8 hours ago

5,864

Source: CICC's finishing touch

Under the impact of "reciprocal tariffs", the global trade system has ushered in a century of changes, and global asset prices have also fluctuated significantly. Although this tariff increase will inevitably bring challenges to the economy, we believe that compared with 2018 or the past three years, the stock market has more favorable conditions, including changes in geopolitical narratives and technological narratives, as well as the valuation advantages of the assets themselves, and space for macro efforts. Overall, we believe that assets are resilient in the short term compared to global stock markets, and the medium-term opportunities outweigh the risks. If properly handled, the market risk premium is expected to continue to improve, and "asset revaluation" is still in progress. At the allocation level, short-term allocation is mainly stable, and stocks with low dividends may be relatively dominant. The consumption and investment sectors that benefit from domestic demand also have trading opportunities in the short term. In the medium term, the AI industry is still an important main line, and the pullback will usher in an opportunity to make plans. And with the steady growth, further increase in investment and rebounding of effective demand, the consumer sector is expected to gradually usher in a trend.

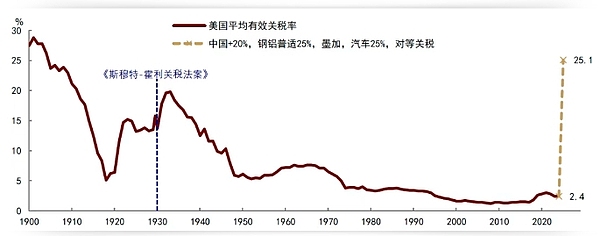

Under the impact of "reciprocal tariffs", the global trade system has ushered in a century of changes. On April 2, US time, Trump's "reciprocal tariffs" were implemented, and the comprehensive "carpet" tariffs and country-style tariffs with "one country, one tax rate" were superimposed, covering more than 60 economies. The scope and extent of the tariffs imposed this time are much higher than previous market expectations. If the tariffs are fully implemented, the effective tariff rate in the United States will exceed the US tariff level after the implementation of the Smut-Holly Tariff Act in 1930 (Figure 1). This means that the global trade system formed in the past few decades will be significantly affected, with far-reaching impact on the global economy in the medium and long term, and global asset prices will also fluctuate greatly.

Figure 1: The effective tariff rate in the United States will rise sharply

Note: 1900-1918 and 2024 are the U.S. fiscal years, 1919-2023 are the calendar years, and 2025 are the CICC Macro team's estimates.

Source: USITC, Wind, CICC Research Department

Global assets fluctuate significantly after the tariff impact, and assets show resilienceGlobal assets fluctuate significantly, and the aftermath is uncertain. After Trump announced an "reciprocal tariff" that exceeded expectations on April 2, US time, recession transactions heated up, US bonds rose sharply, global risky assets suffered a heavy blow, US stocks fell the most in major economies around the world, Nasdaq/S&P 500 fell sharply for two consecutive days, with a cumulative decline of 11.4%/10.5%. VIX hit the highest since the epidemic in 2020, and European and Asia-Pacific stock markets were also affected and significantly rebounded; commodity prices also fell sharply, with London copper and Brent crude oil falling by more than 10% in two days, respectivelyWith new lows in 1 year and in the past three years, gold also saw profit rebates after expected cashing out after a sharp rise in the early stage.

