53 mins ago

9,886

A speculation about the future of risk, time and currency

I hope today's question does not surprise you. Because reality slapped the question "face":

Gold, today (March 16), broke through $3,000 per ounce in a short period of time, setting a record high.

Bitcoin, after falling from a high of 102,000, it fell below 77,000, and now it is hovering around 84,000.

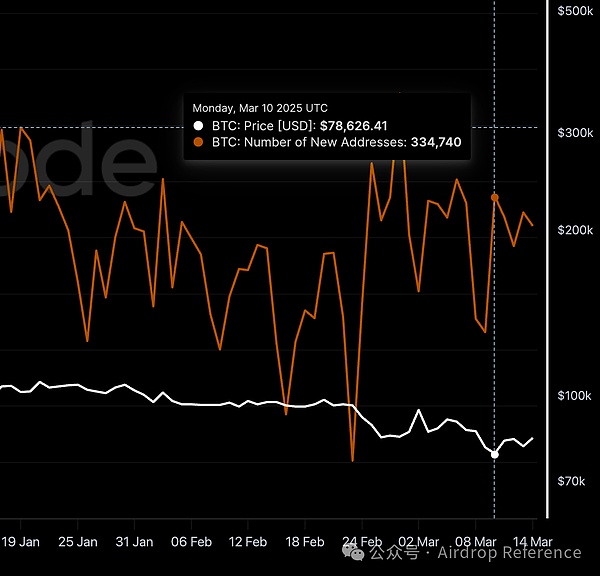

After such a sharp contrast, you can tell at a glance that gold is a better safe-haven asset than Bitcoin. Then I ask you, are you willing to sell your Bitcoins to buy gold now? Anyway, I don't want to, and I think you will definitely not. Moreover, not only those who hold Bitcoin may not be willing to sell it, but more newcomers are joining continuously. Please see the picture below.

From the above picture, you will find that even when Bitcoin is at a historical low of 78,000, there are still 330,000 new addresses for Bitcoin that day. Obviously, behind the contradiction, there must be unknown secrets. Your decision to buy gold without selling Bitcoin is correct, and today I will tell you the real reason behind it. If you don't keep it a secret, the answer is the title. Remove the question mark: Bitcoin, the ultimate hedging plan for long-termists.

Of course, it is far from enough to just tell you the answer. I should also tell you the reasons. At the same time, as a science column, you should also achieve the unity of knowledge and action. So in the end, I will also give a path and method to implement this concept. If you agree with long-termism and are not the kind of person who wants to get rich by relying on leverage trading, then please continue to read.

We must first understand what safe-haven assets are?

1. What are safe-haven assets?Hell-haven assets, as the name implies, refer to market turmoil, economic uncertainty, or other possible causes of traditional investment (such asWhen the value of stocks, bonds, etc.) falls, assets that can maintain or even increase their own value. Such assets are often regarded by investors as a "safe harbor" to protect their wealth from losses during periods of risk.

Hell-haven assets in the traditional sense usually have the following core characteristics:

Low volatility or negative correlation: Ideal safe-haven assets should show relative stability when the market fluctuates violently, and even negatively correlated with those high-risk assets (such as stocks). This means that when the stock market falls, the price of safe-haven assets may rise, thus hedging the risk.

Storestoration Capacity: Safe-haven assets need to have the ability to preserve their value for the long term and be able to withstand the erosion of wealth by factors such as inflation. When people hold such assets, they value their ability to maintain purchasing power rather than pursuing high short-term returns.

Strong liquidity: being able to buy or sell quickly and at a reasonable price when needed is also crucial for safe-haven assets. This ensures that investors can operate flexibly when they need to adjust their asset allocation.

Historical verification: In history, assets that have shown hedging attributes during multiple market crises or economic downturns are often more likely to be accepted and trusted by investors.

