37 mins ago

5,751

Author: Insights4vc Translation: Shan Oppa, Golden Finance

Since 2020, major U.S. banks, asset management companies and payment institutions have shifted from cautious wait-and-see to actively investing, establishing partnerships or launching crypto products. By early 2025, institutions had held about 15% of the Bitcoin supply, and nearly half of hedge funds had allocated some of their funds to digital assets. Key factors driving this trend include the launch of regulated crypto investment vehicles (such as the first bitcoin and Ethereum spot ETFs in the United States in January 2024), real-life assets (RWA) tokenization on blockchain, and the growing use of stablecoin settlement and liquidity for institutions. Institutions regard blockchain as a tool to streamline traditional financial backend systems, reduce costs and enter new markets.

Many banks and asset management companies are piloting licensed DeFi platforms that combine smart contract efficiency with KYC/AML compliance, while also exploring licenseless public DeFi in a controlled environment. DeFi’s automation and transparency are expected to bring faster settlement speeds, all-weather markets, and new earnings opportunities, thus solving the long-standing inefficiency problems of traditional finance. However, institutions still face severe challenges, mainly including regulatory uncertainty in the United States, difficulty in technology integration, and market volatility, which to some extent limit the speed of adoption.

Overall, as of March 2025, the trend of institutions adopting crypto assets is "cautious but accelerated." Traditional finance is no longer just a bystander, but is carefully tested in selected areas such as digital asset custody, on-chain lending and tokenized bonds to gain tangible benefits. The next few years will be a critical period that determines how traditional finance and DeFi can be deeply integrated in the global financial system.

Paradigm Report - The Future of Traditional Finance (March 2025)As a leading crypto venture capital fund, Paradigm surveyed 300 traditional financial institutions professionals from multiple developed economies and released its latest report. The following are the key data in the report.

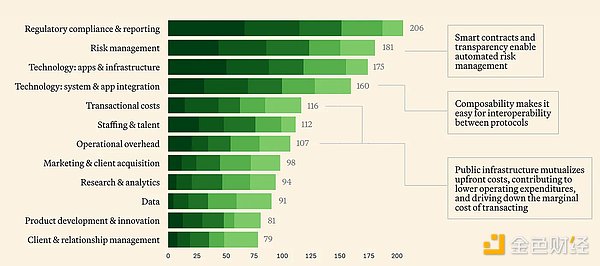

What areas contribute the most to the cost of financial services?

What cost-cutting strategies does your organization adopt when providing financial services?

At present, about 76% of companies are involved in cryptocurrencies

About 66% of TradFi companies are working with DeFi

At present, about 86% of companies participate in blockchain and DLT

institutions entering the crypto market (2020–2024 Year Timeline)2020 - Initial attempt

Banks and financial institutions began to enter the crypto market with caution. In mid-2020, the US Currency Complaints Agency (OCC) made it clear that banks can provide crypto asset custody services, which opened the door for custodians such as BNY Mellon (the bank announced digital asset custody services in 2021). The field of corporate fund management has also begun to be laid out, with MicroStrategy and Square's high-profile purchase of Bitcoin as reserve assets, marking an increase in institutional confidence. PayPal, a payment giant, in 2020 The launch of cryptocurrency buying and selling features for US users at the end of the year has brought digital assets to millions of consumers. These moves mark the beginning of mainstream institutions to regard cryptocurrencies as a legal asset class.

2021—Fast expansion

Institutions are accelerating their adoption of cryptocurrencies driven by bull markets. Tesla spent $1.5 billion to buy Bitcoin, and Coinbase went public on Nasdaq in April 2021, becoming a key bridge connecting Wall Street and the crypto market. Investment banks adapt to customer needs, Morgan Stanley began offering Bitcoin funds to wealthy customers, and JPMorgan restarted its crypto trading division. In October, ProShares launched its first U.S. Bitcoin futures ETF (BITO), providing institutions with regulated investment channels. Fidelity and BlackRock have set up special digital asset departments. Meanwhile, Visa and Mastercard have also begun to use stablecoins for settlement (such as Visa pilot USDC settlement), showing that the combinedConfidence in the secret payment system.

