31 mins ago

4,501

Source: Dragonfly; Compiled by: Wuzhu, Golden Finance

Airdrop is a strategic tool for blockchain adoption and value distributionAirdrop distributes tokens directly to the wallet address (usually free), and is a strategic tool for blockchain projects to enhance user engagement, decentralize token distribution and reward community loyalty. This analysis explores the impact of airdrops in the blockchain ecosystem and provides insights on how they contribute to the broader goals of value creation and distribution in emerging digital economies.

We analyzed data from 12 airdrops (11 geoblocked airdrops and 1 non-geographed airdrop as a comparison) between 2019 and 2023 to determine the economic impact of preventing US users from receiving tokens.

Number of Americans affected by geographic blockade: We estimate that in 2024, between 920,000 and 5.2 million active U.S. users (5-10% of the estimated 18.4 million to 52.3 million cryptocurrency holders in the U.S.) are generally affected by geographic blockade. These limit airdrop participation and limit their use of certain projects.

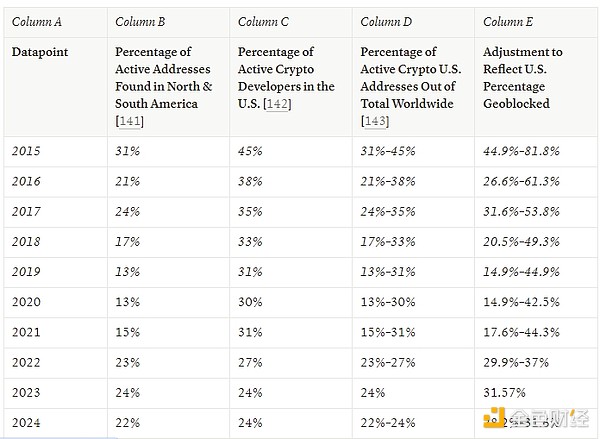

Percent of active US addresses in 2024: About 22-24% of all active encrypted addresses worldwide belong to U.S. residents.

Total airdrop value in our sample: Of our 11 project samples, they have created a total of approximately $7.16 billion in total value to date, with approximately 1.9 million claimants worldwide participating during this period, with an average median claim value of approximately $46,000 per eligible address.

Estimated revenue losses for U.S. users based on our sample: Among our 11 samples of geo-blocked airdrops, the total revenue losses for U.S. users are estimated to be between $1.84 billion and $2.64 billion from 2020 to 2024.

Estimated revenue losses for U.S. users based on CoinGecko’s sample: Applying the percentage of our active U.S. addresses to another 21 geo-blocked airdrop sample analyzed by CoinGecko, the potential total revenue losses for Americans could range between $3.49 billion and $5.02 billion between 2020 and 2024.

Personal Tax Income Missed Due to Geographical Lockdown Airdrops: Based on our sample of Geographical Lockdown Projects (for the lower limit) and CoinGecko (for the upper limit), the estimated loss of federal tax revenue from geographic lockdown airdrops between 2020 and 2024 is estimated between $418 million and $1.1 billion in 2024, with an additional estimated state tax loss of $107 million to $284 million. Overall, this means an estimated tax loss of $525 million to $1.38 billion. These estimates do not include the additional capital gains tax that will arise after the final sale of these tokensTaxation, which is another source of loss for income.

Offshore migration leads to corporate tax losses: The transfer of cryptocurrency businesses overseas has significantly reduced tax revenue in the United States. For example, Tether reported that the company had a profit of $6.2 billion in 2024, but the company was incorporated overseas and could be paid about $1.3 billion in federal corporate tax and $316 million in state tax if the company fully accepts U.S. taxes. While actual liability depends on the company structure, it is only a company, which suggests that cryptocurrency companies operate overseas will cause wider tax losses.

ForewordCryptocurrency and blockchain technology are not fleeting technological trends; it is a major shift in the global economic landscape, providing the United States with a golden opportunity to provide visionary leadership and pioneering governance in this transformative industry. However, the United States did not accept this role, but found itself trapped in internal struggles and efforts to undermine the development of this new model.

In such an environment, it is no surprise that many crypto projects are reluctant to engage with American users, as fuzzy application of digital assets hinders them. This uncertainty leads to significant financial losses and limits U.S. users’ opportunities to participate in the industry, including participating in airdrops—an innovative approach to distributing new tokens and promoting user engagement.

This report is intended to provide data-driven insights into the role of cryptocurrency airdrops in accelerating economic growth and to illustrate financial losses due to U.S. restrictions. It will meet the urgent need for regulatory frameworks that support innovation, while providing clear guidelines to protect investors and market integrity. Our analysis explores the tangible economic impact of current regulatory practices, including detailed indicators of geofencing of US users to prevent airdrops and the resulting tax losses.

We advocate for regulatory change by examining these key factors and a broader analysis of the U.S. regulatory environment and its impact on the cryptocurrency sector. These adjustments will enable U.S. citizens and businesses to actively and effectively participate in the global cryptocurrency market, using airdrops to stimulate job creation, drive business growth and increase tax revenue. The urgency of this study is underscored by the ongoing development of the global digital economy and the need for the United States to take a more competitive and supportive regulatory stance to maintain its leadership.

This paper adopts a two-pronged approach to analyze airdrop distribution, and utilizes off-chain and on-chain data sources. By combining these complementary datasets, the analysis aims to provide a comprehensive assessment of the distribution patterns, token claims and valuation dynamics of multiple projects in the United States. Our approach aims to test specific assumptions about the effectiveness and coverage of airdrops in the U.S. cryptocurrency ecosystem. The key questions we aim to answer include:

- How many percentages of cryptocurrency users worldwide are U.S. users?

- How many active US cryptocurrency users are affected by geo-blocking practicesring?

- Will geographic blockade of US claimants lead to significant revenue losses for users and the United States?

1. Definition of airdrop background airdropWhat is airdrop?

Cryptocurrency airdrop is a way to distribute platform native tokens to a specific wallet address without paying money. Blockchain startups often use airdrops to attract early interest and support for their projects, promote decentralization by expanding token distribution, and reward community engagement. [6] Typically, airdrops involve sending small amounts of tokens to the wallets of active users within the project ecosystem. [7] Airdrops usually reward those who are always informed of cryptocurrency developments, participate in social media communities, and meet certain criteria. [8]

How to determine the short investment range?

Blockchain projects use various methods for airdrops—in most cases, combined with several methods to maximize impact. This tailored approach ensures that airdrops are not only used to distribute tokens, but also support the broader goals of the project, such as user acquisition, community building or market penetration. The project uses various criteria to determine eligibility for receiving airdrops, including the following:

Past activities. The team determined a series of heuristics based on previous on-chain activities to derive the claimable amount for each address. These methods usually consider past interactions with airdrop protocols. Additionally, these protocols often reward users for previous activity on competitor platforms, part of a strategy called vampire attacks designed to entice users away from competitors.

Early Contributors. In almost all cases, airdrops reward early users. Airdrop participants will choose to receive tokens individually based on a variety of factors such as reputation and contribution to the project. [9] This approach is a more centralized way to reward early and active users’ participation, providing targeted rewards for those who have made significant contributions to the community or project. [10]

Snapshot. Existing token holders receive token time based on their actual token holdings at a specific point in time. [11] Take a "snapshot" of the blockchain, recording all transactions and balances to determine whether you are eligible for airdrops. [12]

Fork. Forking refers to the splitting of the blockchain into two independent chains to distribute new tokens to users. [13] Most of the time, if you hold the original token of the forked chain, you are eligible for this airdrop. This ensures that new tokens are widely distributed among existing holders, providing an established broad user base for newly created chains from the outset. [14]

Raffle lottery. Some airdrops are combined with a raffle draw, and participants have the opportunity to get a raffle ticket by holding tokens, accumulating points, or simply expressing interest. [15] This is usually used when the number of individuals interested in airdrops exceeds the number of tokens that the project plans to distribute. In this case, a raffle is held, with a limited number of wallets randomly selected to receive airdrops, adding some opportunity elements to the process. [16]

How do users who meet the criteria receive airdrops??

