30 mins ago

5,020

Author: Arthur Hayes, founder of BitMEX; Translated by AIMan@Golden Finance

Jerome Powell and Haruhiko Kuroda have forged a deep friendship within the global central bank circle. Kuroda's BOJ governor's term ended a few years ago, and Powell often called him for comments or chatting. In early March this year, Powell held a very chaotic talk with new U.S. Treasury Secretary Scott Bessent. This left him with psychological trauma and he needed someone to talk to - let's hear what he said.

Powell: Hiroki, I really need to talk to you. I just had a very disturbing meeting with Scott.

Kuroda: I'll listen carefully?

Powell: You won't believe what happened just now. Scott called me and asked me to chat in Washington. I said, "I'm very busy; I'm going to attend the FOMC in a few days. Can we talk over the phone?" But Scott insisted. I should know something strange will happen.

Kuroda: Wait a minute—I have a suggestion before you say anything. Have you heard of Jung Central Banker Center?

Powell: No. Did you mean Jung, a psychologist, Carl Jung?

Kuroda: Yes, that's him. During his tenure at the German Bank, he created a project to help the then-renowned central bank governor deal with all the pressure and responsibilities brought about by his new role as the master of the universe. After World War II, this practice expanded to London, Paris, Tokyo and New York.

Powell: This is amazing; I always feel lonely. As the most important banker in the world, I really hope someone can talk to me about the unique pressures I face.

Kuroda: I will inform Justin that you are coming. She hosted clients at her apartment at 740 Parker Avenue.

Powell: Thank you, I plan to try making an appointment tomorrow.

Kuroda: Don't worry. At any time, there is only one customer who is suitable for her service. That is the Federal Reserve Chairman. Her existence is to serve you, and only serve you.

Jerome felt a little relaxed. He couldn't believe there was a mental health expert who specialized in serving him. He couldn't believe her address, either. He spent his entire career struggling to rent a co-op apartment at an address like 740 Park Avenue. "What the hell is going on," he thought to himself. As long as he says a word, he can bankrupt most of the financiers living in that building. They are all a bunch of conceited, over-debt bastards.

The next day,Jerome went downtown to meet Justin. After checking in at the front desk, he was taken to the private elevator and went straight to Justin's room. As soon as he walked out of the elevator, he saw a goddess. The gods of the central bank must have understood his thoughts. In addition to her appearance, the interior decoration was the same as what he wanted to decorate. Justin greeted him and signaled him to lie on Le Corbusier's recliner. There was a smoothie on the Noguchi coffee table next to him. Powell took a sip; it tasted so good that it was refreshing. Justin seemed to know him well.

Justin: That's perfect, isn't it?

Powell: I was shocked; we have never met before, but you know me so well.

Justin: For nearly a century, my company has served central bank governors. We know you very well. I think I understand why you came to me today. Often, the FED chairperson knows that we exist only after a disturbing meeting with peers in the finance or financial sector. Let me guess: You witnessed the manifestation of dominance.

Powell: You are right, you are very good at this. Yes, it caused a lot of trauma to my spirit, and after this recent experience, I felt like I was no longer like a man, no—no longer like a human.

Justin: Tell me what happened.

Powell: First of all, I was a little angry at Scott's insistence on me going to Washington, DC, New York is the capital of the empire, not Washington, DC, who the hell did he think he was!

Justin: This is a safe space, this is your space. Let it be free.

Powell: OK, so I arrived at Scott's office on time. He made me wait for an hour. asshole. Then he led me into the room and I didn't know how to react. I saw aRealBotixfemale sex doll on all fours. She had a piece of paper wrapped around her head, which read "Financial Dominance". She had another piece of paper on her lower back, which read "Fed inflation versus credibility." Scott then let me sit in a chair across from the room. A sign was written on the back of the chair, “Cuck Chair.” Scott then said to me, "Do you know what I have? I have the BBC (the Big Bessent Cock)." Then he started to Fuck dolls.