2022 - Infrastructure Construction in Bear Market

Although the crypto market declined in 2022 (Terra collapse, FTX bankruptcy), institutions are still continuing to build infrastructure. BlackRock partnered with Coinbase in August 2022 to provide crypto trading services to institutional clients and launch a private Bitcoin trust, an important signal from the world's largest asset manager. Traditional exchanges and custodians are also expanding digital asset services. For example, BNY Mellon has begun providing crypto asset custody to some customers, and Nasdaq has launched crypto custody platform. JPMorgan Chase uses blockchain for interbank transactions, and its Onyx division processes hundreds of billions of dollars in wholesale payments through JPM Coin. At the same time, the number of tokenization pilot projects has increased, and companies such as JPMorgan Chase simulated DeFi transactions on public chains, including tokenized bonds and Forex trading (Project Guardian). However, U.S. regulators have responded hard to market volatility, leading some companies (such as Nasdaq) to suspend or slow down the launch of crypto products by the end of 2023, awaiting clearer regulations.

2023—Institutions return to the market

At the beginning of 2023, institutional interest rebounded. In mid-2023, BlackRock applied for Bitcoin spot ETF, and then Fidelity, Invesco and other companies submitted applications one after another, which was a major turning point, especially when the SEC had rejected such applications many times. Traditional financially backed crypto infrastructure has also been officially launched, such as the EDX Markets Digital Asset Exchange, powered by Charles Schwab, Fidelity and Citadel, aiming to provide institutions with a compliant trading venue. Meanwhile, a tokenization boom in traditional assets has emerged, such as private equity giant KKR tokenized some funds on the Avalanche chain, and Franklin Templeton moved its tokenized money market fund based on U.S. Treasury bonds to the public blockchain. International regulators have also begun to provide a clearer regulatory framework (the EU passes MiCA, Hong Kong reopens crypto transactions). By the end of 2023, the United States approved Ethereum Futures ETFs, and the market's expectations for spot ETFs to pass are heating up. The momentum of institutional adoption of crypto assets appears to be more solid by the end of 2023, provided regulatory barriers are eliminated.

Early 2024 - Spot ETF approval

In January 2024, the US SEC approved the first batch of Bitcoin spot ETFs (and subsequently approved the Ethereum spot ETF), ending years of delays. This approval has become a watershed in the mainstreaming of crypto assets, allowing pensions, registered investment advisors (RIAs) and conservative portfolios that were unable to hold crypto assets to enter the market. In just a few weeks, crypto ETFs ushered in a large amount of capital inflows, and investor participation increased significantly. During the same period, institutional crypto services continued to expand, including PayPal's launch of PYUSD stablecoin, Deutsche Bank and Standard Chartered's investment in digital asset custody startups. As of March 2025, nearly all major U.S. banks, brokers and asset managers have launched crypto-related products or established strategic partnerships in the field, marking the full entry of institutions into the crypto market since 2020.

DeFi in the eyes of TradFi (2023-2025)Traditional finance (TradFi)'s attitude towards decentralized finance (DeFi) has gradually changed between 2023 and 2025. From initial curiosity and caution to trying to explore the efficiency advantages of DeFi in a controlled environment, many institutions have recognized the importance of public blockchains. Although DeFi remains functioning normally during the turbulence of 2022, showing the advantages of automation and transparency, compliance and risk issues make most institutions more inclined to “licensed DeFi”—that is, to use DeFi technology in closed or semi-closed environments. For example, JPMorgan’s Onyx network launched JPM Coin, providing regulated stablecoin payment services to institutional customers, while Aave Arc introduced a KYC certification mechanism that allows qualified institutions to trade in a decentralized liquidity pool. This strategy of "embracing technology but controlling participation" has become TradFi's main response to DeFi by 2025.

Institutional DeFi PilotAt the time of 2023 to 2025, several large financial institutions conducted DeFi pilot. JPMorgan’s Onyx platform works with Project Guardian led by the Monetary Authority of Singapore (MAS) to conduct tokenized bonds and forex transactions on public blockchains and utilize smart contracts to enable instantaneous settlement. BlackRock launches BUIDL fund by the end of 2023 to tokenize a U.S. Treasury money market fund and through SecuThe ritize platform is available to qualified investors and demonstrates how large institutions can leverage public blockchains within the compliance framework. Goldman Sachs’ digital asset platform (DAP) issued tokenized bonds and promoted digital repurchase transactions, while HSBC (HSBC) used the Finality blockchain platform for foreign exchange settlement. These pilots show that traditional financial institutions are exploring how to apply DeFi technology to core businesses such as payment, lending and transactions through the "learning and doing" method to improve efficiency.