In most cases, the airdrop collection process follows a similar structure. Airdrop collection smart contracts are created by the project team, which contains a list of address qualifying and related available amounts. The user goes to the collection website, proves the ownership of the address by connecting to the wallet, and then collects the allocated tokens. In some cases, users can also register using other blockchain addresses or accounts on off-chain platforms such as X, Github and Discord, which may have related receivable tokens.

In most cases, users must take the initiative to collect tokens. In rare cases, the project may not require the user to take any proactive steps, but instead transfer the tokens to each recipient in batches, which is usually done with low transaction fees. If the airdrop date is consistent with the blockchain creation date, the token may be distributed via airdrop at the time of blockchain creation, thus mitigating the need for transfers.

How is airdrop technically executed?

Performing airdrops involves multiple technical processes. First, the process involves defining airdrop parameters and ensuring that all prerequisites are in place. This involves establishing eligibility criteria, determining total token allocations, specifying schedules for airdrops, finalizing snapshot dates, allocation mechanisms, and any related claims requirements to provide a clear framework for subsequent steps. In addition, existing wallets and network activities can be audited to improve eligibility criteria to meet the project's objectives. [17]

To identify qualified participants, blockchain snapshots will be taken on a specified date. The system utilizes advanced snapshot tools to capture wallet status that meets predefined criteria and provides a verifiable recipient ledger. The system filters data to exclude unqualified addresses, such as dormant wallets or known robots, ensuring that the distribution list is fair and accurate. [18]

At the same time, the development of airdrop smart contracts is also to automate the distribution process. These smart contracts play a key role in automated distribution, ensuring fairness and transparency, while eliminating the need for manual intervention and efficiently handling tasks such as managing lists of qualified wallets and allocating the appropriate number of tokens. [19]

Before deployment, smart contracts will undergo a comprehensive third-party security audit to identify and resolve vulnerabilities and ensure they can resist potential attacks. Anti-robot mechanisms, wallet verification protocols, and repeated claims prevention are integrated into the contract to provide additional security. [20]

After preparing the qualification list and smart contract, new tokens will be generated specifically for the airdrop process for distribution. The tokens will then be transferred to a designated distribution wallet under the control of the smart contract. This ensures that all tokens used for airdrops are securely managed in a traceable environment. [21] Through smart contracts, wallets identified during snapshots can seamlessly receive their allocated tokens. For claims-based distributions, participants will be notified through official communication channels and provide detailed instructions to ensure user-friendly access. Throughout the process, the blockchain provides all transactionsand thus enhance transparency and accountability.

Evolution of Airdrop

Airdrop was originally a mechanism to attract users and distribute tokens, but later evolved into a more complex tool influenced by user expectations, regulatory interpretations, and market behavior.

Initial Phase: Large Gift (2014-2019):

The initial airdrop is a simple token distribution mechanism used to create an initial market and increase project visibility. [22] A classic example is the Aurora Coin issued in Iceland in 2014, which aims to provide cryptocurrency to all Icelandic citizens as a form of universal access. [23] Users need to actively collect tokens. [24] Aurora experiment marked the beginning of airdrops as a digital asset distribution strategy, although it was restricted in attracting users to participate in the decentralized ecosystem. The subsequent airdrops of the era involved distributions of platform forks (such as Zcash in 2018) and community building (such as Stellar’s XLM in 2016)—essentially focused on rapidly expanding the user base rather than meaningful interaction with the protocol.

Retrospective and regular airdrops (2020-present):

After Uniswap airdrops in 2020, the airdrop distribution model has become a more strategic tool, marking a critical moment in the evolution of airdrops. When Uniswap found itself under attack by SushiSwap, a Uniswap fork platform that provides token-incentives for users, Uniswap counterattacks with its own tokens and airdrops. [25]Uniswap rewards users who have previously interacted with the platform with UNI tokens, which gives governance rights within their ecosystem. [26] This successful, traceable airdrop shows that airdrops are promoting decentralized governance and positioning them as both a user reward mechanism and a tool for community participation. [27]

After Uniswap's success, airdrops have evolved to reward users based on protocol usage. [28] These changes encourage behaviors that are directly beneficial to the project and help build an engaged community. For example, the 2021 dYdX airdrop interacts with the dYdX protocol based on specific transaction volume rewards implemented in a specific time frame. [29]

In addition, the project has begun attempting to phased or periodic airdrops in order to provide feedback on the airdrop design. An example is Optimism, which launched its fifth airdrop in November 2024. In this airdrop, the project rewards users who interacted with at least 20 smart contracts on their hyperchain between March 15 and September 15, 2024, and later developed to also reward users who interact frequently with various categories of applications on their hyperchain. [30]

However, withAirdrops are becoming more and more popular and they are beginning to have unintended consequences such as “cultivation” behavior, which participants can play with the system to drop from the airdrop. [31] Users start to expect airdrops and interact with the platform simply to qualify for future token allocations, usually through surface or minimal interaction. [32] The problem with this is that airdrop farmers rarely increase long-term value because they stop farming and sell immediately after receiving and rarely participate in the project. Interestingly, projects become savvy and sometimes use mining behaviors that occur on the protocol to raise usage metrics. Overall, over time, mining behavior weakens the effectiveness of airdrops in promoting organic use, and instead users try to use these airdrops to acquire as much value as possible. [33]

In response to airdrop mining, the project implemented a sybil attack detection procedure before determining the airdrop allocation, which included certain addresses on the airdrop claim blacklist. However, mining behavior develops as fast as sybil attack filtering, resulting in a continuous cat-and-mouse game between projects and airdrop miners.

While innovative thinking has greatly promoted the evolution of airdrop design, the US legal environment has become one of the most important factors affecting its development trajectory. The project faces scrutiny from regulators such as the Securities and Exchange Commission (“SEC”) and the Commodity Futures Trading Commission (“CFTC”), prompting people to carefully consider the structure of airdrops to avoid triggering legal pitfalls.

To reduce the risk of triggering SEC or CFTC actions, the project excludes U.S. users [34] or avoids early announcement of airdrops, thereby reducing any signs of soliciting investments, which may otherwise be interpreted as an attempt to create a secondary market that indirectly benefits the issuer. This strategy is strengthened by ensuring that no compensation is received directly or indirectly from the recipient.

In response to increasing regulatory pressure, some projects have explored alternative token allocation models. These models include "locking airdrop", where users lock assets within the protocol in exchange for tokens (the longer the locking time, the more tokens you get); [35] and Dutch auctions, where tokens are released at a price cut, allowing participants to buy at a price consistent with market demand, ensuring fair and transparent distribution. [36] These models are designed to deal with complex regulatory environments, but they are still not tested to a large extent in the legal environment and may still face scrutiny. Most projects continue to rely on established low-risk strategies and are cautious about trying new models that are not legally tested, as they can lead to regulatory challenges.

Ultimately, the evolution of airdrops demonstrates a balance between innovation and compliance. When projects strive to attract users and reward loyal participants, they must also deal with regulatory environments that view many of these strategies as potential securities transactions. This often leads to market distortions and undue incentives, obscuring the full potential of airdrops and how they continue to grow organically.