After finishing, he said, "I do this to show you who is the real power. I have the BBC, and next week at FOMC, you will start to reduce my NTD quantitative easing and announce that I will start implementing NTD quantitative easing in the near future. Do you understand? When I say it's time to give SLR (Note: supplementary levEra ratio, supplementary leverage ratio, a Fed's capital adequacy ratio indicator for commercial banks) when it is exempted from Treasury bonds, you'd better approve it immediately. ”

I was very mentally unstable, cried, and nodded to affirmation.

Justin: I guess something like this will happen. Listen, don't be sad. You're not the first Fed chairman to be fiscally swayed. It's not your fault. It's not your fault.

Powell (crying): But Justin, I'm Paul Volcker of the new era; he's my hero. When Scott fucked that doll, I tried to restore some spiritual power by talking to myself, "I'm Paul Volcker, I'm Paul Volcker." "You know what Scott said when I walked out of his office? It seemed like he understood my mind? "Bitch, you're just another Arthur Burns." ”

Justin: That's OK, I know. It's heartbreaking to be the president of the world's most powerful central bank to realize that he's fiscally controlled and blamed in person. But before you, others have experienced this. You remember the Fed merged with the Treasury Department during World War II until 1951 Year. I know you think you are independent, but deep down, you know you are not. You need to accept that. I can help you, come back every week and we can talk. But at the same time, I hope you read an Arthur Burns speech titled “The Pain of the Central Bank.” It will give you the strength to know that you never have a choice. What you are doing is right. Today’s meeting is over; you still have homework to do. I hope this will make you feel better about performing your duties at the FAP in a few days. It doesn’t matter; the universe still loves you. Let me use some crystal to heal your energy before you leave.

Powell: Thanks. I feel much better.

I feel that some incisive irony is needed to emphasize this: at the Fed’s last 3 The rules of the game have changed substantially after the meeting on global dollar liquidity held in the month. Powell has laid out a path to resuming quantitative easing, focusing on the U.S. Treasury market. When everyone is hesitating whether the impact of tariffs is good or bad, the cryptocurrency market should be glad that quantitative easing will resume this summer.

The rest of this article will focus on the mathematical and philosophical reasons for Powell’s surrender. First, I will discuss the consistent campaign commitments of U.S. President Trump and how this mathematically forces the Federal Reserve and U.S. commercial banking systems to print money and buy Treasury bonds. Then, I will discuss why the Fed never had the opportunity to maintain a tight enough currency condition long enough to curb inflation. Finally, I will discuss how Maelstrom will hold positions to profit from the recent Powell transition.

Make a promise, fulfill itI have been reading articles from my favorite macroeconomic analysts over the past few weeks. A large part of every article I read is analyzing Trump’s true intentions. Some say Trump will take tough measures to break the status quo until his approval rating falls below 30%. Others say that Trump believes that it is his mission to reshape the world order and keep the United States financial, and military order in the final stages of his term. In short, he was willing to endure huge economic pain and a sharp drop in popularity to do what he thought was good for the United States. As traders, we must remove "right" and "wrong" from the equation and measure ourselves with probability and mathematics. Ultimately, our portfolio does not care whether the United States is stronger or weaker than others, but rather whether there are more or less fiat currencies circulating globally in the near future. So instead of trying to predict Trump’s tendency, I focus on a chart and a mathematical identity.

The consistent message Trump has been sending since 2016 is that the United States has been treated unfairly over the past few decades because its trading partners have taken advantage of it. While you might think he has or will mess up his plans, his intentions have not changed. The Democrats, while not so enthusiastically demanded a change in the global order, also somewhat agreed to achieve the same change. Former U.S. President Biden continues Trump's , restricting access to U.S. semiconductor and other market areas. During the failed presidential campaign, Biden's Vice President Kamala Harris also used tough remarks against China. While Republicans and Democrats may have differences in the speed and depth of change, both parties advocate change.