VC-backed infrastructureA group of crypto infrastructure companies supported by venture capital and traditional financial companies are emerging, providing a bridge for institutions to enter DeFi. Custodians such as Fireblocks, Anchorage and Copper have built "institutional-level" digital asset management platforms to help banks securely store and trade crypto assets, while providing compliance tools to enter DeFi protocols. Compliant technology companies such as Chainalysis and TRM Labs provide transaction monitoring and analysis, enabling banks to meet anti-money laundering (AML) requirements, even on public blockchains. In addition, crypto brokers and fintech companies are also reducing the complexity of DeFi, such as crypto custodians providing “earnings agriculture” or liquidity pool access services, without the need to directly manage on-chain operations. With the improvement of wallets, APIs, identity authentication and risk management tools, the threshold for DeFi access for TradFi institutions has gradually lowered. By 2025, decentralized exchanges (DEXs) and lending platforms are gradually integrating institutional portals to ensure that counterparties are verified. TradFi no longer regards DeFi as a “barbaric western that is untouchable”, but as a financial innovation that can be used cautiously under the compliance framework. Large banks are becoming early adopters in controlled environments, recognizing that ignoring DeFi growth may leave them behind in financial development.

The U.S. regulatory environment (and global comparison)The ambiguity of U.S. regulation has hindered the advancement of TradFi in the field of encryption, but it also brought opportunities. In 2023, the Securities and Exchange Commission (SEC) took a tough stance, suing major exchanges for providing unregistered securities and proposed to classify many DeFi platforms as stock exchanges, making institutions struggling in the DeFi field. Meanwhile, the U.S. Commodity Futures Trading Commission (CFTC) regards Bitcoin and Ethereum as commodities and imposes fines on DeFi protocol operators while advocating a clearer regulatory framework. The US Treasury Department focuses on the anti-money laundering risks of DeFi. The 2023 report pointed out that the anonymity of DeFi may be exploited by illegal elements, so DeFi platforms may be required to implement KYC in the future. In 2022, the U.S. Office of Foreign Assets Control (OFAC) sanctions on Tornado Cash, indicating thatThis is a decentralized code service that cannot escape the constraints of supervision. The U.S. banking regulators (OCC, Fed, FDIC) issued guidance to restrict banks from directly contacting crypto assets, forcing institutions to participate in the crypto market more through regulated custodians and ETFs rather than directly using the DeFi protocol.

As of March 2025, the United States has not passed comprehensive crypto regulations, but proposals such as stablecoin regulation and securities-commodity division have entered the stage of in-depth discussion. In the future, the US regulation of stablecoins (such as whether it is defined as a new payment tool) and custody rules (such as the SEC's custody proposal) will determine the depth of TradFi institutions on DeFi. Due to regulatory uncertainty, U.S. TradFi agencies often limit DeFi experiments to controlled "sandbox" environments or overseas subsidiaries, waiting for clearer regulations to be introduced.

Europe - MiCA and forward-looking rulesUnlike the United States, the EU has developed a comprehensive regulatory framework (MiCA - Crypto Asset Market) that by 2024 will provide clear rules for crypto asset issuance, stablecoins and service providers in member countries. MiCA, together with the tokenized securities trading pilot system, provides more innovative certainty for European banks and asset management companies. By early 2025, companies in Europe will know how to obtain licenses to operate cryptocurrency exchanges or wallet services, and guidelines for institutional stablecoins and even DeFi are being formulated. This relatively clear rule prompted TradFi’s European branch to advance pilot projects for tokenized bonds and on-chain funds. For example, several EU commercial banks have issued digital bonds under regulatory sandbox plans and can legally process tokenized deposits under supervision. The UK has taken a similar approach: it has signaled to become a “cryptocurrency hub” by tailoring financial regulations – Since 2025, the FCA is developing rules for cryptocurrency trading and stablecoins, and the Legal Commission has recognized crypto assets and smart contracts in its legal definition. These moves could give way to institutions in London to deploy DeFi-based services faster than their U.S. counterparts.