The three pillars of traditional safe-haven assets:

Gold: As a millennium hard currency, the safe-haven myth of gold originated from the 70-fold increase after the collapse of the Bretton Woods system in 1971. Its physical scarcity (about 205,000 tons of gold mined worldwide) and anti-inflation properties (annualized yields of about 7.3% over the past 50 years) make it a classic choice for crisis times. Treasury bonds: Taking US Treasury bonds as an example, their "risk-free" label is based on credit, but in 2024, the scale of US Treasury bonds exceeded US$35 trillion, and the actual yield was negative for 18 consecutive months, revealing the inflation trap behind "safe assets".

Help currency: The US dollar, as a global settlement currency, accounts for 59% of foreign exchange reserves during the 2020 epidemic crisis; the yen relies on a low interest rate environment (Japan-0.1%) and the Swiss franc rely on a bank confidentiality system to maintain a safe haven status.

But, gold has long been considered a classic safe-haven asset. In many historical periods, when the stock market falls or geopolitical risks heat up, investors flock to gold, causing its price to rise. Gold itself does not generate interest or dividends, but its scarcity and historical recognition as a store of value make it an important means of preserving value in uncertain times.

However, with the continuous development and innovation of financial markets and the diversification of investors' risk appetite, the definition of "safe-haven assets" is also constantly evolving. Some emerging assets are beginning to show their risk-haven potential in a specific environment, although they may not fully comply with all the characteristics of traditional safe-haven assets. This is also why we will discuss the relationship between Bitcoin and safe haven today.

The most critical sentence in the above paragraph is "investor risk preferences". Because of the existence of "investor risk preference", everyone has different perceptions and feelings about risks. For example, for me, I don't expect to get rich through leverage trading, so the price fluctuations of Bitcoin have never been a risk or an opportunity for me.

So, what is the risk for you?

2. Relativity of riskNow, let's turn our attention to the broader stage and see how risks show different aspects with changes in regions and time.

Imagine that you live in different places and feel the different pressures brought by risks. For example, during the turbulent period of Zimbabwe, hyperinflation turned the currency almost into waste paper. For local residents, holding their own currency is the biggest risk, and they will try their best to convert their assets into more stable foreign currency or physical goods. In an economically stable, such as Switzerland, people may pay more attention to the long-term preservation of assets than the short-term risk of currency depreciation.

This is the "space" relativity of risk - the same assets bear different risks in different economies.

The passage of time will also profoundly affect our perception of risks. Assets that were once considered high-risk may gradually be accepted by the market and regarded as mainstream over time; assets that were once considered safe may also expose new risks due to changes in the times.

Please look at the picture above, you may think that such a large callback must be Bitcoin or other cryptocurrencies, but it is not, but gold.

Because, the risk-averse attributes of gold are not static. In different historical periods, the price fluctuations and safe-haven effects of gold will also be affected by various factors such as economics and other factors. For example, gold shows good risk-haven function in some recessions, but in others, it may not perform well.

With the panoramic view above, you can clearly see that gold experienced significant callbacks in the 1970s, 1980s and 2010s.

So, reposition the coordinates of space-time, what should we do for today's long-termists?

First of all, it is necessary to be clear that a long-termist will not regard making money as a life goal. We all try to do something more meaningful. In addition to work, I choose blockchain science popularization, and you may choose others. But we all have one thing in common, that is, we don’t want to worry too much about making money. We hope to have a once-for-all way to manage our investments. We do not have too high interest demands and are unwilling to take unnecessary risks.

But as long as we still live on the earth, there is a risk that we can't hide even if we want to.

3. Risks of fiat currencyFiat currency, as the name suggests, is a currency granted by a law and forced to be used as a currency in circulation. The banknotes we use on a daily basis, such as the US dollar, euro, Japanese yen, etc., are all fiat currencies. Unlike currencies that have existed in history that have been pegged to a physical object such as gold or silver, the value of modern fiat currencies is entirely based on people's trust in their issuing institutions (usually central banks) and their economic strength.

