36 secs ago

6,359

Author: David C, Bankless; Translated by: AIMan@Golden Finance

New stablecoins continue to emerge, heralding the arrival of a new era in which asset managers, banks, and even the presidents coexist with us on the chain.

To be honest, this is not surprising. Stablecoins, like BTC, have long been regarded as one of the basic use cases for cryptocurrencies. While they feel a little "dry" in cryptocurrency products, they do work and the market continues to expand.

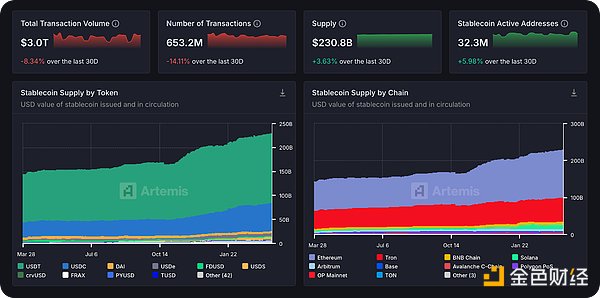

In 2024 alone, fiat-backed stablecoins grew by 53%, with over $200 billion in circulation (of which Ethereum accounts for 58%) and contributed to $5.8 trillion in on-chain transaction volume.

Source: artemis

This growth has brought stablecoins far beyond DeFi speculation and entered the mainstream business sector, with large tech and fintech companies such as PayPal, Venmo and Stripe entering the blockchain space with us through stablecoins. Plus, the universally favorable legislation that Congress is introducing – from the GENIUS Act to the STABLE Act of 2025. Everything is almost ready.

Everyone wants to get a piece of the pie. Last week's announcement made the enthusiasm even more:

Financial giant Fidelity (asset management scale of $5.9 trillion) is expected to launch a currency pegged to the US dollar.

Trump-backed World Liberty Fi has launched the stable currency USD1 on Ethereum and BSC.

Wyoming announced that it will issue its own state stablecoin, which is currently under test and is expected to be launched in July.

Custodia Bank and Vantage Bank Texas launch the first stablecoin issued by Bank of America on a license-free infrastructure.

All of these moves emphasize the same story: Stablecoins have quickly proven themselves to be a superior payment method, and institutions see golden opportunities to gain value by issuing their own stablecoins.

Today, let's dive into why stablecoins are a major opportunity, why institutions are joining, and how to grasp this trend!

Why Stablecoins WinBefore we discuss the advantages of institutions, let’s quickly review how stablecoins have become an easier and faster payment tool—especially compared to traditional payment methods that are slow, expensive and costly.

Traditional payments are dominated by middlemen: Credit card networks, banks and other intermediaries receive nearly $2.4 trillion in revenue each year, with a fee of 1.6-3% per transaction.

Stablecoins provide a more convenientA good alternative: One cent stablecoin transaction fee is a huge advantage for anyone who remits across borders compared to the $12 or above transaction fee for traditional remittances, which has not yet taken into account faster and easier transfers.

Stablecoins as inflation hedging tools: In high inflation rates, stablecoins have become the core use case for savings accounts because their value is linked to relatively stable assets such as the US dollar. This stability helps individuals avoid sudden devaluation of their currency, conduct daily transactions with lower volatility, and store wealth in a more reliable way—especially in places that are difficult to access by banks or traditional financial systems.

As more people, whether merchants, asset managers, or states, realize that our outdated, extremely complex payment systems are wasting billions of dollars, this convenience, accessibility and cost savings are the reasons why stablecoins are increasingly being accepted and used.

Source: a16z crypto

Why institutions need stablecoinsSo institutions at the heart of traditional payment systems quickly realized that they had to upgrade to compete with fintech companies—because while there could be a lot of gains, if they were late, the losses would be even greater.

For example, Tether made $13 billion last year, while Circle made $825 million in just half a year, mainly relying on holding customer deposits in low-risk, profitable assets such as money markets or government bonds. By launching their own stablecoins, banks and financial institutions can take advantage of this profit model to directly earn money from customer deposits.

Better yet, institutions can offer reduced fees, favorable loan rates or brand new financial products to create a seamless experience within their platform, inspiring users to trade with their stablecoins and keep returning to their products, thereby promoting a loyalty cycle.

Now, financial institutions no longer regard payments as pure cost centers, but can transform them into profit centers. For example, banks can adopt classic fintech strategies such as sharing reserve earnings (floating earnings) with merchants and partners, just as Visa rewards United and Chase to attract credit card users. It's a win-win situation: institutions build larger deposit pools that can be used to earn income and increase product supply, merchants earn revenue by transferring transactions from credit cards to stablecoins, and customers benefit from loyalty-driven incentives that promote widespread adoption and retention.

