45 mins ago

5,751

Author: HashKey Capital Translation: Shan Oppa, Golden Finance

"Ethereum is dead".

This argument has been rampant in various communities and media recently. In fact, Vitalik himself also used this sentence to analyze the various difficulties Ethereum experienced at the previous Wanxiang Blockchain Conference. The audience understands that Vitalik is self-deprecating—and perhaps even jokingly mocking the ongoing FUD (fear, uncertainty, doubt) surrounding Ethereum. But the difference this time is that many people are beginning to believe that Ethereum may have passed its peak.

ETH price performance has been lower than expected in the past year. The ETH/BTC ratio declined throughout 2024, and competitive networks steadily erode Ethereum's market dominance. It is worth noting that Solana surpasses Ethereum in terms of the number of active DEX users and transaction volume. The worrying decline of Ethereum prompts us to examine the broader macro environment and competitive landscape.

Comprehensive analysis of the current situation in EthereumWe will review its performance and competitive landscape before analyzing specific issues in Ethereum.

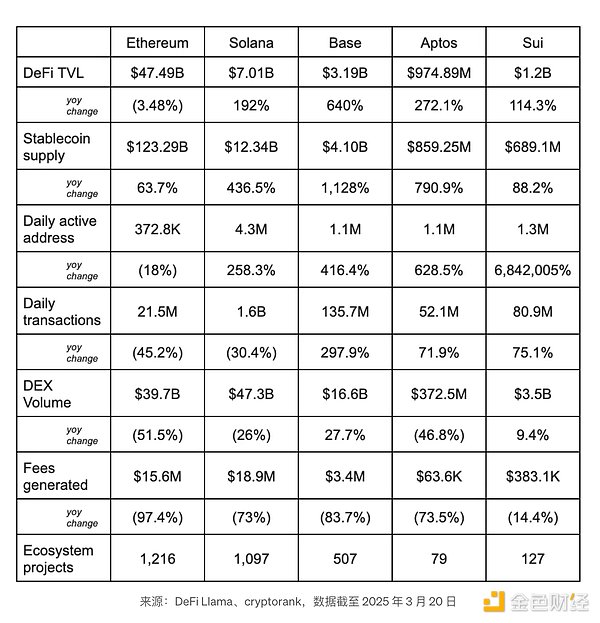

On-chain activityWe compared the performance of the L1/L2 network and evaluated it based on indicators such as TVL, stablecoins, active addresses, and transaction volume.

Ethereum's TVL still ranks first with US$47.49 billion, with a stablecoin supply of US$123.29 billion, which is also an order of magnitude higher than Solana. Ethereum’s vibrant ecosystem has over 1,216 projects, demonstrating the network’s maturity, although Solana follows closely behind. However, Solana's trading volume surpassed Ethereum with $47.3 billion. Despite the higher TVL, the relatively low transaction volume highlights the different user profiles: Ethereum users tend to passive DeFi mining, while Solana users prefer positive speculative trading.

Blockchain NetworkIf we compare Solana, Sui and Aptos horizontally, Ethereum is still the most decentralized blockchain network after Bitcoin. In 2025, the number of active validators on Ethereum remained at around 1.05 million. In comparison, it was about 980,000 in the same period last year, an increase of about 7% year-on-year. From the etherThe technology roadmap of the Purge shows that it is still working to maintain a balance between decentralization and scalability.

Compared with March and April last year, there was a significant decrease in validator entry queues, reflecting a decline in staking demand. Although staking ETH has stabilized, the persistent positive entry queue supports strong network security across the ecosystem.

DevelopersEthereum continues to lead with the largest developer base—this number will be even higher if developers built on Layer 2 and related EVM-compatible chains are included. Additionally, discussions on the ethresearch forum remain active, highlighting the vibrant community of developers on Ethereum.

According to Electric Capital 2024 report:

In 2024, the number of mature developers in Ethereum increased by 21%, while the number of developers with shorter term life decreased.