2. Current U.S. Regulatory EnvironmentThe U.S. cryptocurrency industryIt is at a critical moment, facing strict regulatory scrutiny, which could kill innovation and bring promising projects overseas. Recent enforcement actions by the SEC and Commodity Futures Trading Commission highlight the shift to “law enforcement regulation” where institutions impose penalties and litigation on individual projects to establish regulatory standards rather than creating clear and consistent rules. This approach (particularly the SEC practice) bypasses formal rule-making requirements and poses blatant overreach through the fact that regulation of key emerging technologies is a blatant overreach that the original securities laws of 1933 and 1934 did not consider nor address. [37]

This strategy brings great uncertainty and risks, has a chilling effect on innovation and forces many crypto projects and companies to seek clearer regulatory frameworks overseas. This uncertain atmosphere complicates the compliance of startups and established companies, forcing many companies to seek a more favorable regulatory environment abroad and raises questions about the long-term legitimacy and transparency of U.S. regulatory practices in this area.

Is a cryptocurrency a securities, commodities or something else - *Ouve* Test

The Securities Act of 1933 (the “Securities Act”) and the Securities Exchange Act of 1934 (the “Transaction Act”) granted the SEC the power to regulate “securities”, a term widely defined in two regulations through a detailed list of categories, including stocks, bonds, warrants and “investment contracts.” [38] It is worth noting that terms such as “tokens,” “cryptocurrency,” and “digital assets” do not appear in this definition. Therefore, the SEC attempted to classify these assets as "investment contracts" by applying the quadruple*Ouvian test.

The Howey Test originated from the Supreme Court case in 1946 SEC v. W.J. Howey Co., is the main criteria for determining whether a transaction qualifies for an “investment contract” and is therefore bound by U.S. securities laws. [39] To be considered an investment contract, it must involve: (1) investment in money, (2) investing in a common enterprise, (3) expecting profits, and (4) mainly from the efforts of others. [40] However, applying the Ouvian test to crypto assets raises new and complex problems, as the test was originally intended to regulate traditional securities, which are often centralized and rely on identifiable entities that are obliged to investors. [41]

Crypto assets themselves often lack the basic characteristics of securities. [42] Under Howey rules, the key to a transaction being recognized as a security is the structure and context of the specific transaction (such as an ICO, i.e. raising funds and promising profits), rather than the underlying asset itself. [43] By contrast, many tokens in the secondary market do not establish the necessary legal relationships that identify the issuer and the individual token holder, which is a key feature that distinguishes securities from other assets. [44] In addition,Cryptokens usually do not promise or imply profits associated with ongoing management or entrepreneurial efforts. Therefore, viewing crypto tokens as securities may require the introduction of a completely new concept in securities laws: "securities independent of issuers", which no current legal precedent supports. [45]

The regulatory ambiguity surrounding crypto airdrops and token classifications highlights a major challenge facing the crypto industry: the inability to “come in and register.” [46] The existing U.S. securities laws are designed for centralized assets such as stocks and bonds, issued by identifiable entities and have an ongoing obligation to investors, making traditional registration requirements unsuitable for decentralized, practical-focused tokens. These laws do not take into account the various token types—stable coins, governance tokens and practical tokens—each plays a different role in its ecosystem. For example, a practical token can grant access to the service, while a governance token allows holders to participate in decentralized decisions. Unlike traditional securities, these tokens usually do not promise profits or direct financial returns, which challenges the assumption that digital assets are essentially an investment contract and therefore a securities.

The diversity of distribution models in the encryption field further complicates the regulatory environment. Unlike traditional assets issued through a single centralized entity, crypto tokens are distributed through mining, forks, airdrops, and ICOs, with the structure and purpose of each method varying greatly. [47] For example, mining generates tokens as rewards to network participants rather than through financing investment plans. The fork splits the existing blockchain into a new token and distributes it to holders for free, while airdrops involve giving out tokens to expand network adoption rather than raising funds. [48] These models generally do not meet the criteria of “investment of funds” and “expect to profit from other people’s efforts” under the Howie test, challenging the assumption that tokens are essentially securities based solely on their issuance.

The real problem lies in the nature of the transaction, not the token itself. The Howie Test is used to determine what constitutes an investment contract, and it focuses on the situation of the transaction—the commitments, relationships and expectations of both parties to the transaction, not just assets. [49] For example, if the token is sold to fund a project under an investment plan, it can be considered a security. But the same token, if later freely traded in the secondary market without any accompanying contractual commitments or obligations, does not necessarily become a securities. This distinction reflects the core legal principle, namely, transactions, rather than assets, which determine whether an investment contract exists. Just like the Orange Garden in the landmark Howie case [50], the assets themselves (the tokens in this case) are not an investment contract just because they are sold. The situation and nature of the transaction determine whether the transaction itself meets the investment contract qualification under the Ouvian case.

In this case, traditional registration is unrealistic. Cryptocurrency companies often face the dilemma of either trying to build products to avoid triggering securities laws, which brings considerable legal uncertainty and costs,It completely restricts the United States to evade regulatory issues. Registering as a securities will bring a disproportionately high compliance burden, as the existing framework requires that each token transaction be considered a securities sale. This requirement is not only unfeasible for lean crypto startups operating decentralized networks, but also does not conform to the nature of the blockchain ecosystem, where tokens often have different roles than traditional securities. The current regulatory framework does not take into account the highly diverse functions and distribution of tokens in the blockchain ecosystem and is often used as a tool within the network rather than an investment tool. Therefore, a clear and updated regulatory approach is crucial - distinguishing between financing transactions (the securities law may apply), secondary market token trading, airdrops, mining, etc. - all of which should be treated differently.

As we explore the complex situation of cryptocurrency regulation, it is obvious that differentiating different types of crypto activities is crucial. This distinction is particularly important when considering airdrops, as airdrops have unique characteristics that differ from traditional securities offerings.

Airdrops are more similar to these paradigms

Cryptocurrency airdrops are more similar to (i) loyalty programs or (ii) membership rather than traditional securities or stock allocations. Loyalty programs are designed to inspire customers to retain and reward customers for repeat purchases or continuous participation in brand activities. Such programs include airline frequent flyer programs or credit card rewards. Member programs, on the other hand, often offer exclusive benefits, such as attending private events, discounts, or advanced features, with the focus on creating a sense of belonging and exclusiveness for participants. Despite these functional differences, the SEC often evaluates airdrops based on the “free” stock case framework, [51] regards it as free stock allocation and is regulated by securities. This regulatory approach fails to take into account the unique nature of airdrops, which are more suitable for analogies to promote participation and community-building mechanisms rather than equity allocations.

i. Loyalty Program

Frequently Flying Mileage and Credit Card Points, such as cryptocurrency airdrops, are stored value programs that inspire user loyalty and engagement. Miles and points are redeemed for flights, upgrades or catering, encouraging users to be loyal to a particular brand, just as airdrops use tokens as a means of rewarding loyalty or encouraging participation in the platform. Both approaches prioritize engagement and ecosystem growth, but neither is the fundamental purpose of providing a return on investment.

Companies often offer loyalty programs, such as airline mileage or credit card points, without triggering the *Howey* test. It is worth noting that the SEC has not yet taken enforcement action on credit card points or airline miles, further emphasizing that their nature is consumer incentives, not investment vehicles. If applicable to airlines, credit card points fall within the jurisdiction of the Consumer Financial Protection Bureau (“CFPB”) and the Department of Transportation (“DOT”). [52] Therefore, there is strong argument that airdrops should not be treated differently from these well-established loyalty programs, which companies often adopt to build loyalty and drive engagement.

AlthoughTokens are different from points and mileage because they have a secondary market and can be used for governance, but it is important to consider that the existence of the secondary market itself does not necessarily classify tokens as investments. Like gift cards, the transferability of tokens is mainly used to improve consumer utility and flexibility rather than to indicate investment intentions. In addition, allowing token holders to participate in governance is similar to joining a client advisory committee or club with voting rights, which does not convert these tokens into securities, but promotes greater user engagement and community input. The core purpose of token airdrops is very similar to traditional loyalty programs, which is to inspire usage and loyalty to the platform. Regulatory precedents surrounding similar functions support this explanation, highlighting the need to view airdrops as an extension of consumer loyalty strategies.

