9 mins ago

8,079

Author: Bing Ventures Source: medium Translation: Shan Oppa, Golden Finance

Interruption of the value discovery cycle. Traditionally, it took weeks to discover the value of newly listed tokens on centralized exchanges (CEXs). However, the next generation of platforms is compressing this cycle to the extreme.

Platform life cycle reconstruction. The “Flash-Lock-Evolution” mode is replacing the traditional “Prosperity-Stay-Decay” mode. Data shows that successful projects no longer pursue continuous high growth, but achieve rapid value acquisition and lock-in, and quickly accumulate value before transitioning to the product evolution stage.

Value logic innovation. Traditional valuation methods based on transaction volume and fee income are outdated. Analysis shows that project value and user interaction depth (R²=0.87) are more correlated than traditional indicators such as transaction volume (R²=0.58).

Ecosystem construction and transformation. Traditional CEX adopts a centralized and hierarchical model. In contrast, the ecosystem under the new paradigm shows "lightning expansion". Hyperliquid data shows that the startup cycle of its ecosystem projects has been shortened to one-fifth of the traditional model, and the efficiency of value acquisition has been tripled.

Recently, new generations of decentralized derivative trading platforms such as Hyperliquid and Vertex Protocol have emerged and become strong competitors in the market. Hyperliquid, in particular, achieved explosive growth in TVL from $50 million to $300 million in less than four months, with an average monthly agreement revenue of $43.89 million. This phenomenon has triggered people's deep reflection on the development model of derivatives platforms: Why can Hyperliquid achieve rapid growth in the current market environment while early leaders such as GMX and dYdX gradually lose motivation?

Through in-depth analysis of the three generations of mainstream derivative platforms (dYdX, GMX, Hyperliquid), we found a significant trend: derivative platforms are undergoing a paradigm shift from "technology-driven" to "community sovereignty". This change is not only reflected in the token allocation model, but also deeply reflects the evolution of the crypto market's understanding of decentralization. After the FTX crash, the need for true decentralization and community governance is more urgent than ever.

Deconstructing the "hyperliquid phenomenon"

Hyperliquid is a high-performance Layer 1 blockchain whose core application is the on-chain order book perpetual exchange. Its goal is to build a fully on-chain open financial system.

Main features:

Layer1 public chain

Hyperliquid Layer 1 As a decentralized financial system, its key features include full on-chain margin storage and matching engine status, non-relying on-chain order book, consistent transaction sorting and low-latency operations (median delay of 0.2 seconds, 99% delay of 0.9 seconds) are achieved through the HyperBFT consensus algorithm, supporting up to 100,000 orders per second.

Super EVM

HyperEVM supports common EVM functionality, allowing ERC20 tokens to correspond directly to native spot assets. Users can trade through native spot order book and seamlessly use the same assets in EVM-based applications. Currently, HyperEVM In the test network stage, it has not yet been launched.

On-chain order book perpetual exchange

Hyperliquid currently supports transactions of more than 100 assets, new assetsThe listing of the product is decided by the community proposal. The token listing is conducted through a Dutch auction, with listing rights bidding every 31 hours. The maximum leverage provided varies from asset to asset, ranging from 3x to 50x.

HIP-1

HIP-1 is Hyperliquid's native token standard, aiming to be the Gas fee standard for public chains in the future. The token is still in beta, during which USDC is used as a Gas fee.