56% of Ethereum ecosystem developers are now working on L2, up from 25% in 2022.

Ethereum has the largest number of developers despite the Dencun upgrade and increasingly turning to rollup. However, in L2, Base has the most active developers.

According to a16z Crypto statistics, Ethereum is still the most favored ecosystem for developers, and 20.8% of crypto projects are built on Ethereum. Solana and Base ranked second and third respectively, accounting for 11.2% and 10.7% of crypto companies, respectively.

Ethereum has experienced a period of relatively stable status, and has not yet shown signs of weakness until recently. Various views emerged - from criticizing the Foundation's inaction to concerns about L2's "vampire attack". Below, we will explore Ethereum's performance and future growth from multiple perspectives.

Is Ethereum's low performance and high cost hindering?Had Meme's development been hindered?Solana's success in this cycle is largely due to its strategic fit with the Meme coin wave and is positioned as the most important Meme coin issuance base. Many new users entering this cycle have chosen Solana over Ethereum, and even US President Trump has chosen to issue his Meme coins on Solana (see our previous report for more information). Meme currency traders are attracted to Solana because of its significantly lower transaction fees and excellent throughput – at its peak, it processes 2909 transactions per second, compared to Ethereum’s 62.34 TPS.

This raises the question: Does Ethereum's relatively limited performance and high gas fees hinder retail Meme currency traders, prompting them to migrate to high-performance chains such as Solana?

But this argument is easily refuted.

Authentic, Ethereum may not be able to provide a low-cost and seamless experience for retail investors who want to trade fast Meme coins. But this seemingly rhetorical question can be refuted by some factual counterexamples. The emergence and success of Meme can be attributed to the increasingly mature DeFi ecosystem that facilitates seamless token creation and transactions. As the most mature smart contract platform, Ethereum laid the foundation for the booming development of DeFi activity and its rapid growth in what is now known as DeFi Summer. In addition to Meme currency trading, DeFi also includes various sub-fields such as lending, pledge, liquid pledge and on-chain asset management.

During the DeFi Summer in 2020, the gas fee is much higher than the current level, and the final block confirmation time is relatively long. In addition, competitive Layer 1 networks at the time (such as Binance Smart Chain (BSC)) also prioritized EVM compatibility while providing lower transaction fees. As a pioneer in shaping the DeFi landscape, Ethereum has benefited a lot, and compared with other competitive chains, it has obtained the highest DeFi TVL. Although the huge TVL looks stagnant now, it has huge growth potential if it is reignited.

Even for problems that have been plagued by Ethereum for a long time, such as state explosions, analysis shows that it will not greatly affect Ethereum's performance.

So, what's the problem? The most critical factor is not technical, but non-technical—For example, the strength and overall culture of the community.

CommunityThe core developers of Ethereum generally dislike Meme. This emotion is clearly reflected in Vitalik's article. In addition to publicly expressing resentment to Meme culture, this may also reflect a broader shift in the mindset of ecosystem stakeholders.

On the surface, the Ethereum ecosystem seems to prioritize value creation in moral and social significance rather than pure profit-driven. This idea is not completely new, in fact, it has been reflected during the DeFi Summer period (for example, Uniswap refused to yield farming, Vitalik donated his $1 billion Shib airdrop, etc.).

This cycle shows that having Meme-centric, consumer-oriented applications (Ethereum is currently inferior to Solana in this regard) plays an important role in attracting users and driving network revenue. While some believe that the Ethereum ecosystem does not require user activity that is purely Meme or gambling-driven, if rollup fails to support mainstream non-gambling applications such as gaming or social platforms, this may limit wider adoption and may exacerbate downward pressure on ETH prices.

The failure of the "Fat Protocol" theoryIn addition to the Ethereum community's exclusion of Meme, changes in the industry cycle have also had a significant impact on the success of Ethereum.

