4 mins ago

216

Author: Larry Fink, CEO of BlackRock; Translated by: Golden Finance

BlackRock CEO Larry Fink recently released the full text of the 2025 Annual Letter to Investors. Larry Fink starts with the democratization of investment, and then talks about unlocking the private market and tokenization.

Larry Fink also talked about the threat of Bitcoin's status against the US dollar's reserve currency, DeFi and tokenization issues in his investor letter. He said that if the United States cannot control its debt and the deficit continues to expand, the United States may hand over the dollar's reserve currency status to BTC. Decentralized Finance (DeFi) is an extraordinary innovation that makes the market faster, cheaper and more transparent. Tokenization is democratization, and every stock, every bond, every fund, every asset can be tokenized. If they do achieve tokenization, there will be revolutionary changes in the investment field of capital markets. Most importantly, tokenization makes investment more democratic. Tokenization allows partial ownership. This means that assets can be divided into infinitely small parts. This reduces one of the barriers to investing in valuable, previously unavailable assets such as private real estate and private equity.

In order to democratize investment and unlock private markets, BlackRock is entering the field of infrastructure and private credit. In the field of infrastructure, BlackRock acquired Global Infrastructure Partners (GIP) in 2024, which owns some of the world’s most important infrastructure assets – London Gatwick Airport, major energy pipelines and more than 40 global data centers. Also notable are GIP is joining forces with Mediterranean Shipping Company (MSC), Terminal Investment Company (TiL), etc. to acquire the Panama Canal under the Yangtze River Hutchison. In the private credit field, BlackRock acquired Preqin, the world's leading private equity market data company, and HPS Investment Partners, a top private credit management company, in 2024.

1. Prosperity FlywheelDemocratization of investment: Let more places and more people share prosperity

Almost every customer, every leader, and almost every person I have talked to, say: their concerns about the economy are more than ever in recent times. I understand the reason. But we have experienced such moments before. And, in the long run, we will always find solutions.

Humans are smart and resilient creatures, and the systems we build reflect our own image—systems that solve the chaos around us, make sense, and produce unexpectedly good results. Computers process complex data for us (and languages now). Cities allow millions of people to live in peace, and most of them are productive.

But of all the institutions we create, the most powerful and most suitable for our moment began over 400 years ago. This is our purpose to overcome such as lack in prosperity and anxiety in prosperity.The system invented by shield.

We call this system the capital market.

Of all the systems we have created, the most powerful (and especially suitable for moments like us) began over 400 years ago...we call this system the capital market.

In 1602, the world's first stock exchange opened in Amsterdam, and investment became a more democratic cause. Before this, investment was mainly the patents of wealthy businessmen. In fact, about 90% of the initial 1,143 investors on the Amsterdam Exchange were rich. But the rest of the investors are ordinary people. They included 53 artisans, 8 shop owners, 6 silk weavers, 4 soap makers – and at least two maids, each investing 50 guilds, about enough to rent a humble cottage for a year.

Even if the capital market crosses the strait and enters the UK with a strict class system, the London Stock Exchange was not established in the palace. Instead, it began at Jonathan’s Coffee House in “Change Alley”. The bishop and bookkeeper invested with farmers who came directly from the livestock market, with mud still on their boots. Some come here to speculate, but many come here to invest in new businesses – including one that is particularly promising: the Bank of England. This is the first time that ordinary people aren't just watching the economic growth around them. They have a portion of this growth—a real, tradable share.

Our market has grown from coffee shops in alleys to today for four centuries. But fundamentally, the market still operates the same way—like a thriving flywheel: people use savings to invest, the market directs that money to companies and industries, and any success goes back to investors—helping them afford retirement, college, and housing. The flywheel kept turning.

Over our lives, market participation has exploded. In the first half of the 20th century, Americans' stock ownership rose from 1% to 4%. But since I came to Wall Street for my first job in 1976 — with long hair, turquoise, and the ugliest brown suit in the world — investment has become more and more fashionable (luckily, so do I). By 1989, less than one-third of American households had invested in the market; today, that number is about 60%.

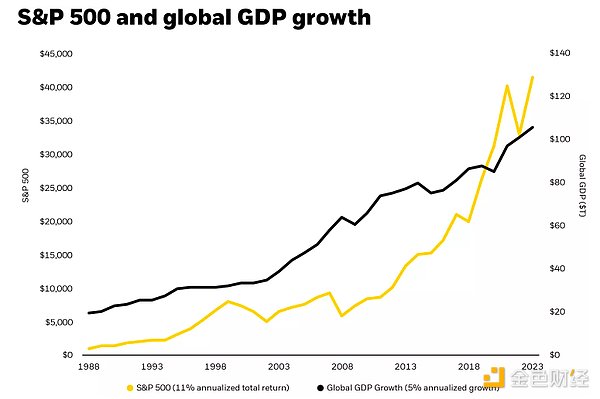

These investors benefited from the greatest wealth creation period in human history. Over the past 40 years, global gross domestic product (GDP) has grown more than the previous two thousand years combined. This extraordinary growth—it must be noted, partly due to historic low interest rates—has excellent long-term returns. But of course, not everyone shares this wealth.

Figure 1.1

Historical performance does not necessarily reflect future investment performance.

This extraordinary era of market expansion coincides with globalization and is driven to a large extent by globalization. While a flatter world has lifted a billion people out of $1 a day of poverty, it has also hindered the wealthy millions of people working to pursue a better life.

Today, many have double inverted economies: one accumulates wealth while the other is full of difficulties. This disagreement reshapes our, and even our perception of possibilities. Protectionism returns strongly. The self-evident assumption is that capitalism doesn't work and it's time to try something new.

But there is another view: capitalism does work—it’s just for too few people.

The market is like everything humans build, not perfect. They reflect us – unfinished, sometimes flawed, but always improve. The solution is not to give up the market, but to expand the market, complete the democratization of the market that began 400 years ago, and to give more people the meaningful benefits of the growth that is happening around them.

In the following content, I will put forward some ideas on how to further democratize investment in two aspects:

1. Help existing investors enter some markets they were previously restricted from entering

2. Let more people become investors first

I will start with BlackRock's work, but both efforts go beyond asset management and involve broader issues such as retirement, energy and tokenization.

The market is like everything humans build, not perfect. The market reflects us – unfinished, sometimes flawed, but always improves. The solution is not to give up the market, but to expand the market.

More investment. More investors. This is the answer.

Given that BlackRock is a trustee and the largest asset management company in the world, some readers may think I’m talking about my book. This makes sense. But this is also a book we chose specifically - long before it became a bestseller. From the beginning, we believed that when people can invest better, they can live a better life—that's why we founded BlackRock.