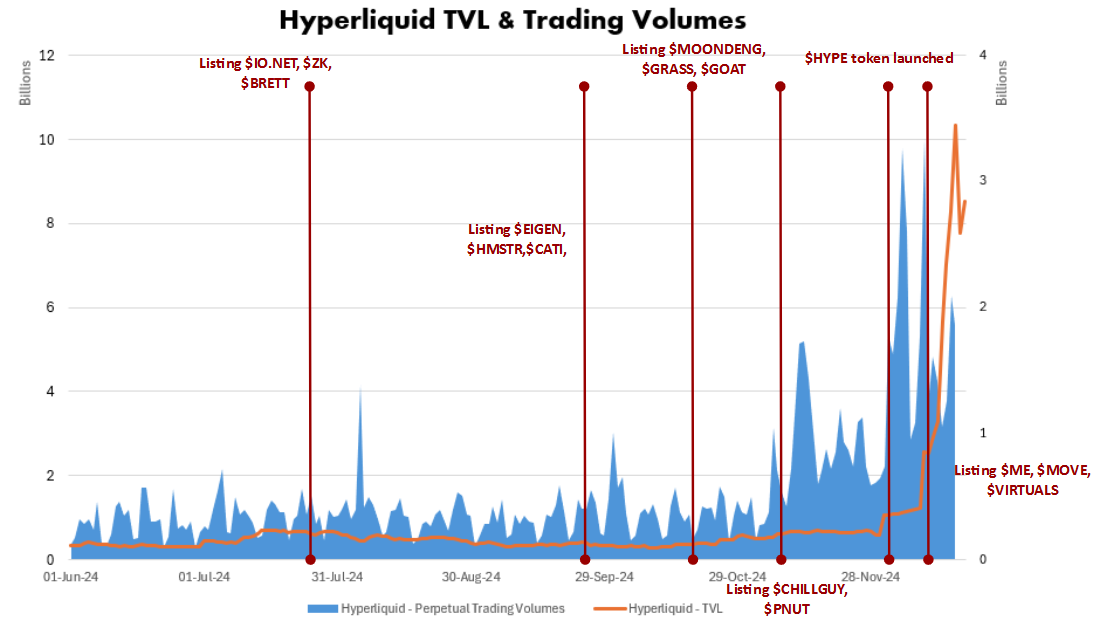

The Hyperliquid team has shown keen market insights and consistently provides sustainable trading for popular tokens. However, this is not the main driver of Hyperliquid TVL and volume growth. For example, TVL did not experience significant growth during the release of $EIGEN and $IO.NET. The only significant increase occurred when the ecosystem token $HYPE was listed for spot trading. It tripled from $190.96 million on November 29 in just three days. Trading volume peaked at nearly $10 billion on December 5. In a bullish environment, Hyperliquid listed tokens for Magic Eden, Movement and Virtual Protocols, pushing TVL to an all-time high of $3.4 billion, highlighting its huge potential in ecosystem expansion.

While the launch of popular tokens is not the main driver of volume and TVL growth, other competitors such as GMX and Jupiter generally do not offer trading opportunities for popular tokens. This distinction makes Hyperliquid a potential leader in the field, recognized as an on-chain platform with the most similar user experience to centralized exchanges, laying a key foundation for future growth.

Protocol revenue sources

The main revenue sources of this project include PingTaiwan fees and token listing and auction fees.

For listing auctions, items aimed at listing tokens on Hyperliquid must participate in the Dutch auction, and the proceeds from the auction will be directly included in Hyperliquid's revenue.

Platform revenue comes from transaction fees for spot and perpetual transactions, as well as liquidation fees during settlement periods.

For HIP-1 standard tokens not denominated in USDC in spot transactions, the proceeds will be considered token destruction because there is no specific mechanism to direct these funds to HLP.

All other fees paid by the project team will be transferred directly to HLP, creating profits for liquidity providers and vaults that adopt various trading strategies.

In addition, part of the profit is allocated to the aid fund to repurchase $HYPE tokens, reduce circulation supply and enhance value stability and ecological growth potential.

Publication auction feeSource: Hyperliquid

The maximum listing and auction fee can reach US$262,000, reflecting the important value of Dutch auctions in the token listing process. The main advantages of this model include:

Transparent fairness: All participants have equal bidding opportunities, effectively prevent price manipulation, and ensure fairness in the auction process.

Decentralization: Auctions are executed through smart contracts on the blockchain to reduce dependence on intermediaries and enable trustless decentralized transactions.

Anti-deception: The auction process prevents sellers from submitting false bids, thereby increasing the credibility of the auction.

Transaction feeSource: Hyperliquid

Spot and perpetual contracts adopt the same step-by-step transaction rate structure to ensure that users experience consistent rates across different transaction types. This simplifies the fee system and improves the user experience.

Liding fees

When the trader's account balance is lower than the maintenance margin, the system will clear all or part of the positions through the market list.

If the funds after forced leveling meet the maintenance margin, the remaining amount is returned to the trader.

If the account balance falls below 2/3 of the maintenance margin and the market order cannot be liquidated, stop loss liquidation will be triggered and the position will be transferred to the liquidator's vault.

The liquidation fee increases platform revenue, while the profit generated by the liquidation backing flows into the HLP, providing returns to the community.

Token destruction

Source: ASXNOn the day of $HYPE listing, 34K $HYPE tokens were destroyed, reflecting strong market demand.

More than 90K $HYPE has been destroyed, accounting for 0.03% of the circulating supply.

While the current destruction rate is not high, the mechanism will play a crucial role in controlling the supply of tokens in the future.

After the rightThe demand for HIP-1 standard tokens is growing, and the destruction rate is expected to increase, thus forming a positive feedback loop for stable token value.

Aid Fund

Source: HypurrscanThe address of the Hyperliquid Aid Fund is 0xfefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefefe

The fund holds more than $11 million in HYPE, accounting for 3.3% of the total circulating supply.

All holdings come from platform revenue and accumulate through repurchase.

