3 mins ago

2,213

The recent global market seems conservative to describe it as "storm". Various "once-in-decade" major changes have been staged one after another, from Trump's position on the Ukraine issue to Musk's big tide in Washington, and Germany's determination to "do everything".

How to understand all this? Today we will deeply analyze the core logic behind this major change and try to give a prediction: What else will happen next?

From the "Biden Loop" to the "Trump Reset"Let's start with a recent exciting research report from CICC. In this report titled "Trump's "big reset": Debt resolution, deviating virtual and real, and devaluing the dollar", CICC's macro research team first explained the most important logic of global capital flows in the past few years - the "Biden big cycle": After the epidemic in 2020, Biden launched a huge amount of fiscal stimulus and a technology frenzy promoted by AI and industry. The United States achieved high growth, high interest rates, and stock market prosperity, attracting overseas funds to continue to flow into the United States, supporting the appreciation of the dollar trend. From the perspective of approach and effect, Biden actually reproduced the "Reagan cycle" and raised the valuations of US stocks and the US dollar to historical highs.

But the "Biden Loop" has two fatal flaws:

One is the huge risk in the financial market: high debt. This has been interpreted in the "Reagan Circle". The huge amount of fiscal stimulus drives high economic growth and the appreciation of the US dollar, which often leads to the deterioration of the trade deficit. In addition, the fiscal deficit is difficult to converge in the short term. The problem of double deficits will eventually arouse investors' attention and even worry. When the US double deficit exceeds a certain threshold for a certain period of time, under certain catalysts, the US dollar often triggers to start a long-term depreciation.

To a certain extent, this is what is happening in the US market at the moment. But at least before last year's election, Biden successfully suppressed the risks of the US financial market. The US economic situation looks very good, with high economic growth and rapid stock markets.

But Biden and the Democrats lost.

The problem is another fatal flaw of the "Biden Loop": the gap between the rich and the poor.

U.S. New Treasury Secretary Becent made a sharp analysis this week.

He bluntly criticized Biden for his uncontrollable fiscal spending actually hurt the interests of the bottom 50% of the people. In the years when US stocks soared, the wealth of the top 10% of rich people rose as their assets appreciated, while ordinary people without assets faced the dilemma of soaring prices and high debts.

What's more serious is that inflation hits different classes of people in different classes, and the daily consumption of the lower class (such as used cars, car insurance, rent, food, etc.) has increased much higher than other goods and services. Becente believes that this inequality has exacerbated social instability and is undoubtedly a heavy blow to the "American Dream".

In other words, the "Biden circulation" allows a small number of American producers to earn more, and financial capital is popular. Industrial capital is constantly declining, and for most Americans, the "American Dream" is gone. As the famous saying says, living in dire straits.

Biden lost without any worries, but Trump, who won, "taken over the Biden big cycle at a high level."

Trump has seen the lessons of Biden clearly, so "Trump 2.0" must clean up the mess left by the "Biden Loop".

Trump's idea is "a big reset".

What are the tricks for Trump’s “big reset”?On the surface, "Trump 2.0" has made three moves, and Becent explained it very clearly.

The first move is to reduce debt by cutting expenses, and it plans to lower debt and deficit levels to the long-term average by 2028, which means that the deficit accounts for about 3.5% of GDP.

The second trick is to relax financial supervision and encourage the private sector to re-leverage, that is, deleverage, and the private sector to increase leverage, so that those civil servants who have been laid off will be absorbed by more productive departments.

The third move is to readjust the international trade system and pass tariffsBig stick brings manufacturing jobs back to the United States to revive the middle class.

CICC calls this the American version of "de-virtual to real", which aims to reset the capital structure and adjust the relationship between industrial capital and financial capital, that is, focusing on industries vs. neglecting finance.

But it is extremely difficult to achieve the goal. Because the "Trump reset" also has its own flaws.

If the United States wants to reduce high debt, it must control new debts and resolve existing debts.

To control new debt, the United States must increase revenue and reduce expenditure.

In terms of open source, Trump does everything he wants. The whole world is waving the tariff stick and even selling American gold cards.

I have to mention it here, which is also what shocked Wall Street and the American business community: tariffs are not means, they are really the purpose!

What is even more difficult is to reduce federal spending.

Trump's most direct trick is Musk's DOGE. Musk, like the "Nezha" released by Trump, has been in a state of great and rough layoffs in Washington.

However, the problem is that reducing fiscal spending will lead to an economic recession. How to deal with the anger of the people? Trump must take the blame to Biden just now.

So there is a recent famous saying from Becente: The United States has "debt addiction" and the economy will have a withdrawal period.

