49 mins ago

284

Author: insights4vc Translation: Shan Oppa, Golden Finance

Circle Internet Financial was founded in October 2013 by serial entrepreneurs Jeremy Allaire and Sean Neville. Allaire’s vision is to use cryptocurrency technology to revolutionize online payment methods.

In an early interview, he described Bitcoin and digital currencies as "a one-time opportunity to shape the future of the Internet and global business" and hoped to make payments "simpler, safer, and less costly for consumers and businesses."

Circle's original mission was to build a "universal pipeline system for money in the network", just as the HTTP protocol facilitated information transmission (a sentence Allaire often used to describe a company's long-term goal).

Early Products and TransformationsIn the first few years, Circle launched a consumer-oriented service designed to simplify payments in cryptocurrency. In 2015, Circle obtained the first BitLicense license in New York to operate digital currency services, reflecting its early emphasis on compliance. The company's business model has also undergone significant evolution: 2013–2016: Circle Pay, a Bitcoin-based payment application, was developed, where users can collect and pay in digital currency. During this period, the company raised more than US$135 million in financing, of which the US$50 million in financing led by Goldman Sachs in 2015, showing the strong endorsement of mainstream financial institutions.

2018: Business focus shifts to cryptocurrency trading services. Circle acquired the major cryptocurrency exchange Poloniex in early 2018 in an attempt to enter the trading market. But the decision ultimately proved a mistake - Circle sold it in 2019, with a rumored loss of $156 million. During the same period, other non-core products were also sold (such as Waager Digital, a mobile investment app sold in 2020) to refocus the business direction.

2018–2019: USDC launch

Circle's real "killer application" is USD Coin (USDC). In October 2018, Circle and Coinbase jointly formed the CENTRE alliance and launched USDC - a stablecoin anchored to the US dollar 1:1. USDC is fully reserved by US dollar assets and is available as a regulated, highly transparent alternative to stablecoin. This marks the company's transformation from consumer application development to stablecoin issuers and crypto financial infrastructure providers.

2020–2021: After divesting the trading platform business, Circle focuses on the expansion of the USDC ecosystem. In early 2020, USDC's circulation was about $500 million (compared to the USDT of the top stablecoin Tether, by comparison, was about $4.2 billion). But USDC has grown rapidly due to Circle's efforts in transparency and compliance. In the crypto bull market in 2020–2021, its circulation soared to tens of billions of dollars, verifying the correctness of the direction of transformation. It is worth noting that Circle completed a US$110 million Series E financing in 2018 to support USDC's launch, and announced a merger and listing in 2021 to cope with USDC's rapid growth.

Strategic PartnershipIn the process of development, Circle has established a number of key cooperation to promote stablecoins into the mainstream financial system:

Coinbase – USDC Alliance: As the co-founder of the CENTRE Alliance, Coinbase has supported USDC on the platform from the very beginning and became a minority shareholder of Circle in 2023. This collaboration ended the CENTRE alliance, making Circle the sole issuer of USDC, while Coinbase received a 50% share of reserve interest income. Coinbase plays a key role in USDC's retail and institutional distribution, strengthening both parties' shared commitment to regulated stablecoins.

Visa – Global Payment: In 2020, Circle joined Visa's Fintech Fast Lane Program and piloted the use of USDC for Ethereum-based settlement in 2021. In 2023, Visa expanded the project to settle millions of dollars in USDC on Ethereum and Solana chains through partners such as Worldpay and Nuvei. Circle CEO said the collaboration demonstrates how stablecoins can drive global payment modernization.

BlackRock – Asset Management: Circle will start from BlackRock and Fideli in 2022Institutions such as ty raised US$400 million in financing. BlackRock has also become a key manager of USDC reserves, pushing for the establishment of the "Circle Reserve Fund" - a regulated money market fund that now holds most of USDC's cash reserves. This cooperation strengthens institutional trust and optimizes reserve management.

Institutional Alliance: Circle also establishes partnerships with Stripe, MoneyGram, Mastercard (crypto cards), as well as JPMorgan Chase, Bank of New York Mellon, etc. As a founding member of the Blockchain Association, Circle continues to actively participate in regulatory dialogue. These relationships have helped Circle become the core bridge between the traditional finance and crypto worlds.

