology, but also reshapes the future pattern of deep integration of energy and computing.

We believe that we are still in a battle for computing power, but looking forward to the next five years, the battle for energy infrastructure may become mainstream. In the short term, the capital expenditures of CSP giants in the third quarter of this year have all reached new highs, and they tend to be on the computing power side. In the next 5-10 years, combined with the continued increase in investment in AI computing power and the current power supply situation in the United States, we believe that the current power supply in the United States will be flat. The era of 2020 is coming to an end, and the battle for computing power will gradually transform into a battle for energy. The investment plans of computing giants such as Amazon, Microsoft, and Google in nuclear power projects such as SMR have initially proved this. The addition of IT giants will significantly introduce new technologies and accelerate iteration, and investment opportunities in related energy infrastructure will gradually emerge.

Investment advice: To sum up, energy is the next battle in technological competition. Just like the process of liquid cooling from optional to mandatory, AI upstream The infrastructure track is also moving from traditional industries to core technology supporting facilities, and seizing the opportunity for layout is the key to winning in the future. It is recommended to pay attention to the core targets of U.S. stocks such as ETN, EMR, SMR, OKLO, NNE, BE, etc. For A-shares in the nuclear power, natural gas and infrastructure supply chains, it is recommended to pay attention to Guangdong Nuclear Power, Nuclear Power, New Natural Gas, CGN Mining, Jinpan Technology, Invic, and Mai Gemet, Nengke Technology, Kehua Data, Euroland, One Stone, etc.

Risk reminder: Technical and regulatory risks, high capital requirements and financing pressure, market demand and competition risks

Investment RequirementsOpenAI founder Sam Altman once said in an interview: The two important resources in the future will be computing power and energy. AI's pursuit of performance has gradually become more intense in the field of computing power, and the core factors of competition in the next stage will initially appear in energy infrastructure.

[From computing power to energy: the next battle in technological competition]

PeopleThe rise of artificial intelligence has more directly led resource competition to computing power and energy. In the AI-driven digital world, computing power is the basis for iteration and innovation, and energy is the key to supporting the operation of these computing power. "The two most important resources in the future are computing power and energy." This trend will run through every stage of AI technology development, from algorithm optimization to hardware breakthroughs to the current demand for efficient energy systems.

[Acceleration requirements for computing power and hardware limits]

The demand for AI computing power is Exponential growth. Taking the NVIDIA H100 GPU as an example, the computing power of 60 TFLOPS is promoting large-scale training of large models, and the surge in computing power has brought huge energy consumption challenges. Vertiv predicts that total installed power demand for global data centers is expected to soar from 40GW to 140GW by 2029, while the value of data centers per MW will increase from US$2.5-3 million to US$3-3.5 million. The power consumption of more than 1MW in a single cabinet of NVIDIA's next-generation product Rubin ultra also shows that the increase in AI computing power is exerting unprecedented pressure on power infrastructure. How fast the calculation can be done depends largely on the power.

[The emergence of energy bottlenecks and infrastructure challenges]

The expansion of data centers is exposed the vulnerability of the power supply system. Elon Musk once pointed out that the production capacity of key electrical equipment such as transformers cannot meet the current demand for AI, and this shortage of power infrastructure will further amplify the load fluctuation of the power grid, especially during the peak period of AI training. Power demand may instantly exceed the average load by several times, and peak and valley power consumption patterns pose a huge threat to the stability of the energy system. This bottleneck was not obvious in the early stages of AI development, but will become more obvious as the cluster scale expands and AI applications increase in volume. This dilemma can be seen in the implementation process of Sora.

[Energy technology innovation and computing power ecological synergy]

With the rapid growth of computing power demand In the context of the epidemic, energy bottlenecks are becoming the core obstacles limiting the development of AI. Nuclear energy, especially small modular reactors (SMRs), has gradually emerged as one of the best solutions for AIDC. Emerging nuclear energy companies represented by OKLO\Nuscale are developing microreactor technology, and cloud services such as Google and MicrosoftThe provider has launched the SMR project layout, with the goal of powering future data centers through distributed small nuclear power plants to provide continuous and stable computing power support. Solutions such as natural gas + fuel cells / clean energy / energy storage are also being actively promoted as one of the options for rapid implementation. Start-ups represented by Bloom Energy are also rapidly rising with the help of industry trends.

From an investment perspective, the market has already recognized the importance of computing power, and is eagerly looking forward to the implementation of applications, constantly looking for mapping, and ignoring The importance of AI infrastructure is not just an opportunity for liquid cooling and computer rooms. From a larger perspective, the next stage of competition is gradually gaining momentum in various energy (natural gas, nuclear power, etc.) fields.

1. “Electricity Tiger” AIDC and Weak Grid 1.1 Electricity Consumption: AIDC’s Next Short Board1.1.1 Supply and Demand of Electricity in the United States

< p style="text-align: left;">Demand side: Data centers are already "big consumers of electricity," accounting for 4% of the nation's electricity consumption. The total power of U.S. data centers in 2023 is about 19GW. Based on this estimate, the annual electricity consumption is about 166TWh (terawatt hours), accounting for 4% of the national electricity consumption.The data center consumes 166 TWh of electricity, which is more than the annual electricity consumption of New York City and equivalent to the annual electricity consumption of 15.38 million household users. In terms of regions, New York's annual electricity consumption in 2022 was 143.2TWh, Texas' annual electricity consumption was 475.4TWh, California's 251.9TWh, Florida's 248.8TWh, and Washington's 90.9TWh. The U.S. data center's annual electricity consumption exceeded New York City's annual electricity consumption. power consumption. The average annual electricity consumption per residential user in 2022 is 10,791kWh. Based on this estimate, 166TWh is equivalent to the annual electricity consumption of approximately 15.38 million household users.

*1 TWh = 1000 GWh = 10^6 MWh = 10^9KWh

p>Supply side: The annual power generation in the United States is relatively fixed, and thermal power is still the main source. New energy power generation is growing rapidly, and the proportion of nuclear energy has further increased. The annual power generation capacity in the United States is approximately 4,000-4,300 terawatt hours (TWh), of which thermal power (coal, natural gas, fossilOil) accounts for about 60% and is the main energy source; new energy power generation (wind energy, solar energy, etc.) has grown rapidly in recent years and accounts for 21%; nuclear energy accounts for about 19%, and its proportion has further increased.

Electricity prices: The United States has one of the lowest electricity prices in the world, and some states have energy advantages. There are lower electricity prices. The U.S. electricity consumption structure is mainly divided into four areas: residential, commercial, industrial and transportation. In September 2024, the electricity price for residential users is US$0.17/kWh (approximately 1.24 yuan/kWh, the exchange rate is as of December 13), and the electricity price for commercial users is US$0.135/kWh (approximately 0.98 yuan/kWh); industrial The electricity price is US$0.09/kWh, and the transportation electricity price is US$0.13/kWh. kWh, wholesale electricity prices in 2023 are $0.036/kWh. Some states have lower electricity prices due to their energy advantages. As of April 2024, the electricity price in Texas (rich in natural gas and renewable energy) is approximately US$0.147/kWh, and in Louisiana (rich in energy resources), the electricity price is approximately US$0.147/kWh. It is US$0.115/10 million hours, and Tennessee (rich in hydropower resources) is about US$0.125/kWh. Some large-scale power-consuming infrastructure, such as data centers, are often built in provinces with low electricity prices. The above-mentioned state capitals have also become the concentration of today's computing power industry.

Estimation of annual electricity cost for data centers: Based on the wholesale price of US$0.036/kWh, the U.S. data center (when AI has not yet been applied on a large scale) for one year It consumes 166TWh of electricity and is estimated to require approximately US$6 billion.