3.1 DepreciationThe fatal flaw of fiat currency lies in its unlimited supply mechanism. In order to cope with economic downturns, stimulate economic growth or repay debts, the central bank often takes measures to increase the money supply. Although moderate inflation may have a certain positive effect on the economy in the short term, in the long run,, Continuous inflation will lead to a continuous decline in the purchasing power of the currency.

Taking the US dollar as an example, after it was decoupled from gold in 1971, its purchasing power has decayed by 98%. In 2024, the Federal Reserve implemented quantitative easing to cope with the US debt crisis, resulting in a surge in M2 money supply by 23%, and the real inflation rate soared to 8.5%, far exceeding the 2% target. This "money printing tax" is creating a "time black hole" of wealth worldwide - the real rate of return of cash assets held is negative for 18 consecutive months, equivalent to an implicit loss of 6.3% of purchasing power per year.

What is even more severe is the negative feedback loop between sovereign debt and fiat credit: the global sovereign debt has reached 356% of GDP, and US debt has exceeded US$35 trillion, and its "risk-free" label is disintegrating. The Bank of Japan's share of government bonds exceeded 52%, causing the yen to plummet by 15% against the US dollar. This "debt monetization" mechanism is pushing the fiat currency system to the edge of the cliff.

In addition to depreciation, there is also a more important personal sovereign risk. Banks can block or restrict your account at any time.

3.2 ClosingImagine that you have worked hard to accumulate a fortune and stored it in your bank account. This money belongs to you in a legal sense and you can freely control it. However, in real life, your control over this money is not absolute. Banks as intermediaries may, in some cases, limit or even freeze your account. This may be due to suspected legal disputes, cooperation in regulatory investigations, or even just to the bank's internal operational errors.

This indirectness of control over funds is a potential risk of holding fiat currency. Although your wealth exists in the form of numbers, the ultimate control is in the hands of and financial institutions.

Cyprus Capital Controls 2013: To prevent the collapse of the banking system, Cyprus implemented severe capital controls in 2013. Initially, the daily withdrawal limit of banks was set to €300. What is even more shocking is that for bank deposits over 100,000 euros, depositors face up to 60% of their assets, some of which are directly converted into bank shares. These strict capital controls lasted for about two years, severely limiting the dominance of ordinary people over their own wealth.

Argentina Foreign Exchange Control 2011-2015: In order to deal with economic difficulties and prevent capital flight, Argentina implemented complex foreign exchange control measures between 2011 and 2015, strictly restricting individuals and businesses from purchasing USD. This led to the rise of an illegal “black market” dollar transaction, which made it difficult for many individuals and businesses to obtain the USD needed for international trade or savings. It was estimated that at that time, grain exporters hoarded billions of dollars in agricultural products, waiting for the lifting of the control to sell at a more favorable exchange rate, reflecting the significant impact of foreign exchange controls on economic activities.

Iceland Capital Control 2008-2017: In 2008 After the outbreak of the financial crisis in 2017, Iceland implemented nearly a decade of capital controls to prevent large-scale capital flight. These measures strictly restrict foreign exchange outflows, including restrictions on cross-border payments and capital flows. The main reason for the implementation of capital controls was concerns that large amounts of capital outflows from bankrupt banks held by bankrupt Iceland banks could lead to a substantial depreciation of the Icelandic currency Krona. These controls were not gradually lifted until 2017.

2017 Venezuelan Bank Withdrawal Limits: Strict restrictions were imposed on bank withdrawals amid the continued deterioration of the Venezuelan economic crisis. In 2017, the daily withdrawal limit for ATMs was only 10,000 Bolivars, which was worth less than 1 Dollars. Worse, ATMs often have no cash, and people have to queue for hours to withdraw up to 20,000 bolivars at the bank counter, which is far from meeting the needs of daily life.

The above real cases and data clearly show that under the fiat currency system, in a specific economic or crisis period, strong measures may be taken to limit or even freeze individual bank accounts to maintain financial stability or other goals. This is undoubtedly a risk that needs serious consideration for long-termists who pursue long-term wealth security and personal financial autonomy.