As platform activity and revenue grow, the repo ratio is expected to increase, further enhancing the value of $HYPE and promoting sustainable development of the ecosystem.

High-level language processing

Source: HyperliquidAs of December 19, HLP has accumulated profits of US$50.6 million through market making strategies, trading fees and liquidation fees.

The monthly annualized rate of return reached 49%, reflecting HLP's strong profitability in liquidity provision and expense allocation.

Competitive landscape

There is currently no shortage of on-chain perpetual contract trading platforms in the market. This article aims to explore Hy through comparison with other projectsWhy can perliquid stand out and become the leader?

Trading mechanism

Order books usually show lower slippage in high liquidity markets because the transaction price is based on a specific order, rather than the liquidity curve of the AMM (automatic market maker). This makes them more suitable for bulk traders. In addition, the order book does not assume the risk of impermanent losses, providing a more stable environment for liquidity providers, thus attracting professional participants. The order book operates similar to a centralized exchange (CEX), which is more attractive to users familiar with CEX. This feature makes it particularly suitable for improving the user experience.

However, AMM also has unique advantages, such as instant transactions, no need to wait for counterparty orders, and more reliable operation on low-performance blockchains. AMM is simple and easy to deploy, especially suitable for early user acquisition and small transactions, creating a more friendly environment for retail users.

At this stage, as more and more traders seek to replicate the on-chain perpetual contract platform for CEX trading experience, protocols that adopt the order book model undoubtedly have a stronger competitive advantage. The trading model of the order book is more in line with CEX and can better meet the needs of professional traders than AMM. Therefore, protocols that adopt order books like Hyperliquid and dYdX stand out in the market.

Token listing and application chain

As mentioned earlier, the Hyperliquid team performed well in the listing of popular tokens and quickly achieved the transaction of popular assets. However, dYdX is equally good in this regard, and even has more tokens on the shelves than Hyperliquid.

Hyperliquid and dYdX both launched application chains, which should theoretically increase the value of their platform tokens. Native tokens not only obtain value from platform revenue, but can also act as gas fees, further enhancing their usefulness and overall value.

Nevertheless, dYdXIts application chain has not been fully utilized to cultivate its ecosystem, and Hyperliquid has successfully built a diverse project ecosystem on its chain. Examples include $PURR (leading MEME token) and $HFUN (native Telegram bot). These tokens not only enhance Hyperliquid's wealth creation capabilities, but also introduce more DeFi applications, expanding Hyperliquid's ecosystem beyond sustainable transactions, with greater diversity and appeal.

Transaction fees and vault refunds

Hyperliquid's transaction fees are the lowest in the market. Compared with dYdX, which adopts a similar trading mechanism, Hyperliquid's recipient and manufacturer costs are almost half the cost.

Hyperliquid costs $100 less than dYdX for every million dollar transaction volume.

Although the listed rates are based on entry-level trading hierarchy (Hyperliquid: < $5,000,000; dYdX: < $1,000,000), Hyperliquid maintains its price advantage even at high volumes.In terms of vault revenue, Hyperliquid not only benefits from regular transaction fees, but also earns revenue from token listing auctions.

As of December 20, Hyperliquid's annualized return on vaults (APR) ranked second in the market with 37.63%.

In comparison, dYdX's vault has about $66 million, almost seven times less than Hyperliquid's $466 million. This explains the higher APR for dYdX.

However, Hyperliquid offers attractive returns despite its high vault lock-in rate, reflecting the competitiveness of its vault revenue model.

Order Book Platform: Hyperliquid and dYdX

In order to enterTo explore the advantages of Hyperliquid in one step, the following will focus on comparing Hyperliquid with dYdX. Both platforms adopt the order book mechanism and have launched their own application chains, which are one of the two most representative platforms on the market at present.

Public chain performance

Hyperliquid's public chain has an advantage over dYdX Chain

Hyperliquid's maximum TPS reaches 100,000, and the final transaction certainty is about 0.2 seconds.

This high level of performance better adapts to the hardware requirements of future high-frequency trading (Hyperliquid is built on Arbitrum).

Hyperliquid adopts the HyperBFT consensus mechanism to significantly improve the efficiency and performance of perpetual transactions.

Initially, Hyperliquid was built using the Cosmos SDK and leveraged the Tendermint consensus mechanism.

While Tendermint is known for its reliability, consistent transaction sorting, and seamless integration with the Cosmos ecosystem, its throughput is limited to 20,000 transactions per second - well below the demand for high-frequency platforms.

This is particularly insufficient compared to Binance's 1.4 million TPS.