2. Unlock the private market BlackRock's performance in the past 14 months and the futurethe economy relies on capital to operate. Whether it is forming a 17th-century trade fleet or a 21st-century data center, funds must come from somewhere. But historically, the source of funds has not come from investors. Despite 400 years of financial innovation, from Amsterdam to Change Alley to the New York Stock Exchange, most financing comes from banks, businesses and , not capital markets.

Why are banks, enterprises and? Because people put money into these institutions. They deposit their savings into their bank accountsConsumption drives business growth and pays taxes to fund public spending.

But when my partner and I founded BlackRock in 1988, we believed the world was changing. The capital market is not only a supplement to banks, businesses and enterprises, but will also become the same source of capital alongside these institutions.

We believe the world is changing. The capital market is not only a supplement to banks, enterprises and, they will also become the same source of capital alongside them.

The logic is simple: the capital market returns higher than the other three. Higher returns will attract more investors. More investors will deepen the market. A deeper market means more capital. In addition, asset managers can accelerate this transformation through innovation. For BlackRock, this means first developing better technology to manage risk, then expanding options and reducing fees through products like exchange-traded funds (ETFs).

We have been lucky in the past 37 years. Our logic is correct. But now it’s surprising that we are still in the early stages of the story of market expansion. The real reward has just begun.

As we enter the second decade of this century, the mismatch between investment demand and the capital that traditional sources can provide is growing.

Funding for infrastructure construction cannot be provided through deficits. The deficit cannot be higher. Instead, it will turn to private investors.

At the same time, companies will not rely solely on banks to obtain credit. Bank loans are restricted. Instead, businesses will turn to the market.

The money is already there. In fact, there is more capital idle today than at any time in my career. In the United States alone, about $25 trillion is deposited in banking and money market funds.

But we repeat an early mistake in finance: capital abundance. But the deployment is too narrow. As one historian wrote, if investors had more companies to invest, Amsterdam's first stock exchange "would have made a greater contribution to the economy." The same is true today.

The assets that determine the future—data centers, ports, power grids, the world’s fastest-growing private enterprises—are not accessible to most investors. They exist in private markets, blocked by high walls, and only the richest or largest market participants can open the door.

The reasons for being excluded have always been risk, insufficient liquidity and complexity. That's why only certain investors are allowed to enter. But nothing in the financial field is unchanged. Private markets don't have to be so risky, opaque or out of reach. As long as the investment industry is willing to innovate, that won’t be the case – that’s exactly what we’ve done at BlackRock over the past year.

BlackRock has been involved in the private market. But we are a traditional asset management company first. That's what we did in early 2024. But now we are no longer like this.

In the past 14 months, we have announced the acquisition of two fastest growing areas of the private equity market: infrastructure and private credit. We acquired another company to get better data and analytics so that we can better measure risks, identify opportunities and open access to the private equity market.

We have achieved the company's transformation. The next section will give you a detailed look at why we do this, how we do this, and why it is important to do this.

The $68 trillion investment boom: Who will own it?BlackRock has been involved in the private market. But we are a traditional asset management company first. That's what we did in early 2024. But now we are no longer like this.

Throughout history, infrastructure has driven amazing economic growth. Between 1860 and 1890, the construction of railways alone increased U.S. GDP by about 25%. A century later, highways played a similar role: In a way, between 1950 and 1989, investment in interstate systems accounted for about a quarter of productivity growth.

Today, we are on the brink of a huge opportunity that is almost difficult to grasp. By 2040, global demand for new infrastructure investment will reach $68 trillion. From another perspective, this roughly amounts to building the entire interstate system and transcontinental railroad every six weeks—for the next 15 years.

Figure 2.1

In the past year, I have been stressing that I have been carrying a heavy burden of historic deficits and cannot rely solely on taxpayers to bear the huge costs of new infrastructure, otherwise I will face the risk of a spiral of debt. But it is not the only institution facing restrictions. Even the world's largest tech company, despite billions of dollars in free cash flow, does not have the ability to invest at this scale. The cost of an AI data center could be between $40 billion and $50 billion.

When I talk to technology leaders, they often tell me that their companies want to focus on what they do best—invent breakthrough technologies, rather than funding the vast infrastructure needed to deploy the technology.

The market is eager to intervene when the company exits. Investors have voted with their money – making infrastructure one of the fastest growing segments in the world. However, this investment is limited due to our capital market structure.

Private market is privateMost of us associate "markets" with open markets—stocks, bonds, commodities. But you can't usually buy stocks on the London or the New York Stock Exchange for the new high-speed rail line or the next-generation grid. Instead, infrastructure projects are usually only invested through the private market.

Private market, as the name implies, is a private market. For individual investors,They usually require a higher minimum investment. Even if the minimum investment is low, investment is usually limited to people with a certain income or net worth.

Most companies in the world face the same obstacles. Only a small percentage of companies are publicly traded companies, and that percentage is shrinking: BlackRock’s path to raising funds through IPOs 25 years ago is becoming increasingly rare. Conversely, 81% of U.S. companies with revenues of more than $100 million are privately held. The EU is higher, and the UK is even higher

However, these companies still need funds to innovate and grow. For decades, they turned to banks, just as families borrowed home mortgages from banks. But that era is rapidly disappearing. Today, banks themselves cannot meet the capital needs of growth companies.

Figure 2.2

The private credit industry is stepping in to help fill this gap. In fact, private credit assets are expected to more than double by the end of this century. However, like infrastructure, many individual investors are unable to participate in growth. Even some larger institutional investors have difficulty building portfolios that distribute these assets the way they want.

From 60/40 to 50/30/20The beauty of investing in a private market is not having a specific bridge, tunnel or medium-sized business. It depends on how these assets complement your stocks and bonds - diversification.

Diveristic investment is known as the "only free lunch". It was this philosophy that prompted Nobel Prize winners Harry Markowitz and Bill Sharp to create the modern portfolio theory, which became the basis for a standard portfolio of about 60% of stocks and 40% of bonds. Generations of investors have followed this approach, holding the entire market rather than a single securities, and achieving good results. But with the growing global financial system, the classic 60/40 portfolio may no longer represent a true diversified investment.

The standard portfolio of the future may be more like 50/30/20—stocks, bonds and private assets such as real estate, infrastructure and private credit.

The attraction is obvious. While these private assets may take greater risks, they also offer huge benefits. For example, infrastructure provides:

1. Inflation protection – income generated by infrastructure (such as tolls and utility bills) usually increases with inflation.