In more extreme cases, if you encounter a financial crisis or a bank collapse, your deposit may also face the risk of loss. Although there is protection from the deposit insurance system, there is still a certain upper limit.

For those who pursue greater financial autonomy and personal sovereignty, this is a question that needs to be seriously considered. Now, it should be possible to answer: Why "bitcoin" is a better safe-haven asset for "long-termists".

4. Why should long-termists choose Bitcoin?ItIn fact, the first thing we should exclude is fiat currency, even if it is US dollar, yen, or euro, you should not choose it.

4.1 Fiat Coin Vs. BitcoinWe have seen that taking the US dollar as an example, its purchasing power has shrunk significantly since it decoupled from gold. One of the most eye-catching features of Bitcoin is its constant total amount. The total upper limit of 21 million pieces is written into its underlying code, which cannot be changed.

The supply mechanism of Bitcoin is the first currency contract in human history to be sealed with mathematics: the output is halved every four years, and the total in 2140 is constant 21 million coins. This programmatic deflation model is sharply opposed to the infinite superissuance of fiat currency. Taking 2024 as an example:

Dollar: In order to cope with the US debt crisis, the Federal Reserve expanded its balance sheet by 23%, the M2 money supply exceeded US$22 trillion, and the real inflation rate soared to 8.5%;

Bitcoin: The annual inflation rate fell to 0.9% after the fourth halving, far lower than the 1.7% of gold.

We also discussed the risk of blocking fiat currency accounts above. The decentralized nature of Bitcoin can effectively avoid this risk. The Bitcoin network is not controlled by any single central organization. The transaction records are stored openly and transparently on the blockchain. No one can tamper with or freeze the user's Bitcoin assets at will unless the user leaks his private key himself.

4.2 Treasury bonds Vs. BitcoinTreasury bonds, especially sovereign debts like the U.S. Treasury bonds have long been considered "risk-free assets" in the financial market. This concept is based on credit, and investors believe in the ability to repay the bonds they issue. During times of market turmoil, funds often flow to Treasury bonds in search of security.

However, for today's long-termists, considering Treasury bonds as an ideal safe-haven asset may require more careful thinking, especially in the current global economic landscape, where some data and facts have revealed the possible pitfalls behind traditional concepts.

As we mentioned before, taking the U.S. Treasury bonds as an example, its size has exceeded $35 trillion in 2024. Such a huge debt scale, and the negative real yield for 18 consecutive months, point to a core question: Can Treasury bonds still effectively resist inflation?

Negative real rate of return means that after deducting inflation factors, holding these so-called "safe assets" is actually losing purchasing power. This is obviously unacceptable for long-termists who pursue long-term preservation and appreciation.

In addition, the global sovereign debt has reached 356% of global GDP, a worrying number. Some, such as Japan, have held more than 50% of the government bonds, which has led to a sharp drop in the yen exchange rate. This trend of "debt monetization" has also faced challenges in the long-term security of some government bonds that are traditionally considered safe. It is not a wise move for long-term investors to invest a large amount of money in assets that may be at risk due to the sovereign debt crisis.

Bitcoin, by contrast, is a decentralized digital asset, its value does not directly depend on any single credit. While it also faces its own risks, it offers an option to decouple from the traditional financial system in the long run, which may be more attractive to long-termists who are concerned about the risks of sovereign debt.

Of course, as a low-volatility asset, Treasury bonds may provide certain stability in the short term when market turmoil. But for long-termists who focus more on long-term wealth preservation and growth in the coming decades, it may not be enough to pursue short-term stability. What they need is assets that can resist long-term inflation and have long-term growth potential. From this perspective, despite the volatility of Bitcoin, its unique scarcity and decentralized nature, as well as its huge potential in the digital economy era, make it a better long-term safe-haven option than traditional Treasury bonds.

4.3 Gold Vs. BitcoinAs we mentioned before, gold has achieved an annualized rate of return of about 7.3% over the past 50 years, making it a good long-term value preservation tool. But if we turn our attention to Bitcoin, its long-term performance will be even more eye-catching.