Drug rehabilitation is of course very painful, investors? Sorry, Trump doesn't care.

But those who understand clearly know that DOGE alone is far from enough.

U.S. social security benefits for Americans are iron law of "whoever moves, whoever dies", Trump can move two things: the huge US military expenditure and even greater debt interest expenses. Therefore, we see that Trump is eager to end the Russian-Ukrainian conflict while putting pressure on NATO to increase military spending. This move greatly changed the global geographic landscape and brought about a Wall StreetUnexpectedly, the huge change: Germany shouted "no matter what", ended decades of "financial prudence" and started the "financial rocket launcher".

You must know that since 2022, the interest expenses in the United States have exceeded military expenditures.

"Ferguson's Law" tells us: When any major country's interest expenditure exceeds military expenditure, it is no longer a major country.

Trump must dismantle debt.

As China Securities Investment said, there are generally three ways to convert debt: debt restructuring; inflation; technological progress.

The US debt restructuring, a concept that the market had never dared to imagine before, seems less fantastic now.

The "Malago Manor Agreement" that has been hotly discussed in the financial market recently is debt redeem. One proposal is to convert some of the U.S. Treasuries into 100-year, nontradeable zero-interest bonds. If these are in desperate need of cash, the Fed can temporarily provide liquidity to them through special lending tools.

In addition to forcing others to submit, Trump must also try his best to lower the debt interest rate, which requires the cooperation of an important institution: the Federal Reserve.

The Federal Reserve is in an extremely awkward position at this time.

On the one hand, the "Trump's detox period" is causing the US economy to slow down or even recession, and the Federal Reserve needs to cut interest rates.

On the other hand, the "Biden circulation" has already put inflation at a high level and shows strong stickiness. The Federal Reserve has failed to suppress inflation after many interest rate hikes, but instead has a trend of making a comeback at any time. Trump's tariffs may be the next fire for the second round of inflation, and the interest rate cut at this time is "adding fuel to the fire."

Powell was "in a dilemma" and could only maintain the status quo. At the press conference after the March resolution, he used a meaningful word: "inertia". The implication is that even the Federal Reserve is not sure what will happen in the future.

It is difficult to cut interest rates, and the Fed needs to think of other ways. There is a potential big move to reserve: QE.

Finally, let’s talk about the third method of debt conversion: the productivity improvement brought about by technological progress. CICC believes that the "AI narrative" in the United States in the past two years has not only supported the valuation of US technology stocks, but more importantly, it has supported investors' "fiscal belief" in the United States: it tends to believe that the United States has a high probability of driving real technological progress through AI and thus improving total factor productivity to reduce debt.that is, the "American exceptionalism" formed by the financial market in the past few years, supporting the high valuation of US stocks.

But DeepSeek's "coming out of nowhere" at the beginning of the year severely damaged the American AI narrative and shook the "American exceptional theory."

The market began to question: Can the massive investment of the United States and AI technology giants at all costs bring the expected returns in the past two years? Can this round of AI technology revolution really improve the total factor productivity of the United States? Even, is it more likely to achieve an improvement in total factor productivity?

In other words, the market may gradually price U.S. debt risks in U.S. dollar assets.

So it is not an exaggeration to say that DeepSeek is a "national fortune-level innovation".

The above is the change in the US thinking since Trump took office, which is the logic of "Trump's major reset".

Next, we will talk about what this means for the financial market and the global capital flow pattern? What happens next?

The great changes in global capitalThe keen capital market has realized that "thing is wrong".

After Trump's victory in November last year, the US stock market and the US dollar have made rapid progress, and the market is full of joy. The logic is that the market believes that Trump will definitely promote growth.

Since Trump took office, everything has completely reversed, and both the US stocks and the US dollar have fallen for two months. According to Goldman Sachs statistics, this situation has only happened 5 times in the past 33 years!

Because the market realizes that Trump no longer uses US stocks as a KPI, the KPI of "Trump 2.0" is a US debt. For this reason, Trump has spared no hesitation to let the United States decline and let the US economy "detoxify".

Over the Atlantic Ocean, the rich but famously stingy Germany suddenly started to borrow money and spend a lot of money! This brought an unexpected variable to Trump, which not only gave Germany and European stock markets a shot in a puff of heart, but also significantly pushed up the yield on European government bonds, including German government bonds.

The result of this unexpected change is that the interest rate spread between the United States and Europe narrowed sharply, affecting the flow of trillion-level "European old money", which in turn will affect the demand for US bonds and thus push up US bond yields, which may have been unexpected by Trump.