2. Stability— Unlike open markets, infrastructure returns tend to be much less volatile.

3. Returns – Historically, even if only 10% of the portfolio is allocated to infrastructure, it can improve overall returns.

Figure 2.3

Past investment performance does not represent current or future results

The standard future portfolio may be more like50/30/20 – Stocks, bonds and private assets such as real estate, infrastructure and private credit.

But the challenge is: the industry is not built on the 50/30/20 pattern. The industry is mainly divided into two major categories: traditional asset management companies focus on 50/30 (stocks and bonds), while specialized private market companies dominate 20 (private assets).

For most people, it is nearly impossible to bridge the gap between 50/30 and 20. Even those who are affordable face another problem of decentralization within that 20%. Often, their capital is barely enough to meet the minimum requirements of a private equity fund – and locking 20% of its portfolio into one fund is not really diversification.

We can help investors achieve better results. The divergence between open and private markets is a tricky problem—but it can be solved. In fact, BlackRock has solved similar market challenges before.

Before public and private ownership, there were indexes and initiativesIn 2009, BlackRock acquired Barclays Global Investors (BGI). They created iShares, the world's leading ETF business. At the time, most people thought our acquisition was just a bet on ETFs. But in reality, the deal is much larger.

At that time, the investment community showed different split trends:

1. On the one hand, index funds, such as ETFs provided by BGI, are low-cost, rules-based investment portfolios that only track indexes such as the S&P 500.

2. The other party is active investment, managed by a portfolio manager trying to defeat the market.

The industry acts as if you have to choose one side—as if these two approaches are mutually exclusive. Our acquisition of BGI was based on the belief that they were not mutually exclusive.

We realize that even if you just choose an index fund, every investment decision is positive. After all, there are indexes for large-cap stock value, large-cap stock growth, the entire stock market, emerging markets, energy stocks, financial stocks, Brazilian small-cap stocks and all stocks in between. Choosing among these stocks requires important decisions such as the right portfolio, the amount of risks you are willing to take, and how to manage them.

When we integrate active and index strategies together, we provide investors with something unprecedented: the freedom to seamlessly integrate strategies. ETFs are no longer purely passive. Instead, they become a fundamental component in creating any type of portfolio (active, exponential, or a combination of both). Diversification becomes easier. The cost is lower. In fact, our ETFs have saved our customers $642 million since 2015. Most importantly, investors finally have more control over their funds—regardless of themAre they individuals saving for retirement or are they large institutions that manage billions of dollars.

Now, we see opportunities to resolve the gap in the public and private markets, just as we solve the gap in index and active markets. In October, BlackRock completed the first of three acquisitions, the Global Infrastructure Partner (GIP), to remove the boundaries that hinder investment.

GIP and Infrastructure OpportunitiesNow, we see opportunities to solve the problem of the public-private market gap, just like we solve the problem of the index market and the active market gap.

GIP represents our clients with some of the world’s most important infrastructure assets – London Gatwick Airport, major energy pipelines and over 40 global data centers. They are good at finding the world's most attractive infrastructure investments and directing capital to build or improve them. In other words, GIP itself is a pipeline—connecting BlackRock customers directly to the global $68 trillion infrastructure boom, including data centers.

As Nvidia CEO Jensen Huang recently stressed, “At present, we are investing $150 billion in AI infrastructure into trillions of dollars, so we have a partnership with BlackRock.” The partnership also includes xAI, Microsoft, MGX and most importantly BlackRock’s customers. Their capital will drive the rise of decisive technology this century and earn rewards. All of this is done through GIP.

Same goes for the landmark port agreement we announced this month. The agreement covers 23 43 port networks in principle. Every year, one out of every 20 containers worldwide passes through these ports.

Our partners include Mediterranean Shipping Company (MSC), one of the world's leading shipping and logistics companies, and Terminal Investment Co., Ltd. (TiL), one of the world's largest container terminal operators. Once the transaction is completed, our consortium will have a portfolio of approximately 100 ports worldwide. Together, we understand how to invest, own and operate these assets. In fact, GIP is an expert in improving infrastructure efficiency. When they bought Gatwick Airport, they managed to cut security checks by more than half — partly through simple solutions like oversized luggage pallets. This gives travelers more time to shop and eat, thereby increasing the profitability of the airport. In other words, we are not only providing more infrastructure for our customers, but also providing better infrastructure for our customers.

HPS, Preqin and why private markets don’t have to be opaque marketsAs we finalized the GIP deal, BlackRock was busy with two other major acquisitions. At the beginning of the summer of 2024, we announced plans to acquire Preqin, one of the world's leading private equity market data companies. Then,We announced plans to acquire HPS Investment Partners, a top private credit management company at the end of the year.

These acquisitions will allow our customers to enter the private equity market more directly—a market that provides financing for global businesses and maintains the operation of the consumer economy. But it also contains deeper long-term strategic thinking.

For decades, the private equity market has been one of the most opaque areas in the financial field. Investors know that these assets have long-term value—but how much is it? This is not always easy to determine.

A good analogy is real estate. If you are buying a home, you want to know if the price you are paying is reasonable and there are many ways to do this. You can view community benchmarks, recent sales or historical appreciation trends; companies like Zillow make it all simple. But nowadays, investing in a private equity market is a bit like buying a home in an unfamiliar neighborhood before Zillow appeared, where it is difficult or impossible to find the exact price. This lack of transparency can hinder investment.

Our acquisition is intended to change this. For example, Preqin provides the industry's most comprehensive private equity market dataset. The company tracks over 190,000 funds and 60,000 managers. This rich data set clearly demonstrates managers and funds' performance and also provides comparable valuations of assets they own. In other words, Preqin's role in the private equity market is equivalent to Zillow's role in real estate. Or, if you prefer to compare with the financial industry, it's the equivalent of the role of Bloomberg terminal on stocks and bonds.

But our vision goes beyond that.

With clearer and more timely data, you can index the private market as you do now with the S&P 500. Once this is achieved, the private market will become a simple and easy-to-access market. Easy to buy. Easy to track. This means that capital will flow more freely throughout the economy. The boom flywheel will spin faster and generate more growth—not only for global economy or large institutional investors, but also for investors of all sizes around the world.

The new era of investmentWith clearer and more timely data, private markets can be indexed, just like we do now with the S&P 500. Once this is achieved, the private market becomes simple and easy. Easy to buy. Easy to track.

To a certain extent, this moment is like a microcosm of BlackRock's starting journey.

In 1988, our first employee—the late, missed Charles Hallac—buyed a computer. This computer costs $25,000 and is about the size of a washing machine. Charlie stuffed it in usBetween the refrigerator and the coffee machine, use this computer to start developing Aladdin. This software provides investors with something unprecedented: a clear, unified view of portfolio risk. It fundamentally changes the way you invest.