Characteristics of this round of asset fluctuation: US assets weaken, assets show resilience. We have noticed two differences in this round of global asset fluctuations in the past: First, the United States has imposed tariffs on other economies in the past, and funds are usually withdrawn from other economies. US stocks perform better than the world, but this time the United States imposed tariffs on the world, and the US stock market led the decline in the world, and the US dollar also experienced a significant decline, which may reflect multiple meanings. First, as a deficit country, the sharp increase in tariffs is a major supply shock for the United States, and the risk of "stagflation" has increased; secondly, the increase in tariffs exceeds most market expectations before, and the uncertainty of the future interpretation path is high, which is an uncertain impact; finally, the extremely low risk premium of US stocks previously implies too optimistic expectations, and tariffs have a great impact on the basic prospects of the United States, the global trade system, and even the rules of goods and capital flows, so this is also a risk premium impact. Moreover, the decline in the US dollar and the leading decline in US stocks may also reflect that global funds choose to flow out of the US market. The second difference is the resilience of assets. After the United States announced "peer tariffs", the Shanghai Composite Index/Shanghai and Shenzhen 300 fluctuated slightly, with a drop of only -0.2%/-0.6%, respectively, which was significantly lower than other major markets; and from the performance from the beginning of the year to the present, the stock market, especially the Hang Seng State-owned Enterprise Index, led the world in terms of performance, and the US stock market fell the most (Figure 2). This may mean that under the unprecedented tariff impact, new changes may occur in the global valuation system, and global funds will be re-arranged based on the progress of geopolitical revaluation.

Chapter 2: Performance of major global assets since 2025: Stocks are resilient, and US stocks lead the decline worldwide

Source: Wind, Research Department of CICC; Note: As of April 3

The impact of this tariff has exceeded 2018-2019, and the global economy is still facing great uncertainty.This US tariff increase is not only targeted, but is generally affected worldwide. The characteristic of this US tariff is that it is not only targeted, but involves major and regions around the world. In addition to the United States that will impose a basic 10% carpet-style tariff on all imported goods, some and regions will face higher tax rates. At present, the president's executive order has not yet released the specific appendix details on the White House official website. However, according to Trump's statement, economies with higher reciprocal tax rates include the EU (20%), Japan (24%), South Korea (25%), mainland China, Hong Kong and Macao (34%), Taiwan (32%), India (26%), Thailand (36%) and Vietnam (46%). CICC Macro team estimates that if the above tariffs are fully implemented, the effective tariff rate in the United States will rise sharply by 22.7 percentage points from 2.4% in 2024.To 25.1%, it will also exceed the US tariff level after the implementation of the Smut-Holly Tariff Act of 1930.

Tariff uncertainty is still high, and short-term fluctuations in asset prices are unlikely to subside soon. First of all, the reciprocal tariffs have a wide range and a large range. We believe that they will have a significant impact on the United States and even the global economy. It is also crucial to see how countries will respond after the tariffs are implemented. For example, on April 4, Beijing time, the Tariff Commission of the Court announced that it would impose a 34% tariff on all imported goods originating in the United States from April 10. The Ministry of Commerce announced that 16 U.S. entities will be included in the export control list and 11 U.S. companies will be included in the list of unreliable entities. This means that trade frictions have further escalated, putting downward pressure on the global economy. Secondly, after the reciprocal tariffs, we also need to pay attention to whether additional tariffs are imposed on semiconductors, medical products, wood, copper and other commodities, as well as Mexico and Canada, which have received tariff exemptions this time, will still have variables in the future. Finally, the length of time the reciprocal tariffs last and whether there may be variables through negotiations in the future, which means that short-term global asset price fluctuations will be difficult to calm down soon.

Tariffs have different meanings for China-US and global economies. The impact of tariffs on trade surplus countries and deficit countries varies. As a deficit country, tariffs on the United States mean that companies and residents will face rising costs and inflationary pressures. Moreover, tariffs are essentially increasing taxes, and companies and consumers bear costs. The effect is equivalent to fiscal tightening and the economy is facing downward pressure. Therefore, we believe that the United States is facing "stagflation" pressure and the Federal Reserve will be in a dilemma. CICC Macro team estimates that based on the previous tariffs and adding reciprocal tariffs may push up US PCE inflation by 1.9 percentage points, increase US fiscal revenue by 737.4 billion US dollars, and reduce US real GDP growth by 1.3 percentage points. As a surplus country, the imposition of tariffs has caused pressure on foreign demand, mainly facing the problem of insufficient demand, and the economy may face certain challenges. However, the response direction is clearer, and focusing on supporting the expansion of domestic demand has become a relatively intuitive option. For other economies around the world, such a large-scale tariff shock will itself damage global demand, especially for small export-oriented economies such as Southeast Asia, which will have a significantly greater impact. Moreover, if US economic growth declines or even declines, it will inevitably face greater challenges for other economies around the world.

