17 mins ago

2,347

DeepSeek After R1 leaves, Sam Altman will give you the GPT-4.5 and CoT process, which will improve your Deep Research, not because they find their conscience, nor because they become good people, but because the little whale has been here.

Under the support of AI, cracks have emerged from the pillars of platform capitalism, small teams and individual developers have the opportunity to attack major manufacturers. Under the repeated impact of Hyperliquid and PumpFun, Binance began to take listings seriously, build the BSC Meme ecosystem, and respect the basic human rights of retail investors in Binance Wallet.

But the situation is not exactly the same. The Bonding Curve that Pump Fun relies on is not a new paradigm. In 2020, the Order Book, AMM (Automated Market Maker) and Bonding Curve (United Curve) competed with each other. In the end, AMM became the first choice for DEX. Order Box hides in CEX and Perp DEX and becomes a united man, lying dormant in the sea of people and truces.

So far, all the history of blockchain is the history of trading platforms.

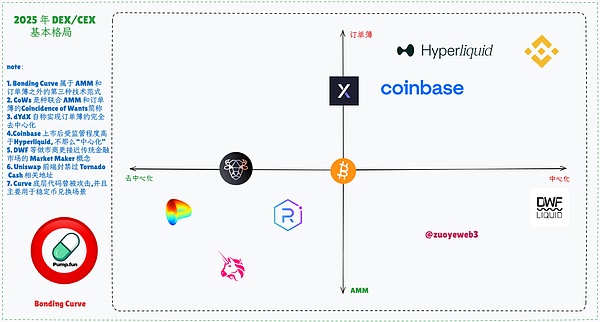

Unlike stereotypes, in the spot trading scenario, CoWs combines AMM and order thin mechanisms to introduce Solver operations to improve matching efficiency. The demand coincidence is more intentional, while the efficiency of contract trading products, dYdX and Hyperliquid are more like the convergent evolution of CEX.

In 2025, it is meaningless to measure decentralization, transaction efficiency is the core, and the above formula should be rewritten asThe following format:

It needs to be explained that there is a mixture of asset issuance models and asset issuance platforms. The two are like the wave-particle duality of light, two-way entanglement, which is difficult to distinguish and resolve.

For example, NFT, FT and Memecoin are all asset issuance models, but different assets will also inspire different new platforms. For example, OpenSea and Blur are already the tears of the times. This article mainly explores what the next asset platform will be.

Whether it is BSC taking over the Meme new wave or Base launching the stock chain drama, it is essentially a change in the asset issuance model. Instead of FOMO specific tokens, it is better to focus on model changes.

After all, what we really want to know is not how Binance is, but how Binance is formed and how to replace Binance.

The arrival time determines the industry's positionI miss the summer of 2020 so much, even surpassing the 2018 when there was a blowing wind.

Using the current as the end point to reverse the development history of the entire trading platform, Binance in 2017 was indeed the son of the times. This matter has been recorded in cryptocurrencies from pioneers to old money - Zhao Changpeng, so I will not repeat it here.

*Note: The horizontal axis of the above figure is the number of established distances between each trading platform, and the bubble size is the current trading volume, where FTX is the previous average trading volume (remembering SBF for one second).

From the picture, we can see that CEX started the earliest and most crowded track. Starting with Mt.Gox in 2010, Binance started to trade BTC, and until FTX ended in 2022, Binance became the king, and experienced it.12 years of cruel competition, and today's compliance and investment are just a boring interwar period.

However, the establishment of Binance did not completely terminate the competition for trading platforms. In the 2020 DEX war, on-chain trading is finally no longer just a gimmick, but a profitable real business of LP. However, $UNI is a semi-destructive product of the hasty response to SushiSwap's move and has not unified the chain like Binance.

The FTX in 2022 is a real crisis moment for Binance. The SEC's high leverage supervision and money laundering allegations have allowed the well-established SBF to kill all over the world, but the story later has become well known, leaving only a sigh.

The on-chain DEX did not drop Binance on 2020/2022/2025 Flip, and the spot trading volume of DEX accounts for at most 15% of CEX, as if it has become an invisible disaster.

Curve's large-value stablecoin exchange, Ethereum represented by Uniswap/Jupiter, Solana DEX, and Memecoin represented by Pump Fun are the entire story of spot DEX on the chain. It is still 4 years ago, and it is unknown whether the AMM+Bonding Curve+ order book has any problems.