The crypto industry widely accepts the "fertile protocol" theory—that is, the infrastructure layer (including but not limited to L1 and L2) captures most of the value generated by dApps built on it due to its critical role in value transmission, settlement and security. Therefore, infrastructure projects tend to obtain higher valuations in the capital market compared to application-layer projects. This is in sharp contrast to the traditional Internet model, where the latter protocol design does not have a built-in value transfer mechanism. Therefore, most of the economic value of Web2 has historically accumulated at the application layer, not within the protocol stack.

But this time the situation is different. An important feature of this cycle is the low return on investment for ultra-high value infrastructure projects. One reason is that the industry has carried out excessive infrastructure construction in the past few years, which may be the hope that "there will be more cars in the future after the road is widened." However, this cycle has produced few breakthrough applications on Ethereum—whether in DeFi, NFT or gaming—and the Meme project has become a major destination for retail investors.

In view of the high valuation of projects in the market before, we believe that the recent pullback is necessary for a broader market recovery. The industry has also begun to recognize the community value behind Meme to a certain extent, which is a correction to the previous lower community sentiment. In any case, this cycle has once again sparked the ongoing debate on the distribution of value between protocols and applications, while also underscoring the importance of strong consumer-facing products that can grow and maintain a user base by providing low barriers to entry.

Is Ethereum lagging behind in this cycle?Does this mean that Ethereum, known for its proven security and strong infrastructure, is no longer suitable for today and future consumer-centric landscape?

Even a market that is completely centered on the interests of users, it can be in trouble, especially when profit-driven motivations, such as those that drive most Meme currency transactions, are damaging the ecosystem.

Analyses like "Everything is a Ponzi scheme" tend to reduce all on-chain activities to the logic of on-chain casinos. Many industry professionals have formed a clear survivalist or even nihilistic view. Some people also believe that Ethereum cannot keep up with current community-based gameplay and is "difficult to reality", thus lagging behind networks such as Solana in this cycle.

Practitioners who have been involved in the industry for a long time may find the statement of "on-chain casino" extremely familiar - indeed. A similar pattern appeared in EOS in 2018. At the time, when people talked about "Dapp", they usually refer to gambling applications, blockchain games built on EOS, rather than early DeFi protocols that quietly formed on Ethereum. Due to EOS's high performance and low handling fees, these applications have created many "magic projects" that generate $3 billion in turnover in 30 days. EOS also vigorously promoted its DPoS-based consensus mechanism, claiming that one day it could support millions of transactions per second - an idea that sparked huge imagination and hype at the time.

However, when EOS cannot scale network capacity as it claims, its decentralization (21 supernodes) sacrificed for performance is gradually exposed. As the overall market cools down and its self-interest effects weaken, these centralized problems began to surface and were completely left behind at the beginning of DeFi Summer in 2020; EVM chains became the de facto standard for dApps.

In view of the maturity of infrastructure at that timeThe degree is relatively low, and the development and adoption of consumer-oriented applications can be said to be unsatisfactory at best. Currently, blockchain infrastructure has made a leap forward, enabling it to better support high-performance consumer applications, which could eventually translate into higher ROI for the underlying protocol.

Did the PoS transformation cover up the Ethereum problem?Ethereum's price performance has been relatively stable since its transition to PoS. Some believe that this shift has led to greater centralization and loss of miner support – factors that lead to its current challenges. However, this statement deserves a closer look.

If governance centralization is a concern, it is worth noting that even before the merger, Ethereum's core developers had long had a significant influence on network upgrades. From hard fork rollback after DAO events to strong push from EIP-1559, centralized decision-making has been part of Ethereum's history.

We will not repeat the 2021 analysis of EIP-1559, but will study the impact of EIP-1559 in the current rollup-centered Ethereum environment.

EIP-1559 proponents believe that during a period of increased activity in Ethereum network, the mechanism will burn more ETH, creating a deflationary environment that positively affects Ethereum price dynamics. However, when most of the activity on Ethereum moved to L2, Ethereum played a role similar to the “central bank”, taking on more DA roles, while most of the retail activity gradually moved to rollup. At this point, the EIP-1559 model may begin to “counterproductive” ETH, causing the overall supply to change from deflation to inflation, especially if the amount of ETH burned does not exceed the issuance rate. This is particularly evident after the Dencun upgrade, as Ethereum has difficulty maintaining deflationary supply.