Credit cards such as Chase Sapphire Preferred are typical of this model, which provides points that can be redeemed within a flexible reward incentive structure to promote reuse. [53] In this model, the accumulated points can be used in various services and products within the Chase ecosystem, or can be transferred to numerous partners. [54] This flexibility allows cardholders to choose from a variety of redemption options, including different airlines and hotel chains, thereby maximizing the utility and potential value of points to meet a wider range of preferences and needs. Similarly, Aave’s Merit program reflects a loyalty program that rewards user token allocations based on user’s meaningful contribution to the protocol, such as governance participation or liquidity provisions. [55] The functions of these tokens are similar to points, creating an open-loop incentive structure that encourages continuous participation and strengthens user commitment to the platform, but also allows users to transfer points to take advantage of better transactions. Although regulatory frameworks often confuse airdrops with securities, their true similarities are closer to loyalty programs, as they both allocate value primarily to enhance engagement rather than provide financial returns.

This analogy is even stronger for tokens with stable value such as stablecoins. Just as loyalty programs reward recommended friends’ user points, airdrops also incentivize user acquisition and ecosystem participation. These mechanisms are not speculation, but lay the foundation for long-term participation.

Ultimately, loyalty programs and cryptocurrency airdrops share a common core principle: leveraging value allocation to deepen user engagement, promote community development and enhance ecosystem sustainability. Both show how incentives are combined with utility to drive meaningful participation without relying on speculative investment dynamics.

ii. Membership

Whether in traditional industries or in digital ecosystems, membership programs are designed to develop loyalty and engagement by providing exclusive, practical benefits. For example, NFL fan membership grants privileges such as priority ticketing rights, team merchandise discounts, VIP event invitations and behind-the-scenes content, creating a sense of community and deepening connections with the team ecosystem. [56]The value of these rewards stems from their direct connection to the platform, not from external resale opportunities. It is worth noting that the SEC has confirmed that such membership programs (such as the Los Angeles Rams Fan Club) do not fall under the jurisdiction of the Securities Act and the Exchange Act. [57] In a letter that does not take action, the SEC clarified that these memberships were purchased for entertainment and consumption, rather than as investments for expected profits, further distinguishing them from securities. [58]

Similarly, airdrop services in the cryptocurrency sector have similar purposes. For example, Stargate Finance airdrops reward active participants with free tokens that can be used within the ecosystem. [59] This strategy not only inspires engagement and loyalty, but also supports the development of new projects within the platform. Both examples emphasize the intrinsic value of rewards designed to enhance participation and commitment within a specific ecosystem, prioritizing utility and community engagement over external financial returns.

Why airdrops do not meet the securities trading qualifications specified by *Howey*Airdrops should not be classified as securities trading. The SEC's position is that airdrop tokens constitute an investment contract and therefore belongs to unregistered securities. This position is reflected in many enforcement actions and informal guidance detailed later in this report. [60] However, unlike traditional securities offerings designed to raise funds, airdrops are often designed to facilitate network participation by distributing tokens for free. [61] Therefore, applying the securities law to airdrops is a mischaracter of its purpose, posing unnecessary regulatory burden to many blockchain projects.

According to the *Howey* test, airdrops failed to meet key criteria:

Failed to invest: The core element of the *Howey* test is "investment of funds" that aims to generate income or profits, thereby establishing a direct link between investment funds and expected returns. [62] However, in the case of airdrops, the distribution of tokens does not require the recipient to provide any financial consideration. Minimum operations such as registering an account do not constitute financial investment, which makes airdrops more closely related to promotions than securities trading.

Lack of common cause: To make an arrangement meet the conditions of a securities, it must involve a “common cause”, which requires a common financial relationship between participants and aggregation of financial resources between participants. This can be manifested as horizontal commonality—investors concentrate resources into a single enterprise, linking their destinies together [63]; it can also be manifested as vertical commonality—investor's financial success is directly related to the efforts or success of the promoter or issuer. [64] However, airdrops are independently distributed tokens, and there is no shared financial interest or risk of interdependence among the recipients, thus lacking common career elements. Regarding horizontal commonality, airdrops distribute tokens directly to individual recipients without the need for the recipient to invest any money, energy or resources. There is no asset concentration or shared risk, because the fate of each recipient is completely independent ofOther recipients. For vertical commonality, the receiver does not need to invest because they do not pay any money, so it is impossible to have any dependence on the initiator because there is no investment in the first place.

No profit expectations: Securities usually means expected to make profits from the efforts of the promoters or third parties. In contrast, airdrop tokens are often used for consumer purposes within the platform, rather than investment purposes. Tokens may grant users access to platform-specific features in order to participate, such as voting on governance proposals or paying for services. While some recipients may choose to sell them, any potential profit comes from market forces rather than the issuer’s active promotion, eliminating this criterion for *Howey* testing.

Not relying on issuer's efforts: Recipients of airdrop tokens do not rely on issuer's actions to increase the value of tokens. Unlike securities that usually rely on continuous management to maintain or increase value, airdrop tokens fluctuate based on external market factors, which further distinguishes them from securities. Furthermore, any effort comes entirely from the individual receiving the airdrop tokens, not from the platform or the project itself.

Distinguishing past precedents from modern airdrops The “free” stock case of the 1990s/21st centuryIn the legal debate on whether airdrops are eligible for securities, it must be distinguished from the “free” stock case of the “internet bubble” in the late 1990s and early 21st century. At the time, the SEC targeted internet companies that distributed stocks to attract online traffic, deeming these giveaways illegal “sales” of securities because they were not registered or exempted. [65]The explicit purpose of these free distributions is to create profits for the promoters and to allow the issuer to gain financial benefits. These companies often engage in fraud, using the temptation of free stocks to lure investors to provide personal information or actively promote these businesses, which was ultimately curbed by strict SEC enforcement actions. [66] In addition, these securities are expected to be sold on the secondary market, indicating that these free securities are an investment.

SEC's analysis shows that these are not really free gifts, but transactions that trade stocks for value. [67] By referring new users or attracting public attention, these companies have gained considerable benefits from recipients who effectively act as marketing agents. [68] The SEC considers these transactions as “sales” of securities because there is a value exchange under the Securities and Exchange Commission regulations. bill. [69]

In determining whether there is a value exchange, there are several key differences between token airdrops and “free” stock cases:

No exchange conditions: In the “free” stock promotion, rewards are explicitly promised, and users recommend others in exchange for stocks, resulting in widespread spam. In contrast, cryptocurrency airdrops often lack such exchange conditions; many recipients receive rewards simply for active participation without prior knowledge that their participation will lead to token segments.hair. Without exchange conditions, it is impossible to exchange valuable things.

Laser consideration: In the “free” stock case, consideration given by participants includes personal data such as email addresses and social security numbers, which have intrinsic value because they can be used by issuers for targeted marketing and other monetization strategies. Under the securities laws, it is logical that these personal data can be considered “consideration” because it provides economic value to the issuer. In contrast, in airdrops, the only requirement for participants is to provide a public wallet address. The values of these addresses are different because:

Public information: Public wallet addresses are already accessible on the blockchain and can be easily obtained by anyone. Their public nature means they do not provide exclusive value to airdrop issuers.

No Personally Identifiable Information: Unlike email or social security numbers, public wallet addresses should not be classified as Personally Identifiable Information from the perspective of securities laws. They do not provide direct means to identify, contact or locate individuals, thus reducing their usefulness for purposes other than transaction verification on the blockchain.