Charles "Charlie" Haraker (1964-2015)

Looking back over the past 37 years, BlackRock's founding has not only created a company, it has also transformed the industry. Decades later, we may see 2025 as another critical moment when the financial landscape will change again.

But this future will not be shaped only by asset management companies. The market never exists in isolation. The economic rules we choose, the investments we take, and the ways in which we attract and allocate capital will determine who will benefit – and how far the prosperity will spread.

This is the challenge I will face next. The best starting point is the end most of us hope for: a comfortable, economical and secure retirement life.

3. From retirement to tokenization How can we democratize investment?On September 30, 1933, at the height of the Great Depression, a California newspaper, The Long Beach Telegraph, published a letter from Francis Townsend. Townsend, a local doctor, wrote the letter in anger after witnessing an elderly woman searching for food on the street. Townsend’s proposal — offering $200 per month to every American over 60 — triggered a campaign that led to social security in the United States.

Social security saves nearly 30 million Americans from poverty every year, according to the U.S. Census Bureau data – an extraordinary achievement. However, forecasts show that Social Security’s retirement and disability funds will be exhausted by 2035. After that, people can only receive 83% of the promised benefits, and this percentage will decline over time.

But even if we strengthen social security, it is not enough. The system was designed to be exactly what Francis Townsend wanted to lift the elderly out of poverty. But getting rid of poverty does not mean getting economic security. That's why today, even with the promise of social security, more than half of Americans are still worried that their savings will run out rather than death itself.

A good retirement system provides safety nets for people when they fall. But a great retirement system also provides a ladder for their savings to grow and their wealth grows year after year. This is exactly what the United States is short. At present, the United States is paying great attention to preventing people from falling to the bottom, which is what we should do. But the United States needs to do the same, through investment, helping people climb to the ceiling.

More than half of the funds managed by BlackRock are pensions. This is our core business, which makes sense: For most people, retirement accounts are their first (and usually only) investment experience. So, if we really want to democratize investment, retirement is the starting point of discussion.

33% of Americans do not have retirement savings, 51% of Americans are more worried about not enough savings than death itself, and one-third of Americans will find it difficult to pay an unexpected $500 bill

A good retirement system provides a safety net for people to fall. But a great system also provides a ladder for their savings to grow and their wealth grows year after year.

While BlackRock helps people around the world invest in pensions, I want to highlight the United States in this section. Because the situation is bad. Public pensions face huge gaps. Nationally, data shows that public pension funds are only about 80% – which may be an overly optimistic figure. Meanwhile, one-third of Americans have no retirement savings at all. No pension, no 401(k) – nothing.

As money gets less and less, life span becomes longer and longer. Now, if you are married and both of you are 65 years old, the chances of at least one of you living to 90 are 50%. With biomedical breakthroughs such as GLP-1 drugs, more chronic diseases may be cured soon.

It's an incredible blessing, but it also emphasizes some frustrating things: We're very good at extending people's lifespan, but we're spending little effort to help them afford the extra lifespan.

What should worry us the most is the issue we don’t talk about. From this perspective, my concerns about the U.S. retirement crisis are less than a month ago.

In March this year, BlackRock held a retirement summit in Washington, D.C., where Republicans and Democrats, asset management companies and pension funds, small business owners, firefighters, teachers, union members and farmers gathered. It's an eclectic group, and that's what it means. Good ideas may come from unexpected places. After all, the most important retirement plan in American history began with an op-ed article published by an unknown doctor in a small newspaper.

The same happened at the summit: We saw a consensus on practical ideas to help more Americans start investing, increase savings to achieve retirement goals, and confidently spend the money they make - so Americans don't have to worry about spending all of their money, and they will definitely not be more terrible than death itself.

From left to right: James Slevin (New York Fire Department, District 1 Vice Chairman, International Firefighters Association), Michelle Crowley (former Biloxi Fire Department), Shebah Carfagna (Panache Wellness and Fitness owner), Nate Wilkins (founder of Ageless Workout Method) and Gayle King (host, CBSMornings Co-host and Oprah Daily Special Editor)

Where do we start?At the summit, a group invited a firefighter who recalled joining the pension plan without knowing it when he was a recruit. A senior firefighter gave him a form and gave an order: "Just sign it. You will thank me 25 years later." He signed it.

Every American should be able to start investing so easily. But for millions of people, investing is still not an option.

We can solve this problem in three ways.

First, expand emergency savings. If you are worried about paying for a bolt blowout or emergency room tomorrow, no one will invest in retirement. However, one-third of American voters say they can’t afford $500 in surprise spending, and that’s the reality.

What is the solution? BlackRock Charitable Foundation has partnered with a group of nonprofits to establish an emergency savings program that helps most low-income Americans deposit $2 billion into an “emergency savings account.” We found that people with these dedicated emergency funds were more likely to invest in retirement – a study showed that the likelihood was 70% higher.

The SECURE 2.0 Act was passed in 2022 to promote the idea nationwide. The law allows workers to deposit up to $2,500 in emergency accounts linked to retirement plans, including employer matching and easy withdrawals. But this is just the beginning. We can further simplify the rules, increase the payment limit, and enable automatic registration of independent emergency accounts.

Second, narrow the gap in small businesses 401(k). Half of Americans work in small businesses, but nearly half of them do not offer retirement plans. This problem can be solved. States that tried incentives promoted 401(k) adoption and employee savings. Makers can be more involved in this area, helping small businesses provide plans and automatically register employees.

Third, help people start investing as early as possible. At our retirement summit, Senators Cory Booker (D-Jersey, New Jersey) and Todd Young (R-Indiana) talked about the market-oriented version of “baby bonds.” The idea is to open an investment account for every American child on the day of birth. Senator Booker mentioned that the program could be initiated by redistributing a portion of the existing tax relief that mainly benefits the rich. This is an interesting concept. Even a small amount of money can accumulate into a very large portfolio in a lifetime.

Every American should be able to start investing so easily. But for millions of people, investing is still not an option.

From left to right: Senator Cory Booker (New JerseyDemocratic Senator), Senator Todd Young (Republican Senator of Indiana), Shai Akabas (Biblical Center)

For many state and federal makers have proposed different versions of the plan over the years. I think this idea is worth reconsidering. The real reward is not just economic, but fundamental. When people have a part of their economy, they not only benefit from growth, they also believe it. Ownership creates a connection. It turns passive observers into participants.

Imagine a child born today whose personal wealth grows simultaneously with the United States. This is what economic democracy looks like: here, everyone has a new way—investment—to pursue happiness and financial freedom.