L2 is a "vampire attack"After discussing the issue of L2, we can see to a certain extent that the community's criticism of L2 as an Ethereum's "vampire attack" makes sense. L2 takes advantage of Ethereum's security, but L2 does not pay high DA fees on Ethereum. This causes the DA and settlement demand generated by rollup to not support Ethereum's price as DeFi in the previous cycle. Therefore, it is difficult to capture the added value brought by L2 users.

This cycle lacksSustainable narratives limit the profit opportunities of retail users. Meme coins related to emotional value and community attention have become the biggest beneficiary as retail users turn their attention to this sub-field. Networks such as Solana and Base perform better than Ethereum, so they are ideal for developing large-scale consumer applications.

At present, Ethereum seems to be at a crossroads, requiring careful decisions that match scalability and value accumulation. As the number of users and applications on L2 increases, demand and prices for Ethereum are expected to rise. This situation is similar to Solana, where transaction fees are significantly reduced. However, because users need SOL to execute transactions, the demand generated by Meme currency transactions has greatly pushed up the price of SOL.

In addition to the "vampire attack", the interoperability problem between L2 further disperses asset liquidity and weakens user attention.

As we pointed out in our previous report, the Ethereum ecosystem includes rollup-based, shared sorter, cross-chain intent, ERC-7683 and ERC-7802. Recently, the Cosmos community has been actively promoting IBC v2 to provide mature cross-chain solutions for Ethereum.

Ethereum FoundationIn addition to the above concerns about Ethereum economic model, value capture and technology roadmap, the Ethereum Foundation (EF) has also become the target of major criticism recently.

Let's take a look at the main example of EF selling tokens in the first place. From a rational point of view, selling tokens is necessary to maintain operational needs. However, every time this happens, it also represents another downside that hinders Ethereum price growth. Ultimately, much of the community’s criticism stems from dissatisfaction with whether the Ethereum Foundation really prioritizes Ethereum’s long-term price stability.

The problem may again lie in the guidance culture of EF. Under Aya Miyaguchi's management, EF prefers to build Ethereum as a nonprofit network for "human coordination" rather than short-term value. Meanwhile, within the team, Aya doesn't want people to compete and win. Under this guidance, the Ethereum community is clearly at a disadvantage when competing with networks such as Solana in terms of execution and competitive efficiency.

Nevertheless, it is worth mentioning that the Ethereum Foundation has recently recognized the seriousness of the problem. They have begun to introduce the originalPeople outside the EF system, such as Tomasz Stańczak, served as ED to improve the culture of the Ethereum Foundation.

In addition, the Ethereum Foundation (EF) has shown signs of being more sensitive to community sentiment. Instead of selling ETH, they began to use treasury assets for productive purposes—such as depositing ETH into AAVE, etc. These actions have not reached the level of pledge as EF expressed concerns about being forced to take sides during a potential fork. However, recently, EF said it intends to explore staking opportunities again with these initiatives, which is considered a positive signal for ETH prices.

On the other hand, according to Haseeb's observations, EF is also reducing its focus on research and academia and increasing its interaction with founders. In addition, based on feedback from some Ethereum wallet projects, EF is strengthening its connection with products directly targeting end users (such as wallets) to understand the needs of average users. Together, these developments represent positive progress in the Ethereum community.

ConclusionEthereum faces various technical challenges, including the "cannibalization" of Layer 2, as well as the impact of MEV on user experience and the fuzzy market positioning of account abstraction (AA). However, besides these technical issues, perhaps the most critical factor affecting Ethereum's future is its community and culture. They have a significant impact on Ethereum’s sentiment and beliefs.

As the Ethereum Foundation plays a more active role in supporting the ecosystem, it remains to be seen whether Ethereum can reverse its recent decline.