The real impact of the "Trump reset" lies in the reshaping of the US dollar system.

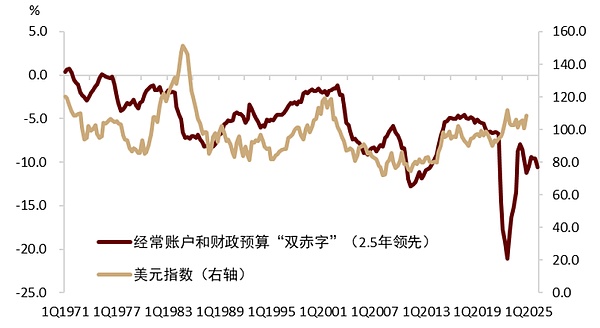

CICC Research Report believes that: Since the United States and Europe launched global integration and financial liberalization in the 1980s, the US dollar circulation has been based on the following key paths: the United States maintains the current account deficit, trading partners purchase US dollar assets through trade surplus, and the United States maintains the financial account surplus. Since the epidemic, the US dollar trend has strengthened due to the deterioration of the US double deficit. One of the important reasons is that overseas funds tend to purchase large amounts of US dollar assets. According to the balance of payments identity, the improvement of the U.S. trade deficit means a decrease in financial capital account surplus, among which securities investment projects (portfolioinvestment) will be the first to be affected.

To put it bluntly, the less trade deficit in the United States, the demand for US dollar assets will also decrease accordingly. The "sky-high valuation" formed by US stocks in the past will face severe challenges, which will bring opportunities to other assets, and "rise from east to west" is not groundless.

Trump's tariff increase will hit hard by core US stock assets such as Mag 7 and US bonds.

The US dollar no longer has a safe-haven attribute as before. When US stocks fall, the US dollar will fall with it.

U.S. debt is also the one that loses the hedging and safe-haven attributes with the US dollar. If the U.S. economy is reallyThere is a recession, even if the Fed is forced to cut interest rates, the market may see a repeat of last September, that is, the Fed cut interest rates and US Treasury yields will rise instead.

What will happen next?CICC has warned about the risk of "three kills" in short-term U.S. stocks, bonds and foreign exchanges: From a technical perspective, since the Federal Reserve's balance sheet shrink in 2022, U.S. hedge funds (especially multi-strategy platform funds) have become the largest marginal buyer of U.S. bonds. Hedge funds continue to buy US bonds on a large scale not because they are bullish on US bonds, but because they are doing US bond arbitrage trading: they are long on US bonds with their left hand and short on US bond futures with their right hand. When the market fluctuates greatly, futures holdings can earn maturity margins at a lower risk. These hedge funds often leverage to buy US Treasury cash bonds in the repurchase market to increase returns. The transaction size may have nearly doubled the historical high in the second half of 2019, and the fuse of the global financial market fluctuations in March 2020 (selling all assets for cash) was the unexpected closing of the historically high basis arbitrage transaction at that time. This transaction is essentially short volatility, so once the volatility rises sharply, it is easy to cause closing risks and asset sales.

What factors may trigger a sharp rise in volatility in financial markets? We believe that the resolution of the debt ceiling is a key event. Once the debt ceiling is resolved, the Treasury Department will issue new U.S. bonds that were previously unable to issue due to debt restrictions will be issued after reissue. In the absence of debt restructuring, the risk of "three kills" of US stocks, bonds and foreign exchanges will increase.

What other moves will Trump do?

First, the Mar-a-Lago agreement or its variant may become a reality soon. Some, such as Japan, are likely to agree to replace and reorganize the US debt it holds under the threat of tariffs. Others You may also agree to purchase US bonds in exchange for exemption of tariffs.

When interest rate cuts are invalid or even have a counterproductive effect, the Federal Reserve may restart measures such as QE or YCC, and the United States will also relax bank regulatory measures and encourage more banks to hold US bonds.

Even, we may see the United States' statistical methods and caliber of redefining inflation and even GDP.

Speaking ofI believe everyone understands here that Trump is playing a difficult tightrope walking game, testing the fate of the United States. If Trump succeeds, it will begin as he himself claims a new golden age in the United States.

Even so, the huge uncertainty in the process will make the financial market earth-shaking.

If Trump "plays out", what will we see?

The good situation is: the valuation of US dollar assets is declining, and the attractiveness of physical assets and cash flow assets is increasing.

The bad situation is: internal reform cannot solve the problem, and the United States can only transfer the contradictions to the outside world.

What does this mean? It has been staged too many times in history, and you will understand it.