How to achieve $2,089,000?This is what economic democracy looks like: everyone has a new way—investment—to pursue happiness and financial freedom.

Once people start investing in retirement, the goal is simple: make their money add as much value as possible, as quickly as possible.

In January this year, BlackRock surveyed Americans and asked how much they would need to retire comfortably. When we averaged these answers, the number just exceeded $2 million — $2.089 million to be exact. This is quite a lot. More than I expected. And almost no one is close to this number. Even Gen X, the oldest of which will start retiring in five years, doesn’t have enough money. In fact, 62% of people save less than $150,000.

We need better ways to improve our portfolio. As I have written before, private assets such as real estate and infrastructure can boost returns and protect investors during market downturns. Pension funds have been investing in these assets for decades, but 401(k) doesn’t. This is one of the reasons why pensions usually perform around 0.5% better than 401(k) each year.

Half a percentage point doesn't sound like a lot, but over time it accumulates. BlackRock estimates that an additional 0.5% annual return will increase your 401(k) account by 14.5%. This is enough to give you another nine years of retirement and help you stop working as you wish. Or in other words, private assets allow you to have an additional nine years with your grandchildren.

If private assets perform so well, why aren’t they in your 401(k) plan? One major reason is that it is an unfamiliar area for a 401(k) provider that chooses the investment you plan to offer.

When you invest in private assets (such as bridges), the value of these assets will not be updated every day, and you cannot withdraw funds at any time. After all, it's a bridge, not a stock. As I've beenWritten, while BlackRock is working to make the markets of these assets more transparent and liquid, many 401(k) providers have not yet adapted to this ever-changing financial landscape. In fact, incorporating assets such as real estate or infrastructure into 401(k) has only become practical within the last five to ten years.

This is a complicated thing. Need clarification. Asset managers, private market experts, consultants and consultants all play a role in guiding 401(k) providers. This is part of the reason I wrote this letter - to clear the fog. We need to be clear: Private assets are legal in retirement accounts. They are beneficial. And they are becoming more transparent.

Target date funds are a great starting point. People love its simplicity: You just choose the year you plan to retire—2040, 2055, 2060—and let the fund do the rest. This simplicity makes target date funds ideal for introducing private assets. When you invest for decades, the barriers that 401(k) providers often face — such as daily valuations or instant liquidity — are less important.

How do we help people spend their savings?Or in other words, private assets allow you to have an additional nine years with your grandchildren.

Accumulating savings is only half the challenge. The other half – especially for 401(k) savers – is knowing how to spend money.

Most pension holders are not worried about this. Their income comes every month, like a stable salary check. But the 401(k) plan does not come with instructions. When you retire, you get a sum of money and are asked to spend the rest of your life with it—but don’t know how long that money will last.

What is the result? Even retirees with adequate savings often spend too little because they worry about spending all their money. They narrow their dreams and delay their happiness. Economist Bill Sharp called this problem "the most difficult and difficult problem in the financial field." Although it is difficult, it can be solved.

Last year, BlackRock launched LifePath Paycheck® to address this concern. It gives people the option to convert 401(k) retirement savings into stable and reliable monthly income. In just 12 months, LifePath Paycheck® has attracted 6 program sponsor clients representing 200,000 individual retirement savers.

But no one declared victory. As the oldest Gen X begins to retire, the problem only becomes more difficult and tricky. They are the first generation who relied primarily on the 401(k) program. And the trend for the 401(k) program is growing among millennials and Gen Z. Their employers need to provide solutions that convert their savings into predictable income. In this way, everyAny American can retire with confidence.

If it takes 13 years to build a power line, we will not be able to democratize investment.In the United States, retirement savings investment accounts for approximately 30% of the stock market funds. This is our greatest opportunity to help more people grow with the wider economy. But just as retirement is not the entire market, it is not the entire solution.

For example, if the infrastructure is never built, it makes no sense to allow retired investors to enjoy the infrastructure. This happens frequently nowadays.

In the United States and the European Union, approval time for infrastructure projects is usually longer than construction time. High voltage transmission lines may take 13 years to get approved, and only a quarter of the time will be approved.

Ezra Klein and Derek Thompson skillfully describe this permission nightmare in their new book Abundance. One particularly vivid text puts California’s stalled bullet train project in historical context:

"California... built the western section of the Transcontinental Railroad in the 1860s, leaving only a few hundred miles. The project spans nearly 1,800 miles. It took only six years to complete. Today, six years roughly amounts to the time California realizes that its high-speed rail construction needs to be delayed by another ten years. More than 23,000 miles of high-speed rail have been built in the time when California failed to complete its 500-mile high-speed rail system."

But delays in energy infrastructure "can cause chaos in the best case and catastrophic consequences in the worst case."

The global demand for electricity surges in part due to the rise of artificial intelligence. A single data center can consume 1 GigaW of electricity. This is enough to power the entire city of Honolulu on the hottest day of the year. In Utah, Ohio and Texas, utilities have warned that demand for AI-powered electricity will drive the grid beyond capacity. Even Silicon Valley power companies have stopped accepting new data center requests.

Without large-scale investment in energy production and delivery, as well as electricians and engineers who build these facilities, we face an unacceptable trade-off: Who gets electricity—people or machines? If a society chooses to cool servers while citizens spend their days in stuffy or cold, then it fundamentally misplaces its priorities.

We need energy pragmatism. The slow, imperfect licensing procedures in the United States and Europe are first to address. But this also means keeping a clear understanding of our energy structure.

Most new infrastructure investments are flowing to renewable energy. But without major breakthroughs in storage, wind and solar energy alone cannot reliably maintain lighting. In the short term, more than half of the power supply of data centers must come from dispatchable energy. Otherwise, the air conditioner will be turned off, the server will overheat, and the data center will be turned off.

Where does dispatchable power come from? Nuclear energy is itOne of them. But nuclear energy is becoming less and less common. Over the past 55 years, the United States has closed more nuclear power plants than newly built. As Klein and Thompson wrote, “It’s not that the private market fails to take risks responsibly, but that the federal government fails to measure risks correctly.” After all, nuclear power today is no longer old-fashioned large nuclear power plants and intimidating cooling towers. Small modular reactors (SMRs) have everything that old nuclear power plants don’t have—lower construction costs, safer operation, and can be built anywhere.

No waiting. They are building a 100-gigaW nuclear power plant, which, once completed, will mean they supply half of the world’s nuclear power. Why are you so optimistic about nuclear energy? They believe that decarbonization is a way to master the future of industry.