1.1.2 Marginal changes: AI’s challenge to the power grid

[Challenge 1: Total electricity consumption increases significantly]

Compared with traditional data centers, AI data centers It consumes a lot of power. The main reasons are the massive growth in data volumes, complex algorithms, and the need for instant response 24/7. For example, a Google traditional search request consumes about 0.3Wh, while a ChatGPT request consumes 2.9Wh, which is ten times the former; a paper published in "Joule" stated that if Google uses AIGC for every search, its usage Electricity will rise to29 billion KWh, which will exceed the total electricity consumption of Kenya, Croatia and many other countries; according to the New Yorker Magazine, ChatGPT consumes more than 500,000 KWh every day.

[Challenge 2: Using electricity to intensify the voltage]

Phenomena: The current demand of AI data centers (whether training or inference) is highly transient, with huge swings occurring within a few seconds. As the task load of the neural network model increases or decreases, the current demand will fluctuate wildly, even up to 2000A per microsecond.

Principle: 1) Peak load fluctuation: The training and inference of AI models require huge computing power, but they do not run continuously. Peak loads will occur when model training starts. , while basic operation is maintained during low periods, causing power consumption to fluctuate; 2) Dynamic resource scheduling: AI tasks are cyclical. For example, large-scale training requires centralized resources, while the inference phase is relatively dispersed, which makes the power consumption curve more unstable; 3) Respond to needs in real time: Generative AI and large model applications require low latency and high throughput, driving real-time expansion of infrastructure and further amplifying power consumption fluctuations.

Result: Affects the stability of the power grid. The design of the power grid is not suitable for excessive swing voltage. The power grid is basically designed for the power load. We hope to see a relatively stable, regular and slowly changing load. For example, an electrical device with a power load of 100GW may change after being connected to the power grid. There are two 200GW transmission lines for power supply, and operation can be guaranteed if one of the two transmission lines is normal. The AI power consumption characteristics will have huge swings within a few seconds, and this violent fluctuation may affect the stability of the power grid.

[Challenge 3: The subsequent demand for electricity will be greater]

Inference in the AI data center consumes more energy than training due to the large number of requests from users. Currently, Google has announced in the first half of this year that it will add new AI features to improve the search experience and will launch Gemini-based AI Overviews, which is already available for trial for some users; Microsoft has launched a personal AI assistant called Microsoft Copilot and has already ChatGPT is integrated into Bing. At present, the number of visits to Google's search engine has reached 82 billion times per month, and the number of Office business products has reached 82 billion.The number of paying users has exceeded 400 million. The huge user base means that if the trained large model is integrated into the company's products, the number of user requests will increase significantly, and the number of AI instant responses will surge, causing the model inference energy consumption to exceed the training energy consumption. U.S. data center power loads could account for 30% to 40% of all new demand until 2030, according to McKinsey estimates.

Conclusion: With the rapid development of AI, AI software that integrates large language models is expected to It will develop rapidly, and training needs and inference needs will resonate. In the future, the power consumption of data centers will increase significantly. AIDC will become a new generation of "electric tigers", and the proportion of data center power consumption will further increase.

1.2 Realistic dilemma: The power grid is difficult to supportThe economic development structure determines that the power grid infrastructure in North America is relatively weak. Over the past 20 years, the decoupling of U.S. electricity demand from economic growth has accelerated dramatically. Since 2010, the U.S. economy has grown by a cumulative 24%, while electricity demand has remained almost unchanged, and in 2023, U.S. electricity consumption even fell by 2% from 2022. Its essence is that it is different from the fact that the economy is mainly driven by industry and service industries. The economic growth of the United States does not mainly rely on electricity or energy consumption, but mainly relies on high-tech industries, with low energy consumption. And efficiency gains, primarily the replacement of incandescent lights with fluorescents and LEDs, have offset demand for electricity from population and economic growth, leaving utilities and regulators without expanding grids or generating capacity.

Current situation: lack of time, lack of people, lack of infrastructure, lack of experience, and many obstacles.

Lack of time: It takes about two years to build a data center, but construction of the power grid is much slower, and it may take three to five years to build a power station , and it will take 8 or even 10 years to build a long-distance, high-capacity transmission line. According to MISO, the U.S. regional transmission organization, the 18 new transmission projects it is planning could take seven to nine years, compared with 10 to 12 years for similar projects historically. It can be deduced from this that the construction speed of the power grid is likely to be unable to catch up with the growth rate of AI.

Lack of infrastructure: According to the power investment trend in the United States, capital expenditures of U.S. utilities will increase significantly from 2016 to 2023, especially for power generation, distribution and Transmission field, grid investmentThe acceleration started in 2018, mainly due to the reshoring of manufacturing industry to promote power demand. Against this background, the United States still has not expanded the power grid on a large scale. According to a survey report issued by Grid Strategy, from 2010 to 2014, the United States installed an average of 1,700 miles of power grids per year. of new high-voltage transmission miles, but fell to only 645 miles per year in 2015-2019.

Shortage of workers: A tight workforce is also a constraint, especially a shortage of professional electrical workers necessary to implement new grid projects. According to McKinsey estimates, the U.S. could see a shortage of 400,000 specialized workers based on projected construction of data centers and similar assets requiring similar skills.

Lack of experience: For the United States, practitioners in the entire power industry have not seen large-scale growth in power demand in the past 20 years, and these 20 years Years will likely mean an entire group of engineers and staff without experience in building a new power grid on a large scale.

Many resistances: The construction of the power grid requires infrastructure such as power stations and transmission lines, and these may require the joint efforts of countless stakeholders to reach a compromise on the route of the lines and the cost. .

Conclusion: Compared with the construction speed of data centers, the current speed of power grid construction in the United States is relatively slow. It is slow and has limited power generation capacity, so in the short term the United States will face a power demand dilemma under the development of AI. North American utility Dominion Energy, for example, said it may not be able to meet Virginia's power demand, delaying construction of one of the world's fastest-growing data center hubs for years. And in the power industry, new infrastructure planning takes five to 10 years, according to Wood Mackenzie. Additionally, most state public utility commissions have little regulatory experience in a growth environment. It can be inferred that electric energy may become one of the biggest constraints on the development of AI in the next few years. Although the market is paying attention to innovative solutions such as controllable nuclear fusion, water from afar cannot quench the thirst for nearness, and it is inevitable to form short-, medium-, and long-term comprehensive solutions.

1.3 Multi-angle calculation: How much power does AIDC consume?* Total power (GWh) = Total power (GW) × Time (h)

* Total power (GW)=IT equipment power (GW)×PUE (energy efficiency ratio)

1.3.1 Calculation angle one (conservative): AI chips

Calculation logic: Calculation angle one is from the number of chips From this perspective, extrapolate to 2030, and then use the number of chips * chip power consumption to predict the total power consumption, without considering that the overall power consumption of the server will be greater than that of a single chip * The quantity does not take into account the possible increase in single-chip power consumption after future chip upgrade iterations. Therefore, we believe that the calculation angle 1 is a "conservative" calculation. The calculation data is the smaller of several methods. The AIDC power demand in 2030 is 57GW.

