4 mins ago

216

Author: Tanay Ved Source: Coin Metrics Translation: Shan Oppa, Golden Finance

Key points:•The total market value of the crypto market fell 19% in the first quarter of 2025 to $2.65 trillion. Bitcoin (BTC) fell 7%, while Ethereum (ETH) and Solana (SOL) fell more significantly due to risk aversion.

•The total supply of stablecoins exceeded $230 billion, with USDC and Ethereum becoming the main beneficiaries, while new entrants are stepping up their product launches to cope with the increasingly advanced stablecoin legislation.

•Ethereum's Layer-2 expansion strategy creates a short-term value gap and affects ETH performance. Expanding data block capacity, increasing L2 demand, and attracting high-value use cases such as tokenization and stablecoins to return to L1, may become a feasible path to restore value accumulation.

•Solana has carried out a critical SIMD upgrade to reshape validator incentives and destruction, while the cooling of memecoin activity highlights the need for a more sustainable usage model for the network.

In this special edition of the Network Status report, we have an in-depth analysis of the main developments, market performance and network activities that have had an impact on the digital asset industry in the first quarter of 2025 based on data.

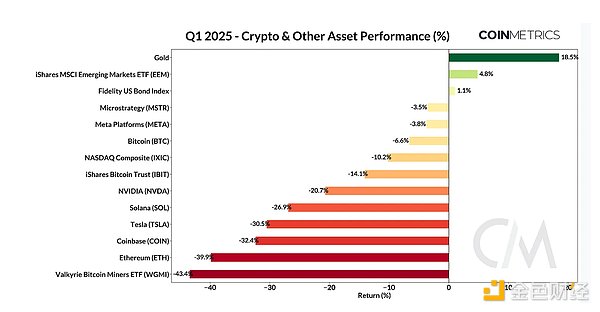

Market performance: Risk aversion sentiment dominatedIn the first quarter of 2025, macroeconomic pressure dragged down digital assets and traditional markets. Trade uncertainty, inflationary pressures and weak economic outlook have prompted investors to flock to safe-haven assets, especially gold, which have gained 18% year-to-date, exceeding all major asset classes. Meanwhile, risky assets including the Nasdaq Composite Index and the "Tech Seven" gave up on the gains before the election.

While there has been some positive momentum in the crypto industry, such as the SEC's withdrawal of major enforcement actions, the establishment of Bitcoin strategic reserves, and the growing interest in stablecoins and tokenization, market sentiment is still affected by Bybit's largest vulnerability attacks and memecoin speculation in history. Driven by these factors,The total market value of the Michigan market fell 19% to $2.65 trillion.

•Bitcoin (BTC): 7%

•Solana (SOL): 27%

•Ethereum (ETH): 39%

In terms of crypto stocks, MicroStrategy continued to be active in the first quarter, expanding its Bitcoin holdings through new financing tools. As of March 31, MicroStrategy's Bitcoin holdings have reached 528,185 BTC. The company launched two preferred stocks, STRK and STRF, and issued $2 billion in zero-interest convertible bonds. GameStop recently announced a $1.3 billion convertible bond financing, joining companies such as Marathon Holdings and Metaplanet. Coinbase (COIN) and Bitcoin mining companies are underperforming under wider market pressure.

Stablecoins and tokenization have increased momentumStablecoins occupy a core position in the volatile market environment, with a total market value exceeding US$230 billion. The field is attracting new entrants, trying to get a share of the fast-growing market. As GENIUS Act and STABLE Act proposed in the U.S. Senate and House of Representatives, stablecoin legislation is gradually being promoted, prompting institutions such as Fidelity to launch their own stablecoins and tokenization plans.

The recognition of stablecoins is increasing on multiple levels: Stripe calls it a "financial superconductor" in its annual letter. Tether has become the seventh largest U.S. Treasury holder in the world, further cementing the role of stablecoins in the dominance of the dollar and supporting demand for U.S. Treasury bonds.

Of all stablecoins issued on various blockchains, USDC supply on Solana has the largest increase, up 137% to $9.9 billion. While liquidity is pouring into the Solana ecosystem, TRUMP meme coins have also been launched, and liquidity remains stable despite longer cooling down on network activity. PayPal's PYUSD supply on Ethereum increased by 105% to $670 million, while USDC(Ethereum) and USDT (Solana) also grew steadily by about 28%. Overall, Circle's USDC was a major beneficiary of the first-quarter stablecoin momentum, with a market cap hitting an all-time high of $60 billion.

The total transfer volume of stablecoins (adjusted) continues to rise. Most notably, most of the growth in the first quarter came from USDC on the Base Layer-2 network. Base contributed $956 billion and $1.1 trillion in adjusted transfers in January and February, even surpassing USDT on Tron. This momentum in Base highlights its growing DeFi ecosystem and its dominance in stablecoin use in low-cost networks.