Take BYD as an example. The automaker sells more electric cars than any other company in the world. Next year, they plan to add fully autonomous driving features to their cars—the same price as last year’s models. They are now selling electric cars for $10,000 — a price that is unmatched by automakers in the United States or Europe. Within five years, internal combustion engines may be completely eliminated—not just for environmental reasons, but also to monopolize the global market of driverless, battery-powered cars—those cars do not require gasoline and are only one-third of the price of foreign competitors.

Without investing in energy production and transmission on a large scale…we will face an unacceptable trade-off: Who gets electricity—people or machines? If a society chooses to cool servers while citizens spend their days in stuffy or cold, then it fundamentally misplaces its priorities.

Figure 3.1

A 's wealth and its energy consumption are an interesting relationship. This correlation is almost perfect: the more energy, the more wealth. However, to some extent, the relationship should break down.

As the economy becomes richer, they usually maintain growth with less incremental energy due to increased efficiency. But you might say that things are different now. Even in the richest, prosperity once again depends on our ability and willingness to produce and consume more energy.

Should we be optimistic about Europe again?BlackRock was born in the United States, and our first customers were in Japan—but it was Europe that really brought us globalization.

In 2006, we acquired the London-based Merrill Lynch Asset Management business and since then we embarked on the road to becoming the world's largest asset management company. Today, we manage $2.7 trillion in assets for our European clients, including about 500 pension plans that support millions of people.

The economic outlook for Europe has been pessimistic over the past decade. Slow economic growth, stagnant markets and cumbersome supervision have dominated the headlines. Former Italian Prime Minister and European Central Bank President MaliO'Draghi recently pointed out that Europe has lowered trade barriers outside the continent, but it has not done so within the EU. Draghi highlighted an International Monetary Fund (IMF) analysis that painted a stunning picture: For a German company, doing business now may be more attractive than doing business in neighboring France.

But I think Europe is awakening. The makers I've talked to - I've talked to a lot of people - now realize that regulatory barriers don't automatically disappear. These issues need to be addressed. And the benefits are huge. According to the International Monetary Fund, reducing internal EU trade barriers to levels between U.S. states could increase productivity by nearly 7%, adding a staggering $1.3 trillion to its economy—the equivalent of recreating Ireland and Sweden.

BlackRock was born in the United States, and our first customers were in Japan—but it was Europe that really brought us globalization.

What's even better is that artificial intelligence may be able to resolve the population time bomb in Europe.

The biggest economic challenge facing the continent is the aging of the labor force. Among the 27 EU member states, 22 working-age populations are declining. Since economic growth depends largely on the size of a workforce, Europe is at risk of a prolonged recession. The European Commission also recently issued a warning that sustained growth can only be achieved if the European labor force is expanded, productivity increases, or both.

Figure 3.2

This is exactly where artificial intelligence may play a key role. In economies that rely heavily on manufacturing and manual labor, artificial intelligence has a smaller impact. But in service-based economies, artificial intelligence can effectively automate tasks, thereby significantly improving productivity.

People are worried that artificial intelligence may replace jobs. This concern is reasonable. But in an aging and wealthy society, labor shortage is inevitable, and artificial intelligence may not be a threat, but a lifeline.

Will Bitcoin erode the dollar's reserve currency status?For decades, the US dollar's status as the world's reserve currency has benefited the United States a lot. But this situation may not last forever.

Since the debt clock in Times Square began to ticke in 1989, debt has grown three times that of GDP. This year, interest expenses will exceed $952 billion, more than defense spending. By 2030, mandatory expenditures and debt repayments will consume all federal revenues, resulting in a permanent deficit.

If the United States cannot control its debts, if the deficit continues to expand, the United States may hand over this position to digital assets such as Bitcoin.

Figure 3.3

To be noted, I obviously do not object to digital assets (my viewThe method goes a step further, see the next section). But two things can be established at the same time: Decentralized Finance (DeFi) is an extraordinary innovation. It makes the market faster, cheaper, and more transparent. However, if investors start to see Bitcoin as a safer option than the dollar, the same innovation could undermine the U.S. economic advantage.

Tokenization is democratizationWhen the trading hall still operates revolutionarily by shouting slogans and placing orders and fax machines, the world's currency is circulated through this channel.

Taking the Global Banking Financial Telecommunications Association (SWIFT) as an example. The system supports trillions of dollars in global transactions a day, and it works much like a relay race: banks issue instructions one by one, meticulously checking details at every step. This relay method was reasonable in the 1970s, when the market size was much smaller and the daily trading volume was much smaller. But nowadays, relying on SWIFT is like sending emails through the post office.

Tokenization has changed all this. If SWIFT is a postal service, then tokenization is the email itself—the assets can be transferred immediately and bypassed by the intermediary.

What exactly is tokenization? It converts real-world assets (stocks, bonds, real estate) into digital tokens that can be traded online. Each token proves your ownership of a particular asset, just like a digital contract. Unlike traditional paper certificates, these tokens are securely present on the blockchain and can be purchased, sold and transferred instantly without the need for tedious paperwork or waiting time.

Each stock, every bond, every fund—every asset—can be tokenized. If they do achieve tokenization, the investment field will revolutionize. The market will not need to close. The transaction that currently takes several days will be completed in seconds. Billions of dollars currently blocked by settlement delays can be reinvested into the economy immediately, thereby boosting economic growth.

Each stock, every bond, every fund—every asset—can be tokenized. If they do achieve tokenization, the investment field will revolutionize.

Perhaps most importantly, tokenization makes investment more democratic.

It can democratize access. Tokenization allows partial ownership. This means that assets can be divided into infinitely small parts. This reduces one of the barriers to investing in valuable, previously unavailable assets such as private real estate and private equity.

It can democratize shareholder votes. When you own stocks, you have the right to vote on the company's shareholder proposals. Tokenization makes this all easier because your ownership and voting rights are digitally tracked, allowing you to vote seamlessly and safely from anywhere.

It can democratize benefits. Some investments generate much higher returns than others, but only big investors can participate. What is the reason? friction. law, operations, bureaucracy. Tokenization eliminates these, allowing more people to obtain potentially higher returns.

I expect that one day, tokenized funds will be as familiar to investors as ETFs—as long as we solve one key problem: identity verification.

Financial transactions require strict identity verification. Apple Pay and credit cards can easily handle billions of authentication times a day. Trading venues like the New York Stock Exchange and MarketAxess also managed to provide the same services for securities trading. But tokenized assets will not go through these traditional channels, which means we need a new digital authentication system. This sounds complicated, but India, the most populous in the world, has done it. Today, over 90% of Indians can safely verify transactions directly through their smartphones.