Number of GPUs and TPUs in use: According to DCD reports, the total shipments of GPUs in the three enterprise data centers of Nvidia, AMD and Intel in 2023 are estimated to be 3.85 million units , the number of TPUs produced for Google in 2023 is expected to be 930,000. Further tracing the supply chain, TSMC predicts that the year-on-year growth rate of demand for AI server manufacturing from 2024 to 2029 will be approximately 50%. Based on this calculation, GPU shipments in 2030 will be approximately 65.78 million, and TPU shipments will be approximately 15.89 million. According to NVIDIA's official statement, the average service life of most H100 and A100 is 5 years. Therefore, we assume that the number of chips in use in 2030 is the sum of chip shipments in 26-30 years. Therefore, the number of GPUs and TPUs in use in 2030 is approximately were 171.36 million and 41.39 million.

GPU, TPU power consumption: The maximum power of H100 NVL can reach 800W. Then there are expected to be 171.36 million GPUs in 2030. Assume that GPU and TPU energy consumption account for 90% of the total energy consumption of IT equipment. Assume that the United States accounts for 34%, the utilization rate is 80%, and the PUE is 1.3. Calculate, in 2030, the US AIDC GPU power demand is approximately 54GW (Number of GPUs*GPU power consumption*U.S. share*PUE* Utilization rate ÷ chip ratio = 171.36 million * 0.8kW * 34% * 1.3 * 80% ÷ 90% = 54GW);

According to Google’s official statement , the average power of TPU v4 chips is 200W. Combined with the above estimate that the number of TPUs in use in 2030 is about 41.39 million, we predict that the number of TPUs in use in 2030 Total power consumption is approximately 3.3GW (other metrics are assumed to be the same as for the GPU).

Angle 1 Conclusion: The total AIDC electricity consumption in the United States in 2030 is 57GW. The chip inventory in 23-26 years only takes into account the chip shipments after 23 years. Other calculation methods are the same as the above methods. , the calculation method is the same as above from 27 to 30 years. Finally, adding up the power consumption of GPU and TPU, we can get that the power capacity required by the US AIDC will reach 24 to 30 years respectively. 3/6/10/17/25/38/57GW.

Hypothesis 1: The chip growth rate is 50% per year (refer to TSMC's statement)

Assumption 2: Assume that the average chip life is 5 years (refer to the GPU life given by NVIDIA).

Assumption 3: The average power utilization rate of IT equipment is 90% (considering the power consumption of NVSwitches, NVLink, NIC, retimers, network transceivers, etc. in IT equipment, assuming that GPU and TPU energy consumption account for 90%, and others IT equipment energy consumption accounts for 10%).

Assumption 4: Considering that IT cannot be operated at full capacity and cannot be operated 24 hours a day, refer to Semi analysis, set the possible utilization rate to 80%

Assumption 5: PUE is 1.3 (PUE is the total power consumption of the data center divided by the power used by IT equipment). .

Hypothesis 6: The United States’ computing power demand accounts for 34% of the world’s computing power demand (according to the calculation of the Institute of Information and Communications Technology, the United States’ share of global computing power is 34%. ).

1.3.2 Calculation angle two (optimistic): data center

Calculation logic: The second calculation angle is from the data center From a construction perspective, refer to the global data center construction progress predicted by a third party (compound growth rate of 25%). At the same time, since the forecast data ends in 2026, we assume that it will still maintain 25% from 2027 to 2030. The compound growth rate of global data center power demand is predicted, and the power consumption and proportion of AIDC are assumed. Therefore, we believe that the data obtained from this forecast perspective is relatively "optimistic", and the final forecast is that by 2030, the United States willAIDC power demand tops out at 91GW.

Research firm SemiAnalysis used analysis and construction forecasts of more than 5,000 data centers and combined these data with global data and satellite image analysis to predict the next few years. Annual data center power capacity growth will accelerate to a compound annual growth rate of 25%, and the proportion of AIDC will further increase. In terms of data centers, according to forecast data, global data center critical IT power demand will surge from 49GW in 2023 to 26 years. of 96GW. We assume that data centers will continue to maintain a compound growth rate of 25% from 27 to 30 (refer to the growth rate from 2023 to 2026, which is 25%). Then, by 29 and 30, the key IT power demand of global data centers will increase to 188 and 188 GW respectively. 234GW; referring to Semi Analysis data, combined with the booming development of AI computing power and the explosion of downstream applications, we believe that the future of AI The proportion in data centers is expected to continue to accelerate, so we assume that the global AIDC proportion will reach 12%/16%/30%/44%/56%/68%/78%/88% respectively in 23-30, so as to calculate In 2029 and 2030, the global power demand for AIDC IT equipment was 65GW and 91GW respectively.

Conclusion from perspective two: Calculated based on the US share of 34% and PUE of 1.3, US AIDC power demand will reach 91GW by 2030.

Hypothesis 1: Combined with the background of the booming development of AI computing power and the explosion of downstream applications, we believe that the proportion of AI in data centers is expected to continue to accelerate in the future. Therefore, we assume that the proportion of global AIDC in 23-30 will reach 12%/16%/30%/44%/56%/68%/78%/88%.

Assumption 2: PUE is 1.3 (PUE is the total power consumption of the data center divided by the power used by IT equipment).

Hypothesis 3: The United States’ computing power demand accounts for 34% of the world’s computing power demand (as measured by the Institute of Information and Communications Technology, the United States’ share of global computing power is 34%) .

1.3.3 Summary 1: AIDC’s proportion of total U.S. electricity consumption has increased

(1) AI’s proportion of U.S. electricity consumption has increased. The proportion is expected to exceed 10%

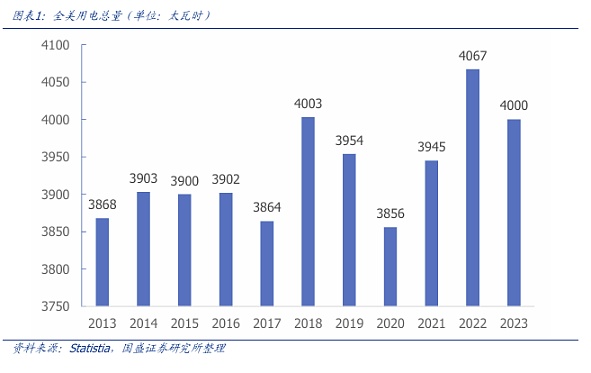

According to Statista forecast data, in 2022, the electricity consumption in the United States will be approximately 4,085 terawatt hours. Electricity usage will continue to rise to It will reach 4315 terawatt hours (corresponding to 493GW) in 2030, and will reach 5178 terawatt hours in 2050. According to our previous "Calculation Angle 1", if the total power consumption of AIDC in 2030 is the highest at 57GW, it will account for 50% of the US electricity consumption. The proportion will increase to 12% (57GW/493GW), a significant increase from 4% in 2023.

1.3.3 Summary 2: AIDC power consumption is expected to be comparable to Bitcoin mining< /p>

In our report "AI "The east wind has arrived, and Bitcoin mines have started their second growth curve", we have made assumptions and predictions about the electricity consumption of Bitcoin mines. In this report, we predict that Texas will have The loads of Bitcoin mines are 4.7/6.5/8.3/10.1/11.9GW respectively (assuming that the annual new load of Bitcoin mines in Texas is 1.8GW), regarding the share of Texas Bitcoin mine load in the United States, we assume that it remains unchanged at 28.5%. Therefore, according to our forecast, the annual load of Bitcoin mines in the United States is 17/23/29/36/42GW respectively.

For the convenience of comparison, we forecast the data to 2030, assuming: 1) The annual new load of the Texas Bitcoin mine is 1.8GW, 2) Assumption Texas mine share remains unchanged at 28.5% in 2029 and 2030. Therefore, it is concluded that in 2024/2025/2026/2027/2028/2029/2030, the annual power consumption of U.S. Bitcoin mining farms is 17GW/23GW/29GW/26GW/42GW/48GW/54GW respectively.