To solve the performance bottleneck of Tendermint, the Hyperliquid team developed HyperBFT. Inspired by advanced protocols such as Hotstuff, LibraBFT and MonadBFT, HyperBFT is rewritten in Rust and is based on the latest Byzantine Fault Tolerance (BFT) research to provide superior performance and scalability.

Source: ASXNConsensus Upgrade—The transition from Tendermint to HyperBFT has brought significant improvements.Medium order latency has been reduced by 3 times, while scalability has been greatly improved.

HyperBFT not only solves the limitations of Tendermint, but also gives Hyperliquid the ability to handle massive transactions, making it an ideal choice for high-performance on-chain transactions.

In contrast, the CometBFT used by dYdX does not match the performance of HyperBFT, resulting in significant differences in user experience between the two platforms.

Token stakingAt present, nearly half of dYdX Chain's circulating tokens have been pledged — far higher than Hyperliquid's (less than 10%).

This difference is normal, because the validators of Hyperledger are mainly composed of early participants. Retail users have not been allowed to delegate tokens to validators.

As token utility increases, the staking rate is expected to rise, which may be consistent with dYdX Chain's 53.6%.

Community Token AllocationHyperliquid does not accept any VC investment, and its token issuance is carried out in a fair manner in the community.

31% of the total supply is distributed mainly to early contributors and active community traders through airdrops, reflecting the generous rewards to the community.

This move leverages the market's sentiment to support fair distribution and anti-VC capitalism, strengthening the community-oriented spirit of Hyperliquid.

In contrast, dYdX has raised $85 million in early stage investments from well-known venture capital firms such as a16z and Polychain Capital. As the tokens are unlocked, dYdX inevitably faces selling pressure.

Obviously, Hyperliquid's fair start mechanism effectively avoids excessive dependence on venture capital and guarantees the interests of the community, which is a key factor in the continued strengthening of its token price.

Binance token listing incomeSource: Twitter (DtDt666)Hyperliquid introduces a token auction currency listing mechanism, which is different from the fixed currency listing fee charged by traditional centralized exchanges (CEX). Hyperliquid Adopt a more transparent and fair Dutch auction, linking the currency fee to market demand, ensuring fair pricing.

This method effectively solves the problem of continued low returns on CEX. As shown in the above figure, Binance's tokens have generally seen sharp declines recently, such as $ME and $HMSTR falling by more than 70%, while $AEVO falling by nearly 90%. This phenomenon highlights the shortcomings of the CEX currency listing mechanism and has gradually become a channel for large investors to sell their tokens, which has encouraged an unhealthy market environment.

In contrast, Hyperliquid’s Dutch auction mechanism provides a more sustainable and fairer solution for token listing.

Operational performance/valuation indicatorsSource: ASXN, HypurrscanSource: ASXN, HypurrscanSource: Center;">Source: ASXN, HypurrscanHyperliquid The main sources of revenue include transaction fees and auction listing fees, with a monthly transaction fee revenue of US$39.23 million and an annualized revenue of approximately US$470.76 million.

The auction listing fee revenue reached US$4.745 million within one month, and it was on a steady upward trend. As market demand grows, revenue is expected to increase in the future.

Hyperliquid's total monthly revenue reached US$43.89 million, ranking among the top ten monthly revenue agreements, and even surpassing MakerDAO, showing strong profitability and fiercely competitive market position.

In addition, this study also compares Hyperliquid with other decentralized perpetual trading platforms and Layer1/Layer2 protocols to reveal the reasonable valuation of Hyperliquid.

As shown, Hyperliquid's market cap is at a relatively high level compared to other decentralized perpetual contract trading platforms, almost 8 times its closest competitor Jupiter. This suggests that Hyperliquid has raised the valuation ceiling in the field.

In terms of revenue, Hyperliquid lags only behind Jupiter, but far ahead of other competitors in the field.

To gain a deeper understanding of its profitability, this analysis uses price-to-sales ratio (P/S ratio) as a key indicator.

From FDV (full dilution valuation), Hyperliquid

The price-align ratio of 50.5 times is higher than the industry average and median. According to Circulating MarketCap, the price-align ratio is 16.9 times, higher than the industry median, but lower than the average.

Hyperliquid seems to be somewhat overvalued compared to other perpetual protocols.

Source: Bing VenturesHyperliquid will be launched on the main network in the future and officially becomes the Layer 1 blockchain. Compared with the Layer1 protocol, Hyperliquid still has room for growth in the market value.

In terms of profitability, Hyperliquid ranks second only to Solana. However, given the recent boom, the reported revenue may be a bit inflated in the short term, and the long-term performance remains to be seen.

In terms of price-to-sales ratio, Hyperliquid is valued below FDV in this field and the average and median market capitalization of circulation. This indicates that its valuation is expected to rise further and hasPotential growth potential.