Ethereum is out of touch with ETHEthereum's leading position in stablecoins and tokenization continues to increase, with stablecoins supply on the network reaching a record $130 billion, and tokenized assets like BUIDL exceeding $1.8 billion. Despite such sufficient liquidity, activity on Ethereum is still lagging behind in previous years. The poor performance of ETH expanded further in the first quarter, with the ETH/BTC ratio falling to its lowest level in five years. So, what led to the disconnect between Ethereum blockchain, its Layer 2 ecosystem and ETH performance?

This disconnect seems to stem from a variety of factors, especially the roadmap for Ethereum to scale through layer 2, and the meaningful value added to ETH through fees. With the implementation of EIP-4844 in the Dencun upgrade, the introduction of blobspace has brought about a significant transformation in the network economy. In March 2024, Ethereum incurred nearly $30 million in total expenses; a year later, that figure dropped to around $500,000.

This decline is mainly due to the execution migration to L2, and the value of flowing back to L1 is extremely small. Layer-2 such as Base, Arbitrum and Optimism paid only $13 million in total blob costs while maintaining a profit margin of over 90% through serializer revenue. This dynamic has sparked concerns about value leakage, with Ethereum bearing security costs and L2 taking up a disproportionate share of economic value. Blob FeesNow it only accounts for 0.07% of the total cost, and because of the lower base cost, less ETH is destroyed. In the past week, only about 70 ETH were destroyed per day, increasing net issuance and increasing annual inflation to 0.79%.

While this dynamic is currently affecting ETH's valuation, it may take some time for Ethereum to expand through L2. The number of L2 and blob transactions in the Ethereum ecosystem is expected to grow due to the commodification of blobspace and the profitability of the Tier 2 business model. About 21K blobs are published every day, and blob transactions always reach the target capacity (3 blobs per block).

The upcoming Pectra upgrade (and subsequent Fusaka) is designed to further expand blob capacity (EIP-7691), reduce costs, drive more demand for L2 transactions, thereby increasing overall blob fees. Meanwhile, extending L1 by adding gas limits and attracting high-value use cases to the underlying layer (such as stablecoins, tokenization, and DeFi) may provide a viable way to restore long-term value accumulation of ETH. In the upcoming quarter, the focus of the Ethereum staking ecosystem may be in the spotlight as Pectra brings new improvements and issuers seek to launch staking Ether ETFs.

Solana's stress testing and network upgradeQ1 was a turbulent time for Solana. Earlier this year, the network underwent an important stress test with the launch of TRUMP memecoin. Over time, network activity has risen to unprecedented levels, resulting in increased network congestion, fees and MEV tips (non-protocol tips used for transaction priority). The incident also brought about a surge in non-voting transactions to 112 million, with the number of active wallets briefly rising to 5.6 million. However, this surge in activity is short-lived as memecoin activity cools down and wider market conditions worsen.

From the perspective of network development, this quarter is also important to Solana. Three key Solana Improvement Documents (SIMDs) were submitted to vote, affecting the cyber economy and validator incentives. The most important one isSIMD-0228, a proposal to implement dynamic issuance rates based on staking participation (% of SOL supply for staking). Since Solana currently has an annual inflation rate of about 4.5% (15% annually), the goal is to curb issuance and reduce reliance on inflation rewards, shifting validator income to priority fees and MEV tips.

However, the proposal ultimately failed to gain most support, as concerns arise about the profitability of smaller validators and the possibility of validator centralization. While priority fees and MEV tips have fallen from their peak, they together account for 87% of Solana’s economic value.

On the other hand, Solana SIMD-0096 passes, transfers 100% of the priority fee to the verifier. This eliminates the previous 50% priority fee destruction, increasing the rewards for validators and stakers. This change inspires native priority fees for using Solana, reducing reliance on off-protocol tipping systems such as Jito. Since its implementation, the average destruction of SOL has dropped from about 15.9K to about 950, putting inflationary pressure on the supply. Meanwhile, SIMD-0123 has created a mechanism for verifiers to allocate priority fees with stakeholders.

As the Solana network matures, it will demonstrate its ability to promote more sustainable forms of activity in the coming quarters. Meanwhile, signs of institutional appeal are emerging, with SOL futures now listed on the Chicago Mercantile Exchange (CME), which could pave the way for SOL spot ETFs.

ConclusionAlthough this quarter was plagued by macroeconomic uncertainty, structural catalysts such as regulatory clarity and institutional adoption are still advancing. Bitcoin and stablecoins are the main beneficiaries, cementing their position as the basic anchors of crypto ecosystems. Meanwhile, progressive network upgrades such as Ethereum’s Pectra upgrade and Solana’s recent SIMD proposal, despite being in different growth stages, are expected to strengthen on-chain infrastructure and improve the utility of builders, users and network stakeholders. Although near-term volatility may persist, the medium-term outlook remains optimistic, as the shift in macro conditions may bring new liquidity and risk appetite to the crypto market.