Conclusion: Under conservative forecasts, the power consumption of AIDC in the United States will surpass Bitcoin mining power demand in 2030; under optimistic forecasts, AIDC power demand in the United States will exceed Bitcoin mining in 2029.

< p style="text-align:center"> 2. What is the solution to the dilemma: "Natural gas +" is the mainstream in the short term 2.1 The fastest implementation plan in the short term is natural gas2.1.1 Substations have become traditional power bottlenecks

[Current situation of data center power supply]

Purchasing electricity and Substation: Data centers typically purchase electricity through a contract with a power company, which means that the data center's electricity supply is generated from the power station and transported to the data center through the transmission network. However, after power is transported over long distances, the voltage often needs to be adjusted through substations to ensure that the power meets the voltage needs of the data center.

Necessity of substations: Substations convert high-voltage electricity into low-voltage suitable for local use. Most power systems require voltage conversion and distribution through substations. Without a local substation, power cannot be used directly in the data center.

The construction of substations is difficult, takes a long time, and costs high: The construction of substations usually requires a large amount of capital investment, involving land, infrastructure construction, and equipment. Procurement and manpower reserves, etc. In addition, substation construction takes a long time and needs to meet strict environmental and safety standards.

Conclusion: Under the current electricity purchase method, substations have become a bottleneck restricting AIDC's power consumption. As data center power demands continue to grow, building new substations or expanding existing substations takes a long time and requires significant approval and construction time, which may not keep up with data center demand quickly.

[Natural gas does not require a substation and is the first choice for distributed power supply]

Natural gas power generation does not rely on substations. Natural gas power generation generates electricity by burning natural gas. Natural gas power stations are usually connected to data centers through dedicated pipelines. The natural gas is directly transported to the power generation facility for combustion and power generation. The generated electricity is then supplied to the data center through the local power grid or dedicated lines. It can usually be Completed at a power generation facility near the data center, unlike traditional power transmission methods, natural gas power generation does not need to pass through the high-voltage power transmission network, and therefore does not rely on remote substations and power transmission facilities. Natural gas power generation can build small natural gas power stations (such as distributed power generation systems) near data centers, reducing dependence on external power grids and shortening the response time of power supply.

2.1.2 There is a time lag between the rapid development of AI and the implementation of SMR nuclear power

< p style="text-align: left;">Although nuclear power has advantages in many aspects, the most important demand in the North American computing power market is "rapid implementation". Quickly light up the GPU to obtain computing power, and natural gas has become the current first choice.Although in February 2023, the U.S. Nuclear Regulatory Commission approved the design of the first SMR (Small Modular Reactors) by nuclear power company Nuscale Power, and China, Russia and other world Countries are racing to put SMR technology into practice, but the commercialization of SMR will still take some time, and the safety approval process is complex and time-consuming. It can already be seen that SMR has sparked global interest in nuclear energy. The U.S. nuclear fission industry has received a boost from the Inflation Reduction Act, which includes a number of tax credits and incentives while providing $700 million in funding for the Office of Nuclear Energy to support the development of high-purity low-enriched uranium (SMR). fuel) supply; there are more than 70 commercial SMR designs under development around the world, and there are currently two SMR projects operating in China and Russia. But according to the U.S. Energy Regulator, nuclear reactors are extremely complex systems that must meet strict safety requirements and account for a wide variety of accident scenarios, and the licensing process is cumbersome and varied. This means that SMRs require some standardization before they can enter the commercial market, so other solutions need to be found to address short-term energy shortages.

2.2 The combination of "natural gas + multiple energy sources" is more stableThe combination of natural gas + other multiple energy sources The solution is currently the fastest implementation solution that can meet the power needs of AI. Compared with SMR nuclear power, an independent solution with high energy density but long deployment period, natural gas power generation can be used as a basic energy source to quickly respond to load demand due to its high efficiency and flexibility. At the same time, it can be combined with renewable energy, fuel cells, and energy storage systems. Used in conjunction, they can effectively compensate for intermittency and lack of stability. This multi-energy combination can not only meet the needs of AI data centers for stable power supply, but alsoProviding a balance between carbon emissions and costs has become an important choice in current data center energy strategies.

Collaboration is not necessary, but for large-scale AI data centers that need to comprehensively balance stability, environmental protection and cost, collaborative use of multi-energy solutions is more flexible and long-term choice, when there are clear goals (such as low cost, ultra-fast deployment), a single solution can also satisfy:

[Use only natural gas to generate electricity (single solution) )】

Advantages: Natural gas power generation itself can be used as an independent power supply solution, suitable for scenarios that require stable power demand and rapid deployment, especially AI data centers that require high dispatchability;

Limitations: Although deployment is fast, carbon emissions are higher in the long run.

[The necessity of multi-energy synergy]

More stable and secure: AI data center for The power continuity requirements are extremely high (short-term power outages are not allowed), and natural gas + energy storage system or fuel cells can be used as backup support;

More environmentally friendly: natural gas + Combination of low-carbon energy sources such as wind energy and solar energy.

2.3 Natural gas solution: taking xAI as an exampleNatural gas power generation technology has mature technology paths, complete supporting equipment, and high cost performance. In the short term, it is the fastest choice to solve the AI power shortage problem. Tesla xAI uses natural gas solutions as emergency power supply. A natural gas generator is a generator that uses natural gas instead of gasoline or diesel. Compared with diesel, the purchase cost of natural gas is lower and there is no "wet accumulation" problem. Therefore, from the perspective of short-term energy solutions, natural gas generators have the advantages of cost-effectiveness, high operating efficiency, and more environmental protection than other generators using fossil fuels such as oil. According to DCD reports, Tesla CEO Musk has purchased 14 mobile natural gas generators from Voltagrid, each of which can provide 2.5 MW of power, to alleviate the power shortage problem in the data center of his startup xAI.

* Additional details 1: Musk xAI mainly uses NVIDIA H-series servers, and the cluster heat dissipation uses liquid cooling solutions. Each liquid-cooled rack in the xAI data center contains 8 NVIDIA H100 GPU servers, with a total of 64 GPUs. The dense layout requires each computing node to dissipate heat efficiently. The traditional air cooling method is difficult to adapt to, so xAI chose AMD's Liquid cooling solution.

* Additional details 2: The xAI data center also uses the Megapack energy storage system. xAI said that when building the computing cluster, its team found that the AI server did not run at 100% power all day long, but had many peaks and valleys in power consumption, so Tesla's battery storage product Megapack was added in the middle to buffer the fluctuations. Thereby improving the reliability of the overall system and reducing power loss.

2.4 Fuel cells: Take Bloom Energy as an exampleCompany profile: Bloom Energy focuses on development Efficient, low-emission energy technology, committed to promoting global energy transformation through innovative solid oxide fuel cell (SOFC) and solid oxide electrolyzer (SOEC) technologies. As a leading clean energy company, the company is committed to providing sustainable, reliable energy solutions for high-demand areas such as industry, commerce and data centers through its advanced hydrogen and fuel cell technologies. Founded in 2001, the company is headquartered in California, USA, and has expanded operations globally.

Core technology: The company's core technologies include solid oxide fuel cells (SOFC) and solid oxide electrolyzers (SOEC). The SOFC system uses 100% hydrogen Provides efficient power output with electrical efficiency as high as 65%, far exceeding traditional energy systems. Bloom Energy’s fuel cell systems can also integrate combined heat and power (CHP) technology, resulting in total energy efficiency of up to 90%, effectively reducing energy consumption and carbon emissions. In addition, SOEC technology can be used for efficient hydrogen production and is one of the key technologies in the clean energy transition.