Asia—Regulatory balance and innovationSingapore and Hong Kong provide a sharp global comparison. The Monetary Authority of Singapore implements a strict licensing system for cryptocurrency companies (implemented since 2019), but it is also actively trying DeFi through public-private cooperation. Singapore’s major bank DBS Bank has launched a regulated cryptocurrency trading platform and even conducts DeFi transactions (such as tokenized bond transactions with JPMorgan Chase). The city’s approach regards licensed DeFi as a field explored under supervision, reflecting a view thatControlled experiments can provide information on reasonable rule formulation. After years of restrictions, Hong Kong turned around in 2023 by creating a new framework that licensed virtual asset exchanges and allowed retail cryptocurrency trading under supervision. With support, this shift has attracted global cryptocurrency companies and encouraged Hong Kong banks to consider providing digital asset services in a regulated environment. Other jurisdictions such as Switzerland (its DLT Act allows tokenized securities) and the UAE (Dubai’s VARA has customized crypto rules) further emphasize that global regulatory attitudes range from cautious adaptation to active promotion of crypto finance.

Impact on DeFi participationFor U.S. agencies, the fragmentation of regulatory regulations means that most direct participation in DeFi is not possible until compliance solutions emerge. We have seen Bank of America insist on using alliance blockchains or trading tokenized assets that meet existing legal definitions. Instead, in jurisdictions with clearer frameworks, institutions are increasingly willing to interact with DeFi-like platforms—for example, European asset managers may provide liquidity to licensed lending pools, or Asian banks may use decentralized trading protocols internally forex swaps because they know the regulators are aware of the situation. The lack of unified global rules also presents challenges: an agency operating globally must coordinate strict rules in one region with opportunities in another. Many have called for international standards or safe harbors for decentralized finance to leverage its advantages (e.g. efficiency, transparency) without undermining financial integrity. In short, regulation remains the biggest factor in determining the pace of TradFi's participation in DeFi. By March 2025, progress is clear—the U.S. approved ETFs, and global regulators issued tailor-made licenses—but there is still much work to be done to establish legal clarity that allows institutions to fully accept licensing DeFi on a large scale.

Key DeFi Protocols and Infrastructure Bridges TradFiMany of the leading DeFi protocols and infrastructure projects are directly meeting the needs of traditional finance, creating an entrance for institutional use:

Aave Arc (Institutional Lending Market): Aave Arc is a licensed version of the popular Aave liquidity agreement launched in 2022-2023 to meet institutional needs. It provides a private pool where only KYC-verified participants on the whitelist can lend and borrow digital assets. Aave Arc resolves TradFi's sanctions by enforcing AML/KYC compliance (via whitelisted proxy like Fireblocks) and allowing only pre-approved collateralA key requirement—counterparty trust and regulatory compliance—while still delivers DeFi’s smart contract-based lending efficiency. This helps banks and fintech lenders use DeFi liquidity to secure loans without exposing themselves to the anonymous wilderness of public pools.

Maple Finance (on-chain capital market): Maple is an on-chain low-collected institutional loan market similar to the syndicated loan market on the blockchain. Through Maple, approved institutional borrowers (such as trading companies or medium-sized businesses) can obtain liquidity from global lenders on agreed terms, assisted by a “pool representative” who conducts due diligence. This solves a gap in TradFi: low-collateralized credit is often relationship-based and opaque, but Maple brings transparency and 24/7 settlements to such loans. Since its launch in 2021, Maple has issued hundreds of millions of dollars in loans, showing how reputable companies can raise funds on-chain more effectively. For TradFi lenders, Maple’s platform provides a way to earn stablecoin gains by lending to reviewed borrowers, effectively reflecting the private debt market, but with lower administrative expenses. It shows how DeFi can simplify loan issuance and services (interest payments, etc.) through smart contracts, thereby reducing management costs.