The market environment is relatively favorable, and assets are expected to be relatively resilient. "Asset revaluation" is still in progress.Combining the experience of trade frictions from 2018 to 2019, market performance is determined by economic fundamentals and response in the medium term. In 2018, the United States began to impose tariffs on China, coupled with financial deleveraging, external impacts and internal contraction, A-shares and Hong Kong stocks performed weakly overall, but in the subsequent 2019, the scope of tariffs imposed by the United States expanded and the tax rate increased significantly, and the market instead regained its upward trend from 2019 to 2020 (Figures 3 and 4). The core reason is that the tight credit of deleveraging ends in 2019, and the macro turns to loose and supports new onesA round of credit expansion and the depreciation of the RMB exchange rate have also hedged the impact of tariffs to a certain extent, and economic fundamentals have entered a new recovery cycle. And structurally, although industries with a high proportion of exports such as home appliances, light industry, electronics, and machinery are facing pressure after the introduction of trade, new industrial trends such as 5G communications are rapidly penetrating, domestic substitution of semiconductors accelerated, and the rise of new energy vehicles have injected new vitality into the economy.

Chapter 3: A-share market trends and export performance to the United States before and after the Trump trade was released from 2017 to 2019

Source: Wind, CICC Research Department

Chapter 4: The rise and fall of various A-share industries after Trump trade from 2017 to 2019

Source: Wind, CICC Research Department

Objectively speaking, although this increase in tariffs is inevitably challenging the economy, we believe that compared with 2018 or the past three years, The stock market has many favorable conditions, including changes in geopolitical narratives and technological narratives, as well as the valuation advantages of the assets themselves, and space for macro efforts. Overall, we believe that the stock market is still relatively resilient in the medium and short term, and when "asset revaluation" is still in progress, the specific logic is as follows:

1) Geographical narrative changes, global capital is facing re-layout. In the past two years, the AI revolution, big fiscal and global capital inflows have formed a positive cycle, pushing up the U.S. stock market. At the same time, the narrative of "anti-globalization" began to become popular after the Russian-Ukrainian conflict, and major global economies were in camp, becoming the main reason for the global capital outflow market. Judging from the latest data, the market's share of global active funds' holdings has dropped from 14.6% at the beginning of 2021 to the lowest 5% in 2024, and has been under-allocated by about 1 percentage point compared to passive funds for two consecutive years. From the perspective of shareholding shareholding, the free circulation market value of overseas funds in A-shares has dropped from a high of 10% in 2021 to around 7.5% (Figures 5 and 6). However, after Trump was elected, the recent imposition of large tariffs, strengthening the deportation of illegal immigrants, and DOGE's fiscal cuts have all brought a tightening effect on the US economy (Figure 7). The US economy is facing the risk of stagflation, and the uncertainty index of the US and global economics has risen sharply, hitting a new high since 2021 (Figure 9). Trump's portfolio has triggered a global re-examination of the overly optimistic outlook of the US economy. Faced with the current "certain uncertainty" of the United States, global investors are forced to start a new round of "geopolitical revaluation." This round of tariff imposition of US dollar did not rise but fell. This abnormality may also reflect that global funds no longer regard the US dollar as a safe-haven currency, and the pressure on funds to flow out of the US market has increased.Recently, other non-US markets have received inflows of funds. Whether foreign capital has re-allocated money or not depends on the repair of fundamentals, but it also means that the market's potential for foreign capital to inflows is gradually emerging. Judging from the low correlation between the Chinese and US stock markets in recent years, assets have risk-diversified value for global funds (Figure 8).