Product application: The company's products are widely used in many fields, including industrial power supply, Commercial energy management and data center energy solutions. Particularly in the data center space, as demand for energy efficiency and carbon neutrality goals continues to increase, the high efficiency and low emissions characteristics of Bloom Energy's fuel cell technology are even more prominent.Its hydrogen solutions can not only meet large-scale energy needs, but also provide enterprises with reliable backup power to ensure the continuity and stability of operations. Bloom Energy's market currently covers many regions such as North America, Asia and Europe, especially in South Korea's cooperation with SK Ecoplant. Bloom Energy's hydrogen fuel cell project is expected to come online in 2025. Additionally, the company has announced a gigawatt fuel cell purchase agreement with AEP to power AI data centers.

3. Medium-term plan: SMR nuclear power stands out 3.1 Why nuclear power: more suitable for AI3.1.1 Characteristics of AIDC: Distributed and High Density

Compared with the traditional IDC data center, there are two most significant differences between the AIDC computing power center and the AIDC computing power center. important characteristics.

[AIDC Feature 1: Distributed Deployment]

AI application scenarios and task requirements etc. determined that AIDC needs to adopt a distributed deployment method. There are significant differences between AIDC and traditional IDC in terms of computing requirements, application scenarios, resource consumption, etc. AIDC tasks are usually computationally intensive, especially large-scale deep learning, machine learning, data analysis and other tasks in the AI field. A single calculation Nodes cannot carry all tasks. Therefore, AIDC needs to split computing tasks into multiple small tasks and distribute the tasks to multiple nodes for parallel computing through a distributed computing framework. This requires data centers or computing nodes in multiple geographical locations. Work collaboratively.

[AIDC Feature 2: 24-hour high-density computing]

Continuity of AI computing tasks The performance and high load determine that AIDC must operate at high load 24 hours a day, which requires higher power resources and cooling support. AI model training is often a long-term process that requires continuous computing power support, so AIDC usually performs long-term and continuous computing tasks; the load of traditional IDC generally fluctuates according to business needs, and many applications do not require such long-term , uninterrupted computing support. Therefore, AIDC's high-power computing hardware requires round-the-clock strong power supply and cooling support.

AIDC's distributed deployment + high-density computing characteristics determine that other energy sources are difficult to meet the adaptation needs, and small nuclear power SMR best meets the power supply needs.

Thrust - other energy sources are not suitable for AI needs, and stability and geographical location are difficult to meet AIDC:

Hydropower has obvious seasonality, which makes it difficult to meet stable and large power supply needs. At the same time, the geographical location with rich water resources is fixed, and it is difficult to meet the distributed deployment needs of AIDC. At the same time, hydropower requires a distribution network to transmit power. , the overall cost is higher, and the new construction cost and time are higher;

Thermal power has high fuel costs and strict carbon emission restrictions. Even if you purchase carbon emission indicators, the overall cost of thermal power will be higher. Therefore, it is not suitable for AIDC that requires a lot of power. At the same time, thermal power also faces power distribution The problem of higher costs caused by the network;

Although other new energy sources (such as solar energy, wind energy, etc.) are clean, their power generation capacity is affected by weather conditions and geographical restrictions. Large, intermittent and unstable make them unable to ensure AIDC under high loads Stable operation around the clock. In addition, the conversion efficiency of some new energy sources such as photovoltaics is still low, and the later operation and maintenance costs are high. From a cost-effective perspective, it is not suitable for AIDC.

Attractiveness - SMR nuclear power has stronger comparative advantages, its modular design is suitable for distributed deployment, and it also adapts to the environmental protection requirements of carbon emission reduction. The modular characteristics of SMR technology enable it to be flexibly applied in distributed deployment scenarios. Modules can be flexibly added or reduced according to the needs of different regions, ensuring that the power supply of AIDC distributed data centers is not affected by geographical location, weather, and energy price fluctuations. Moreover, as a clean energy source, nuclear power is in line with the global trend of reducing carbon emissions and is suitable for AIDC's demand for green energy. Therefore, nuclear power SMR is suitable as the main power supply source for AIDC.

3.1.2 Nuclear power SMR is the fastest to be implemented

What is an SMR - a modular, smaller, more deployable nuclear reactor. SMR (Small Modular Reactor) is a new development of nuclear energy technology. SMR is a type of nuclear power plant.type, but are significantly different from traditional nuclear power plants. An SMR is a small, modular nuclear reactor that is designed to provide smaller-scale power output and is built using modular components to facilitate factory production and transportation. Generally, the output power of an SMR is lower than that of a traditional large nuclear reactor. smaller. Before the advent of AIDC SMRs were commonly used in remote areas off the grid, on small islands, on military bases, or as a supplemental source of power for industrial use.

Compared with traditional nuclear power plants, SMR has the advantages of small scale, short construction time, (construction and maintenance), lower cost, higher safety, cleaner and greener, longer life, etc.:

Small module output power: SMR The output power is smaller than that of traditional nuclear power plants, usually between tens to hundreds of megawatts, while the scale of traditional nuclear power plants is usually more than 1,000 megawatts. For example, NuScale's SMR module can provide 77MW of power individually, and can be assembled into up to 12 modules. Can provide 924 MW of electricity;

Shorter construction time: Because SMR adopts a modular design, it allows factory prefabrication and rapid assembly, such as NuScale's SMR nuclear power plant takes only 36 months (3 years), compared to the typically longer construction period for conventional nuclear power plants, which can take more than five to ten years.

Small footprint: Traditional nuclear power plants occupy a large area, usually larger than 1 square mile (approximately 2.6 square kilometers), while modular SMRs occupy Areas are generally smaller, with NuScale predicting that the SMR plant would cover an area of 0.06 square miles, close to the size of a small park.

Lower costs: The construction costs of traditional nuclear power plants are usually higher and are affected by economies of scale, but the construction costs of SMRs are relatively low, partly due to the use of standardization , Modular design enables each module to be mass-produced and reduces the construction and maintenance costs of a single reactor.

Higher safety: SMR designs often have higher passive safety features and disaster resistance, and can automatically shut down the reactor in the event of a fault without human intervention. Moreover, SMR reactors are smaller and therefore have higher safety and reliability.

Cleaner: SMR uses advanced reactor design,It can use fuel more efficiently and reduce the generation of nuclear waste, which is more in line with the requirements of clean energy;

Longer life: SMR is designed to have a service life of several There is no need to change the fuel for ten years, and the lifespan is far longer than that of traditional power generation modes. For example, Nuscale's SMR has a design life of up to 60 years.

The principle of SMR - basically the same as that of large nuclear reactors, it is still produced through nuclear fission reactions The thermal energy forms steam, which drives a generator to generate electricity. (1) Nuclear fission reaction: Like traditional nuclear power plants, the core of SMR is a nuclear reactor, which generates heat through nuclear fission reaction. Uranium-235 in the reactor When fissile materials (such as uranium or plutonium) absorb neutrons and undergo fission, the fission process will release a large amount of heat energy and neutrons; (2) Heat exchange and steam generation: The heat generated by the fission reaction in the reactor can be used for heating Coolant, the coolant flows inside the nuclear reactor, taking away heat and transferring it to the steam generator The generator or directly transfers heat to water through a heat exchanger to form steam; (3) Steam-driven generator: The generated steam is introduced into the turbine, and the generator is driven by the rotation of the turbine. The generator then converts mechanical energy into electrical energy to supply Grid or user; (4) Cooling system and safety mechanism: SMR Natural circulation cooling systems or passive safety systems are often used, using natural physical processes (such as thermal convection) to keep the reactor cool, thereby reducing reliance on external power and equipment. These systems can automatically shut down the reactor and cool down in the event of a failure.