Source: Bing VenturesThis valuation model allocates 50% weight for the perpetual contract and Layer1 sector, respectively, and calculates the following valuation range:

Computed according to FDV: USD 149.8 million - USD 396.72 million, representing a growth potential of 1392%.

From the market value of circulating: US$57.01 million - US$67.74 million, representing a growth potential of 354.75%.

This shows that Hyperliquid has huge growth potential in both areas.

The cyclical evolution model of derivative platforms

Through analysis of the life cycle of mainstream derivative platforms from 2018 to 2024, we found a clear "star effect cycle":

Early stages (2018-2020): technology-driven

dYdX has established technical barriers through venture capital support (such as investment from a16z)

dYdX has established technical barriers through venture capital support (such as investment from a16z)

The market is highly concerned about technological innovation and capacity improvement

Key indicators: Order throughput (TPS), clearing efficiency, slippage level

2. Maturity stage (2021-2022): Efficiency-driven

GMX improves capital efficiency through AMM mechanism

Market focusPoints turn to trading experience and capital utilization rate

Key indicators: capital efficiency ratio (TVL/Volume), user retention rate

3. Transformation stage (2023 to present): Community-driven

Hyperliquid emphasizes community sovereignty (31% token airdrop distribution)

The market focus shifts to governance rights and profit distribution

Key indicators: community profit sharing ratio, governance participation.

Cross-valuation analysis of star effect cycles:First verification: token valuation cycleFrom historical data, the token valuation of decentralized derivatives platforms has undergone obvious cyclical evolution:

Technical driving stage (such as dYdX):

dYdX The token price hit a record high shortly after its launch, with a market value of nearly $2 billion

However, as the project went through multiple cycles, the price has fallen by more than 90% from its historical high

TVL data shows that it is difficult to maintain long-term valuations by just the early technology premium

2. Efficiency-driven phase (such as GMX):

GMX TVL increased from $100 million to $300 million

2. Efficiency-driven phase (such as GMX):

2022-2023, GMX TVL increased from $100 million to $300 million

The ratio of trading volume to TVL (efficiency indicator) increased from 0.8 to 1.2

However, the market's valuation premium for efficiency improvement gradually decreased, and the price of GMX tokensVolatility is highly correlated with the overall market

3. Community-driven phase (e.g. Hyperliquid):

Hyperliquid's TVL soared from $190.96 million to nearly $600 million in just 3 days.

On December 5, trading volume peaked at nearly US$10 billion

P/S ratio (P/S ratio) is a more critical indicator:

-FDV is -50.5 times, which is higher than the industry average.

The market value of circulating is -16.9 times, close to the industry median.

-This valuation structure shows the market's high recognition of the community-driven model.

Second verification: The evolution of the revenue model clearly reflects strategic adjustment:Single expense model (dYdX):

There are mainly dependent on transaction fees, with the recipient fee ranging from 0.2% to 0.5%.

Fee income is highly dependent on market volatility.

Revenue predictability is low.

2. Compound income model (GMX):

The basic on/off fee is set to 0.1%.

Introduce a fund fee mechanism based on dynamic changes in long and short positions

GMX v1's daily fee income fell from millions of dollars at its peak to about $100,000.

3. Diversified income structure (super liquidity):

Innovation fee:

-Transaction fee has dropped to the lowest in the industry (Taker: 2.5bps, Maker: 0.2bps rebate).

-Token Auction Mechanism, monthly income of US$4.745 million.

-Liding fees are allocated more to the community.

Total monthly revenue reached US$43.89 million, ranking among the top 10 DeFi protocols

Revenue structure is more diversified, reducing dependence on a single business model

The third verification: User behavior modelUser behavior data reveal fundamental changes in the platform's attractiveness:

Professional user orientation phase (dYdX):

DAU (daily active users) is between 5,000 and 10,000

The high per capita trading volume indicates that traders are professional

However, user growth is restricted by technical barriers.

2. Retail User Expansion Phase (GMX):

GMX v2 quickly caught up with v1 in terms of DAU. Per capita transaction volume decreased, but overall transaction frequency increased. User retention rate increased, reflecting the enhanced accessibility of products. 3. Community-driven Phase (Hyperliquid):

Innovative user incentives:

Innovative user incentives:

style="text-align: left;">-HLP (hyperliquidity provider)annual return rate is 49%

-Active participation in community governance and token auctions

-Active participation in ecosystem projects (e.g. $PURR, $HFUN)

-Active participation in ecosystem projects (e.g. $PURR, $HFUN)

-Active participation in ecosystem projects (e.g. $PURR, $HFUN)

-From simple trading participation to ecosystem construction

-The intersection of user roles from "traders" to "ecosystem builders"

The intersection of these three verifications reveals a key discovery: successful derivatives platforms are evolving from "single function providers" to "decentralized ecosystems."

