22 mins ago

3,810

Author: Michael Nadeau, The DeFi Report; Compilation: Baishui, Golden Finance

Many of you want to see more data/analysis about the current cycle status.

So that's what we're focusing on this week.

Is there still a bull market for cryptocurrencies in 2025? Despite many positive developments, why am I so bearish? How can we find vulnerabilities in my analysis?

Our goal is to answer these questions and more.

Bear Market CaseBefore we discuss on-chain data, I want to share more qualitative analysis of how we view cryptocurrency cycles.

Early bull marketThis is probably from January 23 to October 23.

This is the period after the market bottomed out after FTX. Things got very calm (low transaction volume, crypto Twitter silence). Then we started to rise again.

BTC rose from about $165,000 to $33,000 during this period.

However, no one calls this a bull market. During the "early bull market", most markets are still on the wait-and-see state.

Wealth CreationThis is probably from November 2023 to March 2024.

At this time we saw some big moves and some major wealth creations. SOL rose from $20 to $200. Jito's airdrop (December 23) created an additional wealth effect in Solana and repriced Solana DeFi (Pyth, Marinade, Raydium, Orca, etc.). The venture capital market reached its peak of fanaticism during this period (which is typical).

BTC rose from $33,000 to $72,000. ETH rose from $1,500 to $3,600.

Bonk's market value has risen from $90 million to $2.4 billion (26 times). WIF's market value has risen from $60 million to $4.5 billion (75 times). The seeds of a larger "Meme Coin Season" have been planted.

But it was still quite "quiet" during this period. Your "regular friend" may not have asked you questions about cryptocurrencies.

Wealth DistributionThis is probably from March 24 to January 25.

The "focus on the peak" period. We tend to see “WAGMI” type emotions, quick rotations, new metadata (which disappears quickly) and blind adventures pay off. Celebrities and other "cryptocurrency transients" often enter during this period. Crazy headlines like "Tesla Buy BTC" or "Bitcoin Strategic Reserve"News often occurs in the wealth distribution stage.

Why?

New investors are entering the market driven by these headlines. They didn't know they were late.

This is the second wave of the "Meme Coin Season" and then evolved into the "Artificial Intelligence Agent Season". During this period, the market ignored many obviously problematic behaviors. No one wants to speak out. People are making money.

Now. This brings us to where we are today.

Wealth destructionWe believe that we entered this period shortly after Trump took office.

This is the period following the peak of the outbreak. The bullish catalyst is now a thing of the past. The seemingly positive news encountered bearish price action.

In the current state, administrative actions on "strategic Bitcoin reserves" have not promoted market development - this is an important signal. During this period, reversals tend to encounter critical resistance periods and gradually fade away (we saw this after Trump tweeted about cryptocurrency reserves last week).

Some other signals we look for in the phase of wealth destruction:

Cleans and "panic" disrupt the market, but still have not completely awakened the market. We see this in the DeepSeek AI panic and tariff uncertainty.

Investors have "hope". We see a lot of discussions today about the decline in the US dollar and the rise in global M2 (more on this later in this report).

The "scammer" type enters the market. More and more people send us private messages asking for “look at their projects.” More advertising capital is circulating everywhere. Projects with sufficient funds were paid at will. More PvP/competition/infight. The industry generally exudes a worse atmosphere. During the "wealth destruction", the bad guys began to be named.

Download investors also began to surface during this period—usually after liquidation. The previous cycle began with Terra Luna. This led to the bankruptcy of Three Arrows Capital. This led to the bankruptcy of BlockFi, Celsius, FTX, etc. This ultimately led to the demise of Genesis and the sale of CoinDesk.

We haven't seen any explosions yet. We will notice that this cycle should be less – simply because there are fewer CeFi companies. Time will tell. Fewer explosions could lead to higher lows when we officially bottomed out.

Where could these explosions come from?

No one knows, but I guess it's a look at the common culprits.

Exchange. Pay close attention to hidden leverage and/or potential fraud on some foreign "B and C" exchanges.

Stablecoin. We are focusing on Ethena/USDe – the current stablecoin in circulation is worth nearly $5.5 billion. It guaranteesHold its peg and earning from cash and arbitrage trading (holding spot assets, shorting futures) – this is the main source of leverage in the previous cycle (via Greyscale). Ethena's reliance on centralized exchanges adds additional counterparty risk. In addition, MakerDAO also invested part of its reserves in USDe, bringing additional cascading risks to DeFi.

Protocol. Beware of the increase in hacking and the potential liquidation cascading due to crypto collateral on platforms like Aave – the platform still has more than $11 billion in active loans (below the $15 billion peak).