The composition of SMR - usually includes multiple modules, using standardized components, which can Quickly assemble and deploy. (1) Reactor core: contains nuclear fuel, nuclear fission occurs, and generates a large amount of heat energy; (2) Cooling system: heat is taken away from the reactor core by circulating coolant, which can be liquid metal (such as sodium), gas (such as carbon dioxide) or helium), or water, some SMR The design adopts natural convection or passive safety system, which does not rely on external power to maintain cooling, which enhances the safety of the system; (3) Steam generator: transfers the heat-exchanged coolant to water to generate steam, which is introduced into the turbine to drive Generate electricity; (4) Turbines and generators: convert mechanical energy into electrical energy; (5) Control system: SMR uses a digital control system, and some also introduce AI Technology; (6) Safety system: Use a passive safety system, that is, the system can automatically cool the reactor without external power supply or operator intervention. Common designs include natural convection cooling, thermal storage devices, etc. These designs can emergencyWhen operating, the safety of the reactor is maintained through physical principles (such as thermal convection or gravity); (7) Nuclear waste treatment system: stores or processes nuclear waste and radioactive materials.

At present, there are several different technical routes for small modular reactor SMR, the most mainstream The most popular one is the light water reactor (LWR-SMR) because the technology foundation is mature and it is easy to obtain regulatory approval. As of 2021, countries around the world have proposed more than 70 different SMR nuclear power solutions, including pressurized water reactor solutions, helium gas-cooled reactor solutions (HTGR), high-temperature gas-cooled practical reactor solutions, and sodium-cooled fast neutron reactor solutions (SFR). About half of the plans are light water reactor reactions, which evolved from second-generation nuclear power technology. The technology is highly adaptable and can be commercialized quickly. However, due to the Fukushima Nuclear Power Plant issue in 2011, the technology tree selection for nuclear power has become more complicated, and safety concerns about light water reactors have become more prominent. Safer non-light water reactor solutions have become more popular, and high-temperature gas-cooled reactor solutions have gradually become popular. :

Light water reactor (LWR-SMR): based on mature light water cooling technology, such as NuScale's design, the most mainstream and close to commercialization;

High-temperature gas-cooled reactor (HTGR): cooled by inert gas (such as helium), suitable for high-temperature process heat requirements, such as Huaneng high-temperature gas-cooled reactor;

Liquid metal-cooled reactor (such as sodium-cooled reactor): such as the Natrium reactor developed by TerraPower, which has efficient heat dissipation capabilities;

Molten Salt Reactor (MSR): uses high-temperature lava as cooling Fast Neutron Reactor (FNR): uses fast neutrons for high-efficiency fission fuel, such as the Russian BREST reactor type.

3.3 SMR Nuclear Power Current Situation and Industrial Chain3.3.1 Cloud giants are vigorously deploying nuclear power

There is a shortage of power, and various cloud giants are deploying SMR nuclear power. On the one hand, the data center’s demand for power The demand is huge, SMR Providing long-term stable clean energy can reduce dependence on traditional power grids. On the other hand, in the long run, SMR can reduce the risk of electricity price fluctuations, optimize long-term operating costs, andAnd help the company achieve its carbon neutrality commitment:

Amazon: As early as March this year, it began to look for nuclear power support solutions and acquired Susquehanna, Pennsylvania, for $650 million. The Talen Energy data center park next to the Steam Electric Station nuclear power plant; and in October this year announced three major nuclear power investment agreements, cooperating with Energy Northwest and Dominion Energy to build 960MW and 300MW in Washington and Virginia respectively. SMR; led the US$50 billion C-1 round of financing obtained by nuclear energy startup X-energy;

Microsoft: Support for nuclear power is also significant, Bill Gates said in June this year that he would continue to invest billions of dollars in the "next generation" nuclear power plant in Wyoming, the United States, through the start-up company he founded, TerraPower LLC. The first commercial reactor is expected to be completed in 2030; in September In March, it reached a strategic agreement with Constellation Energy to restart the Three Mile Island nuclear power plant, which will provide approximately 835 megawatts of power for Microsoft's data centers.

Google: In October it said it had agreed to buy nuclear power from a small modular reactor being developed by a startup called Kairos Power to develop more than 500MW of electricity and The first reactor is expected to be operational in 2030;

Oracle: Founder Larry Ellison said in September that Oracle planned to build a three-SMR reactor Supported 1GW Data center campus;

Meta: is actively soliciting proposals from nuclear power developers, aiming to promote the development of its artificial intelligence technology and achieve environmental protection by increasing nuclear power generation capacity Target, plans to add 1 to 4 gigawatts of US nuclear power generation capacity by the early 2030s.

The huge power gap caused by AI data centers and the urgent power requirements faced by CSPs have made the trend of SMR nuclear power industry more and more obvious. It is expected that more SMR layouts will be announced in the future. .

3.3.2 SMR Nuclear Power Upstream and Downstream

The SMR nuclear power industry chain covers all aspects from upstream fuel uranium mines, midstream R&D and construction, downstream operations and waste processing. Relatively speaking, upstream design and manufacturing have higher thresholds for professionalism and technical barriers, so upstream manufacturers have higher bargaining power. Due to the long and stable operation cycle of the downstream operation and maintenance links, they can bring long-term cash flow and are also relatively profitable. The profit margin of midstream project construction is subject to factors such as construction cost, project cycle and engineering risks, and the profit margin is relatively less stable than that of upstream or downstream.

[Upstream: raw materials and processing]

The upstream industrial chain mainly involves the requirements for nuclear energy development The supply of basic raw materials, key equipment and nuclear fuel mainly includes uranium mining and uranium enrichment.

(1) Uranium mining and uranium processing

Uranium mining: uranium around the world The supply market is highly concentrated. U.S. uranium mines mainly rely on imports. Global uranium mines are mainly dominated by Kazakhstan, Canada and Australia.

Main uranium mining and typical companies that mine locally: Kazatomprom in Kazakhstan, Cameco in Canada and Orano (formerly Areva, a French company but mining uranium globally ) and Denison Mines, Australia's BHP (BHP Billiton) and Rio Tinto (Rio Tinto Group), Russia's Rosatom, etc. In addition, there are also some uranium mining companies in the United States, such as Energy Fuels (NYSE: UUUU), Uranium Energy (NYSE: UEC), etc.

Uranium processing: Uranium enrichment technology has very high safety, cost and technical requirements. Therefore it is mainly dominated by a few multinational companies. Natural uranium is mainly composed of uranium-235 and uranium-238. When a neutron collides with uranium-235, it will release huge energy through a fission reaction. The fissionability of uranium-238 is smaller than that of uranium-235. Natural uranium only contains About 0.7% uranium-235, so isotope separation (uranium enrichment) is required to increase its content to 3% to 5% for use as fuel for light water reactors. Concentration methods include gas diffusion, laser concentration and centrifugation.

*Principle of centrifugation: The gaseous uranium compound uranium hexafluoride is fed into the rapidly rotating rotor of the centrifuge to separate U-235 and U-238. The heavier isotope U-238 is pushed outward, while the lighter isotope U -235 is concentrated in the center of the rotor. The gas with a higher concentration of U-235 is extracted and fed into another centrifuge, where the process is repeated several times to produce uranium with a higher concentration of U-235.

Main uranium enrichment companies: Centrus Energy (NYSE: LEU, United States, dominates the global market), Orano (France, both mining and processing), Rosatom (Russia) ), Urenco (Europe).