Centrifuge (Real World Asset Tokenization): Centrifuge is a decentralized platform focusing on introducing real-world assets (RWA) as collateral to DeFi. It allows promoters (such as trade finance, invoice factoring, lenders in the real estate sector) to tokenize assets such as invoices or loan portfolios into alternative ERC-20 tokens, which investors can then finance through the DeFi liquidity pool (Tinlake of Centrifuge). This mechanism essentially links TradFi assets to DeFi liquidity—for example, a small business’s invoice can be pooled and funded by stablecoin lenders around the world. For institutions, Centrifuge provides a template for turning illiquid assets into investable on-chain tools with transparent risk grading. It solves one of the core inefficiencies of TradFi by leveraging a global investor base on blockchain: There are limited opportunities for certain industries to access credit. By 2025, even large agreements like MakerDAO will use Centrifuge to join collateral, and TradFi companies are watching how this technology can reduce capital costs and open up new sources of funding.

Ondo Finance (tokenized income product): Ondo Finance provides tokenized funds that allow cryptocurrency investors to obtain traditional fixed income returns. It is worth noting that Ondo has launched products such as OUSG (Ondo Short-term US Bond Fund), which is completely supported by short-term Treasury ETFs, while USDY is the tokenized share of high-yield money market funds. These tokens are available to qualified buyers under Ordinance D and can be traded 24/7 on-chain. Ondo effectively acts as a bridge, packaging real-world bonds into DeFi-compatible tokens, so that, for example, stablecoin holders can swap for OUSG and get about 5% of their gains from Treasury bills, and then seamlessly exit the stablecoin. This innovation addresses a pressing problem facing TradFi and cryptocurrencies: it brings the security and benefits of traditional assets into the digital asset space and provides traditional fund managers with new distribution channels through DeFi. The success of Ondo's tokenized Treasury bonds (issuance of hundreds of millions of dollars) has prompted competitors and even existing companies to consider launching similar products, blurring the line between money market funds and stablecoins.

EigenLayer (re-staking and decentralized infrastructure): EigenLayer is a new Ethereum-based protocol (launched in 2023) that supports restaking - re-uses staking ETH security to protect new networks or services. Although still in its infancy, its significance to institutions is the scalability of infrastructure. EigenLayer allows new decentralized services such as oracle networks, data availability layers, and even institutional settlement networks to inherit the security of Ethereum without the need for a separate set of validators. For TradFi, this may mean that future decentralized transactions or clearing systems can be run on an existing trust network (Ethereum) rather than starting from scratch. Institutional stakeholders are viewing EigenLayer as a potential solution to scale blockchain use cases with high security and low cost of capital. From a practical point of view, banks can one day deploy smart contract services (such as for interbank loans or forex) and use restakes to ensure billions of dollars of pledged ETH are protected, achieving a level of security and decentralization that is not possible on licensed ledgers. EigenLayer represents the forefront of decentralized infrastructure, and while TradFi is not yet used directly, it could become the basis for next-generation institutional DeFi applications by 2025-2027.

These examples illustrate a broader view: The DeFi ecosystem is actively developing solutions to integrate TradFiNeeds – whether it is compliance (Aave Arc), credit analysis (Maple), actual asset exposure (Centrifuge/Ondo) or strong infrastructure (EigenLayer). This convergence is two-way: TradFi is learning to use DeFi tools, and DeFi projects are adapting to meet the requirements of TradFi, resulting in a more mature, interoperable financial system.

Tokenization and RWA OutlookOne of the most direct intersections of traditional finance and crypto worlds is the tokenization of real-world assets—that is, to put traditional financial instruments (such as securities, bonds and funds) on the chain. As of March 2025, institutional participation in tokenization has gone beyond the proof of concept stage and entered into actual product applications: Several large asset management companies have launched tokenized funds. BlackRock’s aforementioned BUIDL Fund and Franklin Templeton’s OnChain U.S. Money Fund (with public blockchains to record shares) allow eligible investors to trade fund shares in the form of digital tokens. WisdomTree launches a set of blockchain-based funds (providing exposure to Treasury bills, gold, etc.), with the vision of achieving 24/7 trading and simplifying investor access. These initiatives are often constructed under existing regulations (e.g., issuing private securities under exemptions), but they mark a significant shift in traditional assets trading on blockchain infrastructure. Some banks have even explored tokenized deposits (regulated liability tokens) that represent bank deposits but can be moved on-chain, designed to combine bank-grade security with cryptocurrency-like speed. Each of these projects suggests that institutions see tokenization as a way to improve liquidity and reduce settlement time for traditional financial products.