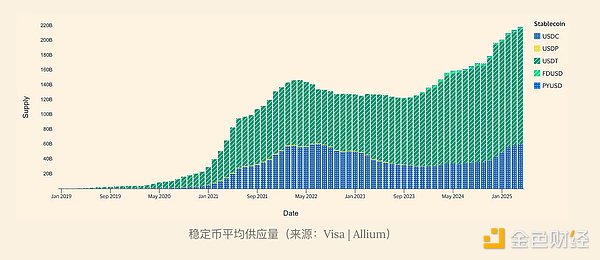

USDC's role in the global marketUSDC is currently the world's second largest stablecoin, second only to Tether's USDT, and plays a key role in the crypto market. Its market value was once close to USDT, and the dominance of the two had several alternating positions.

In early 2022, USDC grew rapidly and is expected to surpass USDT. After the Terra collapse in May 2022, investors fled from high-risk stablecoins, with USDC circulation growing from about $49 billion to $55 billion, while USDT falling from about $83 billion to $66 billion. The rise of USDC at this stage is generally attributed to Circle's advantages in transparency and regulatory compliance — by contrast, Tether has been criticized for its opaque reserves and has gradually cut its riskier commercial paper positions.

But in 2023, under the US banking crisis and regulatory pressure, the market structure reversed. USDT is leading the way, especially in the banking crisis in March 2023, USDC confidence was hit. When Silicon Valley Bank (SVB) went bankrupt, Circle disclosed that $3.3 billion in USDC cash reserves were frozen in the bank. USDC once "deaned" and its price fell to about $0.88, and then quickly recovered due to the Federal Reserve's guarantee of SVB deposits. However, investors netted $6 billion in USDC in the week of the crisis. Relatively speaking, USDT, which is not directly exposed to the US banking system, gains market share.

As of early 2024, Tether's USDT accounted for more than 70% of the stablecoin market (about US$97 billion in February 2024/the total market value was US$137 billion), while USDC share dropped to approximately 20% (about US$28 billion).

Stablecoin market share will fluctuate with the market environment. In 2023, USDT's dominance rose to about 63%; while USDC's share declined for a while, it rebounded to about 25% at the beginning of 2025, reflecting the market's renewed trust in it. The collapse of the algorithmic stablecoin UST in 2022 has made investors more inclined to asset-backed stablecoins like USDC.

Current statusAs of the first quarter of 2025, USDC has once again entered the growth track. Circle reported that USDC circulation in March 2025 was approximately US$60 billion, a year-on-year increase of 78%. This rebounded from a low of about US$24 billion at the end of 2023, showing a rebound in market confidence and demand brought by new application scenarios. USDC currently accounts for about one-quarter of the total value of the stablecoin market, while USDT accounts for about two-thirds. USDC and USDT together account for more than 90% of the supply share of the stablecoin market, while others such as BUSD and DAI occupy the remaining part. It is worth noting that algorithmic stablecoins (maintaining anchorage through algorithms rather than full reserves) are mostly eliminated by the market after experiencing high-profile failures. The collapse of TerraUSD's zeroing in May 2022 highlights the systemic risks of unsecured stablecoins, making full reserve stablecoins such as USDC and USDT an option of trust. USDC has benefited from this "help-haven" trend - both regulators and users are beginning to see fully collateralized stablecoins as a safer model.

Adoption in DeFiUSDC has been deeply integrated in the decentralized finance (DeFi) ecosystem. Due to its transparency and reliability, it is often selected as the first choice stablecoin by DeFi platforms. Many decentralized protocols rely on USDC to provide liquidity and use it as a stable unit of account:

On lending platforms such as Aave, Compound, USDC is one of the most commonly lent and provided assets, suitable for earning income or leverage operations. Due to its stable value, USDC has also become the ideal collateral for crypto mortgages.

On decentralized exchanges (DEX), USDC trading pairs connect crypto assets with stable dollar value. For example, the USDC/ETH pool on Uniswap is one of the largest pairs of trading volume and can provide critical liquidity in low volatility.

In stablecoin exchange pools (such as Curve Finance), USDC is also a core asset. Users can redeemed with extremely small slippage between USDC, USDT, DAI, etc. Since 202Two years later, due to the low risk, the proportion of USDC in this type of pool increased.