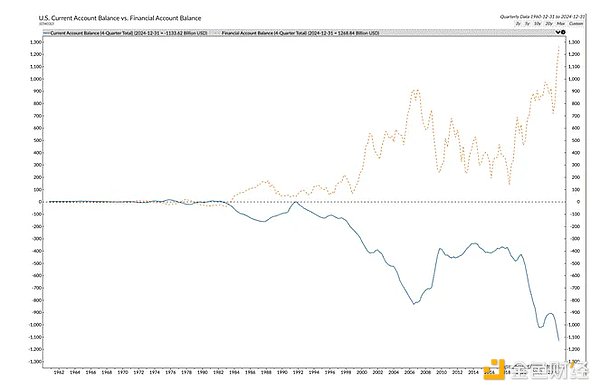

The blue line is the U.S. current account balance, basically the trade balance. You can see that since the mid-1990s, the United States imported far more goods than exports and accelerated its growth after 2000. What happened during that time? .

In 1994, the RMB was depreciated sharply, embarking on its journey as a major mercantilist exporter. In 2001, U.S. President Bill Clinton allowed him to join the World Trade Organization, significantly reducing tariffs on exports to the United States. As a result, the US manufacturing base was transferred, and the rest became history.

USDCNY y-axis inversion.

Trump supporters are those negatively affected by offshoring of US manufacturing. These people do not have a college degree, live inland, and have very few financial assets. Hillary Clinton calls them lamentable people. Vice President JD Vance affectionately called them and himself a country bumpkin.

The orange dotted line on this chart and the top is the balance of US financial accounts. As you can see, it is actually a mirror of the current account balance. and other exporters can continue to gain huge trade surpluses because when theyWhen they earn dollars by selling products to the United States, they do not reinvest those dollars. Doing so means they sell the US dollar and buy domestic currencies such as the renminbi, and then their currency appreciates, thereby increasing the price of their exported products. Instead, they use these dollars to buy U.S. Treasury securities and U.S. stocks. This allows the United States to experience huge deficits without causing the Treasury market to collapse and have the best performing global stock markets over the past few decades.

The yield on the 10-year U.S. Treasury bonds is slightly lower (white), while the total outstanding debt (yellow) has increased by 7 times over the same time frame.

Since 2009, the MSCI U.S. Index (white) has performed 200% higher than the MSCI Global Index (yellow).

Trump believes that by bringing these manufacturing jobs back to the United States, he can provide good jobs for about 65% of the population without a college degree, strengthen military strength, because sufficient amounts of weapons, etc. can be produced to fight equal or near equivalent competitors, and to bring economic growth above trend levels, such as real GDP growth rate of 3%.

There are some obvious problems with the plan. If and others, there is no dollar to support Treasury bonds and stock markets, prices will fall. U.S. Treasury Secretary Scott Besent needs buyers to buy the huge debt that must be rolled out and the ongoing federal deficit in the future. His plan is to reduce the deficit from about 7% to 3% by 2028. The second problem is that the capital gains tax brought about by the stock market is the marginal income driver. When the rich don’t make money, the deficit increases. Trump's campaign platform is not to stop military spending or cut benefits such as health care and social security. His campaign platform is to grow and eliminate fraudulent spending. So he needs capital gains tax revenue, although all stocks are owned by the rich and on average, they didn’t vote for him in 2024.

This is Trump's primary goal. Let's dig into it.

Assuming Trump succeeds in reducing his deficit from 7% to 3% by 2028, he will still be a net borrower year after year and cannot repay any existing debt. Mathematically, this means interest expenses will continue to grow exponentially.

This sounds bad, but mathematically, the United States can get out of the situation through economic growth and reduce the leverage of its balance sheet. If the real GDP growth rate is 3% and the long-term inflation rate is 2% (I don't think this will happen, but let's be generous), this means nominal GDP growth rate is 5%. If debt is issued at 3% of GDP growth, but the nominal economic growth rate is 5%, then mathematically, the debt-to-GDP ratio will decline over time. There is one problem that has not been solved: What interest rate can you raise funds for yourself?

