49 mins ago

2,905

Author: Stacy Muur Translation: Shan Oppa, Golden Finance

Although Bitcoin and Ethereum set a precedent for digital payments, it is difficult to achieve mainstream adoption due to slow speed, high costs and large price fluctuations.

We rarely see anyone buying coffee or paying rent with BTC or ETH for simple reasons: high transaction fees, slow settlement times, and price fluctuations make it difficult to use for daily payments.

Stablecoins (such as USDC and PYUSD) have improved payment efficiency, but have not fully released the time value of the currency or achieved seamless integration with traditional finance.

This is where PayFi comes into play. It connects DeFi, real-world assets (RWAs), and on-chain credit, making payments instant, efficient, and scalable.

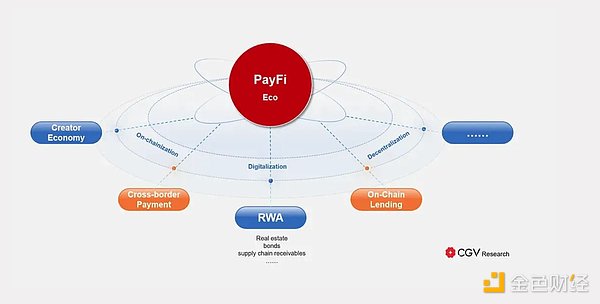

PayFi: a new model of payment finance

PayFi (Payment Finance) is an innovative financial model that integrates traditional payment systems with decentralized financial services through blockchain technology to improve the efficiency, transparency and accessibility of financial transactions.

PayFi's core value propositionPayFi's core concept is the Time Value of Money (TVM), that is, due to the potential value-added ability, today's money is more valuable than the same amount of money in the future.

In other words, would you get $100 today or $100 a year later?

Most people will choose to get it today because the money can be invested, pledged or generated income, and the $100 you get in the future may depreciate due to inflation and opportunity costs.

How does PayFi release the time value of currency?Traditional finance traps capital in slow-moving systems. Delayed settlement, illicit assets and rigid credit structures hinder the effective operation of funds and create for both individuals and businesses.It has become a bottleneck. PayFi changes this situation by enabling real-time trading, automatic lending and instant access to future cash flows, keeping liquidity flows.

Whether it is changing the "buy first and pay later" model into a revenue generation model, helping companies obtain funds from unpaid invoices, or allowing creators to obtain income instantly, PayFi is making the financial system more flexible and efficient. By connecting DeFi, risk-weighted assets and on-chain credit, it ensures that funds are not idle but are active.

Buy-as-you-go (BNPN): Going beyond debt-driven consumptionBNPN redefines people's consumption methods and replaces debt models with income-based spending. Users no longer need to make loans and repay in installments, but instead pledge assets and use their proceeds to pay for expenses. The principal remains unchanged, so users can consume without borrowing.

Before PayFi:

The traditional "buy first and pay later" (BNPL) service seemed convenient at first, but it relies on credit and debt. Users often face hidden fees, interest and overdue fines, causing consumption costs to continue to rise over time. Moreover, one late payment may affect the credit score.

With PayFi:

BNPN allows users to pledge assets and use the generated income to pay for consumption. Users can enjoy the benefits of consumption without having to bear the financial burden of repayment. No interest, no overdue fees, no credit score impact - a smarter and more sustainable way to consume.

Accounts Receivable Financing (ARF): Solve the cash flow problem of enterprisesFor enterprises, waiting for customers to pay can become a major obstacle to operations. ARF allows businesses to convert unpaid invoices into real-time capital, ensuring stable cash flow without relying on expensive loans or lines of credit.

Before PayFi:

Companies usually have to wait weeks or even months before receiving payments from their customers. This delay increases the difficulty of operational management, making it more difficult to pay wages and invest in growth. Many businesses have to rely on loans or credit lines to fill the funding gap, which increases the additional interest cost.

With PayFi:

Accounts Receivable Financing (ARF) enables companies to tokenize invoices and obtain liquidity immediately. Instead of waiting for payment to arrive, companies can directly convert unsettled accounts receivable into funds to ensure smooth business operations and reduce their reliance on traditional financing.

PayFi OverviewImagine PayFi is a multi-layered financial cake, each of which plays a crucial role in making decentralized payments faster, more efficient and more scalable.

1. Application layer (front-end experience)can be regarded as the application you use every day, whether it is a payment platform, lending service, or DeFi wallet. These companies are building real-world user experiences based on PayFi technology.

This is where users, enterprises and financial applications access PayFi. From DeFi lending to cross-border payments, this layer makes PayFi available.

The following lists projects that embed blockchain payments into the field of daily finance and enable real-world applications.