MakerDAO's DAI stablecoin is partially backed by USDC (through its Peg Stability Module), meaning Maker holds billions of USDC to maintain DAI exchange rate stability. This "centralized mortgage" has caused controversy, but it also highlights the importance of USDC as a DeFi reserve asset.

Anyway, USDC has become the de facto digital dollar infrastructure in DeFi. Its purpose has surpassed crypto trading and supports DAO vaults, NFT markets and on-chain foreign exchange markets. Circle promotes its popularity in various ecosystems by extending USDC to more than 19 blockchains (such as Ethereum, Solana, Avalanche, Tron and new chains launched in 2023–24).

Enterprise and real-world application scenariosIn addition to the crypto-native field, USDC is also increasingly used in traditional payment and settlement scenarios:

Cross-border payment: Enterprises in emerging markets use USDC to complete cross-border transactions at a lower cost and faster speed. For example, Brazilian manufacturers can use USDC to pay Nigerian suppliers, bypassing the SWIFT system and multiple transit banks. Stablecoins eliminate exchange rate conversion fees and delays, achieving near-instant settlement. In 2024, the transaction volume of startups (such as Yellow Card and Conduit) focusing on B2B remittances in Africa and Latin America will double, and companies will prefer USDC for trade payments. The cost savings are obvious – sending $200 from the United States to Colombia through stablecoins is only a few cents (<$0.01), while the traditional channel is about $12.

Fund management: Large companies have also begun to try stablecoins. In 2024, SpaceX partnered with startups to accept payments from multiple currencies and instantly converted to USDC for fund management. This shows that stablecoins are not only trading tools, but also operating capital tools for enterprises. The stability and liquidity of USDC (quickly cashable) makes it more attractive in unstable markets of the banking system.

Financial Technology Integration: Major fintech and payment companies have integrated USDC. For example, Stripe supports payments at USDC to certain freelancers and sellers, addressing traditional slow or high fees. MoneyGram launches services to support cash exchange and ex-USDC, connecting physical cash and digitalDollar. Circle's API also supports new banking applications, providing USDC accounts for high inflation users as a local currency alternative.

Visa and Mastercard pilot: Visa has used USDC to settle transactions for merchants. Mastercard works with Circle to test (such as cards paid through USDC balance). Such measures blur the boundaries between credit card networks and blockchain networks, indicating that stablecoins may be used as widely in commercial use as fiat currencies in the future.

Global expansion: In high-inflation emerging markets such as Latin America, Africa, and the Middle East, stablecoins have become alternatives to the US dollar. Both USDT and USDC are widely used to fight the devaluation of the local currency. Circle promotes relevant application scenarios under the slogan of "Global Digital Dollar Access" - allowing anyone who owns a mobile phone to hold stable US dollar assets. For example, in Argentina and Türkiye, residents use USDC to save USD through exchanges or P2P markets to deal with over 50% inflation. Although USDT is more commonly used in some regions (due to longer history or easier access), USDC is gradually attracting more users and fintech companies due to its credibility.

Regulatory PositioningCircle intends to position USDC as a trustworthy, compliant stablecoin and actively cooperates with regulators in the United States and overseas:

In the United States, Circle is a licensed remittance company and has always emphasized compliance with laws (such as KYC/AML). Circle was an early winner of BitLicense in New York in 2015, and demonstrated regulatory credentials as many cryptocurrency companies avoid strict licensing. Circle's Chief Strategy Officer Dante Disparte and CEO Jeremy Allaire often contact the makers. Allaire testified in the U.S. Senate in 2021, advocating for reasonable regulation of stablecoins to incorporate them into the financial system. Circle supports the promotion of federal stablecoin legislation, believing that clear rules will consolidate the U.S. role in cryptocurrency innovation while protecting consumers.