In comparison, the biggest problem with DEX is that there is no absolute market giant, which is inconsistent with the situation where Binance is dominant. Driven by market efficiency, the normal situation will lead to an organization defeating an unorganized situation. The reason is, I guess the transaction itself may require strong intermediaries to match. The stronger the intermediaries, the more serious the centralization, but the higher the transaction cost and success rate.

This is more obvious in Perp DEX, with Hyperliquid reaching 10% of Binance's daily trading volume, but the daily trading volume of Uniswap deployed by multi-chain is only US$1.5 billion, and the recent high is 5.7 billion of Uniswap V3 on January 19, which finally caught up with the rumored annual handling fee profit of coin security.

The biggest problem with spot DEX and Perp DEX is that the transaction volume cannot be increased, but the crime is not Uniswap. The split between public chains and L2 is the culprit. The method given by Crypto is chain abstraction, which is equivalent to re-taking the aggregation path of centralized exchanges. However, in the name of decentralization, it first splits, then bridges, and repeats this.

Of course, BitMEX and Aevo are more of innovative significance. The former develops the product type of perpetual contracts, and the latter launches the Pre-launch (pre-market trading) model, but unfortunately, they are all copied by other CEXs, and they are actually killed by old predecessors.

OpenSea and Blur are typical examples of entering the wrong line. The NFT market has been falsified in stages. Whether to issue coins, list or not, or do Rollup, has lost its significance.

There can be a preliminary conclusion that there will be no new players in CEX, especially spot CEX. If you don’t believe it, you can check the experience of Backpack, the FTX spiritual sequel, the Solana Orthodox bonus, and the wallet/CEX simultaneous promotion are useless.

Today, the only trend in 2025 is the on-chain battle for exchanges, opening up the proxy war for wallets, DEXs and Memes, but we need to understand why these elements are and why they are home to the exchange.

DeFi Literature and Art RevivalIn the face of the universe, we are always children, and in the face of Binance, we are always leeks.

The currency circle is one day, one year in the world. The time of establishment of the trading platform and the current trading volume are not enough to show the speed and cruelty of the paradigm transfer. According to the explosive events of each trading platform, we can clearly outline its development path: go on the chain - off the chain - and then go on the chain.

The initial on-chain ecosystem revolves completely around Bitcoin. P2P does not mean micro-loans, but point-to-point transactions, but the transaction efficiency is obviously not high. The Ethereum 1.0 that was born is to make everything happen on the chain, including but not limited to transactions and DeFi.

Uplink: Outside Binance, Coinlist can participate in token public offerings;

Under the chain: Outside China and the United States, Upbit relies on a country's market to win 9.44% market share;

Re-on-chain: In addition to spot and contracts, Polymarket proves the feasibility of on-chain forecasting markets.

From the sky-high Filecoin fundraising of $150 million on Coinlist in 2017, to the 2024 election forecast, the launch of $TRUMP and the BTC strategic reserve motion, Crypto has officially moved to its own opposite and has become part of the existing system, just like the history of the development of the trading platform.

From the plot point, the existing trading platforms can be roughly divided into four styles of products:

It can be found that Binance, OKX and other Chinese backgrounds are difficult to be classified into a certain category, because they are mixing innovation, copying and modifying, regardless of the chain, they hope to build a circular ecosystem of All in One, such as WeChat, so transactions must be spot and contracts, and the ecosystem must have wallets and L1/L2, and at the same time, they must be mixed with stablecoins, DeFi, financial management and compliance licenses, and VC And market makers also need to make arrangements and control.

In addition to the established "greedy" product thinking, more importantly, the larger the manufacturer, the more it cannot give up the tiny threat. BitMEX pulled out the network cable to save the market on March 12, 2020, in exchange for its own gradual demise; the more it is, the more it needs to look at the traffic effect of the explosive event. Robinhood, as a brokerThe platform was involved in the dispute between GME and Dogecoin, and the result was that black and red were also red.

How did BitMEX not happen and how Robinhood came about, these two problems persist, and are more worthy of deep thought than FTX's sudden life and death.

In other words, the Binance I face today is not Binance in 2017, but the New Binance, which focuses on "diring traffic" to BNB Chain and wallet ecosystem after supervision, just like OKX Wallet has taken down DEX aggregators and must be truly compliant.

There is a further conclusion that as long as you follow specific operations and strategies to act, when the critical point is reached, the moment of tipping points will come and nonlinear growth will come true.