In view of these characteristics, public wallet addresses do not constitute a priced consideration stipulated in the Securities Law.

The independent utility of tokens: Tokens are very different from stocks in terms of function and purpose. While the value of a stock is determined primarily by market performance and company management, tokens often have inherent utility beyond speculative purposes. For example, tokens can provide direct, tangible benefits such as platform access and participation. This utility is an integral part of token design and purpose, emphasizing that its main purpose is not to resell in the secondary market. Therefore, tokens should not be viewed from the same legal perspective as stocks, as their primary value and purpose are fundamentally different.

So, while both free stocks and airdrops can be promotional tools for entities to use to expand their user base or reward loyalty, the basic legal interpretation of these mechanisms varies greatly by investment in funds and profit expectations, which are often not directly applicable to cryptocurrency airdrops.

Morrison Extraterritorial Effect: Offshore transactions should not be governed by the SECThe 2010 U.S. Supreme Court ruling in *Morrison v. National Australia Bank* fundamentally redefines the scope of U.S. securities laws, limiting their application to transactions within the U.S. territory. [70]The ruling established what is commonly referred to as a “trading test”, limiting the extraterritorial effectiveness of U.S. securities [71] Specifically, the court ruled that Section 10(b) of the Exchange Act only applies to securities trading on exchanges and transactions of other securities. [72] This precedent is particularly relevant to the practice of distributing cryptocurrency airdrops, because airdrops are often global and not limited to U.S. jurisdiction.

Cryptocurrency airdrops often involve the distribution of digital tokens to a wide range of international recipients, and usually do not conduct any currency exchange. Unless the token is subsequently traded on US exchanges, otherwise these distributions do not necessarily involve the US market. Even so, the original act of airdropping tokens to non-US recipients (the recipient does not trade on U.S. territory) is beyond the scope defined by *Morrison*.

In view of these factors, the implementation of the U.S. Securities Act on offshore airdrops will not only exceed the geographical restrictions stipulated by *Morrison*, but will also mischaracterize the nature of these transactions under the framework of the Securities Act. Therefore, the argument that offshore airdrops should not be bound by U.S. securities laws is both legally supported by the *Morrison* judgment and also conforms to the basic principles of securities regulation.

The history of law enforcement and regulation and its impact on airdrop and cryptocurrency industriesThe history of law enforcement and regulation in the US cryptocurrency industry reveals a fragmented regulatory approach that has caused serious chaos and contradictions, especially in airdrop and token classification. The next section will dive into how changing regulatory enforcement and changing securities law interpretations create an uncertain and sometimes conflicting regulatory environment for airdrop cryptocurrency projects.

Before 2017: *Regulators begin scrutinizing and enforcing ICsInitially, regulators such as the SEC and CFTC took a non-intervention attitude as the cryptocurrency industry began to grow. It wasn’t until the popularity of ICOs and the growing popularity of cryptocurrencies that the SEC began to show its regulatory intentions.

SEC’s DAO Report

SEC’s DAO Report in 2017 marks the first major regulatory action taken by the SEC in the field of crypto. [73] By applying the *Howey* test to tokens distributed by decentralized autonomous organizations (“DAOs”), the SEC emphasizes that many of these tokens can be considered as securities. [74]The report is the SEC's "bottom line" in the "cryptocurrency field." ” Formal notification of the digital asset industry that participants are required to comply with U.S. securities laws whether the company is located in or outside the United States. [75] Instead of providing a clear regulatory framework, the SEC has adopted an enforcement-led approach that evaluates the structure of token sales and investors’ expectations. This approach increases regulatory uncertainty, especially for companies using airdrops, as they must be cautious about these changing and unclear standards.

2018-2020: The Beginning of Enforcement SupervisionTomahawk – “Free” Token Distribution Case

The real turning point in airdrops came from the SEC’s actions against Tomahawk Exploration LLC in August 2018.[76] In this case, the SEC argued that if tokens distributed through the bounty program meet *Howey* The securities qualifications are prescribed, and these tokens may violate the securities law test. [77] Tomahawk's "Tomahawkcoin" is given to the reception of promotional services, the SEC considers this a form of “sales” stipulated in Article 5 of the Securities Act, although no money changes hands and is a “free” distribution of tokens. [78] The SEC even classifies free token allocations as possible creating securities if they benefit the issuer in some way measurable (e.g., increased visibility, market interest, or network engagement) can be quantified into a form of value. [79] The case warns that the SEC is closely reviewing the U.S. bounty program and similar airdrop activities, and stressing that even free distributions may be considered a securities offering if linked to promotions designed to increase their value.

SEC's Investment Contract Framework

Subsequently, in April 2019, the SEC mentioned airdrops directly for the first time and issued a non-binding guidance document called the "Digital Assets' 'Investment Contract' Analytical Framework" ("Framework"). [80]The framework is designed to illustrate how digital assets are classified as securities based on *Howey* tests. However, it leaves a lot of gray areas—such as what is a “continuous management effort” (Article 4), and when tokens may be transformed from securities to non-securities through “full decentralization”, failing to address how tokens initially play a role as securities, but as they achieve greater decentralization or utility, it may become a non-securities problem. [81]

Specifically to airdrops, the framework suggests that even “free” token distributions can be considered securities offerings if they help promote the economic interests of the ecosystem, putting many promotions under regulatory review. [82] Although the framework does not provide specific guidance for airdrops, projects that promote digital asset networks through airdrops begin to evaluate whether the actions required by third parties to receive and claim assets can be considered a “money investment” under the Howey test. [83]

While the framework provides some useful guidance, it also introduces complex, fact-specific analysis to issuers and platforms, blurring the boundaries between securities and commodities in the digital asset space. [84] This ambiguity leads to an increase in law enforcement actions, and legal projects face stricter scrutiny when trying to comply with the SEC's evolving and vague standards. [85]

SEC’s Actions against Kik, Telegram, and Ripple

Although these subsequent cases do not directly involve airdrops, their significant impact on the wider cryptocurrency market indirectly affects airdrop strategies. From 2019 to 2020, the SEC significantly shifted regulatory priorities, taking enforcement actions against Kik, Telegram and Ripple to major platforms, deepening focus on markets that previously characterized regulatory ambiguity. In these cases, the SEC successfully blocked Telegram’s $1.7 billion ICO[86] and Kik’s $100 million ICO[87], the tokens involved constitute unregistered securities. The court stood on the SEC's side and confirmed that the issuance of these tokens is essentially an investment contract and is therefore subject to federal securities laws. In addition, both cases highlight the SEC's jurisdiction over foreign token sales that could lead to U.S. resale, expanding the international applicability of U.S. securities regulations. Kik and Telegram sent a clear message that token offerings related to ecosystem development may be classified as securities. The lawsuit against Ripple Labs alleges that its sale of XRP tokens constitutes an unregistered securities offering, further exacerbating these regulatory uncertainties, resulting in major exchanges removing XRP, thereby exacerbating market volatility. [88]

The aggressive action taken by SEC against Kik, Telegram and Ripple has profoundly impacted the cryptocurrency market and greatly reshapes the airdrop strategy. In these enforcement actions, the SEC is well prepared to classify the token offering as unregistered securities. As the SEC strengthens its scrutiny, projects that utilize airdrops must carefully consider the way and reasons for token distribution to avoid similar legal challenges. The regulatory ambiguity left by the SEC's actions and guidelines means that airdrops have traditionally been seen as a benign approach to increasing user engagement and network engagement, and now it is necessary to carefully evaluate whether any part of the airdrop process can be interpreted as a "money investment" according to the Howie Test. This includes evaluating whether the steps taken by participants to receive airdrops can be considered as potential returns, affected by the ongoing efforts of the token issuer.