Interaction with U.S. regulators: Circle's attempt to go public through SPAC in 2021-2022 means a large amount of disclosure documents required to be submitted to the SEC, which requires a high degree of transparency (Circle must provide regulators with audited financial statements and reserve data). althoughAlthough the SEC ultimately did not approve the SPAC merger (more on that later), Circle is known for its openness and transparency compared to other cryptocurrency companies. Circle also works with law enforcement — and in August 2022, Circle freezes about $75,000 USDC in sanctioned addresses after the U.S. Treasury Department approved an illegal use of a cryptocurrency mixer (Tornado Cash), indicating that U.S. sanctions will be enforced on its network. The move has attracted criticism from some decentralized advocates, but it highlighted the Circle compliance first position.

Regulatory Challenge: Despite the Circle's attitude, the regulatory environment in the United States remains uncertain by 2023. Stablecoins are in the gray zone – not classified as securities by default, but lack a comprehensive regulatory framework. In early 2023, U.S. bank regulators warned banks about cryptocurrency-related liquidity risks (mentioned loss of stablecoin reserves). The lack of a federal stablecoin law means Circle must deal with state systems and face the risk that regulators (or Congress) may introduce new requirements. This uncertainty may be the reason why the SEC is hesitant about Circle's SPAC. However, by the end of 2023, things were making progress: with bipartisan support, Congress introduced a Payment Stablecoin Clarity Act. By 2025, the climate has changed – the new inaugural term said it would take a more supportive approach to cryptocurrency, with the new SEC chairman nominee pledged to adopt a “rational” regulatory stance. This more supportive tone at the federal level bodes well for USDC as it reduces regulatory tail risks.

Global regulator: Circle is also actively involved in business outside the United States. It has applied for a license in major jurisdictions – for example, Circle Singapore obtained a major payment agency license in 2023, allowing it to provide digital payment token services under the supervision of the Monetary Authority of Singapore. In Europe, Circle became the first stablecoin issuer approved under EU MiCA regulations in 2024. MiCA (Crypto Asset Market) provides a pan-European framework for stablecoins, and Circle premieres its standards (including capital, liquidity and disclosure requirements). Circle also registered as a Digital Asset Service Provider (DASP) in France in 2023, preparing for the expansion of euro-denominated stablecoins. These moves mean that USDC will become one of the few fully compliant stablecoins in the United States and the European Union, simplifying adoption of traditional institutions. Crcle is effectively setting a benchmark for stablecoin issuers' regulatory compliance, which could become a moat for competition.

International Cooperation: Circle aligns with institutions such as the Financial Stability Council (FSB) and cooperates with central banks on how stablecoins coexist with future central bank digital currencies (CBDCs). While some (for example) ban private stablecoins, others are accepting regulated stablecoins—such as Japan’s new stablecoin law or the UK’s proposal to treat stablecoins as electronic currency forms. Circle's transparency could make USDC one of the few private stablecoins that regulators are satisfied with. It is worth noting that Circle announced plans at the end of 2022 to seek federal bank charter to become a digital currency bank, although it has suspended the plan, awaiting clearer legislation. The company’s long-standing goal is to become a fully regulated, fully reserve bank entity in the digital age, reflecting its strategy within the regulatory framework rather than against the regulatory framework.

Financial and Capital Market OverviewCircle has raised a large amount of private capital in its development process, growing from a venture-backed startup to a multi-billion dollar business. Key financing milestones include:

2013–2016: Series A to Series D financing of approximately $135 million, with investors including well-known investors such as Accel, General Catalyst and Goldman Sachs. Goldman’s participation in 2015 was seen as an endorsement of Circle’s attitude toward Bitcoin.

May 2018: A US$110 million Series E funding led by Bitmain (a cryptocurrency mining giant), with a valuation of nearly US$3 billion. This round of financing is explicitly aimed at creating the USDC and CENTRE stablecoin framework.

End of 2019: Circle sold its crowdfunding division and raised some strategic capital (such as $25 million from the Digital Currency Group, which is also involved in collaborating on launching Circle’s earnings products).

July 2021: Announced a merger with SPAC Concord Acquisition Corp, initially valuing Circle at $4.5 billion. In February 2022, as USDC growth far exceeded expectations, the transaction price was modified to value Circle at $9 billion. This means that enterprise value will increase significantly due to USDC's success in 2021.

April 2022: $400 million financing round (a private placement conducted simultaneously with the SPAC process), with investors including BlackRock and Fidelity. This round of funding (ends in the second quarter of 2022) consolidates a $9 billion valuation and brings strategic capital and partnerships (as mentioned earlier, BlackRock becomes a reserve asset manager).