Theoretically, if the American economyThe nominal growth rate of economy is 5%, and treasury bond investors should request a return of at least 5%. But that would significantly increase interest costs, as the weighted average interest rate currently paid by the U.S. Treasury Department for its approximately $36 trillion and growing debt is 3.282%.

Unless Becente can find Treasury bond buyers who don't care about economic gains at high prices or low returns, these numbers don't make sense. And other exporters cannot and will not buy Treasury bonds because Trump is busy reshaping the global financial and trade system. Private investors won’t buy Treasury bonds because the yield is too low. Only commercial banks and the Federal Reserve are able to buy debt at affordable levels.

The Federal Reserve can print money and buy bonds, which is called quantitative easing (QE). Banks can print money and buy bonds, which is called partial reserve banking. However, this is not that easy.

The Fed is busy with its unrealistic pursuits, trying to lower manipulated, unrealistic inflation indicators below their fictitious 2% target. They are actively removing currency/credit from the system by shrinking their balance sheets, which is known as quantitative austerity (QT). As banks performed poorly in the 2008 Global Financial Crisis (GFC), regulators asked them to mortgage their purchased Treasury bonds with more of their own equity, which is called Supplementary Leverage (SLR). Therefore, banks cannot use unlimited leverage to raise funds.

However, changing this situation and making the Fed and banks become inelastic buyers of Treasury bonds is very simple. The Fed can at least decide to end quantitative tightening, and at most it can decide to restart quantitative easing. The Fed can also exempt banks from SLR restrictions, allowing them to use unlimited leverage to buy Treasury bonds.

Then the question is, why would Jerome Powell-led Fed (he is the Fed chairman) help Trump achieve his goals? The Fed lowered interest rates by 0.5% in September 2024, blatantly helping Harris win the election, but after Trump's victory, the Fed stubbornly rejected Trump's demand to increase the amount of currency and reduce long-term Treasury yields. To understand why Powell did what he asked, let's review 1979.

The Cuck ChairNow, Powell is sitting on the "Cuck Chair" (a chair in a hotel room that extends to the bed, which is dominated by others), watching the BBC undermine the Fed's credibility in fighting inflation.

Scott Bessent is dominant because fiscal dominance is playing a role. In short, once the total debt is too large, the Fed will abandon its independence and take all necessary measures to fund it at affordable interest rates.

If you think this is new, let's take a look at the groundbreaking speech by former Fed Chairman Arthur Burns.

Western financial historians severely criticizedComment Burns created a loose monetary environment in the 1970s, leading to shocking inflation in the early 1980s. It is rumored that Powell declared within the sacred walls of the Mariner Eccles Building (FED headquarters building) that he would not go down in history as Arthur Burns of the 21st century, but as Paul Volker. The same historians also praised the inflation and the "better" of the U.S. economy driven by former Federal Reserve Chairman Volcker and U.S. President Ronald Reagan, many of which were undeserved. That's why, I guess Powell would whisper to himself when he sat on Cuck Chair, “I'm Paul Volcker, I'm Paul Volcker” while the BBC tear his credibility to pieces on the other side of the room.

In 1979, Burns delivered a famous speech entitled “The Pain of the Central Bank.” I will take a few excerpts to help understand the current and monetary situation in which Powell is located. I'm going to add some great notes to focus on what I think is the point. Sorry, not about long quotations, this speech is so prescient and so appropriate to the current situation that we must reread and learn from the lessons.

…Philosophy and thought have been changing economic life in the United States and elsewhere since the 1930s, resulting in a persistent inflationary tendency. The unique nature of inflation in our era and the reasons why central bank governors are ineffective in dealing with inflation can only be understood from the perspective of these thoughts and the environment they create.

Politicians asked me to do this.

These measures and other new policies together lay the foundation for aggressiveness—this is not only responsible for relieving suffering and preventing economic adversity, but also limiting "harmful" competition, subsidizing "benefit" activities, and correcting inequality in market forces. In less than ten years, he became the protagonist on the economic stage.

The new policy is awakening, inclusion and DEI in the 1970s. The rich always agree that the central bank prints money to save their financial assets, but they never agree that the poor also get some help. This is not to say that relief can really lift people out of poverty, but they do make people feel good and are unlikely to cause social unrest.

