14 mins ago

1,251

Author: Aiying Aiying, pony; Source: AiYing Compliance

Yesterday, the TUSD-FDT incident exposed that in addition to the misappropriation of US$456 million in the trust, it was invested in high-risk projects such as manufacturing plants and mines; and FDUSD also chose FDT as the trustee, so the price was decoupled to US$0.87. It all started with Techteryx's lawsuit against First Digital Trust (FDT), but it affected far more than both parties - Hong Kong's regulatory loopholes were exposed. As a global financial center, Hong Kong's crypto ambitions are facing severe tests. I couldn't help but wonder: Why can such a huge amount of funds quietly get out of control in Hong Kong? What are the shortcomings of the regulatory system? This article will start from the full picture of the incident, analyze the root causes of the capital transfer, the truth of the TUSD audit, and the "loopholes" of Hong Kong's trust supervision, and some of our experience in serving customer cases.

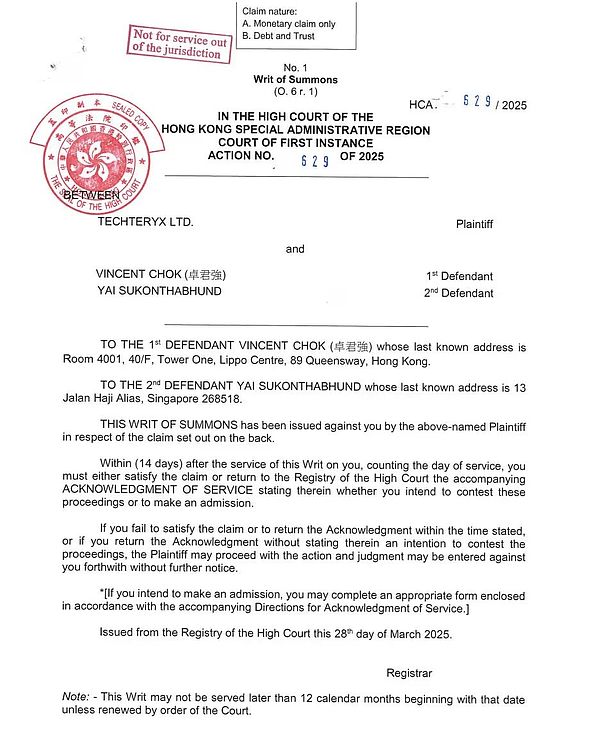

The cause of the incident is not complicated. Techteryx accused FDT of misappropriating TUSD's $456 million reserves and investing it in high-risk and low-liquid assets, such as manufacturing plants and mines, rather than holding cash or Treasury bonds as stablecoin practice. This directly led to the inability of users to redeem funds normally. Techteryx filed a lawsuit against FDT to the Hong Kong High Court, case number HCA 629/2025, accusing him of breach of trust liability.

The event fermented rapidly. Justin Sun jumped out and urgently injected $456 million in loans to try to stabilize TUSD, while publicly bombarding FDT "in fact, it has gone bankrupt." FDT is not willing to be outdone, insisting that it is just executing Techteryx's instructions, and also disclosed the ISIN number reserved by FDUSD, trying to prove solvency. However, the market is not buying it. FDUSD fell to $0.87 from April 2 to 3, 2025, and its market value evaporated by US$130 million. TUSD's market value also slipped from its high of $3.8 billion in 2023 to $494 million today, and investors' panic spread rapidly, even affecting Binance - it holds more than $2.2 billion in FDUSD.

When I saw this scene, my first reaction was that US$456 million is not a small amount. The misappropriation of such a large amount of funds could be delayed until the lawsuit was exposed, which was obviously not a simple management mistake. Behind the market shock, although Sun Yuchen's capital injection temporarily stopped bleeding, it could not hide its trust.rifts. As the site of the incident, Hong Kong's reputation as its crypto-center is also cast in shadow. Although the case is still under trial, the Rashomon incident will need to wait for the final judgment of the court to know the truth. However, the lack of supervision is the real fuse in terms of the specific use of trusts from my personal subjective judgment. The following are some core factors that I have summarized.

2. The root of capital transfer - the ambiguity of trust responsibility

What is the root of capital transfer? In my opinion, the biggest problem is the ambiguity of trust responsibility. Techteryx insisted that FDT arbitrarily invested $456 million in high-risk projects, deviating from the principle that stablecoin reserves should be kept at low risk. FDT refuted that it was just following the instructions of Director Techteryx and that the responsibility for misappropriation was not on its own. This shirking is confusing, but it also points to the fact that there are likely loopholes in the custody agreement between the two parties.

From the details, after Techteryx took over TUSD in 2020, it handed over the reserve fund to FDT, with a total amount of approximately US$501 million. FDT then transferred some of its funds to the Cayman Islands’ AriaCommodityFinance Fund and Dubai’s Aria DMCC, which deviated from the requirements of cash equivalents. But how much autonomy does FDT give in the agreement? Is FDT obligated to reject high-risk directives? These key questions seem to be answered. The ambiguity of the agreement makes both parties have different opinions and makes funds flow unregulated.

The deeper problem is governance failure. FDT obviously lacks real-time auditing, and Techteryx is not effectively supervised. The $456 million flowed to overseas entities, but it was unaware of it from 2022 to 2023, and it was not exposed until the redemption failed. FDT may be a risky investment chasing high-yield investment, and Techteryx's decision-making mistakes may not be related. But no matter who is right or wrong, this chaos stems from loose regulation.