End of 2022: SPAC transaction failed to be completed (end in December 2022), Circle was privatized. Despite the setbacks, Circle had already received a sum of funds from its recent financing at the time and continued to operate strongly. By the end of 2022, some reports set Circle’s implicit valuation in the secondary market at around $8-9 billion, despite adverse open market conditions.

2023: No major public financing rounds were announced; however, in August 2023, Coinbase acquired Circle's equity in the process of disbanding Centre Consortium, resulting in a significant all-weight restructuring. Coinbase’s shareholding size has not been disclosed but is described as a minority stake. The deal may involve little or no cash, but rather an income-sharing arrangement (Coinbase receives 50% of USDC reserve revenue) in exchange for equity. This shows the implicit valuation of Circle, but the specific numbers remain confidential. It is worth noting that Circle's latest SEC filing lists Accel, General Catalyst, Breyer Capital, IDG and Oak Investment as shareholders in the top 5% of IPOs, indicating that these early VC backers still hold a large stake.

Circle is currently preparing for an IPO in 2025, and it has been reported that the company is targeting a valuation of between $4 billion and $5 billion. This is about half of the SPAC peak of $9 billion, reflecting the sluggish and expected readjustment in the crypto market in 2022-2023. However, this is still a high valuation for a fintech company with basically only one major product (USDC). Circle has hired major banks (JP Morgan and Citigroup) as IPOsThe lead underwriter shows confidence that institutional investors will support the issuance.

USDC reserve composition The advantage of USDC is its high-quality, transparent reserves, which are crucial to the financial situation of Circle. Each USDC token is backed by a reserve of equivalent USD held by Circle. As of April 2025, these reserves were conservative and highly liquid:About 80% or more of the funds were invested in the Circle Reserve Fund (USDXX), a SEC-registered money market fund managed by BlackRock. The fund mainly invests in short-term U.S. Treasury bills, overnight Treasury bond-backed repurchase agreements and cash, with a total of more than $53.5 billion, very close to USDC circulation. BlackRock’s daily disclosures ensure market-leading transparency, while competitors such as Tether provide only quarterly summary.

About 20% or less of cash is stored in multiple banking partners (such as Bank of New York Mellon, Customers Bank, Cross River Bank), minimizing exposure. After the acquisition of Silicon Valley Bank, Circle began weekly disclosure of bank holdings, enhancing liquidity and security through the automatic coin/redemption capabilities of Cross River Bank and Bank of New York Mellon.

Circle further improves credibility through weekly updates to reserves and Deloitte’s monthly third-party proof, confirming that reserves always reach or exceed the USDC in circulation. This rigorous report sets Circle apart by ensuring its reserves are essentially risk-free assets (short-term U.S. debt and cash), thus minimizing credit and interest rate risks.

Circle Production ProductsCircle briefly launched Circle Yield, an institutional USDC lending program launched in 2020 in partnership with Genesis Global Capital to facilitate over-mortgage loans. During the crypto credit crisis in 2022, Genesis stopped withdrawing money (affected by Three Arrows and FTX), prompting Circle to quickly shut down Yield. At the time, Circle had little exposure to Genesis—only $2.6 million in excess mortgage—and it took the initiative to turn yield rates before Genesis collapsed.Reduced to 0%. By early 2023, unlike programs like Gemini Earn, Circle Yield ended without significant losses. Circle has since stressed that USDC reserves remain liquid and hold mainly bonds, reflecting its prudent approach. Circle now mainly earns income from low-risk interest income rather than credit activities.

Profit modelCircle's revenue is currently mainly derived from interest generated by USDC reserves. It holds billions of dollars in short-term U.S. Treasury bonds and USDC-backed bank deposits, generating substantial interest income – $1.68 billion in 2024, up from $1.45 billion in 2023. At a 4% yield, about $40 billion, and interest alone can reach about $1.6 billion per year. Under the 2023 agreement, Coinbase will receive 50% interest income, meaning that Circle reported revenues take into account this share arrangement.