But the rapid growth of wealth did not bring satisfaction. On the contrary, the 1960s were an era of social unrest in the United States, just like other industrial democracy. In part, the riots reflected the dissatisfaction of blacks and other minorities over the prevalence of social discrimination and economic deprivation—a dissatisfaction that erupted in the mid-1960s “hot summers” that led to arson and robbery. Partly because social unrest is reflectedThere is a growing sense of injustice among other groups (poor, elderly, physically disabled, minorities, farmers, blue-collar workers, women, etc.). In part, it reflects the growing exclusion of existing institutions and cultural values by middle-class youth. Partly because it reflects the public's more or less sudden realization that the economic reforms of the New Deal and the recent growth of wealth have not touched upon all areas of American life (social, economic, and environmental). Interaction with all these social unrest is the increasing tensions caused by the Vietnam War.

As at that time, "prosperity" was not evenly distributed, and the people demanded measures to change it.

The interaction of behavior and private needs creates an internal motivation that leads to the escalation of both. When it set out to address “unfinished tasks” such as reducing frictional unemployment, eliminating poverty, expanding welfare for prosperity and improving quality of life in the mid-1960s, it awakened new expectations and needs.

The people got what they wanted and intervened directly in trying to solve the problems of key constituencies. "Try" is the keyword. Actual results may vary.

This interaction with citizens actively acted has produced many beneficial results. However, their cumulative effect has brought a strong inflationary tendency to the US economy. The surge in projects has led to an increasing tax burden on individuals and businesses. Even so, the willingness to tax is significantly lower than its tendency to spend.

People think that the responsibility is to solve their problems. Solve problems by spending money to do things, which leads to inflation falling into the economy.

In fact, the expansion of expenditure scope is largely due to a commitment to full employment. Inflation is widely regarded as a temporary phenomenon, or, as long as it remains mild, is an acceptable situation.

Why does the Fed tolerate an annual inflation rate of 2%? Why does the Fed use phrases like "temporary" inflation? The 2% inflation rate over 30 years combined has led to an 82% increase in price levels. But if the unemployment rate rises by 1%, the sky will collapse. It makes you sigh…

Theoretically, the Fed system has the ability to curb the infancy of inflation at any time 15 years ago or after, and today it also has the power to end inflation. At any time during this time, it can limit the money supply and create sufficient pressure in the financial and industrial markets to end inflation without delay. It did not do so because the Fed itself was trapped in the philosophy and trends that changed American life and culture.

This is the joke.The Fed should be independent, but as a sector, it tends to solve all problems philosophically, and it will not and cannot stop inflation that requires such intervention. The Fed acted as a voluntary accomplice and in the process created the inflation they vowed to eliminate.

Faced with these realities, the Fed is still willing to push the currency brakes vigorously at some point—for example, in 1966, 1969, and 1974—but its austerity stance is not enough to end inflation. In general, money is subject to the principle of suppressing the inflation process while still able to withstand a large portion of the pressure in the market.

This is exactly what Powell is doing and is doing in terms of currency. This is the definition of fiscal dominance. The Fed will do everything necessary to fund it. You can argue whether these goals are good or bad. However, Burns’ message is that when you become the Fed chairman, you agree by default to doing everything necessary to ensure you can fund yourself at an affordable level.

I know Powell and the Fed will continue to sit on the “cuck chair” because that’s what he said at a recent Fed press conference. Powell must explain why he has to lower the pace of quantitative easing, because in all respects, the U.S. economy is strong and monetary conditions are loose. I say that because the unemployment rate is low, the stock market is at an all-time high, and inflation is still above the 2% target.

