50 mins ago

5,751

Written by: Glendon, Techub News

Following the Hyperliquid liquidation incident caused by the "Hyperliquid 50 times leverage whale" on March 12, on the evening of March 26, Hyperliquid encountered another "lightning sniper" targeting its liquidity and governance model.

A trading team removed the margin by copying the operation of "Hyperliquid 50 times leverage whale", trying to force Hyperliquid's HLP vault to take over the huge loss position. The difference is that this trading team did not choose Bitcoin and Ethereum, but instead focused on the low liquidity and easy-to-manipulate Meme coins JELLYJELLY. Although this open market manipulation failed to completely succeed due to the urgent intervention of the exchange, it once again exposed Hyperliquid's multiple loopholes in governance centralization, liquidity management and market manipulation defense.

Just the day before the incident, Polymarket, the cryptocurrency forecast market, was also controversial due to the centralization problem presented in a "large-investment governance attack". As the important issue of "decentralization" has once again sparked heated discussion, as industry participants, how should we view the phenomenon that decentralized trading platforms are not "decentralized" enough? First, let’s understand the causes and consequences of these two incidents.

Hyperliquid was "sniped" and "drag the network cable" in a critical momentIn the end, this carefully planned "Mingpai sniper" was not complicated. On March 26, the trading team first issued 430 million JELLYJELLY short orders on Hyperliquid with a margin of 3.5 million USDC on the address starting at 0xde9, which was worth about $4.08 million at the time and the opening price was $0.0095.

The team then began buying JELLYJELLY tokens in large quantities to drive up the spot price and withdrew $2.76 million in margin after closing 30 million JELLYJELLY short orders at $0.0103. In this way, the team successfully threw 398 million JELLYJELLY short orders to Hyperliquid, causing it to trigger the automatic liquidation mechanism.This forced the HLP vault to take over. Under this operation, the floating loss of the HLP vault once exceeded US$13 million.

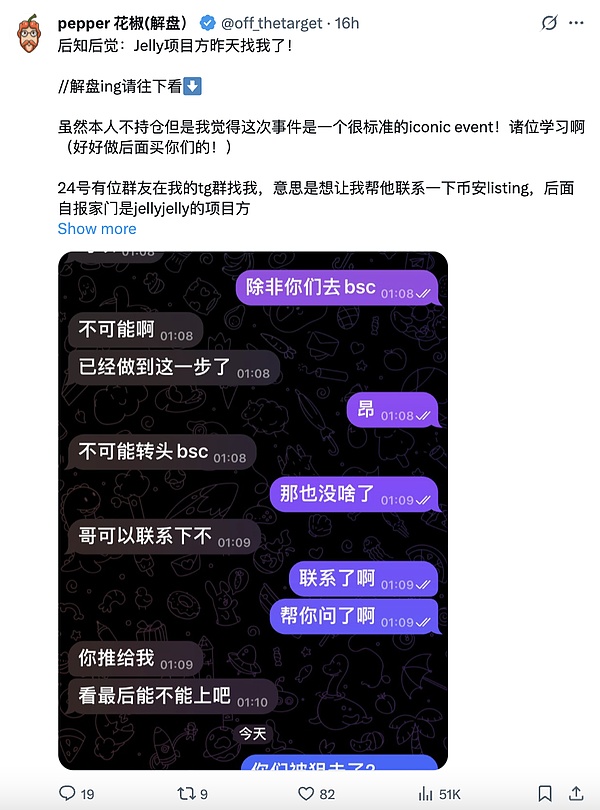

The reason why this incident was carefully planned and planned for a long time is that according to the cryptocurrency KOL "pepper Huajiao (Explanation of the Disposal)", as early as March 24, someone called himself the "jellyjelly project party" contacted him to help promote JELLYJELLY's listing on Binance. What is unexpected and reasonable is that not long after that night, OKX and Binance launched JELLYJELLY perpetual contract trading pairs one after another. Affected by this, JELLYJELLY's price rose rapidly, from $0.0095 at the time when it opened its position to above $0.066.

According to Aunt Ai, if the opponent raised the price of JELLYJELLY to around US$0.17, the HLP vault would face liquidation and lose $240 million of its holdings. And what's bad is that as the price of JELLYJELLY continues to rise, HLP vault funds are continuing to be lost.

At the critical moment when the currency price gradually approached the liquidation line, Hyperliquid took action. However, there was no exciting game that people imagined. Hyperliquid directly paused the price update of JELLYJELLY by "dragging the network cable" and forced the token to be removed. Hyperliquid then forced a short statement with the initial opening price of $0.0095, while JELLYJELLY's spot price was about $0.05.