Micro-Strategy. We think they do a good job of managing their debt with caution, as most of them are long-term unsecured or convertible debt (there is no margin requirement for BTC holdings). Additionally, they were able to withstand a 75% decline in BTC in the last cycle. That being said, a sharp drop in BTC prices could put pressure on Saylor, forcing him to sell a lot of BTC at the worst.

The best time to re-enter the market is the end of the wealth destruction phase. We believe this hasn't come yet. Of course, we will notify you when we think we are back in the “buy zone”.

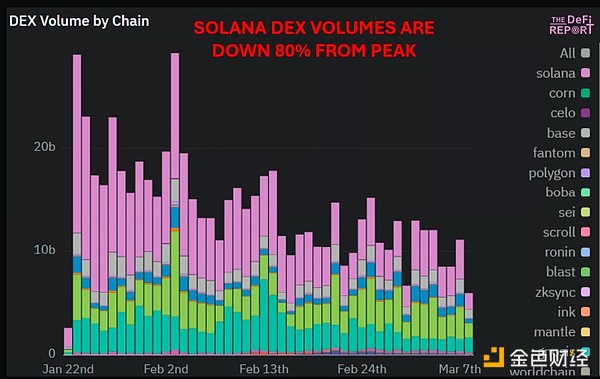

Bad Data DEX trading volumeSolana DEX trading volume fell by 80% compared to the peak after Trump launched memecoin. Meanwhile, the number of independent traders has dropped by more than 50%.

Token IssuanceToken Issuance on Solana has dropped by 72% from its peak. Nevertheless, the chain creates over 20,000 tokens every day.

Bitcoin Long-term Holder MVRV RatioLong-term Holder MVRV (Bitcoin’s “Smart Money”) peaked at 4.4 in December last year. That’s 35% of the 21-year cycle peak of 12.5 and 35% of the 2017 cycle peak.

Bitcoin rose about 80 times from its trough to its peak in the 2017 cycle. It rose about 20 times in the 2021 cycle. It has risen about 6.6 times in the current cycle.

The actual price of Bitcoin (representative of the average cost basis for all circulating Bitcoins) peaked at $5,403 in the 2017 cycle, 15.1 times higher than the peak of the 2013 cycle. It hit $24,530 in the 2021 cycle. This is 4.5 times higher than the peak of the 2017 cycle. Today, the actual price is $43,240, 1.7 times the peak of the 2021 cycle.

Key Points:With each of the data points above, we can observe the symmetry of the periodic decline of the peak. We believe that this dataIt clearly tells us that the law of diminishing returns is quite real.

Bitcoin is now a $1.7 trillion asset. No matter how optimistic the headlines are, investors should not expect to see a parabola as sustainable as we have seen in the past. Mobile assets require too much capital at this time.

When BTC loses momentum, the rest of the market loses everything.

Solana is weakening. We've been paying attention to this because we're worried that Solana's "come story" is built on what seems to be a "house of cards" - considering that 61% of DEX trading volumes so far this year involve memecoins. Additionally, less than 1% of Solana users accounted for more than 95% of gas fees in the past 30 days. This is worrying, as it highlights that a small number of Solana users (“Big Fish”) are plundering everyone else (“Little Fish” that trades memecoin). So if the “little fish” get tired of losing money and take a break (we think they will), we might see Solana’s fundamentals slip rapidly.

Data: DeFi report, Dune (base fee + priority fee + Jito tip for Solana)

BTC long-term holders have made profits twice in the past year. Their actual price (representative of the cost base) is about $25,000. Meanwhile, short-term holders who buy at the highest price are currently in a loss state (the average cost base is $92,000). We believe that this group may continue to sell at lower prices as BTC prices reach its peak of $109,000.

When you put everything out, we think it is undeniable that the “typical” cycle is over. Denying this is denying reality.

Of course, there is no "law" at work here.

We believe that the best way to process this information is to accept reality + assign a probability that the cycle has reached its peak. We think this probability is obviously higher than 50%.

After the basic work is completed, we try to identify the vulnerabilities in the paper and stress-test our views.

Let's do this.

Bull Market CaseI still see that the bear market is subject to considerable resistance. A bull market will not quietly put down your weapons.

This begs the question: Does the bull market provide more evidence that we have entered the "wealth destruction, i.e., negative" phase? Or, before moving higher again, are we likely to become too pessimistic at local lows?

In this section, we will introduce some of the main "bull market perspectives" I have seen.

Global M2/LiquidityThe green box to the right shows that BTC is declining as global M2 starts to rise. Some point this out and cite the correlation with BTC, and the response of BTC is usually lagging (2 to 3 months).

With that being said, the green box on the left shows the same dynamic at the end of the previous cycle: M2 rises as BTC falls. In fact, M2 didn’t peak until early April 2022 — 5 months later than BTC peaking.