Transaction and API fees (from USDC Issues, Institutional Services, and Payments APIs) offer diversity and potential growth, while trivial. Revenue from transactions and subsidiaries (Poloniex, SeedInvest) in the past has now stopped, and Circle's focus has narrowed to a wholesale banking model that relies on interest income.

Circle recently turned a profit, reporting net income of $268 million in 2023 and $156 million in 2024, with a decline in profit reflecting higher operating costs and revenue sharing at Coinbase. This highlights Circle’s reliance on interest rates – higher rates produce substantial profits, but returning to low rates can have a significant impact on financial performance, a crucial factor for investors.

Recent financial performanceCircle Income Distribution (million USD)Circle's financial position (disclosed in its IPO documents) over the past two years is quite strong:

2023: Revenue $1.45 billion and net income $268 million, thanks to substantial interest income for the full year of the first year and reduced revenue sharing costs with Coinbase (new transactions began in the fourth quarter). One-time benefits or reduced expenses may occur.

2024: Revenue grew to $1.68 billion, but net income fell to $156 million due to increased costs (growth investments, public company preparations, compliance, ecosystem rewards, and interest that may be paid to USDC holders). However, profitability verifies the feasibility of the stablecoin business model.

Balance sheet: By the end of 2024, large amounts of cash reserves and shareholder equity will exceed $1 billion. Liabilities are linked to USDC reserves (investment, not traditional debt), similar to money market fund management.

IPO details (2025):

Estimated financing is approximately US$750 million and valuation is approximately US$5 billion (about 15% of the public holdings).

Funds used to support corporate growth, geographical expansion, research and development (such as EURC stablecoins), acquisitions, and meet potential regulatory capital requirements.

Underators: JPMorgan Chase, Citigroup; the New York Stock Exchange stock code is expected to be "CRCL", and the IPO is expected to be held in the second or third quarter of 2025.

Value and Comparability:

Circle has a market capitalization of $5 billion, equivalent to 30 times earnings and 3 times revenues—just reasonable for fintech growth, with volatility below Coinbase (valuation is approximately $50-60 billion, but revenues are less predictable). The market value of similar fintech companies PayPal is 4 times sales and less than 20 times revenue; the market value of bank/money fund managers is usually lower.

Market sentiment:

Circle's IPO tests investors' interest in crypto infrastructure after the 2022 bear market. Due to the recovery of the crypto market, the growth of stablecoins, and the Circle profitability, investors are cautiously optimistic.

Risk: Regulatory uncertainty, competition, dependence on interest rates.

Pros: a rigorous approach (traditional IPO and SPAC), two-year audit financial position, transparency highlighted by CEO Jeremy Allaire.

Governance and Administrative LeadershipCircle is led by co-founder and CEO Jeremy Allaire, an experienced entrepreneur known for its founding of Allaire Corp (ColdFusion platform) and Brightcove (2012 IPO). He positioned Circle as an essential “Internet currency” infrastructure, emphasizing regulatory dialogue, compliance and transparency. Co-founder Sean Neville, former president and co-CEO, withdrew from operations around 2019, but remains an independent director and a key shareholder.

The wider executive team includes experienced professionals from the fintech and traditional finance:

Jeremy Fox-Geen – Chief Financial Officer (CFO): Joined Circle from the fintech industry in 2021. He oversaw Circle's financial strategy through the rapid development of USDC and prepared the company for listing. He often talks about Circle’s path to listing and financial resilience.

Dante Disparte – Chief Strategy Officer and Global Head: Disparte is responsible for Circle's cooperation with countries and regulators around the world. He is a highly respected figure in the Washington, D.C. circle and played a key role in shaping Circle’s global strategy, such as navigating the EU’s MiCA, obtaining overseas licenses. He often expresses Circle's view on risk management.

Mandeep Walia – Chief Compliance Officer (CCO): Circle’s Compliance Director (hired from PayPal) ensures Circle’s license in multiple jurisdictions and leads programs such as sanctions compliance.

Product and Engineering Director: Circle's product line (such as CircleThe growth of accounts, APIs and cross-chain protocols) is led by Joao Reginatto, vice president of product and Fan Li, CTO (formerly head of technology at Tencent and Google). They oversee USDC’s technology integration across blockchains and the development of new products (including the digital euro EURC that may be issued by Circle).