The Fed said on Wednesday that the Fed will slow down its balance sheet from next month as there remains a deadlock on the issue of raising borrowing ceilings, a shift that is likely to continue for the rest of the process. – Reuters

This restriction always exists; even the highly respected former Fed Chairman Paul Volker relaxes the tightening currency when economic pain becomes too great. The following quotes are from the historical archives of the Federal Reserve:

By the summer of 1982, House Majority Leader James C. Wright Jr. asked Volcker to resign. Wright said he had met with Volker eight times in hopes of giving the Fed chairman “understand” the impact of high interest rates on the economy, but Volker clearly didn’t understand that (Todd 2012).

However, July data showed that the recession had bottomed out. Volker told lawmakers that he had abandoned his previous currency tightening goal and said the second half of the economic recovery is "very likely" to achieve - a recovery goal that Reagan has long been touted and targeted.

Even the most respected chairman of the Federal Reserve, Volker, can't resist the pressure to let go of currency. Volker has endured so muchThe U.S. fiscal situation was much better in the early 1980s, for example, when debt accounted for 30% of GDP and today debt accounts for 130% of GDP.

Powell proved last week that fiscal dominance remains. Therefore, I believe that quantitative easing (at least in terms of Treasury bonds) will stop in the short- to medium term. Powell further said that while the Fed may maintain a reduction in mortgage-backed securities (MBS), it will buy Treasury bonds in net. Mathematically, this can keep the Fed's balance sheet unchanged; however, this is direct Treasury QE. Once officially announced, Bitcoin will rise sharply. Additionally, the Fed will provide banks with SLR exemptions due to requirements from banks and the Treasury Department, another form of quantitative easing for Treasury bonds. The reason is simple, because if not, the math I posted above will not work. Even if Powell hates Trump, he cannot stand by and let the United States be crumbling.

The following are some direct quotes from Powell and Becente, supporting my predictions for the future.

As follows Powell talked about what I said about QT Twist (QT reversal):

We will stop net reduction at some point…we have not made any decisions about it yet. We strongly hope that MBS will shrink from our balance sheet at some point. We will be watching closely to keep MBS down, but keep the overall balance sheet size unchanged…at some point… we haven’t reached that point yet.

The following is what Bessent talks about SLR on the recent All-In Podcast:

So, I think if we remove the so-called supplemental leverage, it has the potential to become a constraint on the bank. We might actually reduce Treasury yields by 30 to 70 basis points. Each basis point is equivalent to $1 billion per year.

Finally, let us climb the wall of tariffs. When asked about his views on the impact of Trump’s proposed tariffs on inflation, Powell said his basic forecast was that any tariff-induced inflation would be “temporary.” The belief in "temporary" inflation allows the Federal Reserve to continue to be loose even if inflation soars due to a sharp increase in tariffs. Tariffs, at least for assets that rely solely on legal liquidity, are no longer important. Therefore, I no longer care about Trump’s self-proclaimed “Liberation Day” on April 2, or how high (if any) Trump will raise tariffs.

Dollar Liquidity MathematicsFeder Chairman Jerome Powell said at a press conference after the meeting that the current prospectsYes, any price increase caused by tariffs can be short-lived.

When asked if the Fed is “back to the transition period again,” the central bank leader replied, “So I think this is a basic situation. But as I said, we really can’t know that. –CNBC

Remember, we are concerned about the forward-looking changes in USD liquidity relative to previous expectations.

Treasury QT Early Progress:

Dollar QT Reduction:

Treasury QT Reduction:

Treasury QT Reduction:

Moon 1:

Dollar QT Reduction:

Moon 50 $100 million

Net:

Dollar liquidity is increasing annualized $240 billion

What is the effect of the QT reversal:

Save up to $35 billion in monthly MBS

If the Fed's balance sheet remains unchanged, then they can buy:

Maximum $35 billion in monthly Treasury bonds or $420 billion per year

We know that starting April 1, an additional $240 billion will be generated relative to the dollar liquidity. In the near future, I believe this will happen at the latest in the third quarter of this year, with $240 billion rising to an annualized $4200 $100 million. QE will not stop for a long time once it starts; QE will increase as the economy needs more money printing to remain stable.

Treasury in actionTo perfect my dollar liquidity analysis, I can’t forget some specific questions about how the Treasury will fund it. Specifically, will the Treasury supplement its general account (TGA) after the debt ceiling is raised?