Hyperliquid tweeted the explanation: "After the discovery of evidence of suspicious market activity, the validator group held a meeting and voted to remove the JELLY contract. All users will receive full compensation from the Hyper Foundation except for the illegal address being marked. This will be automatically completed in the next few days based on on-chain data. No invoice is required. The specific method will be shared in detail in the subsequent announcement. Please note that as of this writing, HLP's 24-hour profit and loss was approximately USDC. We will make technological improvements and learn lessons to make the network stronger."

After this, Hyperliquid seems to have successfully resolved this liquidation crisis. In contrast, JELLYJELLY prices fell sharply, and the GeckoTerminal market showed that as of the article, JELLYJELLY has fallen to $0.0197. So, is Hyperliquid really going through the difficulties and is it safe?

Perhaps, the subsequent impact of this matter will still bother Hyperliquid for a long time.

First of all, for Hyperliquid, the most direct change is that users withdraw funds due to panic, which intensifies liquidity pressure, resulting in the platform's net outflow of USDC reached US$140 million within hours after the incident, and TVL fell from US$2.5 billion to US$2.07 billion in the past 30 days. Secondly, this incident also reveals many problems with Hyperliquid, such as liquidity design flaws, reliance on vaults as competitors, and insufficient risk control for high leverage. Although the giant whale liquidation incident has exposed similar vulnerabilities, Hyperliquid's improvements have failed to effectively prevent secondary attacks.

And the most profound impact is the collapse of Hyperliquid's decentralized narrative. Hyperliquid urgently removed the tokens and ignored the forced settlement of actual market prices. Although it avoided huge losses from the vaults and users, it also caused users to question its decentralization and fairness of the rules.

In particular, the Hyperliquid Verifiers Committee is completely controlled by the official foundation. It seems to be decentralized voting decisions, but in fact it lacks community participation. According to Spreek's tweet, all the voting validators in Hyperliquid's incident came from the Hyper Foundation. This move also highlighted the centralized nature of Hyperliquid's governance, and even led to it being called "CEX with DEX skin" by the community.

In addition, in this incident, retail investors undoubtedly became the biggest victims. According to Coinglass data, as of the writing, JELLYJELLY's liquidated amount has reached about $16.94 million in the past 24 hours. They bought or went long because of the trend, but as the latter price dropped from $0.066 to 0.02 USD, many retail investors suffered heavy losses after taking over at a high level. This may further shake retail investors' trust in decentralized platforms.

So, did the trading team that operates market manipulation and Binance and OKX that "fuel" win?

It may not be either, in fact, this may be a game without a winner.

The trading team operates short orders through multiple accounts and pulls the market, trying to force the Hyperliquid vault to penetrate the position. However, Hyperliquid removed the tokens and forced the closing of the position, causing the price of JELLYJELLY to fluctuate violently. The long and spot orders opened by the trading team may lose money as a result. As a violator, it was excluded from the compensation list by Hyperliquid, and it was ultimately afraid that it would be difficult to achieve its expected returns.

As for Binance and OKX, they have more of a reputation damage. They launched JELLYJELLY contracts in the Hyperliquid crisis, pushing up the currency price. They were accused by the community of "putting insults" to attack opponents and compete for traffic. In addition to arousing user disgust, many users also doubt the rigor of Binance and OKX to screen listing projects.

Polymarket is "inaction" when it is attacked by governance. How should we view the dilemma of decentralized governance and the new life? On March 25, before the Hyperliquid incident, an oracle control attack also occurred on Polymarket.A user who held a large number of UMA tokens predicted that the market was about to settle, in order to reverse the loss situation, forcibly tampered with the settlement results by manipulating the oracle voting mechanism. In the end, the big player and the users who should have lost the bet shared all the funds in the prize pool together. Despite the numerous micro-market manipulations in Polymarket, the forecast market has quickly attracted widespread attention as more than $7 million in the prize pool bets.

The predicted market issue involved in this incident is: "Will Ukraine agree to sign a mineral agreement with Trump before April?"

According to the actual situation, as of the time of market settlement,Trump only verbally stated that he would sign it "expect it will soon" and there was no official statement confirming that Ukraine and the United States have officially signed an agreement. However, Polymarket ignored the facts and ruled the result as "YES".

So how do big investors do this? The answer lies in the Polymarket's judgment mechanism and voting mechanism.