Tokenized bonds and debt

The bond market has seen early victories in tokenization. In 2021-2022, entities such as the European Investment Bank issued digital bonds on Ethereum, and participants settled and custodial bonds through blockchain rather than traditional clearing systems. By 2024, banks such as Goldman Sachs and Santander have promoted bond issuance on their private blockchain platforms or public networks, indicating that even large debt issuances can be completed through DLT. Tokenized bonds promise near-instant settlement (T+0 vs. atypical T+2), programmable interest payments and easier partial ownership. For issuers, this can reduce issuance and management costs; for investors,It expands access and provides real-time transparency. Even the Ministry of Finance has begun to look at using blockchain for bonds – for example, Hong Kong issued tokenized green bonds in 2023. The market is still small (the on-chain outstanding bonds are about hundreds of millions of dollars), but growth is accelerating as the legal and technical frameworks improve.

Private market securities

Private equity and venture capital firms are tokenizing partially tokens of traditionally poor liquid assets such as private equity funds or pre-IPO stocks to provide liquidity to investors. Companies such as KKR and Hamilton Lane work with fintech companies (Securitize, ADDX) to provide tokenized access to some of their funds, allowing qualified investors to purchase tokens representing the economic benefits of these alternative assets. While the scope remains limited, these experiments point to the future secondary markets of private equity or real estate that can operate on the blockchain, potentially reducing investors' liquidity premium requirements for such assets. From an institutional perspective, tokenization here is about expanding distribution and unlocking capital by making traditionally locked assets traded in smaller units.

It is crucial that the tokenization trend is not limited to TradFi-led initiatives—the DeFi native RWA platform is solving the same problem from another perspective. Agreements such as Goldfinch and Clearpool (and the aforementioned Maple and Centrifuge) are enabling on-chain financing of real-world economic activity without waiting for action by big banks. For example, Goldfinch funded real-world loans, such as emerging market fintech lenders, through liquidity provided by cryptocurrency holders, essentially acting as a decentralized global credit fund. Clearpool provides institutions with a market to launch unsecured lending pools under pseudonyms (with credit scores) that allow the market to price and finance their debts. These platforms often work with traditional companies—for example, the financial status of fintech borrowers in the Goldfinch pool may be audited by a third party—create a hybrid model of DeFi transparency and TradFi trust mechanisms.

At present, RWA has broad prospects for tokenization. The strong demand for real-world asset returns in the crypto market due to rising interest rates has further boosted the tokenization of bonds and credit (such as the Ondo success story). Institutions are attracted by the improvement of transaction efficiency: the tokenized market can settle in seconds, operate around the clock, and reduce dependence on intermediaries such as clearing houses.

Industry forecasts that trillions of dollars of real assets may be tokenized in the next decade, provided that regulatory issues are resolved. In 2025, we have seen preliminary network effects—for example, tokenized Treasury bonds can serve as collateral in DeFi loan agreements, meaning an institutional trader can use tokenized bonds to borrow stablecoins for short-term liquidity management, which is impossible in traditional markets. This combination of on-chain assets will completely change the collateral and liquidity management model of financial institutions.

Overall, tokenization is closing the gap between TradFi and DeFi, which may be more direct than any other trend. It enables traditional assets to enter the DeFi ecosystem (providing stable on-chain collateral and cash flow), while also providing a secure experimental environment for TradFi institutions (via licensed blockchains or known legal structures). In the coming years, we may see larger pilots – such as major stock exchanges launching tokenized trading platforms, and central banks explore wholesale CBDCs (central bank digital currencies) compatible with tokenized assets, further consolidating the future role of tokenization in the financial industry.

Challenges and strategic risks of entering DeFiAlthough the opportunities are enormous, traditional financial institutions face a series of challenges and risks when integrating DeFi and crypto assets:

Regulatory uncertainty: The lack of clear and consistent regulations is the greatest risk. If banks use DeFi protocols that are later identified as illegal stock exchanges or involve transactions with unregistered assets, they may face enforcement risks. Different regulatory differences further increase the complexity of using encrypted networks across borders.

Compliance and KYC/AML: DeFi platforms on public chains usually allow anonymous transactions, which conflicts with the bank's KYC/AML (anti-money laundering) obligations. How to implement compliance on blockchain (such as whitelisting mechanisms, on-chain authentication, compliance oracles) is still being explored, and compliance risks make TradFi more inclined toward licensed or regulated DeFi solutions.