( 2) Nuclear fuel assembly manufacturing

The fuel used in SMR reactors includes uranium fuel rods, fuel elements and control rods, etc. The components must meet specific standards to ensure the safety of the reactor and efficient operation.

Participants: Such as Westinghouse, Orano, etc., providing nuclear fuel components and technical support.

(3) Reactor component manufacturing

Reactor components are an important part of SMR, including Reactor pressure vessels, cooling systems, control systems, reactor cores and other related facilities require a high degree of radiation resistance, high temperature resistance and reliability. Due to the modular design of SMRs, reactor components are typically mass-manufactured in factories and transported to site for rapid assembly, reducing on-site construction time.

Participants: such as NuScale Power, Rolls-Royce, etc.

[Midstream: Design, R&D and Construction]

(1) SMR design and R&D

Design and R&D: The design company is responsible for the technical development and design standardization of SMR reactors. The R&D of SMR usually includes the structural design, cooling system design, and control system of the nuclear reactor. integration, etc., assumingDesign R&D companies work closely with departments and regulatory agencies to ensure that designs comply with nuclear safety standards.

Participants: SMR design and R&D companies such as NuScale Power, OKLO, TerraPower, Rolls-Royce, etc.; institutions such as the U.S. Department of Energy (DOE) provide financial support And supervise and verify the design of SMR.

(2) Reactor construction and installation

The modular design of the SMR allows most components Prefabricated in the factory and then transported to site for quick installation. The construction phase is simpler than that of traditional nuclear power plants because SMRs are smaller in scale and highly modular, and can be put into operation without large-scale construction. For example, the construction company is responsible for assembling the various modules of the SMR reactor into a complete For nuclear power plants, complete on-site installation and factory-prefabricated components will greatly shorten the on-site construction cycle.

Participants: Construction companies such as Bechtel, Fluor, etc., are responsible for the construction and assembly of SMR power plants.

[Downstream: operations, sales and waste processing]

(1) SMR nuclear power plant operation

The operator is responsible for the long-term management, maintenance, monitoring of the reactor operation of the power plant, and ensuring that the reactor in a safe state. The operation and management complexity of SMR nuclear power plants is lower than that of traditional nuclear power plants. In addition, operators are also responsible for regular maintenance of the SMR system, including fuel replacement, equipment inspections and technical upgrades.

Participants: such as American Electric Power Company (AEP), British Electric Power Company (EDF), Southern Company, Exelon Corporation, Duke Energy (NYSE: DUK), Entergy Corporation (NYSE: ETR), PSEG (Public Service Enterprise Group, NYSE: PEG), Dominion Energy, etc. Some operators may purchase SMR power stations and operate them; management and monitoring companies will provide intelligent monitoring, data analysis and system optimization.Serve.

(2) Electricity sales and power grid connection

The electricity produced by SMR power stations is sold to grid companies or industrial users through power purchase agreements (PPA). SMR is suitable for small grids and is particularly suitable for specific markets such as remote areas, remote cities or industrial projects.

* Power Purchase Agreement (PPA): Operators sign long-term contracts with power purchasers (such as power grid companies, large industrial users, etc.) to ensure stable cash flow and profit model.

Participants: Power purchasers such as local power grid companies, large industrial enterprises, institutions, etc.

(3) Waste and nuclear power decommissioning treatment

SMR reactors require waste management after the life cycle. The long-term storage and processing of nuclear waste is an important part of the nuclear power industry. Waste management companies are responsible for the safe handling, transportation and storage of waste to ensure compliance with nuclear safety. standard.

Players: Waste disposal companies such as Waste Control Specialists, which specialize in the disposal of nuclear waste.

4. Long-term outlook: Controllable nuclear fusionNuclear fusion is achieved through two light The process by which atomic nuclei combine to form a heavier nucleus and release large amounts of energy. Controlled nuclear fusion reactions release about 4 million times more energy than burning coal, oil or natural gas and four times more than nuclear fission, providing unlimited clean and affordable energy if the process could be replicated on an industrial scale. Currently, more than 50 countries are conducting nuclear fusion research. However, due to the strict conditions for nuclear fusion to occur, breakthroughs in new materials and new technologies are still needed to achieve controllable nuclear fusion. How long it will take to achieve controllable nuclear fusion will depend on the technology development progress of the industry. At the same time, it is necessary to develop the necessary infrastructure and formulate management requirements and standards for the technology. According to space reports, British company Tokamak Energy has heated hydrogen plasma to 27 million degrees Fahrenheit for the first time in a new reactor, which is hotter than the core of the sun. The company said that using nuclear polymerizationChanging the production of commercial electricity could be achieved by 2030.

5. Business models and participants in the energy war 5.1 SMR Nuclear Power US Stocks5.1. 1 SMR (NuScale, R&D manufacturer)

Company profile: NuScale Power is the first SMR nuclear power manufacturer to go public. The company originated from the SMR research project jointly carried out by the Idaho Laboratory and Oregon State University in 2002, and received support from the U.S. Department of Energy (DOE). NuScale Power. LLC was established in 2007 and became the first to obtain NRC ( The SMR has been designed and approved by the U.S. Nuclear Regulatory Commission and will become the first SMR technology provider to go on the market in 2022.

Core products: The company's core product SMR power module. The NuScale Power Module is the smallest light water SMR, measuring 76 feet tall and 15 feet in diameter, and can generate 77 MW of power from a single module. The modules, including seals, are completely manufactured in the factory and transported to the factory site by truck, rail or barge, eliminating the need for on-site fabrication or construction, reducing the schedule and cost risks associated with on-site construction.

Competitive advantage: The company has its own nuclear power plant - VOYGR Plant Models. VOYGR Plant Models is a standardized nuclear power plant designed by NuScale for its small modular reactor SMR. It has flexible power output and higher operating efficiency and can meet power needs of different sizes. It is the first and only design approved by the U.S. Nuclear Regulatory Commission (NRC) Approved small modular reactor.

VOYGR Plant Models different parameter modules:

VOYGR-4: composed of 4 NuScale SMRs Composed of modules, it provides approximately 308 MW of power output, suitable for providing power to small and medium-sized communities and industrial applications;

VOYGR-6: Contains 6 modules, providing approximately 462 Megawatt power, suitable for applications with medium-sized power needs, such as small cities or larger industrial facilities;

VOYGR-12: Composed of 12 modules with a total power output of approximately 924 MW, this is NuScale’s largest capacity VOYGR layout and is suitable for meeting large-scale For urban and industrial applications where power is needed, and even as baseload power for grid-level grids, the VOYGR-12 can supply 154 MW of power for 12 years without the use of new fuel, even in the event of a catastrophic loss.

Business layout: The company provides downstream customers with services ranging from license application, construction and commissioning to operation and maintenance full service support. The services provided by the company can be divided into two categories: pre-commercial application (COD) and post-commercial application:

Pre-commercial application: startup and testing, ITAAC management (inspection, Testing, Analysis and Acceptance Criteria), COLA Management (Co-License Application for VOYGR™ Power Plant);

Post-Commercial Application: Design Engineering Management, O&M Engineering project management, requalification training and simulator support, procurement and spare parts management, nuclear fuel and fuel outages, system verification and validation.

Project progress: We have cooperated with many customers around the world on SMR nuclear power projects. To date, the company has partnered with RoPower Nuclear S.A. (Romania), KGHM Polska Miedź S.A. (Poland), Kozloduy Power Plant (Bulgaria), Standard Power (Ohio and Pennsylvania), Prodigy Marine Power Plant (Canada), Indonesia Power (Indonesia) ) and GS Energy (South Korea) have project cooperation.