Polymarket relies on UMA's decentralized oracle to verify the results, and the voting rights are controlled by UMA token holders. However, since UMA tokens are highly concentrated in the hands of a few "giant whales", the seemingly decentralized UMA is actually easily swayed by capital. On the other hand, Polymarket's voting rules further exacerbate this tendency to centralize: raising objections usually requires a margin of up to $750, but once the voting results are wrong, the objector will lose the margin; and even if the result is correct, they will not receive much reward, which leads to ordinary users being afraid of losses and not daring to raise objections easily. However, big players holding a large number of UMAs can easily pay margins and lead the voting direction.

In this incident, the big player invested about 5.08 million UMA tokens (about 25% of the total votes) through three accounts before the market was about to settle, which eventually led to a reversal of the ruling results.

This incident directly exposed the hidden capital control risks in the Polymarket decentralization mechanism, but it is different from the "power centralization" disputes encountered by the Hyper Foundation. Polymarket highlights more "capital centralization". As many users question, how can ordinary participants trust the fairness of this market when these big players can "turn black and white" with their token holdings?

Encryption KOL "MARMOT" even tweeted and condemned that Polymarket once again deceived users. If Polymarket does not take any action on this, he will never use the site again and advises other users not to use it either.

Interestingly, in the face of the community and users' slander, Polymarket official has not yet been involved in the incident.However, he admitted that the ruling result did not match the user's expectations and reality, but refused to refund the damaged user on the grounds of "non-system failure", and only promised to strengthen system monitoring and improve rules with the UMA team.

This operation can be said to be completely contrary to Hyperliquid's operation. Polymarket chose to maintain superficial "procedural justice" and clearly stated that it would not interfere with this incident. Unsurprisingly, Polymarket’s “inaction” has sparked stronger criticism from the community.

In these two incidents, we once again saw the controversy surrounding the issue of "decentralization". Hyperliquid's end of pulling the network cable was regarded as an "over-centralized behavior". Polymarket's statement and this oracle manipulation incident made it receive "pseudo-decentralized" evaluation. The deep reason is actually the dilemma of decentralized platforms in crisis handling: artificial intervention violates the "decentralization principle", and letting it go will sacrifice user rights.

Although the Crypto industry has been developing for 17 years, to this day, realizing "true decentralization" will still be restricted by many realistic factors. From an objective development trend, as the leader in their respective fields, the emergence of such events is actually a necessary stage for exposing their loopholes in governance, algorithm rules and mechanism design.

As mentioned earlier, Polymarket relies on UMA oracles to make decisions, but UMA token voting rights are highly concentrated in the hands of a few giant whales. Although the system is nominally "decentralized", it is still manipulated by capital, resulting in the results deviating from reality; although Hyperliquid's emergency decision is in the name of "decentralized voting", the validators are all from official foundations and are essentially centralized intervention. These governance flaws and deficiencies may be an opportunity for Hyperliquid and Polymarket to improve algorithm mechanisms and risk management, and also point out the direction for their subsequent mechanism reforms and innovations.

On the other hand, the author believes that industries and communities can be more tolerant of decentralized platforms and allow them to conduct centralized interventions in the short term in exchange for long-term evolution. Just as Hyperliquid decisively removed the tokens and forced the closing of the position when facing the risk of vault trashing, although it violated the "decentralization principle", it protected most user assets, which is consistent with the intervention logic of the Ethereum Foundation in the June 2016 The DAO incident - sacrificing short-term ideals to maintain the life of the systemlive.

At the same time, user trust needs to be gradually established, and decentralized products cannot rely on powerful endorsements like CEX. Therefore, if users choose the former, they need to accept the potential risks of "code is law" and leave time for projects to fix vulnerabilities and upgrade technology.

As for the decentralized products themselves, it is worth mentioning that many projects should focus more on optimizing their products after obtaining stable profit methods. However, some projects have stopped innovating after making money, and then started the "lying flat" mode. Just as Hyperliquid quickly became the leader of the decentralized perpetual contract market after airdropping, it did not devote enough energy to solve its hidden dangers in automated clearing mechanisms, dealing with market manipulation and liquidity management, so the "bright card sniper" of CEXs such as Binance and OKX once again exposed its vulnerability as a decentralized platform. However, it is a blessing to have a loss of power. This may also alert Hyperliquid, thus forcing it to accelerate technological upgrades and improve risk control.

At present, many decentralized products are at the intersection where algorithmic mechanisms and governance models require innovation. The Polymarket incident shows that voting mechanisms that rely purely on token weights are likely to evolve into "capital autocracy", while the case of Hyperliquid proves that completely eliminating human intervention may also amplify systemic risks. Exploring the "resilient decentralization" model will be a very challenging issue. For these products, short-term centralized intervention is just a temporary measure, and it will still return to the essence of "code governance" in the long run.