Hosting and Security: Private key management is a significant risk (loss or stolen may cause assets to be unrecoverable). Vulnerabilities or hacking of DeFi smart contracts have also raised concerns to institutions, with many companies relying on third-party hosting or self-built cold storage solutions, but these solutions still lack well-established insurance.

Market volatility and liquidity risk: It is well known that the cryptocurrency market is volatile. Institutions that provide liquidity for DeFi pools or hold cryptocurrencies on their balance sheets must bear large price volatility that could affect earnings or regulatory capital. In addition, DeFi market liquidity can quickly evaporate during a crisis; if a user of a protocol defaults (such as a failed loan with under-collateralization), it may be difficult for institutions to close large positions without slippage, or even face counterparty risk. This unpredictability contrasts sharply with more controlled volatility and central bank support in traditional markets.

Integration and technical complexity: Integrating blockchain systems with traditional IT infrastructure is both complex and expensive. Banks must upgrade their systems to interact with smart contracts and manage 24/7 real-time data, which is a difficult task. In addition, there are gaps in talent – evaluating DeFi code and risk requires expertise, which means institutions need to hire or train experts in a competitive talent market. These factors make initial entry costly.

Reputation Risk: Financial institutions must consider the perception of the public and the client. Participating in cryptocurrencies can be a double-edged sword: although innovative, it can cause concerns among conservative clients or board members, especially after exchanges are out of business or institutions are involved in events such as DeFi hacking or scandals. Many institutions are cautious and participate in behind-the-scenes pilots until they are confident in risk management. Reputation Risk also extends to unpredictable regulatory narratives – Negative comments from officials about DeFi may cast a shadow on the institutions involved.

Legal and Accounting Challenges: There are unresolved legal issues regarding ownership and enforceability of digital assets. If a bank holds tokens representing loans, does it legally recognize that it owns a loan? The lack of established legal precedents for protocols based on smart contracts add to uncertainty. In addition, the accounting treatment of digital assets (although improved, new standards allow fair value accounting by 2025) legacy issues (such as impairment rules) and regulatory authorities’ capital requirements (Basel’s proposal regards unsecured cryptocurrencies as high risk). From a capital standpoint, these factors may make holding or using cryptocurrencies economically unattractive.

In the face of these challenges, many institutions have adopted a strategic risk management approach: starting with small-scale pilot investments, using subsidiaries or partners to test the waters, and proactively working with regulators to achieve favorable results. They also contribute to industry alliances to develop compliant DeFi standards (e.g., creating identity embedding agents for institutionscoin or “DeFi passport” proposal). Overcoming these barriers is critical to wider adoption; the timeline will depend to a large extent on the transparency of regulation and the continued maturity of crypto infrastructure to meet institutional standards.

2025-2027 Outlook: Scenarios of the integration of TradFi and DeFiLooking forward, the degree of integration between traditional finance and decentralized finance may show multiple trajectories in the next 2-3 years. We outline the bullish, bearish and basic situations:

Bull scenario (rapid integration): In this optimistic scenario, regulatory clarity will increase significantly by 2026. The United States may pass a federal law that delineates crypto asset classes and establishes a regulatory framework for stablecoins and even DeFi protocols (and perhaps a new charter or license for compliant DeFi platforms). With clear rules, major banks and asset management companies will accelerate their crypto strategies – providing crypto transactions and earnings products directly to customers and using the DeFi protocol to implement certain backend features (such as overnight financing markets using stablecoins). Stablecoin regulation is particularly likely to be a catalyst: If dollar-backed stablecoins are officially approved and insured, banks can begin using them on a large scale for cross-border settlement and liquidity, embedding stablecoins into traditional payment networks. Improved technology infrastructure also plays a role in the bull market scenario: Ethereum’s planned upgrades and tier 2 expansion make transactions faster and cheaper, with a powerful custody/insurance solution the standard. This enables organizations to deploy to DeFi with lower operational risks. By 2027, we can see a large portion of interbank lending, trade financing and securities settlement will occur on hybrid decentralized platforms. Even ETH pledge consolidation becomes common in bull market situations—for example, the financial department of a company uses pledged ETH as a revenue asset (almost like digital bonds), adding a new asset class to the institutional portfolio. The bull market heralds convergence: Traditional financial companies not only invest in crypto assets, but also actively participate in DeFi governance and infrastructure, contributing to shaping a regulated, interoperable DeFi ecosystem to complement traditional markets.