According to Curvo.eu's backtest data (as of March 2025):

The total return of Bitcoin was about 1067.5%, while gold was about 88.8%. Bitcoin’s average annualized return is 63.5%, much higher than gold’s 13.5%.

The past decade: Total return rate of BitcoinIt is as high as 51,259.5%, while gold is about 142.7%. In terms of average annualized return, Bitcoin is about 86.7%, which is also significantly higher than gold's 9.3%.

Nasdaq Nasdaq also pointed out in an article in September 2024 that in the past decade, Bitcoin has been the best performing asset in the world, with an average annualized return of up to 693%, while gold was only about 5% during the same period.

In addition, Bitcoin's annual inflation rate after the fourth halving was 0.9%, which is only 53% of gold (1.7%). Bitcoin will become increasingly scarce.

Secondly, portability and storage costs are another limitation of gold. Holding a large amount of gold requires physical storage space, accompanied by security risks and storage costs. Bitcoin exists in digital form and can be stored in various electronic devices, with almost no storage cost and is easy to transfer globally, which is an important advantage for an increasingly globalized world.

In addition, Bitcoin is far better than gold in terms of separability. Bitcoin can be divided into eight decimal places (i.e. Satoshi), which makes small transactions and investments more flexible and convenient. The cost of gold segmentation and trading is relatively high.

More importantly, Bitcoin, as a digital asset born in the Internet era, has higher transparency and verifiability. All Bitcoin transactions are recorded on public blockchains that anyone can query and verify, which reduces the risk of fraud and forgery to some extent. The authenticity and purity of gold are sometimes difficult to identify.

In addition, from the perspective of market size growth, although the total market value of gold is still far higher than Bitcoin, the growth rate of Bitcoin is impressive. Currently, Bitcoin’s market value is close to $2 trillion, while gold’s estimated market value is about $18.5 trillion. Galaxy Research predicts that by 2025, Bitcoin’s market value is expected to reach 20% of gold’s market value. This shows strong expectations for Bitcoin’s future growth.

Finally, from the perspective of adoption rate, gold has been widely accepted as a mature asset, but Bitcoin has been a newXing's digital assets have an adoption rate of only 3%, indicating that Bitcoin has a broader future. As I noted in "Above Trends, Between Cycles: Cold Thinking of Bitcoin's "Callback Moment", a 3% adoption rate equals the Internet in 1990, online banking in 1996, and social media in 2005.

Long-termists choose Bitcoin not to completely abandon gold, but to see that in the future, Bitcoin may show stronger potential than gold in fighting the depreciation of fiat currency, protecting personal wealth, and seizing opportunities for the development of the digital economy. We are willing to take on volatility in exchange for possible future returns.

So, how should long-termists invest in Bitcoin?

Leave enough living expenses and start DCA.

5. Why is DCA the way for long-termists to invest?DCA is the abbreviation of Dollar-Cost Averaging, an investment strategy that refers to investing a fixed amount of asset at a fixed time interval (such as weekly and monthly), regardless of the price of the asset. As we discussed earlier, Bitcoin, as an emerging asset, has much greater price volatility than traditional safe-haven assets such as gold and Treasury bonds. Although we are confident in the value of Bitcoin in the long run, price fluctuations in the short term are unpredictable. For long-termists, they do not pursue profits from short-term market volatility, but focus on long-term returns in the years or even decades ahead. In this case, the DCA strategy is particularly important and effective.

The most direct benefit of this kind of batch investment method is to reduce the pressure on investors to try to "buy at the bottom". No one can accurately predict the lowest point of the market, and even professional traders often make mistakes. Long-termists know this well, and they focus more on long-term trends than short-term fluctuations. The DCA strategy allows them to not guess when the market will bottom out, but just insist on investing in the established plan.