Chart 5: Since 2022, overseas active funds have continued to under-allocate assets, and are currently under-allocated by 1.2 percentage points

Source: EPFR, CICC Research Department

Chart 6: The shareholding of foreign capital in A-shares has dropped from 10% in 2021 to 7.5%

Source: Wind, CICC Research Department

Figure 7: Tariffs since Trump took office. A list of

Source: White House, CICC Research Department

Source: White House, CICC Research Department

Source: Bloomberg, Haver, CICC Research Department

Source: U.S. and global economy, uncertainty index has risen sharply

Source: Bloomberg, Haver, CICC Research Department

Source: Source: Wind, CICC Research Department

Classification 10: DeepSeek has become the fastest-growing app in history with its advantages of open source, low cost and high efficiency

Source: Wind, CICC Research Department

Classification 11: The comprehensive level of AI development is second only to the United States12: The added value of manufacturing and global share of the world

Source: IMF, WB, CICC Research Institute, CICC Research Department

Source: UN Comtrade, CICC Research Department

Source: UN Comtrade, CICC Research Department

Source: IMF, WB, CICC Research Institute, CICC Research Department

Source: IMF, WB, CICC Research Institute, CICC Research Department

Source: Center;">Source: UN Comtrade, CICC Research Department

3) A-shares and Hong Kong stocks are at historical lows and are attractive, and the valuation of US stocks implies too optimistic expectations. As of April 4, the dynamic price-to-earnings ratio of the Shanghai and Shenzhen 300 Index was only 11.3 times, which is still significantly lower than the historical average (the dynamic valuation average of the index since 2005 is 12.6 times). The current valuation of A-shares has been repaired compared with the extreme position at the end of September last year, but there is still room for further upward revision. The dynamic valuation of the Hang Seng State-owned Enterprise Index is less than 10 times, which is lower than the Shanghai and Shenzhen 300, and is also lower than its historical average. From the perspective of equity risk premium, the equity risk premium of Shanghai and Shenzhen 300 has been repaired from the highest 7% in the past 10 years after "924", rebounding to 6.5% at the beginning of the year (1 times the standard deviation of the historical average). The equity risk premium of the Hang Seng Index from the perspective of domestic capital (using the 10-year treasury bond yield as a risk-free interest rate) is as high as 10%, significantly higher than the previous center. On the contrary, the equity risk premium of the S&P 500 was once less than 0 at the beginning of the year, which means that the market believes that stock yields do not require additional risk premiums compared to Treasury bond yields, which reflects extremely optimistic expectations and is in a clear contrast with the higher risk premiums of stocks (Figure 14). At the structural level, the market is reevaluating its innovative potential in AI, and the valuation of technology leaders still needs to match the development trend of AI. Overall, we believe that global economic development expectations are changing, and the valuation system will inevitably face reshaping. The current stock valuation is at a historical low, while the valuation of US stocks still implies a lot of optimistic expectations. In the process of re-allocation of global funds, valuation is also relatively beneficial to the stock market.

Chapter 14: Equity risk premiums in A-shares and US stocks converge from extreme levels

Source: Bloomberg, CICC Research Department

Chart 15: Technology giants have severely discounted compared to US stocks, and have narrowed recently

Note: Tiktok does not include version Tiktok Source: AI product list aicpb.com, CICC Research Department

Chart 16: Technology stocks have previously insufficient pricing of AI prospects

Note: Due to industry classification reasons, US technology stocks use Magnificent 7. The 10 technology giants (Tencent, Alibaba, Meituan, Baidu, SMIC, Xiaomi Group, JD.com, BYD shares, Geely Auto, NetEase), and the rest of the economies use MSCI information technology; as of December 31, 2024 Source: FactSet, Bloomberg, CICC Research Department