Pessimistic scenarios (stagnation or contraction): In pessimistic scenarios, regulatory crackdowns and adverse events seriously hinder integration. Perhaps the SEC and other regulators will double down on the law, without providing new avenues – effectively banning banks from access to open DeFi and limiting cryptocurrency exposure to a handful of approved assets. In this case, by 2025/2026, institutions will remain mostly on the wait-and-see state: they stick to ETFs and a few licensing networks, but due to legal concerns,They avoid public DeFi. Additionally, one or two eye-catching failures can ruin emotions – for example, a major stablecoin crash or a systematic DeFi protocol hacking resulted in losses in institutional participants, reinforced the claim that the space is too risky. In a pessimistic scenario, global splits intensify: markets such as the EU and Asia continue to integrate cryptocurrencies, but the United States lags behind, causing U.S. companies to lose competitiveness or lobby against cryptocurrencies to level the playing field. If TradFi considers DeFi as a threat and lacks viable regulation, they may even actively fight back DeFi, which could lead to slowing innovation (e.g., banks promote only private DLT solutions and prevent customers from doing on-chain finance). Essentially, the pessimistic situation is that the prospects for TradFi-DeFi synergies are stagnant, while cryptocurrencies remain niche or secondary sectors for institutions by 2027.

Basic Situation (gradual, stable integration): The most likely situation is between these two extremes—continuous gradual integration, gradual but firm progress. Under this basic prospect, regulators will continue to issue guidance and some narrow rules (for example, stablecoin legislation may be passed in 2025, the SEC may improve its position, perhaps exempting certain institutions from DeFi activities or approving more crypto products on a case-by-case basis). There is no overhaul reform, but it brings some clarity every year. Traditional financial institutions, in turn, are cautiously expanding their crypto business: more banks will provide custody and execution services, more asset management companies will launch crypto or blockchain-themed funds, and more pilot projects will go online to connect bank infrastructure to public chains (especially in areas such as trade finance documents, supply chain payments and secondary market transactions of tokenized assets). We may see alliance-led networks selectively interconnecting with public networks—for example, a group of banks can run a licensed loan agreement that connects to the public DeFi protocol when needed for additional liquidity, all under agreed rules. In this case, stablecoins may be widely used by fintech companies and some banks as settlement media, but may not have replaced the main payment networks. ETH staking and cryptocurrency earnings products are beginning to appear in institutional portfolios on a small scale (for example, pension funds invest several basis points of their allocation into earning digital asset funds). By 2027, in the basic case, the integration of TradFi x DeFi will be significantly deeper than today – measured by 5-10% of transaction volume or loans occurring on-chain in some markets – but it is still parallel to traditional systems rather than a complete replacement. Importantly, the trend is upward: the success of early adopters convinced more conservative peers to try the waters, especially with increasing competitive pressures and customer interest.

Key DriversIn all scenarios, there are several key factors that will affect the outcome. Regulatory development is crucial – any initiative that provides legal clarity (or, contrary, new restrictions) will immediately change institutional behavior. The development of stablecoins is particularly critical: secure, regulated stablecoins may become the backbone of institutional decentralized financial transactions. Technology maturity is also a driving factor—continuous improvements in blockchain scalability (through Ethereum Layer 2 networks, alternative high-performance chains or interoperability protocols) and tools (better compliance integration, private transaction options, etc.) will make institutions more at ease. In addition, macroeconomic factors may also play a role: if traditional returns remain high, the urgency to seek decentralized financial returns may be low (reduced interest), but if returns fall, the additional points of decentralized finance may become attractive again. Finally, market education and historical records will also play a role—every year the decentralized financial protocols show resilience, and every successful pilot (for example, a large bank successfully settles $100 million through blockchain) will build trust. By 2027, we expect the discussion to shift from “whether” to “how” to use decentralized finance, just as cloud computing has gradually been adopted after banking initially doubts. In general, traditional finance and decentralized finance may see from cautious exposure to deeper cooperation in the coming years, and the speed of development will be determined by the interaction between innovation and regulation.