In addition, DCA helps overcome the weaknesses of human nature. When the market rises, people often buy high because they are afraid of missing out; when the market falls, they are prone to cut their losses and leave because of fear. DCA strategy helps investors stay calm and rational through regular investment, avoiding short-term emotions, and thus being able to adhere to long-term investment.Strategy.

以 2015-2025 年数据测算:

每月 100 美元 DCA:总投入 1.2 万美元,终值达 11.1 万美元,年化收益率 25%;

同期标普 500 指数 DCA:终值仅 2.1 万美元,年化收益率 9.8%。

This difference comes from the exponential growth characteristics of Bitcoin. DCA is like "time and space arbitrage" in the Bitcoin ecosystem - exchanging the scarcity premium of Bitcoin at the depreciation rate of fiat currency.

Recalling the historical price trend of Bitcoin, we can see that despite many large pullbacks, its long-term trend is still upward. If an investor insists on adopting the DCA strategy since the beginning of Bitcoin, no matter how many times it has experienced "halved", its final return on investment will be very considerable. Of course, past performance does not represent the future, but the essence of DCA strategy is to diversify risks and reduce the impact of the timing of a single buy on the final return.

For long-termists, we pursue a "one-and-all" investment method and do not want to spend too much time and energy on researching and predicting the market. The DCA strategy fits exactly this need.一旦设定好投资计划,就可以定期自动执行,无需频繁操作,从而将更多的时间和精力投入到更有意义的事情上,例如个人的事业发展、家庭生活或者社会贡献。

因此,对于认可比特币长期价值,并希望以一种省心省力的方式参与其中的长期主义者来说,DCA 无疑是一种非常合适的投资策略。 You may ask, what should you do if you don’t buy Bitcoin? It's very simple, exchange it for US dollar stablecoins. Here is a zero-basic tutorial on stablecoins.

In the cryptocurrency market, DCA is already a relatively mature service, with many ways.如果,你想直接在中心化交易所买入比特币然后发送到冷钱包,这里有两个零基础教程,一个是关于如何购买比特币的(https://t.co/2IzQI80lll ),另一个是如何将比特币发送到冷钱包的(https://t.co/sbT1E9A3bw ).

I recommend the ARP2 project of "Airdrop Reference", because in this project you can not only invest in bitcoin regularly, but also get the additional benefits of automatic rebalancing. For details, please see here (https://t.co/9E8Q9XWe0J).

ARP2 still has 43.77% of the profit even when Bitcoin has plunged. The only drawback to this project is that you need to complete the investment manually every time.

Conclusion: Awakening of Values across the dimension of timeIn the monetary epic of human civilization, gold once used thousands of years to forge the "Temple of Value", fiat currency weaves "flowing illusions" with credit, and Bitcoin is reconstructing the "Tower of Digital Babel" with mathematics and code. This speculation about safe-haven assets is essentially a game between human nature and time - gold carries ancient beliefs about physical scarcity, while Bitcoin shows a future consensus on the absoluteness of digital.

The choice of long-termists is never a simple asset replacement, but a redefinition of monetary sovereignty. When the "inflation tax" of fiat currency erodes wealth, and when the "geographical shackles" of gold restrict flow, Bitcoin opens up a third path for individuals to fight against systemic risks with the transparency of "code is law" and the control of "private key is sovereignty".

History repeatedly proves that the real risk avoidance is not to escape from fluctuations, but to anchor the future. Just as time will eventually reveal the illusion of all bubbles, it will also precipitate the light of true value. Bitcoin, a decentralized network based on mathematics and consensus, is showing potential beyond traditional safe-haven assets in the test of time with its scarcity, verifiability and growing adoption.

Choose Bitcoin is not a short-term speculation, but a belief in the future. It represents a new concept of wealth - not relying on centralized authority, but returning control of value to individuals. For us long-termists who are unwilling to consume life in the mist of chasing wealth, Bitcoin may be the key to opening the door to future value.

Let us take the patience of time as our sail and the long-termism as our rudder, and sail towards the other side of wealth that is more autonomous and safe.