Comparing with the US stablecoin management, the gap is clear at a glance. USDC's custody agreement clearly limits the types of reserve assets and monthly audits ensure compliance. Hong Kong has no similar constraints, and FDT is able to wander in the gray area. I think the ambiguity of trust responsibility is the source of this crisis, and the absence of regulation has led it to evolve from hidden dangers to reality.

3. The truth of TUSD audits - name but not reality. TUSD has always claimed that it has audit support, but this incident made me wonder: how useful are these audits? reviewHistorically, when TrueCoin launched TUSD in 2018, it partnered with the US accounting firm Cohen & Company to release a monthly certificate report showing that reserves matched circulation. After Techteryx took over in 2020, it also claimed that it would continue to maintain a transparent image in quarterly audits. But the actual situation is far from that simple.

These audits have three major problems. First of all, the range is too narrow. The report only verifies the account balance at a certain point in time, but does not check the flow of funds or the investment composition. FDT invested $456 million in mines and manufacturing plants, but this high-risk operation was not discovered, and the audit was obviously failing. Secondly, the frequency decreases. After 2023, the report becomes irregular, sometimes not updated for months, and the details become blurry. Third, the incident itself is ironclad evidence - no one noticed the misappropriation for many years. If the audit is really effective, how could Techteryx wait until the redemption failed to know? In contrast, the USDC in the United States accepts a monthly audit of Grant Thornton, and NYDFS forces asset details to disclose, with transparency above more than one order of magnitude.

Why can't TUSD work? I think there are several reasons: First, cost pressure, TUSD's market value fell from 3.8 billion to 494 million, and audit investment may shrink; second, Hong Kong's supervision is loose, unlike the United States' mandatory requirements; third, management is chaotic, and the custody replacement from PrimeTrust to FDT broke the supervision chain. The SEC fined TrueCoin $500,000 in 2023, also hinting that early audits may be in a state of moisture.

TUSD's "regular audit" is in name but not real and has become a decoration. Not only did it fail to stop the crisis, it also reduced the market's trust in Hong Kong.

4. The institutional "loopholes" of Hong Kong's trust supervision

The FDT incident made me realize that the problem is not only TUSD or FDT, but the shortcomings of Hong Kong's entire trust supervision system. Hong Kong's trust law follows British traditions and applies to heritage and family trusts, but fails to keep up with crypto assets. The ability of FDT to misappropriate funds in the gray area is a manifestation of this lag.

There are four specific defects.

First, regulations are absent. There are no special rules for stablecoins or crypto trusts, FDT'sThere is no clear constraint on the operation.

Secondly, there is insufficient transparency. The United States requires stablecoins to be audited and disclosed, but Hong Kong relies on corporate self-discipline. FDT misappropriation has not been discovered for many years, which shows the problem.

Third, cross-border powerlessness. Funds flow to the Cayman Islands and Dubai, and Hong Kong's supervision is out of reach, and litigation execution is also difficult.

Fourth, weak execution ability. HKMA and SFC have been busy attracting crypto innovation in recent years. The stablecoin discussion paper for 2022 has not been implemented so far, and regulatory details have not been released.

Compared with the United States, the United States has tightened rapidly due to the Terra and FTX incidents, and NYDFS's audit requires preventing problems before they happen. However, Hong Kong has taken the path of "development first and then governance". This strategy attracts companies in the short term, but poses hidden dangers in the long term. The FDT crisis is not accidental, but an inevitable result of the disconnection between traditional frameworks and encryption needs, so this incident is reasonable.

5. Our experience sharing

Aiying related articles: "Application and analysis of Hong Kong TCSP licenses and trust licenses in Web3 enterprises"

I think in the short term, the trust crisis may make Hong Kong's crypto attractive. But this does not mean that Hong Kong's trust system has completely failed - although the loopholes are there, the potential remains. As long as you work hard on details, Hong Kong can fully maintain its advantages in the Web3 track.

Hong Kong's trust supervision does have institutional shortcomings, such as the lack of special regulations and the lack of transparency. But I think this does not mean that Hong Kong Trust is unreliable. Every place has its own characteristics, and Hong Kong's flexibility is precisely the soil needed for Web3 development. Compared with the high regulation of the United States, Hong Kong has given the industry more room for trial and error. This loose environment is both a challenge and an opportunity. The key is how we can use this flexibility well instead of simply amplifying its shortcomings.

From a practical point of view, improvements can be more down-to-earth. First, legislation must be followed. For example, the "Crypto Trust Regulations" was issued to clarify the responsibilities of the custodian, such as limiting reserves can only be invested in cash or low-risk assets, to avoid out of control like FDT. Secondly, transparency must be grasped. Forced third-party audits every quarter are the beginning. When we helped customers set up trusts, we found that regular disclosure and clear asset reports can make investors feel at ease. Hong Kong might as well learn from it. Third, cross-border cooperation must be implemented. Connect with Cayman Islands and Singapore to fund tracking, Our experience shows that sorting out cross-border compliance requirements in advance can effectively reduce risks.

More importantly, even if the supervision is not yet perfect, the industry can take the initiative to make up for leaks. HKMA plans to launch a stablecoin framework by the end of 2025, but before that, we have figured out some solutions when serving our customers. For example, by establishing an internal supervision mechanism, ensure that the flow of funds is controllable; or optimize the audit process and discover hidden dangers in a timely manner. These methods prove that under the existing framework, the vulnerability is not unsolvable. Hong Kong's flexibility gives us room to implement - Web3 needs development, supervision takes time, and what we can do is to use meticulous design to minimize risks.

Our past experience in helping clients improve compliance tells me that a combination of flexibility and meticulous work is enough to meet challenges. In the future, supervision must be upgraded and the industry must work hard, so that Hong Kong can gain a foothold in the global crypto landscape.