The conclusion is obvious. If we really want to build an efficient and accessible financial system, simply supporting tokenization is not enough. We must also solve the digital verification problem.

Things worth expandingAround 80 years after Jonathan Café became the London Centre for Financial Life, a group of 150 wealthy businessmen tried to close its doors.

They offer Jonathan’s boss £1,200 per year (equivalent to the 10-year salary of an average worker) as a reward for exclusive use of the space during the main trading hours. Essentially, they want to create a private market.

But the majority of investors in London do not accept it. They protested, defended themselves in court, and two years later, they won. The market must remain open. Everyone can invest.

From our perspective today, financial history can be seen as a long and stable journey towards a more democratic direction—more investors, broader participation and greater prosperity. To a large extent, this is indeed the case. But this democratization has never been guaranteed. Still so now.

The market will not naturally develop to serve everyone equally. The market requires unremitting efforts, conscious choices and constant vigilance—from the cafe protests centuries ago to today’s complex debates about retirement, tokenization, infrastructure investment and artificial intelligence.

It’s a tough job, but at BlackRock we have been doing it for 37 years as trustees for clients. We feel the job is worth it every day. Because no system designed by humans can create wealth for more people than the capital market.

People invest their savings, whether it’s DDR50 or $50,000, which turn into roads and schools, businesses and breakthrough technologies that power our economy to return wealth to millions of people, so they can no longer have to worry about financial problems on the kitchen table and spend more time enjoying life with their families.

I have always said that investing is a behavior of hope——No one will make long-term investments unless they believe that the future will be better than it is now. But this is not entirely true. Investing is not just an act of hope; investing makes our hope a reality.

This is something worth protecting.

This is worth expanding.

This is something worth democratizing.

IV. BlackRock's performance 2024-2025Last fall, we celebrated the 25th anniversary of BlackRock's initial public offering (IPO). When we went public, we had only 650 employees and the stock price was $14 per share. We manage $165 billion in major fixed income assets for our clients and we are just starting to sell Aladdin’s technology.

Today, we manage $11.6 trillion in assets for our clients, and Aladdin generates more than $1.6 billion in revenue each year. Our workforce is currently nearly 23,000 with offices in over 30. As of 2024, our share price exceeded $1,000 per share. But even though it’s 25 years since our IPO and 37 years after our founding, it’s just the beginning of BlackRock’s story in many ways.

2024 is a landmark year for BlackRock. Clients commissioned us for a record $641 billion net inflow. Our asset management scale increased by $1.5 trillion, hitting record highs in revenue and operating profits, with a total shareholder return of 29%.

In a dynamic investment and re-risk environment, customers want to return to the market more actively. They achieved this through BlackRock. We ended the year with a record of net inflows set for two consecutive quarters, with net inflows of $281 billion in the fourth quarter and an organic base expense growth rate of 7%. Importantly, this organic growth is widely present in institutions, wealth and regions. Clients want to integrate more portfolios with partners they work with for a long time to achieve their business aspirations and portfolio goals. They want portfolios to be seamlessly integrated into public and private markets, vibrant and based on data, risk management and technology.

This historic client activity comes as we execute our most important acquisition since BGI more than 15 years ago. We complete GIP and Preqin deals and plan to acquire HPS later this year, which are expected to expand and enhance our private equity investment and data capabilities.

Customers are always at the heart of our strategy and we are interested in investing to meet our customers’ various needs. We have built a differentiated asset management and fintech platform that fully integrates both public and private markets.

After our planned acquisition of HPS, we expect BlackRock’s alternative investment platform to become one of the top five clients,Assets reach $600 billion and annual revenue exceeds $3 billion. This will be integrated with BlackRock’s platform, which already has the world’s No. 1 ETF franchise, $3 trillion in fixed income, $700 billion in insurance asset management, consulting services, and our proven Aladdin technology.

Aladdin is supporting the entire portfolio ecosystem in both the public and private markets through eFront and our recently acquired Preqin. This evolving platform has changed the face of BlackRock – we think it meets the needs of our customers and makes us more than 20% of our revenue come from long-term, less market-sensitive products and services. Our revenue portfolio will continue to shift organically as private markets, technologies and custom solutions experience higher long-term growth. We believe this will translate into higher, longer lasting organic growth, stronger market cycle resilience, and long-term shareholder value.

Customers have accepted our strategy. Our successful acquisitions and integration records are deepening our client’s relationship with BlackRock. Our ETF franchise achieved a record $390 billion net inflow, once again leading the industry. Since its acquisition of iShares, BlackRock has been leading the way in expanding the ETF market by offering innovative investment products such as bonds or cryptocurrencies, as well as proactive strategies that are more liquid and transparent.

About a quarter of our net inflows of ETFs have flowed into products launched in the past five years. Our active ETF achieved a net inflow of $22 billion in 2024, while BlackRock’s Bitcoin Exchange Trading Product (ETP) launched in the U.S. is the largest exchange-traded product in history, with asset management growing to over $50 billion in less than a year. It is the third largest fund with asset aggregation in the entire ETF industry, behind the S&P 500 Index Fund. We are innovating at the product and portfolio levels and accelerating our distribution capabilities to deliver differentiated investment solutions.

Customer demand is driving industry integration, and investors are increasingly inclined to work with BlackRock because of our capabilities as a scaled multi-asset provider. We see this in the wealth channel, and the management model portfolio is the primary way for wealth managers to seek to grow their business and better serve their customers. BlackRock has a leading model business backed by our multi-asset and multi-product capabilities. We also work across the Fortune Platform to deliver increasingly personalized products to our financial advisory partners and their clients, including through a customized standalone managed account (SMA). We offer index SMA through Aperio, which sets record for the fourth consecutive year in 2024 with net inflows of $14 billion. Last year, we acquired a tax preferential option coverage strategySpiderRock Advisors to expand our customized product suite in the wealth channel.

These clients include the world's largest asset owners, pension plans and businesses, who are deepening their ties to BlackRock. Many corporate partners believe that by expanding their relationship with BlackRock, their core businesses and shareholders will gain a positive network effect. Last year, our clients commissioned us to conduct large-scale outsourcing for more than $120 billion.

The differentiated recommendations and excess revenue potential of our proactive management strategies continue to resonate with customers, driving active net inflows of more than $60 billion in 2024. Active traffic is led by our LifePath Target Date Franchise, Outsourcing License, and our technology and data-driven system active stock strategies. We are providing long-term investment results and we believe proactive strategies can provide advantages in environments where a more dynamic allocation approach is needed.

In the fixed income sector, customers have turned to BlackRock to cope with the transition rate environment, with net inflows reaching $164 billion last year. We believe this is a significant reallocation opportunity for a record $10 trillion of off-market cash, as many investors need to obtain a 4% yield above the current currency market account in order to achieve long-term goals such as retirement.