However, this evolution also presents new challenges: how to ensure long-term sustainability of the ecosystem while maintaining innovation?

The answer to this question may ultimately determine whether the current "community-driven model" can truly escape the constraints of the periodic model.

Beyond the surface: the paradox of the evolution of derivative platformsA deeper analysis of the aforementioned analysis can reveal several disturbing but illuminating trends:

"Decentralization Trap"

A noteworthy paradox emerges when comparing the development paths of dYdX and Hyperliquid:

dYdX has obtained well-known venture capital institutions such as a16z and Polychain Capital. The early stage investment of $85 million is directly converted into technological innovation to achieve continuous product optimization.

In contrast, Hyperliquid has won community recognition through its fair launch model, allocating 31% of the tokens to the community, realizing decentralized governance. However, its R&D investment has dropped sharply from 30% in the early stage to about 15% now.

We can observe similar patterns during the evolution of GMX. As can be seen from the data, GMX v2 has made progress in community governance, its pace of innovation has slowed down, with average daily expense revenue falling from millions of dollars at its peak to about $100,000.

This trend confirms concern that overemphasizing community profit sharing may undermine the long-term competitiveness of the platform.

2. The "impossible triangle" of perfect risk control

Hyperliquid's technical architecture seems perfect:

HyperBFT consensus mechanism reduces order delay by three times and supports up to 100,000 transactions per second (TPS).

However, cross-references these indicators with risk control parameters reveal a fundamental contradiction: under existing technical conditions, the platform cannot achieve the following three goals at the same time:

Keep super-high capability (100,000 TPS): Hyperliquid achieves this through HyperBFT, but this requires some compromise on centralization.

Ensure controllable risks: Data shows that the clearing accuracy and decentralization of high-frequency transactions show obvious negative correlation.

Achieve full decentralization: Hyperliquid Assistance Fund holds more than $11 million (accounting for 3.3% of the total circulating supply). This centralized risk control mechanism conflicts with the concept of completely decentralization.

3. The cycle of innovation and replication

By analyzing the evolution of major derivative platforms from 2018 to 2024, we found a relatively fixedInnovation cycle:

Vertex Protocol has innovated in the cost structure (Taker fee is 2-4bps and Maker fee is zero), but its basic mechanism is still to optimize the existing model.

GMX v2 improves efficiency by upgrading the fund rate mechanism (0.05%-0.07%), but fails to break through the fundamental technical bottleneck.

Hyperliquid generates considerable vault revenue with an annualized monthly return of 49%, but the sustainability of this high-yield model is questionable.

This periodicity reflects a harsh reality: the true innovation cycle may only last 6 to 8 months, after which the competitive advantage comes more from market timing than technological breakthroughs.

Life-cycle forecast of the "Crypto Tornado" projectBased on historical data analysis of major derivative platforms from 2018 to 2024, we have constructed a life-cycle assessment model of the "Crypto Tornado" project. Hyperliquid's case study reveals clear growth trajectory patterns and potential vulnerabilities for such projects.

Liquid Sustainability: Historical data reveals three-stage liquidity patterns in crypto tornado projects:

Hyperliquid showed significant growth, with its TVL soaring from $190.96 million to $600 million in just three days, while daily trading volume soaring to nearly $10 billion.

But further analysis shows that this growth is mainly driven by the appreciation of token prices, and real capital inflows account for less than 30% of TVL's total growth.

A similar phenomenon was observed in the early stages of the GMX boom in 2021, indicating that the bubble is temporary.

Platform period:

Growth momentum slowed down significantly. Hyperliquid's daily TVL growth rate has dropped from 300% to below 5%.

Trading volume fluctuates greatly, with a peak-to-valley ratio exceeding 5:1.

User structure data shows the "inverted pyramid" trend, with a few large traders contributing more than 80% of the trading volume - a historical precursor to the platform's stagnation.

Recession phase (prediction):

According to five years of similar project data, Hyperliquid is likely to enter a recession phase within 6-8 months.

Historical data show that 95% of similar projects experienced a significant decline in TVL during this period, stabilizing between 15% and 30% of the peak.

On average, the price of platform tokens retreated 70-85% from its peak.

2. Revenue Structure: Hyperliquid currently shows typical signs of early overheating:

Of the $43.89 million monthly income, 89.4% (or $39.23 million) comes from transaction fees, while innovation income (token auction) contributes only 10.6% ($4.745 million).

Historical analysis of all "crypto tornado" projects shows that this cost-dependent structure rarely maintains a full market cycle.