"Soft power": Focus on scientific research and cultivating talents, and have opened E2 nuclear energy exploration center laboratories in many universities around the world. In addition, the company has also set up an E2 Center (Energy Exploration Center) to provide users with practical opportunities to apply nuclear science and engineering principles through simulated real nuclear power plant operating scenarios. E2 has center points in multiple universities and regions around the world. Such as Texas College Station, Bucharest Polytechnic University (Romania), Seoul National University in South Korea, Oregon State University, etc.

Financial analysis: The company's financial situation is currently in a volatile stage, with abundant cash flow and no debt, and excellent results in cost reduction and efficiency increase. The company's latest third quarter report shows that the third quarter of 2024:

Revenue: The company’s operating income was US$500,000, compared with US$7 million in the same period last year. The decrease in revenue was mainly due to the termination of the contract with CFPP (on November 8, 2023, UAMPS and NuScale announced that both parties have agreed to terminate the carbon-free power project CFPP);

Net profit: The company's net loss was US$45.5 million (of which US$7.2 million was the fair value of outstanding warrants) Value-related non-cash charges), the company's net loss in the same period last year was US$58.3 million, and the net loss further narrowed;

Expenses: Operating expenses were US$41.2 million, while The same period last year was 93.9 million US dollars, operating expenses decreased by 52.7 million US dollars year-on-year, and the company further improved its ability to reduce costs and increase efficiency;

Cash: As of the third quarter report of 2024, cash and cash equivalents and short-term investments of $160 million (of which $5.1 million is restricted) and no debt

Capital background:

Fluor Corporation: A world-renowned engineering and construction company, it is the major shareholder and owns a large number of shares. Its investment in NuScale began in 2011 , to help companies obtain support in technology research and development and commercialization;

U.S. Department of Energy (DOE): The United States has provided a large amount of funding for NuScale's research and development through the Department of Energy. Support (over $300 million), support SMR Technology development and deployment;

Japanese trading company JGC Group;

Public and private equity: In 2021, NuScale announced that it would go public through a merger with Spring Valley Acquisition Corp.. Through this merger with a SPAC (Special Purpose Acquisition Company), NuScale entered the public capital market and providedNuScale brings about $235 million in funding;

South Korean company Doosan Heavy Industries: the world's leading heavy industry company, not only participates in investment, but also plans to build reactors for NuScale Provide some parts and manufacturing support;

5.1.2 OKLO (R&D manufacturer)

Company Profile: The company is owned by Jacob DeWitte and Caroline Cochran (both founders have a background in nuclear energy engineering) was officially established in 2013, focusing on the development of small modular reactors (SMRs), headquartered in California. In 2014, OKLO entered the well-known start-up accelerator Y Combinator and received start-up funds, 24 In September, OKLO received site authorization for a mini-reactor in Idaho and plans to deploy it in 2027. The company's Aurora microreactors are metal-fueled (unlike other nuclear reactors that use uranium fuel) and currently provide 24/7 clean energy to data centers, factories, industrial sites, communities and defense installations.

Core product: The company's core product "Aurora Microreactor", with a single module power of 1.5 MW, the Aurora module is refueled every ten years (so major expected shutdowns time is maintenance of the power conversion system), Aurora power plants offer power from 15 MW to 50 MW The plant covers only a few acres, has low operating and maintenance costs, and can be located where customers need power, avoiding expensive and long power lines.

Competitive advantage (fuel is different from others):

Microreactors are more suitable for distributed needs : OKLO's Aurora microreactor is a medium-scale SMR. The power plant is usually around 50MW and has a competitive advantage in meeting medium-sized distributed, remote and independent power needs. In comparison, NuScale's power is larger and more adaptable to the grid. Level energy solutions;

Fuel and cooling technology are cleaner, more environmentally friendly, and cheaper: Oklo's Aurora reactor uses metal fuel instead of traditional light water reactor fuel, and its cooling system is also different from common water cooling. Use liquid sodium ascoolant. On the one hand, such a fuel and cooling design can improve the thermal conductivity and efficiency of the reactor, and on the other hand, it can reduce the output of nuclear waste, thereby reducing the cost and environmental impact of nuclear waste treatment. In contrast, systems like NuScale, which uses traditional light water as the cooling medium and uranium as the fuel, are more suitable for existing nuclear power plant technology and supply chains.

Financial analysis: The company continues to expand investment in preparation for initial commercialization. The company's current cash flow is relatively abundant. The company's latest third quarter report shows that the third quarter of 2024:< /p>

Expenses: Operating expenses were US$12.28 million, compared with US$4.66 million in the same period last year. The company continues to expand investment;

Net profit: company's net loss US$9.96 million, compared with US$8.67 million in the same period last year. The expansion of net profit loss was mainly caused by continued investment;

Adequate cash: As of the third quarter report of 2024: Cash and cash Total marketable securities were $290 million, including $91.8 million in cash and cash equivalents and $197 million in marketable securities.

Capital background:

Sam Altman (Founder of Open AI): Oklo’s main funder In 2014, Altman included Oklo into the Y Combinator incubator. In 2024, Altman further helped Oklo successfully list on the New York Stock Exchange through a merger with his special purpose acquisition company (SPAC) AltC Acquisition Corp., raising approximately $306 million in funding to support its nuclear energy projects. Commercialization and future development;

Y Combinator: OKLO is a start-up company incubated by Y Combinator. Early financing mainly comes from YC The incubation project received start-up capital support. After Oklo merged with AltC Acquisition Corp, Oklo went public with a pre-investment valuation of approximately US$850 million. Early backer Y Combinator may retain an indirect shareholding in Oklo, but has not yet announced a target. Additional investment in post-IPO stages;

DCVC(Data Collective): A well-known venture capital company that focuses on investments in technology and deep technology fields, providing financial support to OKLO to help its technology development and market expansion;

U.S. Department of Energy (DOE): DOE has provided funding for OKLO's research and development for the commercialization of advanced fuel cycles and manufacturing technologies. DOE's funded projects have played a key role in promoting the maturity and verification of OKLO's technology.

5.1.3 NNE (NANO, R&D and manufacturing + fuel processing)

Company profile: Nano Nuclear Energy's main business covers 4 SMR-related contents, including manufacturing, fuel, transportation and other links, aiming to create a diversified vertically integrated industrial chain. NNE is an American start-up company. Its founder and chairman, Jay Jiang Yu, was an analyst at the investment banking department of Deutsche Bank. James Walker, CEO and chief R&D nuclear physicist, was responsible for the project of the new Rolls-Royce nuclear chemical plant. Principal, the company is focused on developing small modular reactors and is committed to becoming a commercially focused, diversified and vertically integrated company spanning four business lines:

Micro nuclear reactor technology development: NANO Nuclear Its main products include solid core battery reactor "ZEUS" and low-pressure coolant reactor "ODIN";

Nuclear fuel manufacturing: Establishment of nuclear fuel subsidiary HALEU Energy Fuel Inc. ( HEF), providing HALEU nuclear fuel (an advanced nuclear fuel containing 5%-20% uranium 235), which can be used by itself or supplied externally;

Nuclear fuel transportation: Establish a transportation subsidiary, Advanced Fuel Transportation Inc. (AFT), to provide HALEU nuclear fuel for small modular reactors, microreactor companies, laboratories, the military, U.S. Department of Energy projects, etc.;

Nuclear energy industry consulting services;

Other subsidiaries: NNE also established a space business subsidiary NANO Nuclear Space Inc. ( NNS), explore the application of NNE micronuclear reactor technology inPotential commercial applications in space.