Our customers continue to increase their allocation to the private equity market as a source of diversified and irrelevant alpha generation potential. Private equity markets had net inflows of $9 billion, which included strong demand for infrastructure and private credit strategies. Customer feedback on the recent and planned acquisitions of GIP and HPS has exceeded our own high expectations, which we expect will drive future net inflows and revenue growth in 2025 and beyond.

We have been providing Aladdin technology to our clients for over 25 years, and this technology started after a heated internal debate on whether to be available to the outside world. This is the right decision for BlackRock and our clients. The technology we pioneered as an internal risk management tool has now become the most comprehensive and integrated operating system in the industry.

In 2024, we signed some of the most important licenses in Aladdin’s history, with more than half of Aladdin’s sales involving multiple products. We completed the acquisition of Preqin earlier this year, which will add private equity market data capabilities to our products and services, aiming to increase transparency in the private equity market and ultimately increase investability.

Our connection with our customers drives record results and we are working to deliver a more comprehensive experience across the platform. Our structural growth businesses – ETFs, Aladdin, overall portfolio outsourcing, fixed income – are a solid foundation for our customers and achieving our 5% organic base fee growth target throughout the cycle. Combining our private market and dataWe position our business before we believe that it will determine the future market opportunities of asset management.

Driven our next phase of growthAs part of our ongoing efforts to assess our growth strategy, our management team and board of directors are evaluating what our industry and client opportunities will look like throughout the year. For example, five years later, in 2030, what opportunities will drive differentiated growth? How will clients allocate and create alpha gains in their future portfolios?

We believe that future investments will include the integration of more asset classes and the support of increasingly digitalization. Our customers are already doing this. They combine public and private investment, active and index investments and hope to combine all of this with leading data and analytics to better understand their portfolio. We are expanding our product and technical capabilities across our portfolio to effectively serve our clients in new and changing areas of asset management.

Fifteen years ago, when we acquired BGI, our move to combine active investment and index was the first in the industry; now, combining broad market exposure with a result-oriented portfolio has become the industry standard. Our inorganic investment initiative last year aims to achieve the same goal by connecting public and private investments to our clients. Through GIP and the upcoming HPS, we combine scaled franchise in the infrastructure and private credit sectors with the global capabilities of our public market platform. The recently completed integration of Preqin with Aladdin and eFront will better provide customers with more standardized and transparent private market data.

ETF is a proven technology that provides investment channels for retail investors who are first in the stock market and the world's largest asset owners. Our recently launched Bitcoin ETP is just the latest example, which not only provides cryptocurrency investment opportunities, but also provides efficiency and price discovery capabilities for packaging exchange-traded products. This also expands our connection with more investors. More than half of our Bitcoin ETP demand comes from retail investors, and three-quarters of them have never owned an iShares product before. Just this year, we expanded access to Bitcoin with a convenient exchange trading package and launched in Canada and Europe.

Equally, ETFs have promoted the development of European investment culture. When investors enter the capital market for the first time, it is usually through ETFs, especially iShares. Only one-third of European individuals own capital market investment, while Americans own capital market investments in more than 60%. Not only do they not participate in the growth potential offered by the wider capital market, but they often lose real returns as low interest rates on bank savings accounts are offset by inflation. We are working with well-known European companies and several new entrants, including Monzo, N26, Revolut, Scalable Capital and Trade Republic to lower investment barriers and build financial knowledge in local markets. With our current European ETF platform of over $1 trillion, which exceeds the next five issuers combined, we see a huge opportunity to expand our regional offerings and help more individuals achieve their financial goals through the capital markets.

As countries seek to build their own capital markets, we are also laying the foundation for future growth. I have been in the Middle East and Asia for a while this year, and a stronger and more prosperous local capital market has been at the heart of my discussion with local leaders. In Saudi Arabia, we are working with the Public Infrastructure Fund to encourage investment and further develop local capital markets. In India, our joint venture, Jio BlackRock, is preparing to launch a digital asset management and wealth platform.

Compound annual total return since BlackRock’s IPO until December 31, 2024As we celebrate the 25th anniversary of a listed company, we are also proud of the differentiated returns that shareholders bring. Since its IPO in 1999, our annualized total return is 21%, compared to 8% for the S&P 500 and 6% for the financial industry. It is our bold strategy and coordinated investment that drives our deep connection with our clients and delivers great returns to shareholders.

Our world-class talents are at the heart of our decades of growth and sustained performance. We regularly evaluate our talent strategy to ensure we develop a comprehensive leader with extensive business experience. Earlier this year, we promoted several leaders to new positions in the company.

After working at BlackRock for 20 years and creating multiple businesses, Mark Weedman decided to start a new chapter in his career outside the company. Mark helped shape BlackRock what we know today, including his leadership of iShares, corporate strategy and, more recently, global client businesses. Mark is my good friend and I personally am very grateful for his contribution to the company.

I am proud of the excellent leadership team we have formed, and our recent and upcoming acquisitions will bring a group of top talents to our company. Throughout the platform, we are positioning our people, creating value for our customers, and driving our business into the future.

Our Board of DirectorsBlackRock Board of Directors has been crucial to our success and development. They also play an important role in developing forward-looking strategies and expanding new markets and businesses.

We review the composition of the board every year to ensure we have sufficient background and experience to advise BlackRock’s operations, strategy and management. Last fall, after the GIP deal ended, we were delighted to welcome Bayo Ogunlesi to the board. As we are in thisWe have benefited greatly from his extensive experience in the private market by expanding our capabilities in the fast-growing market.

In March this year, the board of directors voted unanimously to nominate Gregory Fleming, CEO of Rockefeller Capital Management, and Katherine Murphy, former personal investment president of Fidelity Investments, to our board. Gregory and Katherine have extensive experience in financial services and wealth management and I am sure they will provide a different perspective to our board.

At the same time, we are honored to have Marco Antonio Slim Domit as BlackRock director who will not run for re-election this year. His service is reflected in his ability to leverage his experience in investing in various regions to provide keen insights that improve board decisions and ultimately BlackRock itself. We appreciate his service and he will be missed by the entire board and BlackRock leadership team.

BlackRock's Board of Directors will continue to guide the company to invest and innovate to better serve our customers, employees and shareholders.

When we go public, we firmly believe that the growth and depth of the capital market is very important. We hope to share our success with a wider range of investment futures, including our employees. All this is still effective. We are at the strongest turning point, 2025 is coming and I think BlackRock, our customers and shareholders will have unprecedented opportunities.