Boards make up the board of directors of Circle consists of founders, investors and independents:Jeremy Allaire (Chairman) – Founder and Management Speaker.

Sean Neville - Co-founder, Continuity.

Investors (>5%) are represented by:

Jim Breyer - CEO of Breyer Capital, an early-stage investor at Facebook; leads the Series A financing with deep technical expertise.

David Orfao– General Catalyst Partner with operational experience and has served as a board member since 2013.

IDG Capital (early Asian expansion) and Oak HC/FT (fintech experience, investment in 2020) may have board members.

Coinbase, despite holding 2023 shares, clearly rejected the board seat, leaving control to management and traditional investors. After the IPO, more independent directors (regulatory/banking veterans) are expected to raise governance standards.

Governance PracticeCircle said that listing will strengthen its governance. The company has operated like a public company, providing proof monthly and filing documents with the Securities and Exchange Commission. As a public company, Circle will use the Independent Audit Committee, the formal SEC report (10-K, 10-Q) and Sarbanes-Oxley Act controls to enhance transparency. Allaire describes IPO as an extension of Circle’s transparency philosophy—emphasizing governance as a priority.

A key area is risk management. Circle manages tens of billions of dollars in assets, so its risk committee (on the board of directors or management) is crucial. Ensuring liquidity for USDC redemption is the primary concern. Cash buffering and diversified banking partners, etc., have proven to be effective during the SVB crisis. As a potential systemic stablecoin issuer, Circle's governance includes coordination with regulators, especially if it seeks a banking license or adapts to stablecoin regulation.

Ownership (before the IPO and after the IPO):

Pre-listing: Ownership is concentrated in the hands of early stage venture capital firms and management. Companies with ≥5% stake include Accel, General Catalyst, Breyer Capital, IDG, Oak HC/FT. Allaire may hold about 5-10% of the shares, and Sean Neville has similar holdings. Coinbase's shares are "very small" (about 5% or less) and may be related to future revenue sharing. BlackRock and Fidelity didn’t make it to the 5% list – which suggests they hold about 2-3% of the shares, possibly through convertible notes or after investment.

Assuming a valuation of approximately $4-5 billion, a $750 million financing would dilute approximately 15% of the equity of the pre-IPO holders. Capital Stand Estimates: Accel and General Catalyst are about 15%, Allaire is about 7%, Breyer, IDG, Oak are about 5%, Coinbase is about 4%, the others are about 24%, and new public holders are about 15%. Circle may also retain about 10-15% for employee equity incentives, helping retain fintech/banking talent.

After listing: Public investors will hold about 15% of the shares, but this proportion may rise if insiders sell secondary shares. Long-term venture capitalists may take this opportunity to make a profit, but locking up the agreement will delay sales. There is no plan to adopt a dual equity structure – Circle will adopt a single equity structure (1 share = 1 vote). Initially, insiders + venture capitalists will still control about 80-85% of the shares, but this ratio will dilute over time. Venture capitalists may allocate shares to LPs after the lockdown period, thereby increasing public holdings.

Strategic equity (such as from a bank or the Internet) has not been announced, but may occur. Board of Directors is still under managementMainly venture capital, Breyer and Orfao are expected to remain in office during the IPO. Coinbase may coordinate closely with Circle, but will not affect governance through board seats.

Challenges, setbacks and regulatory tensionsTermination of SPAC transactions (2021-2022)

Circle plans to go public through a merger with Concord Acquisition Corp, with a valuation of $4.5 billion (later rising to $9 billion due to USDC growth). The deal failed in December 2022 due to crypto market turmoil (Terra, Celsius, FTX) and SEC delays. CEO Allaire mentioned regulatory timing, not fundamentals, noting that Circle has a strong capital position after raising $400 million.

IPO Delays and Market Conditions

After the SPAC bankruptcy, Circle carefully sought a traditional IPO in the tough 2023 market. USDC's market value fell from $50 billion to more than $30 billion, with regulatory pressures after the Fed rate hike coupled with FTX increased resistance. As the situation improved in 2024, Circle filed the S-1 document in April 2025—nearly two years late. Nevertheless, it maintains operations, morale and key partnerships, including partnerships with Coinbase.