Stripe makes it easier for businesses to accept crypto payments while maintaining compliance with traditional finance.

Rain and ReapGlobal focus on simplifying cross-border payments and solving practical inefficiency problems in global transactions.

Arf is providing a bridge to instant credit through stablecoin-driven trade financing.

Other well-known players include Bitso, Sanctum, Sphere, Kulipa, Fonbnk1, etc.

2. Financing layer (funding promoter)This is where PayFi’s real magic lies—liquidity providers, credit markets and financial instruments are all here. These protocols help users unlock funds, borrow and lend funds in real time.

If PayFi is a car, then this layer is the engine—pushing funds where they need it in seconds rather than days.

Some pioneering entities in the field include:

Huma pioneered the launch of loans for future cash flows, allowing businesses and individuals to borrow based on expected earnings.

Credora makes risk assessments more transparent and actionable, providing lenders, debits and ecosystem participants with the confidence they need to make informed decisions.

3. Compliance layer (oversector)Cryptocurrencies still require security and compliance, which ensures that funds flow safely and legally. The companies here focus on fraud detection, KYC, AML and regulatory risk management.

PayFi adoption will slow down due to uncertain regulation. These platforms help connect DeFi to real-world regulations.

Chainalysis helps track blockchain transactions, prevent fraud and ensure PayFi operates in a legal environment.

TrmLabs focuses on real-time risk monitoring, helping institutions and regulators ensure the security of financial transactions.

Polyflow is a PayFi protocol that connects real-world assets with DeFi through a modular, compliant and friendly crypto payment infrastructure.

Elliptic – A blockchain analytics company that provides risk intelligence, compliance solutions and fraud detection for cryptocurrency companies and regulators

4. The custody layer (digital safe)This layer provides secure storage for assets, ensuring that institutions and individuals do not lose money due to hackers or mismanagement. It can be considered as a cryptocurrency equivalent to a bank vault.

Large institutions need a safe way to hold their funds before entering the PayFi market.

FireblocksHQ is one of the largest brands in the field of digital asset security, providing enterprise-level hosting solutions.

Copper&Cobo focuses on multi-party computing (MPC) Safe, helping institutions manage assets safely.

5. Currency layer (currency itself)This layer supports actual transactions, using stablecoins and digital assets to effectively transfer value across borders.

Without digital currency, PayFi would not exist—stablecoins ensure fast, cheap, and borderless transactions.

USDC and PYUSD (Circle and PayPal) are regulated stablecoins that make PayFi transactions more reliable for businesses and financial institutions.

Tether (USDT) remains the most widely used stablecoin, ensuring liquidity in global markets.

6. Transaction layer (L1/L2 blockchain infrastructure)The basic layer that makes all this possible. Here, transactions are processed, verified and settled at lightning speed.

The faster and lower the cost of this layer, the better the performance of PayFi. That's why high-speed blockchains like Solana and Stellar are at the forefront.

This chart is not only a detailed analysis of the company, but also a snapshot of the future of decentralized finance. PayFi connects traditional finance and DeFi while making payments instant, scalable and accessible.

Solana and Stellar are designed for financial transactions, providing high-speed processing at a fraction of the cost of traditional networks.

Future Outlook: The convergence of PayFi, DePIN and RWAPayFi, DePIN and RWA are fusing together as finance is evolving in real time. Traditional systems run slowly, DeFi has been trapped in its own bubble, and real-world integration is always a missing link. This gap is narrowing and everything is changing.

This is the first time that funds are not just flowing, but are playing a role. PayFi turns payment into a revenue-generating system. Risk-weighted assets release liquidity from real-world assets. DePIN ensures that infrastructure can run on its own with automated on-chain payments. The boundaries between finance, infrastructure and business are becoming blurred. As a result, the economy will rely on real-time, programmable liquidity rather than outdated financial tracks.

This transformation is not to speed up transactions, but to redefine how currency, assets and infrastructure interact. PayFi is not another DeFi trend, but the foundation of a system that incorporates finance into everything we do.

ConclusionPayFi is a structural upgrade of the way capital flows. With the deep integration of real-world assets (RWA) with blockchain, finance is transforming from static traditional institutions to dynamic, programmable systems. Payment is no longer just a simple transaction, but profitable, automated, and embedded in the infrastructure.

The boundaries between finance, commerce and infrastructure are gradually blurring, and PayFi is at the heart of this change. Whether it is instant settlement, machine-driven payment, or income-based expenditure model, a system that operates in real time, frictionless, and does not rely on traditional financial tracks is being established.

The trend has been very clear: finance is coded, liquidity is becoming programmable, and financial access is becoming boundless. PayFi is not a brief innovation, but the infrastructure of the next generation of economic systems.