The global M2 has risen by 1.87% since mid-January as central banks basically shift from tightening to easing.

This is beneficial to liquidity conditions.

However, we should also ask the following questions:

What drives the growth of M2? We think this is mainly due to the depreciation of the dollar (which has dropped 4% since February 28!) – when denominated in US dollars, this means more foreign currencies. This is a push for the global M2. In addition, the reverse repurchase mechanism has been recently exhausted and is relaxing to boost the economy.

Will this continue? We believe that the dollar will continue to decline as investors move their funds overseas, but will not fall like they did in the past few weeks. We believe that the US dollar will continue to depreciate. However, we do not think the Fed will take easing in the near term, as they say reserves are still "adequate". We believe they are still worried about inflation.

How does this compare to the liquidity situation we saw last year? We believe that the current liquidity situation should be seen as a headwind compared to last year. Remember, it's more about the rate of change than nominal growth. We strongly feel that the Fed and the Treasury Department "stimulated" the market last year to help Biden/Harris re-election. This is achieved through "shadow liquidity" - or in the words of Michael Howell of Cross Border Capital, "non-quantitative easing, quantitative easing" and "non-yield curve control, yield curve control". The following figure shows us the impact of Trump’s new cancellation of these on the rate of change.

The above “secret stimulus” is estimated to inject $5.7 trillion into the U.S. market in early 24 years. This is achieved by consuming reverse repurchase + preloading new bond issuances.

Finally, we think investors should pay close attention to what Minister Becente said in an interview with CNBC last week:

"The market and the economy are already addicted. We are already addicted to this kind of spending. There will be a detox period. There will be a detox period."

Business Cycle/ISMWe have previously pointed out that ISM data indicates the beginning of a new business cycle. We also recorded strong data on capital expenditure purchases and small business confidence. We think this is true, but slowing growth is also obviousAnd it's easy to see. The data we saw last month may be distorted by some manufacturers buying “advanced” ahead of expected tariffs. Since then, we have seen data on both services and new orders weaken. The manufacturing PMI reading for February was 50.3, down from 50.9 in January.

Strategic Bitcoin ReserveUntil last Friday, we still saw crypto natives promising negotiations on strategic cryptocurrency/bitcoin reserves – even though the market has been rid of the impact of this news several times in the past 6 weeks.

I think we all agree that this is an incident of "buying rumors and selling news".

Is there any flaw in the "period" thinking?We should also admit that this "cycle" is different from the past cycle.

For example:

BTC hit an all-time high for the first time before the halving.

This cycle is much shorter, with only two years of bull market.

The “altcoin season” has performed very differently, as BTC’s dominance has been gradually rising since the beginning of 23 years.

With the support of the United States, Bitcoin is now fully integrated into the financial system.

If “period thinking” is flawed, then we may not have reached its peak. Instead, maybe we are entering the pause/adjustment/consolidation phase before the next round of ups, rather than a year-long bear market, where prices may fall 75-80% (as we have seen in the past)?

Our view is, yes, cycles are evolving. Having said that, we still expect the bear market may take 9-12 months to end.

SummarySumm our point of view:

We believe we are currently in the "complacent" phase of the cycle shown in the picture above.

All the bullish catalysts that people could identify a few years ago have already played a role.

The economy may be heading for recession. We think Trump's message is very clear. They are actually telling us that the economy needs to detox. We should believe their words. This is very similar to Powell's statement that "pain is coming" before the rate hike in early 22 years. Our current idea is that cryptocurrencies are canaries in coal mines. Traditional financial markets will slowly bleed/fall.

Given the extreme pessimism of this sentiment, we can see the market rebound to the BTC’s low of $90,000 in the near term. However, we think this will be sold out in a big way – which could kill any hope of returning to the bull structure.

As always, we are open to mistakes. Our analysis is based on the information we have today. As new information emerges, we will update our views.

What do we need to be bullish again?

We will focus on the following factors:

Reversal of fiscal austerity/DOGE efforts.

The Fed/Quantitative Easing Sharp.

The Federal Reserve (not just) drives a massive influx of global liquidity.

The S&P 500/Nasdaq index saw a sharp pullback/surrender.

What we worry about is that the arguments of bear markets are beginning to become consensus. This made us hesitate a little. But we still need to consider other factors at the moment - because the top of the cycle is coming and the bear market is coming.

Of course, in the long run, there are many things to look forward to.

Cryptocurrencies have indeed entered a "turning point" period. Now it’s time to rebuild the financial system on public blockchains.

Not to mention, we like bear markets. As the tide recedes, it is easier for us to distinguish the noise from the signal from the past cycle – which will prepare us for the next bull market.