Regulation tension

Circle's role as a stablecoin issuer brings complex oversight:

SEC Review: USDC was marked as payment tokens, not securities, but lack of clarity delayed SPAC approval. 2025 legislation could shift oversight to the Fed or OCC.

Banking industry concerns: The March 2023 SVB crisis exposed regulatory concerns about stablecoin banking. Circle’s response is to diversify partners and seek banking licenses.

Global News: Regulators Closed in New York PAfter axos' BUSD, Circle dissolved the Centre consortium and took full control of the USDC for easier governance.

Market competition: Circle improves transparency between USDC and Tether, maintains real-time reserve reporting and risk control.

Transparency and Audit

Circle instead updates reserves and hires Deloitte for a full audit before the IPO. Its real-time reporting during the Silicon Valley banking crisis helped build trust. Quarterly disclosures after IPO are expected to further increase transparency.

Cryptocurrency Market Turbulence (2023-24)

Big stressful events facing Circle:

Terra Collapse (May 2022): Focus on the fully reserved model of USDC.

FTX Implosion (November 2022): Received only $2.6 million in exposure through Genesis.

SVB Crisis (March 2023): Quickly manage US$3.3 billion of exposure and maintain its linkage to USDC after a US$6 billion redemption.

Slowing market: Despite the decline in transaction volume, increased interest income and cost control have kept revenue stable—no layoffs.

Reputation and competitive pressure

Binance Turns: Binance's turn to BUSD in 2022 hit USDC's market share, although regulatory pressure on BUSD in 2023 has eased the impact.

Technology and Compliance: Despite the challenges of cross-blockchain scaling and criticism from privacy advocates, Circle maintains strong standards for smart contract security and compliance.

Key indicators and market signals worth paying attention toAs Circle transforms into an open market, investors should monitor several key indicators to assess USDC adoption, stability and Circle's financial status. Tracking the total supply (market cap) and monthly net issuance or redemption volumes can provide insight into adoption trends or declines in user confidence. Investors should compare USDC growth with the broader stablecoin market.

Monitoring the on-chain transaction speed and transaction volume can reveal the degree of USDC usage activity. The faster the transaction speed, the higher the frequency of usage. Comparing USDC’s speed with competitors like USDT can highlight its commercial appeal.

Investors should carefully study the reserve composition between cash and U.S. Treasury bonds, as this has a significant impact on Circle's interest income. It is crucial to observe the 7-day yield (USDXX) provided by BlackRock and monitor interest income per $1 billion USD (currently about $50 million per year with a yield of 5%). In addition, reserve periods should be kept short-term to minimize risks. Circle’s potential income from management fees through the Circle Reserve Fund is another area worthy of attention.

Transparency indicators (such as monthly proof reports detailing the support ratio, reserve composition, bank partners and auditor statements) are key indicators for measuring financial stability. Adoption expansion can be measured by holding a unique address for USDC, enterprise integration, and important off-chain use cases.

The competitive landscape, including changes in market share with major stablecoins such as Tether (USDT) and new entrants such as PayPal's PYUSD, provides an important background for Circle's positioning.

Lastly, Circle's quarterly financial report will reveal revenue growth, diversification, cost management (optional expenses relative to revenue), profit margins and cash reserves. After listing, valuation indicators compared to peers such as Coinbase, PayPal and traditional fintech companies will become an important benchmark.

ConclusionEaring 2025, Circle is about to achieve its goal set more than a decade ago - integrating crypto dollar (USDC) into the global financial system under the supervision of open market investors. To date, the company's basic choices (full reserve support, regulatory participation, partner model) have proven wise to make USDC has been widely adopted and has become a sustainable revenue engine. However, the path to the future requires Circle to deal with competitive pressures, regulatory evolution and market volatility with the same caution, as Circle showed in overcoming past setbacks. By monitoring the key metrics and signals outlined above, institutional investors can stay informed of Circle's health and progress at all times. Circle’s IPO is more than just a liquidity event; it will serve as a barometer of maturity in the wider crypto industry, providing a window into how crypto-native companies perform when meeting traditional financial standards. With USDC as its core, Circle’s story in 2025 is the story of the fusion of fintech and cryptocurrency – its successful public debut may mark an important step forward in stablecoins from the edge of finance to mainstream.