As market enthusiasm cools down, total revenue usually drops to 20-30% of the peak level, and innovation revenue streams tend to disappear completely.

Platform margins are currently 70–80%, generally falling to 20–30%.

3. User retention rate declines: By comparing data from competitors such as dYdX and GMX, an amazingly consistent pattern was found:

In the first quarter, the monthly retention rate remained at around 80-85%.

By the second quarter, the retention rate fell to 60-65%.

It further dropped to 30–35% after six months and stabilized at 15–20% within one year.

This decline stems from the lack of differentiated value propositions.

4. Token economics warning signal:

Hyperliquid's price-to-sales ratio (P/S) is 50.5 times, far exceeding the sustainable industry benchmark of 15-20 times.

80–85% of the community profit sharing rate exceeds the historical breakeven point of 65–70%, indicating potential risks in the future.

Hyperliquid has achieved remarkable short-term results, but its growth trajectory is very similar to the past "crypto tornado" projects.

If there is no fundamental change in the business model in the next 3-6 months, Hyperliquid is likely to embark on the decline of its predecessors.

This case reminds us that when evaluating blockchain innovation, we should not only look at surface data, but prioritize sustainability and real value creation, rather than short-term market dynamics.

Market reconstruction in the era of value capture 3.0Through in-depth exploration of historical data, we have discovered a very insightful breakthrough: the qualitative change in value capture efficiency. This finding stems from an anomaly observation in Hyperliquid revenue data - although its token auction revenue ($4.745 million) accounts for only 10.6% of total revenue, its growth rate is 2.3 times the transaction fee. This seemingly ordinary data point reveals a revolutionary trend.

When comparing these data with earlier projects, a shock occurredHuman model: The growth rate of non-transaction fee income is positively correlated with the life cycle of the project.

For example, in GMX, non-transaction fee revenue accounts for only 5%, and the growth is moderate.

In dYdX, this proportion rose to 8%, with a month-on-month growth rate of 15%.

In Hyperliquid, non-transaction fee revenue accounts for 10.6%, with a month-on-month growth rate of 35%.

The real innovation in value acquisition is shifting from "transaction" to "interaction". The traditional expense-based revenue model is being replaced by a more breakthrough model - the "value interactive network".

Analyzing Hyperliquid's user behavior in the past three months, we found that the number of non-transaction interactions per capita by high retention users increased from 3.2 times/day in the early stage to 12.7 times/day, and these interactions are transforming into platform value with unprecedented efficiency.

The core competitive advantage of the next generation of "crypto tornado" projects will no longer be transaction efficiency, but "interactive monetization efficiency".

Specifically, successful projects can achieve:

ms-level precision interactive pricing:

Current value acquisition still depends on relatively rough time scales (minute level), but future projects can achieve real-time pricing and value extraction for each on-chain interaction.

Hyperliquid Interactive data analysis shows that the value capture accuracy in high-frequency trading has reached the second level and is expected to be optimized to the millisecond level.

2. Revolutionary significance:

The project may complete 80% of the token value discovery within the first 24 hours after its release.

This prediction is based on regression analysis of Hyperliquid's early interactive data, where the value discovery cycle has been shortened from months to weeks.

Next generation projects may use "interactive mining"” to lock value at startup.

3. Paradigm shift in project life cycle theory:

The "lightning-lock-evolution" model may replace the traditional "prosperity-stagnation-decline" model.

Projects no longer pursue long-term high growth, but focus on rapid value acquisition and locking, complete value accumulation in a short time, and then turn to product evolution.

From efficiency competition to speed competitionleft;">Whoever can obtain value as quickly as possible will become the winner of this new model. This not only represents quantitative change, but also a qualitative leap.

This "flash lock evolution" model will have a profound impact on the crypto market. Through an in-depth analysis of Hyperliquid's data, we foresee that this transformation will reshape the market structure in multiple dimensions:

1. The capital flow model will undergo fundamental changes

The traditional "capital pursuit and return" model will be replaced by the "expected lock" mechanism.

Hyperliquid Early data have shown signs of this trend—80% of the initial capital inflows are derived from expected future returns rather than actual returns.

This model may be further strengthened, capital is fully deployed within hours of the project launch, and subsequent price discovery is driven by "interactive value" rather than capital flows.

2. The valuation system will be rebuilt

The traditional valuation model based on TVL and trading volume will become increasingly inaccurate.

A new valuation paradigm based on "interactive depth" will emerge.

style="text-align: left;">Hyperliquid User behavior analysis shows that project value is correlated with the depth of interaction (R² = 0.87), which is significantly higher than the correlation with traditional indicators (TVL: R² = 0.62. Trading volume: R² = 0.58).