The consequences of the SEC's highly-watched case have therefore expanded the scope of what may be considered a securities, making airdrops confusing. This regulatory environment forces airdrop strategies to develop in a more cautious and legally meticulous way, such as preventing U.S. users from participating in airdrops. Projects must navigate these muddy waters, adjust their airdrop strategies to minimize legal risks while working to achieve their promotion and network growth goals, which may be under the shadow of SEC enforcement.

2021-2022: Adaptation to ambiguity and direct attacks on airdropsBlock US users and use VPNs

By 2021, the regulatory environment for encryption is tighter as the CFTC and SEC increase legal action on unregistered offshore exchanges that provide crypto derivatives. Both institutions say that under U.S. law, it is illegal for U.S. users to trade on these platforms due to increased risks and lack of investor protection. [89] Under increasing regulatory pressure, major offshore exchanges such as FTX and Binance have announced measures to ban U.S. traders, including mandatory Know Your Customer ("KYC") inspections, IP address blocking and geolocation filters designed to prevent Americans from accessing their accounts. website. [90]

However, despite these restrictions, many American traders have bypassed these obstacles,Continue trading on platforms like FTX and Binance. [91] As there is no choice, U.S. traders began using virtual private networks (“VPNs”) to mask their location, in some cases providing misleading information during KYC verification. The minimum verification requirements of some platforms (such as simple email addresses and self-reported/regions) create exploitable vulnerabilities. However, regulators have noticed such workarounds.

This period also marked a change in the airdrop mode. Following Uniswap's massive token distribution on September 16, 2020 [92] (the last major airdrop not subject to geo-blocking), subsequent projects began to increasingly adopt geo-blocking strategies to exclude U.S. participants. Airdrops such as 1inch[93] on December 25, 2020, dYdX[94] on September 8, 2021, and ENS[95] on November 9, 2021, all reflect this compliance initiative. These examples illustrate how crypto projects develop their strategies to adapt to complex international regulations and remain compliant with U.S. securities laws, emphasizing legal security in a changing regulatory environment.

Gary Gensler swore in as Chairman of the U.S. Securities and Exchange Commission

Tenire relations between U.S. regulators and cryptocurrency companies escalated significantly after Gary Gensler swore in as Chairman of the U.S. Securities and Exchange Commission on April 19, 2021. [96] Gemsler was known for his positive views on cryptocurrencies during his tenure at MIT, [97] During his tenure as SEC, he changed his position. office. [98] He began to describe the crypto industry as the “Wild West,” advocating for increased regulation and often warns that many tokens may be classified as unregistered securities. [99] By 2022, Gensler’s approach has been further toughened, claiming that the “overwhelming majority” of nearly 10,000 tokens on the market are likely to be securities. [100] Disappointed by slow response to Congress legislation, Gensler actively implemented the “law enforcement regulation” strategy, issued Wells Notices, and filed lawsuits against major exchanges such as Binance and Coinbase, which caused shocks across the industry. [101]

Hydrogen – Airdrop

In *SEC v. Hydrogen Technology Corp.* (September 2022), the SEC argued that token allocations through airdrops, bounty programs and employee compensation could be considered an unregistered securities offering, thus expanding the scope of securities laws to include non-monetary distributions. [102] Specifically, the SEC argues that these methods create a “money investment” (*Howey* testArticle 1 below), because airdrop receivers usually have to take the initiative to collect tokens and sometimes pay gas fees, which means financial commitment. [103] This evolving explanation suggests that the traditional concept of “free” airdrops is outdated and that the SEC considers them free statements that require active user engagement and potential financial expenditures. The ambiguity in the drafting of the complaint has raised questions about whether the SEC really distinguishes between bounty programs and airdrops, which makes the industry even more uncertain about the standards to be followed.

In addition, the SEC believes that promotions or “promotions” surrounding token allocations indicate that these tokens are for the purpose of “profit expectations”, thus classifying them as securities. [104] This action underlines the SEC's position that marking token allocations as "airdrops" or "bounty" does not exempt them from securities regulation.

2023-present: Focusing on Big ParticipantsBy 2023, the SEC set a record of crypto-related law enforcement actions, with its focus extending from centralized exchanges to decentralized organizations and protocols. With action against Terraform Labs and Do Kwon in February 2023, the SEC made it clear that the institution is expanding its scope to stablecoins and other crypto products that are traditionally not considered securities. [105] This shift suggests the agency intends to dominate the industry as a major law enforcement mechanism and push it to hunt down some of the industry’s largest players, including Coinbase and Binance. [106]

SEC’s actions against Justin Sun, Tron and BitTorrent – Airborne Substitution

In March 2023, the SEC accused Justin Sun and his three wholly-owned companies, Tron Foundation Limited, BitTorrent Foundation Ltd. and Rainberry Inc. (formerly BitTorrent) of providing and selling crypto-asset securities Tronix (TRX) and BitTorrent (BTT) without registration. [107] The defendant conducted multiple airdrops, distributing BTT to TRX holders and participants in various online activities. These activities have promoted the development of the BitTorrent and TRX ecosystem, increased demand and transaction volume for TRX, and introduced BTT to a wide audience. At present, the case is still being tried in the Federal District Court of the Southern District of New York.

In April 2024, the SEC revised its complaint, claiming jurisdiction over Justin Sun and his related activities in the United States. [108] The amendment highlights Justin Sun’s extensive travel in the United States and his promotional activities for Tron, BitTorrent and Rainberry, including live broadcasts from his San Francisco office. These details highlight the SECWorking to regulate foreign digital assets operations involving U.S. residents or territories, even if there are few connections. The case stems from a foreign issuance, highlights the SEC's strict enforcement of foreign entities linked to the United States and warns airdrop programs to carefully evaluate compliance strategies, including blocking U.S. users.

Feed from the United States

As a result of the violent impact of law enforcement actions, litigation and overall uncertainty in the industry, news reports about crypto projects expressing concerns and wishing to move overseas began around March to August 2023. [109] Companies expressed frustration at their view that the United States was unclear and restrictive, which made it challenging to do business. While the company said it wanted a clearer regulatory environment, nothing helped as more enforcement actions poured in.

Ripple Labs’ decision and Terraform Labs’ decision—the contradiction between court rulings

As a long-disputed defense of the crypto community, on July 13, 2023, U.S. District Court Judge Analisa Torres, the Southern District of New York, achieved one of the most important legal victories in the crypto space. In ruling the motion to dismiss the *Ripple* case, Judge Torres distinguished between institutional sales and programmatic sales and found that the programmatic sales of retail investors did not qualify for securities issuance. [110] She inferred that it is impossible for buyers to reasonably expect XRP sales to be used to enhance the XRP ecosystem and drive up its prices, thus failing to meet *Howey*’s third and fourth conditional tests. [111] In addition, the judgment laid the foundation for the argument that distinguishes the sales of primary and secondary markets, which affects the securities liability faced by exchanges and platforms.

However, less than a month later, on July 31, 2023, in the same district court, Judge Jed S. Rakoff took a very different position from Judge Torres on the difference between institutional sales and programmatic sales, dismissing Terraform Labs’ motion for dismissal because he classified all transactions as securities offerings. [112] Although the facts of the two cases are surprisingly similar, the rulings are very different, highlighting the great uncertainty and lack of clarity in not only how to classify crypto transactions, but also the great uncertainty and lack of clarity in how to classify crypto transactions in the federal courts.