4) Counter-cyclical space is large, and if the problem of insufficient demand can be effectively dealt with, it will have positive support for asset prices. The impact of tariffs on countries with trade surplus and deficit countries has different effects. The United States is facing pressure of "stagflation" and the environment is further under pressure due to insufficient demand. The macro effect of responding to "stagflation" and insufficient demand is different. The "stagflation" environment in the United States means a slowdown in growth or even a recession, and may be in a dilemma. However, in dealing with insufficient effective demand, the direction is clearer. Moreover, some investors compared the impact of trade frictions on the global economy with the 1930s, when mutual retaliation and mutual tariffs were considered one of the important reasons for the long-term economic depression after the US stock market crash in 1929. But we think there is an important difference now and in the 1930s. The current macro framework has undergone time tests. As long as my country's macro can effectively deal with the problem of insufficient demand, there is no need to be pessimistic about the performance of risky assets. On the one hand, after experiencing previous trade frictions, we expect that my country will respond more in this round, and its dependence on US exports is lower than in the past. Moreover, in the past three years, my country has continued to strengthen its efforts to manage real estate and local debt issues, which has also created better conditions for the current space. On the other hand, my country's macro-level has undergone a positive change. After 924 last year, the market has seen the execution of the decision-making level more actively. The work report of the Two Sessions also clearly stated that "it is necessary to be issued and implemented earlier, rather than late, and to compete with various uncertainties." We believe that external risks exceed expectations will prompt more counter-cyclical efforts. Moreover, in the Central Economic Work Conference and this year's work report at the end of last year, "vigorously boosting consumption, improving investment efficiency, and expanding demand in all aspects" was placed first in the work tasks in 2025. This means that our country's framework attaches more importance to the emphasis on supply to demand from the pastSeeking tilt. In the context of uncertainty in foreign demand, stabilizing domestic demand is expected to make further efforts, which will be the key to stabilizing the risk premium of my country's market itself.

The market is resilient in the short term, with medium-term opportunities greater than risks, and short-term allocation is mainly stable, and technology is still the main line in the medium term. Overall, the uncertainty of short-term tariffs and the contagiousness of global market fluctuations may bring volatility to assets but are expected to have a lower impact than other major markets. Assets are resilient in the short term compared to global stock markets. In the medium term, the transformation of geopolitical narratives and technological narratives improves market expectations, promotes global capital re-layout, and combines the market's valuation advantages, and has a large space for response and is expected to make active efforts. If properly handled, the market risk premium is expected to continue to improve, and the "asset revaluation" is still in progress. At the allocation level, in a short-term volatility environment, the allocation may be mainly stable, and stocks with low dividends may be relatively dominant, and the consumption and investment sectors that benefit from domestic demand also have trading opportunities. In the medium term, we recently released "How to judge the growth trend? 》, the medium-term trend of the growth industry depends on the industrial prosperity and profit cycle. DeepSeek's breakthrough provides conditions for the development of AI application scenarios. The current high prosperity of the AI industry may still be in the early stages. We believe that in the future, from computing power, cloud computing and other infrastructure to application links, it is still an important main line in the medium term, and the pullback will usher in layout opportunities. In the future, with steady growth, further increase in investment and rebounding of effective demand, the consumer sector is expected to gradually usher in a trend.

[1]https://www.whitehouse.gov/presidential-actions/2025/04/regulating-imports-with-a-reciprocal-tariff-to-rectify-trade-practices-that-contribute-to-large-and-persistent-

annual-united-states-goods-trade-deficits/

annual-united-states-goods-trade-deficits/

annual-united-states-goods-trade-deficits/

[2]https://www.cnbc.com/2025/04/02/trump-tariffs-live-updates.html

[3] "Trump's "reciprocal tariff" impact exceeds expectations", Liu Zhengning, Wen, Lin Yuxin

[4]https://baijiahao.baidu.com/s?id=1828524062501180073&wfr=spider&for=pc

[5]https://www.research.cicc.com/zh_CN/report?id=362692&entrance_source=ReportList

[6] "AI Economics" Chapter 1: "Artificial Intelligence toward a General Era", Zhou Zipeng, Li Na, Lu Qu, Liu Mengling

[7]https://www.gov.cn/yaowen/liebiao/202503/content_7013163.htm

[8]https://www.gov.cn/yaowen/liebiao/202412/content_6992607.htm