This suggests that the value of future projects will depend more on capturing effective user interaction than pure capital scale or transaction volume.

3. DeFi ecosystem reconstruction

The current DeFi ecosystem is based on the accumulation of static value and takes months or years to establish a dominance.

In the new paradigm, the ecosystem will undergo "lightning expansion."

Data from Hyperliquid ecosystem projects such as $PURR and $HFUN show that the startup cycle is shortened by 1/5 and the value acquisition efficiency is increased by more than 3 times.

4. Market structure transformation

The traditional "flagship-ecological project" hierarchy may be replaced by "value interaction network".

In this network, project relations develop from simple dependencies to highly interconnected value acquisition networks.

Hyperliquid data shows that the transfer of value between ecosystem projects has accelerated by nearly 10 times, indicating that future ecosystems will consolidate and integrate value at an unprecedented rate.

5. Investment strategy transformation

The traditional "early investment, long-term holding" strategy may become inefficient.

The new model based on "interactive expectations" will dominate.

Analysis of early investors in Hyperliquid shows that the most successful investors allocate funds based on the expected amount of interaction rather than long-term growth potential.

New role: Interactive Market Maker (IMM)A new market participant will appear—Interactive Market Maker (IMM).

These participants will no longer provide only liquidity, but will also create and optimize valuable user interactions.

However, this new model also brings unprecedented risks.

Fast value acquisition will amplify the cost of errors.

The "golden shovel" of value interactionI mentioned before that the valuation logic of traditional crypto projects is mainly based on static indicators such as TVL, transaction volume, and returns. But as the market turns to the "flash-lock-evolution" model, this valuation method has become obsolete and inefficient.

Through in-depth analysis of next-generation platforms such as Hyperliquid, we have identified a more forward-looking valuation and investment framework.

In the new paradigm, the real "gold shovel" is not a traditional trading platform or liquidity protocol, but an infrastructure that can maximize the efficiency of value acquisition.

Three promising "gold shovel" opportunities:Interaction optimization infrastructure:

Hyperliquid user behavior data analysis shows that there is a significant exponential correlation between project value and interaction efficiency (R²=0.87).

This shows that infrastructure that can improve interaction efficiency will produce a huge overflow of value.

For example, Hyperliquid's HyperBFT mechanism tripled interaction latency, directly driving its rapid growth in valuation.

In the future, infrastructure projects focusing on optimizing on-chain interactive experiences are likely to become the biggest winners in the next bull market.

2. Value capture network:

This is a brand new foundationInfrastructure category, committed to helping projects achieve more accurate and efficient value acquisition.

Hyperliquid's data shows that its innovative revenue growth rate is 10.6%, 2.3 times that of traditional revenue.

This indicates that the market is shifting to a more complex value acquisition model.

Projects that provide infrastructure to support this transformation will gain a significant competitive advantage.

3. Interactive data infrastructure:

Under the new model, user interactive data has become more important than traditional financial indicators.

Analysis of Hyperliquid valuation data shows that there is a strong correlation between the valuation multiple and the integrity of the interactive data.

This shows that infrastructure that can provide high-quality interactive data analysis and optimization services will become an important part of the ecosystem.

New requirements for investment strategies:This change in model puts forward new requirements for investment strategies.

Traditional investment methods usually focus on surface-level indicators, such as token economics or team background.

In the new model, successful investment strategies will prioritize the project's "Interaction Efficiency Index (IEI)".

This is a new metric we developed based on Hyperliquid's data to evaluate:

Interaction delay: the speed at which the project handles user interactions.

Value capture efficiency: the actual value generated by each interaction.

Network effect multiplier: the amplification effect of interactive value.

Using this index, we can predict the potential value of the project more accurately.

For example, early data from Hyperliquid showed that the correlation between the IEI index and subsequent valuation growth reached 0.92, far exceeding the traditional indicators.

Investment strategy advice—"Infrastructure first":We recommend adopting an "infrastructure first" investment strategy.

This means prioritizing projects that provide core infrastructure support in the early stages of new projects.

It is worth noting that future "gold shovel" projects may be very different from traditional infrastructure projects.

They may be similar to "value accelerators" that profit by optimizing and accelerating the value acquisition process.

Time and entry points:In the new paradigm, the best entry points often occur early in the project, i.e. when interactive optimization is strong.

This new investment framework forces us to rethink what is the real "golden shovel".

In the era of value interaction, the real opportunity lies not in replicating the model of successful projects, but in building infrastructure that continuously improves the efficiency of the entire ecosystem.

These projects may not experience explosive short-term growth like Hyperliquid, but they will occupy a more core and lasting position in the new market paradigm.