CFTC’s actions against Opyn, ZeroEx and Deridex – working to stop Americans under attack

In September 2023, the CFTC simultaneously filed and reached a settlement against DeFi platforms such as Opyn, ZeroEx and Deridex, which face allegations related to illegal derivatives trading.[113] CFTC’s enforcement actions against the DeFi platform highlight the agency’s intention to apply its established regulatory framework for derivatives and margin trading to the decentralized finance sector. These actions underline the CFTC’s position that simply blocking U.S. IP addresses is not enough to exclude U.S. users from the DeFi protocol. However, the agency has not yet clarified what measures are sufficient, which puts the DeFi platform in a situation of instability and uncertainty and has also heightened confusion among projects planned to airdrops on how to effectively comply with regulations.

Beba LLC and DeFi Education Fund v. SEC – an active airdrop project

In view of the lack of clear provisions on airdrops by the SEC and the implementation of enforcement actions against various platforms, companies are forced to take the initiative to actively respond to regulatory uncertainty in their own ways. Beba LLC (“Beba”), a small apparel company based in Waco, Texas, selling handmade suitcases and accessories through its online stores, has partnered with the DeFi Education Fund (“DEF”), a nonpartisan research and advocacy organization based in Washington, D.C., to file a pre-enforcement lawsuit against the SEC. The lawsuit seeks protections for Beba’s plan to airdrop its $BEBA tokens, aiming to clarify regulatory uncertainties surrounding the plan. [114]

Beba created $BEBA tokens and distributed them through free airdrops without any monetary consideration. However, the company delayed its second planned airdrop due to poor regulation of the SEC's enforcement approach and the lack of clear guidance on which tokens and actions fall under the SEC's jurisdiction. Plaintiffs are seeking declarative and injunctive relief, believing that the SEC's regulatory stance on digital assets exceeds its statutory authority and violates the Administrative Procedure Act (“APA”) because the agency has adopted a comprehensive encryption without participating in the official rulemaking process. [115] Specifically, it seeks to declare that the airdrop of the $BEBA token is not a securities transaction and that the $BEBA token itself is not an investment contract. This clarification will provide Beba with legal certainty so that they can continue to operate their business without facing the imminent threat of law enforcement actions.

Although the SEC claims that “no action has been taken against Beba, if there is really a day, Beba will have a chance to defend itself”, [116], this statement seems to be out of touch with reality. Small companies are forced to go bankrupt under the weight of the SEC's unexpectedly harsh law enforcement actions that often catch businesses like Beba off guard and cannot recover. Therefore, the lawsuit also aims to challenge the SEC’s overpowering behavior and confirm that its enforcement strategies and interpretation of digital asset regulations have exceeded its statutory authority. Therefore, by targeting the APA violation allegations, the lawsuit could potentially be for the SECThe role in airdrops and, more broadly, its position in the digital asset industry provides much-needed clarification. At present, the case is still being tried in the U.S. District Court for the Western District of Texas.

The compliance environment for U.S. cryptocurrencies has become so chaotic and confusing that it is nearly impossible for entrepreneurs to navigate effectively. In a letter dated September 17, 2024, a two-member panel led by Rep. Tom Emmer urged the agency to abandon its reliance on “law enforcement regulation” and highlighted concerns about the SEC’s position on airdrops, noting that the agency failed to clarify how airdrops, commonly used to distribute in decentralized networks, should be handled under the Securities Act, leaving projects and investors in a state of regulatory uncertainty. [117]

In order for the United States to maintain its global leadership in technology and innovation, it is urgent to turn to proactive, well-defined and balanced regulation. Only with such a clear understanding can we cultivate a thriving, compliant and innovative crypto ecosystem that benefits the U.S. market and consumers.

Projects are blocking AmericansIn addition to seeking to reduce ties with the United States, many crypto projects are actively blocking U.S. users from using various means to access their platforms to appease U.S. regulators. Since crypto products are often decentralized and license-free, full compliance with regulations designed for traditional centralized businesses is technically challenging and financially cumbersome. [118]

Due to this environment, crypto projects are forced to use various methods to limit US users.

Geo-blocking or geofencing: Geo-blocking involves creating virtual boundaries (fencing) around a specific geographic area so that users in these locations cannot access services or online content. [119] A website can use various methods to detect your location. It can use your Internet Protocol ("IP") address to detect your approximate location, check which/region handles your domain name system ("DNS") services, determines where your payment data is located, and even determines the language you use to shop online. [120]

IP Address Blockade or IP Blockade: IP Blockade is a geo-blocking technology that restricts access to online platforms based on the user's specific IP address. Each internet device has its own unique IP address, so the network can record such addresses. When a person whose IP address is blocked accesses the platform in the future, the platform's security system (firewall) can block access. [121]

VPN Blocking: VPN allows you to encrypt your internet connection so that your traffic and IP address remain unknown. [122]It is used to maintain your privacy and security. VPN servers typically assign the same IP address to multiple users for increased privacy, but this shared use may cause websites and services to monitor high traffic or diversified activity for a single IP. Therefore, the website may block the address to restrict access. [123] As a precaution, VPN blocking is often used with geo-blocking.

KYC Process: The platform may also have KYC inspection and compliance programs, which help detect illegal financing and money laundering. Additionally, some projects require users to confirm their non-U.S. identity by signing messages using their wallets. Such processes can also be used to verify and prevent Americans from entering the platform by checking the identity of users. [124]

Agencies have not yet clarified what actions are enough to stop U.S. usersWhile many projects are trying to really try to stop U.S. users, regulators such as the Securities and Exchange Commission and the Commodity Futures Trading Commission have not yet provided clear guidance on what measures are enough to stop U.S. users. The ambiguity in compliance has made it impossible for projects to determine what they should do. This creates a cycle of self-censorship, where project choices limit their scope to avoid the risk of legal consequences, resulting in a decline in the presence of U.S. companies in the global crypto market.

For example, the CFTC has taken enforcement action against DeFi platform Opyn, accusing it of providing illegal leverage and margin digital assets through its platform to retail goods. [125] However, despite Opyn's efforts to geo-block US users, the CFTC believes that the measure is insufficient and does not specify what is sufficient compliance. [126] CFTC Commissioner Summer K. Mersinger specifically criticized the agency for saying in a statement of objection to the enforcement action:

“However, due to the lack of a transparent notification and comment process to create rules, the Commission has created an impossible environment for those who want to comply with the law, forcing them to either close the U.S. market or keep U.S. participants out.”[127]

Operational Challenges and Compliance CostsWhile the regulatory environment forces crypto projects to implement various restrictions to avoid U.S. enforcement actions, [128] These requirements not only present significant operational challenges, but also increase the company’s costs and legal risks. Many teams have to choose between developing custom geoblocking solutions in-house and relying on third-party providers such as Vercel. [129] While third-party services are more efficient and often more cost-effective, they increase reliance on data accuracy and reliability of external providers, which can lead to compliance risks and system vulnerabilities.

For example, one of the projects we interviewed was rumored to have encountered serious compliance panic as third-party geo-blocking data incorrectly indicated access from restricted areas, raising concerns about the effectiveness and accuracy of third-party solutions. Although this issue was later identified as a mistake, it highlights the operational risks and uncertainties inherent in relying on external data providers to achieve compliance. The responsibility for any violation is ultimately still held by the project party, not the third-party provider, [130] This means that law enforcement actions may still target access violations for crypto companies, even if third-party services cause the problem.

This strict compliance requirement not only increases operational complexity and costs, but also brings huge legal risks, as the project bears strict liability for any sanctions or unregistered securities laws violations. In this case, strict liability means that the company may face serious financial and reputational consequences even if it is unintentional to violate compliance regulations. This increased compliance burden and risk hinders innovation and complicates efforts to securely expand the crypto ecosystem within the U.S., further illustrates the adverse impact of law enforcement regulation on the industry as a whole.