Currently, the TGA is about $360 billion, down from $750 billion at the beginning of the year. TGA is used to fund due to the debt ceiling being reached. In the past, once some last-minute transactions raised the debt ceiling, the TGA would refille. This is negative dollar liquidity. But it is a bit silly to hold such a large cash balance; during Yellen’s tenure, the TGA targeted balance of 8,500 $100 million. Given that the Fed can print money at will, the Fed should of course lend money to the Treasury when needed. The Treasury can issue some Treasury bonds to pay the Fed. This reduces the financing demand. This will require more coordination between the Fed and the Treasury, although the heads of each organization support different factions. But now we know that Powell must bow to the BBC, so I think in the next quarterly refinancing announcement (QRA) in early May, it is very likely that the Treasury predicts that TGA will not increase relative to the current level at the time of QRA is released. Once the debt ceiling is raised, this will eliminate any negative dollar liquidity shock.

2008 Global Financial Crisis Case StudyBoth stocks and gold have responded positively to the increase in statutory liquidity.However, stocks need a polite legal fiction to exist. Therefore, during a deflationary depression, when the system's solvency is questioned, stocks may not respond as quickly to the injection of statutory liquidity as anti-establishment financial assets like gold. Let’s evaluate how the S&P 500 and gold performed during the peak and recovery periods of the 2008 global financial crisis. This case study is important because I want to make sure I am honest with myself. Just because I believe that US dollar liquidity has turned sharply to positive does not mean that negative economic headwinds will not adversely affect the price trends of Bitcoin and cryptocurrencies.

The S&P 500 (white) and gold (gold) indexes are 100 starting October 3, 2008. This is the day when the troubled asset rescue plan (TARP) rescue plan was announced. The plan failed to calm the damage caused by Lehman Brothers' bankruptcy to the market, and both stocks and gold fell. When TARP proved insufficient to stop the collapse of the Western financial system, Federal Reserve Chairman Ben Bernanke announced a large-scale asset purchase plan in early December 2008, now known as quantitative easing (QE1). Gold began to rise, but stocks continued to fall. The stock market did not bottom out until shortly after the Federal Reserve began printing money in March 2009. By early 2010, after Lehman went bankrupt, gold was up 30% and stocks were up 1%.

Bitcoin did not exist in 2008. But now it exists.

Bitcoin Value = Technology + Fiatcoin Liquidity

Bitcoin Technology is effective and there will be no significant changes in the near future, for better or worse. Therefore, Bitcoin trading is entirely based on the market's expectations for future fiat currency supply. If I'm right about the Fed's shift from quantitative easing to quantitative easing, Bitcoin hit a local low of $76,500 last month and now we're starting to climb to $250,000 by the end of the year. Of course, this is not an exact science, but taking gold as an example, if I had to bet I thought Bitcoin would hit $76,500 or $110,000 first, I would bet the latter.

Even if the U.S. stock market continues to fall due to tariffs, earnings expectations plummeted or weaker foreign demand, I believe the possibility of Bitcoin continuing to move higher is still high.

Maelstrom knows the pros and cons, so deploys capital with caution. Instead of using leverage, we buy in a smaller proportion relative to the size of our entire portfolio. I wish I had a bigger scale when the market was up, but I was glad that this was not when the market was down. We have been buying bitcoin and junk coins for various prices between $90,000 and $76,500. The speed of capital deployment will accelerate or slow down, depending on the accuracy of my predictions. I still believe Bitcoin can reach $250,000 by the end of the year, because now the U.S. Treasury SecretaryHaving taken over Powell's position, the Federal Reserve will inject US dollars into the market. This allows the People's Bank of China to stop tightening domestic currency conditions in order to defend the dollar against the RMB, thereby increasing the net amount of the RMB. Finally, Germany decided to build another army that paid for the military with the printed euro, and all other Europe had to respond, using the euro, because they were afraid of reappearing in 1939.

Investment (machine) begins!