Parking companies/fintech companies launch their own stablecoins are several reasons - making deposits more useful (= more sticky) - retaining interest incurred (rather than handing over to another issuer) - providing instant settlement for users/merchants - reducing merchant exchanges/fraud costs https://t.co/neva6fsLx7

— ria bhutoria (@riabhutoria) September 26, 2024

In addition to increasing profits, institutions can also significantly reduce the costs of intermediaries such as Visa and Mastercard, which typically cost 1.6-3% per transaction. Natively issued stablecoins can settle payments at almost zero cost, greatly improving profit margins and allowing them to provide merchants with cheaper and more competitive payment solutions. In addition, instant settlement of stablecoins reduces the risk of fraud, allowing banks to avoid expensive fraud protection services, which traditional payment networks usually bundle in fees that are passed on to users.

In addition, institutions that issue stablecoins can expand to previously underserved markets. Stablecoins excel at instant, low-cost international payments—it is its prominent use case—which enables issuers to obtain high-profit cross-border operations and remittance flows. These markets used to be fragmented and costly, but now they are suddenly becoming easy to enter and profitable, providing banks with a new path to global competition and revolutionizing the global landscape.

Lastly, with rapid increase in regulatory clarity (such as the EU’s MiCA and the emerging US STABLE and GENIUS Acts), institutions have significant regulatory advantages. Banks and regulated asset managers can issue compliant, audited stablecoins, allowing them to gain immediate credibility among institutional users who are cautious about cryptocurrency native issuers. Bank-issued stablecoins will be viewed as safer, more trustworthy, and in line with evolving global standards.

In short, stablecoins provide institutions with a completely new set of tools that enable them to compete in a rapidly growing financial environment: from obtaining billions of dollars in reserve earnings, cutting expensive middlemen, increasing merchant profits, to driving strategic loyalty incentives and seizing new market opportunities. The question now is not why institutions are rushing to launch stablecoins, but why they don't do it?

How to seize stablecoin opportunitiesEven if you are sure that stablecoins will reshape global finance, there is no simple "stablecoin index" for investment. Instead, we only have indirect ways to do long.

If you are optimistic about the adoption of stablecoins, here are some options to explore:

Stablecoin-related forecast marketsWebsites like Polymarket allow you to bet on whether institutions such as Bank of America and even states such as Wyoming will issue their own stablecoins soon. Participating in it or monitoring a new stablecoin is a good choice, but not perfect.

Earn stablecoins APRDeFi lending, CEX stablecoin income, DeFi liquidity provision, Restaking etc., such as Aave, MakerDAO, Pendle, Kamino, Drift, Hyperliquid, etc.

Purchase tokens with stablecoin exposureTokens pegged to stablecoin issuances (such as ENA, SKY or MKR, AAVE and FXS) may be another good choice.

For this path, though, it must be remembered that cryptocurrencies are not an efficient or fundamentally driven market, meaning that the growth of stablecoins for these tokens may not be reflected in their prices.

If you want to go this path, be sure to choose stablecoins-related tokens that need to be located on chains with large amounts and supply of stablecoins, such as Base, Solana, Ethereum and Tron.

Early unissued stablecoin projectsEarly tokenless stablecoin projects provide unique “farming” opportunities, essentially rewarding for early stages. Projects worth noting include Cap Money, Perena, Resolv, Level, Metastable and Rings. However, given that these projects are still in their early stages, you are taking smart contract risks, so keep this in mind. In addition, it is definitely a good thing to pay attention to on-chain protocols with a large number of stablecoins.

Monitoring new opportunitiesPopular stablecoins that have not yet issued tokens (Q1 to Q2 2025)

@capmoney—MegaETH USD

@Perena—Solana native USD

@ResolvLabs—DN stablecoin with thicker reserve funds

@noble_xyz—Cosmos Short-term US Treasury Dollar

@levelusd—Lend/Resolution USD

@Theo_Network- Hyperliquid DN USD

@Rings_Protocol- Sonic Earnings USD

@USDai_Official- Depin backed USD (?)

@hydration_net- DOT USD

@Corkprotocol - Depeg Insurance Protocol

@veda_labs- Yield Infra made easy for launching USD

Circle is the giant behind USDC that has applied for listing and may soon provide direct stock market exposure. Considering they received 8.2 in just six months last yearWith a profit of $500 million and more regulatory compliance than Tether, it is likely to be the first choice for betting on stablecoins. This is the closest approach to the rising dominance of direct investment stablecoins.

In addition, Peter Thiel-backed Plasma is a new USDT-centric Bitcoin sidechain that could be another monitoring option if they launch a token. And if Tether doesn’t have an IPO, it might be one of the best ways to bet on top stablecoins to grow.