In addition to excluding U.S. users, it is recommended that projects do not encourage the use of VPNs, as this may be interpreted as an attempt to circumvent U.S. regulations. Projects that explicitly direct U.S. users to use VPNs may be subject to SEC scrutiny, as seen in cases where organizations face penalties for being considered evading regulatory controls. By clearly declaring that airdrops do not apply to Americans and sincerely working to actually limit Americans, the project parties reinforce their argument that the distribution does not fall within the jurisdiction of the United States.

Law enforcement supervision violates the Administrative Procedure Law.The use of law enforcement supervision by institutions, especially the supervision of airdrops, conflicts with the principles of the Administrative Procedure Law. The Administrative Procedure Law requires the formulation of a structured and transparent rule-making process. [131] The SEC relies on litigation rather than creating formal rules to enforce securities laws in an unpredictable and often retroactive manner. [132] This creates an instability in the regulatory environment, as the SEC has shown in the high-profile case of Ripple Labs, which the SEC alleges that Ripple’s XRP token, a practical token used for international payments, constitutes securities, despite the lack of financial ties between XRP holders and many are unaware of the company’s connection to the underlying token. [133]

Under the APA, federal agencies must follow clear procedures when formulating new regulations, including public notification of proposed rules and setting public comment periods. [134] These procedures require the purpose of ensuring democratic accountability, allowing public and industry experts to provide input and thorough review before finalizing the rules, thus ensuring clear, predictable and fairness. [135] For example, in the Ripple case, there was great uncertainty due to the lack of previous, public rules for the SEC's crypto securities. [136] Ripple has been operating for nearly a decade and it has been believed that XRP does not meet securities standards because it is structurally similar to Bitcoin and Ether, while the SEC has previously stated that neither is securities because they have a decentralized structure. [137] The SEC’s enforcement action without establishing clear, pre-existing guidelines has led to an unpredictable regulatory environment for Ripple and many other token projects. [138]

In addition, law enforcement-based supervision passes orphansProcedural fairness is compromised by establishing cases rather than consistent public rulemaking processes to set unpredictable standards. This arbitrary approach damages the credibility of the institutions and weakens the trust of the industry. Without clear forward-looking rules, small companies and developers may face greater compliance burdens, which seriously affects their operating capabilities. Selective prosecutions not only lack transparency, but also seem arbitrary, especially if Bitcoin and Ethereum are allowed to operate without such regulatory scrutiny. [139] This approach allows institutions to “select winners and losers”, putting smaller and newer projects that enter the market without clear rules at a disadvantage, while benefiting pioneers from regulatory certainty. [140]

III. Economic ImpactAs the continuous development of the cryptocurrency landscape, understanding the scale of US participation and the restrictive financial impacts is crucial for future regulatory decisions. Our goal is to quantify the impact of geo-blocking on cryptocurrency airdrops for U.S. residents and to assess the broader economic consequences of these. Our analysis estimates the number of cryptocurrency holders in the U.S., assesses their participation in airdrops, and describes the economic and tax losses that may result from geographical blockades.

To promote economic impact, we have compiled samples of 11 geo-blocking airdrop projects and 1 non-geo-blocking airdrop project for our control. We carefully selected these airdrops because they are important in the crypto ecosystem and they are all on the Ethereum blockchain, ensuring a significant, streamlined and efficient data collection process. These also happen to be one of the most successful projects in the crypto space. We first estimate the number of Americans affected by the crypto-geographic blockade. We then calculated the number of active wallet addresses controlled by Americans. Next, we determined the number of recipients for the sample, the total revenue, and the median number of each recipient for that airdrop. Using these data, we estimate the potential total tax revenue lost by U.S. residents and the United States due to geographic blockade airdrops in our sample and another CoinGecko sample.

U.S. participation rate

It is estimated that there are 18.4 million to 52.3 million cryptocurrency holders in the United States**, and in 2024, there are generally 920,000 to 5.2 million monthly active US users affected by geographic blockades**, including airdrops and reduced participation in project use.

Table 1: Estimated percentage of active U.S. addresses in 2024

From our sample group, **U.S. residents** estimated losses from $1.84 billion to $2.64 billion in potential revenues from $2020 to 2024** between $1.84 billion and $2.64 billion.

According to a report by CoinGecko, the report analyzed 50 empty timesInvesting (although not a complete list), approximately $26.6 billion worldwide is distributed to claimants through geo-blocking and non-geo-blocking airdrops (items they review - see [Table 4 in the Appendix]. [146] Using CoinGecko to estimate the total value allocated to claimants through its sample and our calculations of Americans affected by geo-blocking, ** From a sample of CoinGecko’s 21-item project, the total income that Americans may lose may range between $3.49 billion and $5.02 billion. **

Tax losses due to airdrop restrictions are estimated at $1.9 billion (lower limit of our sample estimate) to $5.02 billion (CoinGecko’s The estimated upper limit), the corresponding **Federal tax loss (calculated using individual tax rates)** is expected to be between $418 million and $1.1 billion**, and the additional **State tax loss** is approximately $107 million to $284 million million**. [147]**Total**, which means **Tax revenue loss is estimated at $525 million to $1.38 billion**. Offshore migration results in corporate tax lossesRegulatory uncertainty has shifted a large portion of the cryptocurrency industry overseas, resulting in a significant decline in U.S. cryptocurrency developers and business operations. An obvious example is Tether, the issuer of the USDT stablecoin registered in the British Virgin Islands. In 2024, Tether reported a profit of 62 $148, even surpassing traditional financial giants like BlackRock. If Tether is headquartered in the U.S. and pays full U.S. tax, the profit would be paid 21% federal corporate tax, with an estimated federal tax revenue of $1.3 billion. In addition, considering the average state business tax rate of 5.1%, it is estimated to incur a state tax of $316 million.

Together, Tether's offshore status alone could cause a tax loss of $1.6 billion per year. In addition to corporate taxes, the absence of these high-income companies in the U.S. will also result in losses in employee income tax, payroll tax, and local business tax related to business operations, further exacerbating the economic impact. Given that Tether is only a major player in the crypto ecosystem, the cumulative impact of multiple high-income companies operating overseas could become the U.S.

We can see that the ongoing implementation of regulations that restrict airdrop acquisition and promote offshore cryptocurrency innovation has led to a significant shrinkage of the U.S. tax base. Establishing a clear and structured regulatory framework will mitigate these losses by incentivizing blockchain companies to operate, thereby promoting U.S. economic growth and tax revenue generation.

Law enforcement adversely affects the overall regulation of airdrops and cryptocurrencies"Enforcement" has a positive impact on the cryptocurrency industry and other fieldsThis has brought many unexpected harmful consequences, including fragmented and inconsistent regulatory standards, negative externalities, market distortions, tax losses, missed economic opportunities, and weakened overall economic impact on the U.S. economy. This approach leads to inefficiency in the regulatory sector and hinders the economic potential and growth that the booming digital asset industry could have brought to the entire economy.

Lost economic opportunities and censorshipForcing crypto projects to exclude U.S. users is actually censorship because it deprives Americans of access to financial innovation and new technologies that can enhance financial inclusion, autonomy, and personal wealth. This restriction limits the choice of U.S. residents, putting them at a disadvantage compared to users in crypto-friendly jurisdictions. This also hinders the U.S. from benefiting from the economic opportunities, jobs and technological advances that these projects may bring. Between 2018 and the end of 2023, the U.S. developer share lost 14%. [149] In addition, non-US digital asset companies are much more likely to issue tokens than their U.S. counterparts, making them more likely to compensate employees with digital assets rather than traditional fiat currencies—a tempting benefit that attracts talent outside the U.S. company. [150] Thus, by isolating U.S. users from the global crypto ecosystem, regulators are actively stifling innovation and driving talented developers and companies to operate abroad, weakening the U.S.'s competitive position in the digital economy.