Let’s answer now why the exchange is the main player: the on-chain battle is an inevitable move by the exchange after it ate over its existing market share. Hyperliquid’s active attack has resulted in the prosperity of BNB Chain Meme.

But wallets are not new products. L2 is also criticized for Ethereum frequently. Only the exchange can continue to do it. This war of agents still requires the attention of the audience, that is, retail investors.

DeFi is once again in the spotlight, and the Meme frenzy is nothing more than a preview of a larger money offensive in the future.

Life is based on negative entropy, and trading is based on retail investors.Funning the pointer of time, roaming the shadow of fate, and the incarnation of pranks and fraud!

Previously, the wallet was considered the second traffic portal beyond the exchange;

Now, the public chain is considered to be a more important on-chain portal than the exchange;

From now, the wallet built-in trading function products and the main websites will not be distinguished from each other.

For a long time, the chain has been regarded as an ungazing existence like Cthulhu, but the cash machine that a few scientists can roam at will, but the off-chain ecology has been rolled to the extreme, and the migration to the on-chain band has become the mainstream paradigm. The Dogcoin started the Dogcoin in 2021, the Dogcoin started the small picture craze, the 2022 NFT started the inscription gold craze, and the Meme swept in 2024 reached its peak.

Especially inscriptions and NFTs, compared with OpenSea and Blur, the exchange's NFT built-in market is almost unchanged. This is Binance's first failed track. Trust Wallet and Binance Wallet are actually the second time, but unfortunately NFTs have not become the mainstream trend in the industry, and the exchange escapes.

An inscription/runes, together with BTC L2/BTCFi, became a path for BTC development. After the virtual fire, there was only a mess left, leaving only the projects that could not issue coins.

Now, survivable exchanges are still the main force, but compared to the competition between exchanges, the on-chain layout is more gentle. At the same time, they are all choosing the basic configuration of wallet + L2. OKX even continues to launch X Layer under the premise that EVM L1 is already available. Backpack is more special, and its relationship with Solana is just like the relationship between FTX and Solana, which is unclear but closely connected.

Even Kraken, which has always been slow, forces himself to deploy his wallet + Ink L2, but he basically has no market voice, which is far less than the thriving Base that AI, Meme, stablecoins, and RWA are all made.

The same is true for OKX's X Layer. It seems that OKX is born to be in conflict with the public chain. He finally made a wallet. After years of Gas Fee, he worked hard to get an EU license, and was overtaken by Binance Wallet within one day.

The reason why it is in the form of Meme is more of a forced pull from BNB Chain, which snatches liquidity from Solana in the post-$TRUMP era, but the era of Meme has passed, and BNB Chain only Meme will inevitably not last long.

Not only are exchanges being centralized, public chains/L2 itself will also be highly concentrated, leaving only Ethereum, Solana, BNB Chain, Arbitrum and Base. Please forget Sonic. Just like forgetting Monad/MegaETH, only public chains/L2 that are collaborative with exchanges can survive. Ethereum is an extreme alien.

After a short period of TGE and liquidity subsidies, you will fall into long-term silence and boredom.

So the currency-free blockchain can be Base, but the exchange without users will definitely be FTX. The importance of retail investors is not in the glorious moments, but in the lifeline of the product's existence.

Therefore, in the on-chain era, retail investors are more important. Referring to the user stickiness of the Internet, most retail investors will not frequently change the exchanges they use. Now the competition for user stickiness on the chain will be reflected in the retention of the wallet. This is the fundamental reason why the wallet needs to have built-in SWAP, or the introduction and recommendation of more dApps.

You can now answer why it is an agent war, because the competition between exchanges has ended, and it is difficult for the on-chain ecosystem to be completelyOKX Wallet will not reject BSC’s Meme, and Coinbase also hopes to use Base to step out of the US market and compete with Binance globally.

ConclusionIn the Renaissance, the Medici family was behind the scenes, but they would eventually disappear into the clouds of history.

We will deduct the question. After the OKX DEX aggregator is killed, will Binance once again perform the glory of the exchange era? To be precise, will asset issuance platforms inevitably become extremely minority?

GMGN can reach a maximum handling fee of US$2.3 million, which is a new platform created by new assets;

Hyperliquid replicates the miracle of the unity of Binance currency, mainnet tokens and LP income, which is Pinduoduo's overtake after imitating Taobao;

In addition, Binance missed the entire NFT era, which has proved that Binance is definitely not invincible, and Ben Zhou can also distinguish CZ's kindness, which means that practitioners will also learn, review and grow.