58 mins ago

6,437

Author: Peng Xingyun Deputy Director of the Financial and Development Laboratory

After the Central Bureau meeting held on December 9, 2024 proposed to implement "moderately loose currency", the Central Economic Work Conference held from December 11 to 12, 2024 once again emphasized the orientation of currency. This is the first time in more than a decade that my country's expression of currency orientation has shifted from a "stable currency" to a "moderately loose currency", which has attracted high attention from the market. This article analyzes the direction of moderately loose currency, which involves several important issues: Why should we implement moderately loose currency? What measures may be taken by the central bank? What impact may a moderately loose currency have?

Money Analysis - From "stable" to "moderate easing" 01 Why should we implement a moderately easing currency be stable and promote economic growth? It is the ultimate goal of my country's currency legality. As an important tool and means for total demand management, currency is to smooth out the cyclical fluctuations of the economy, and the monetary position depends on the performance of the macroeconomic. When the economy is overheating and inflationary pressure is high, the central bank will adopt a tighter currency; on the contrary, when the economic growth is weak and the employment pressure is high, the central bank will adopt a looser currency. This is the basic principle of central banks in currency operations in various economies. A socialist market economy with characteristics is no exception when implementing currency.In the 24 years since the new millennium, except for the "moderately loose currency" that was clearly proposed in 2009 and 2010, the currencies of the other years were defined as "stable currency". When the first proposed "positive fiscal" and "stable currency", it was exactly the impact of the Asian financial crisis and strong measures were needed to stabilize the macro economy. Therefore, "stable currency" actually refers to loose currency. But after entering the new millennium, "stable currency" has actually transformed into a basic principle of currency operation, which no longer corresponds to loose or contractile currency. In fact, among the "stable currency" that has been implemented since the new millennium, in some years, the central bank has been continuously increasing the statutory reserve ratio or interest rates in the deposit and loan benchmark, and in some years, it has continued to lower the reserve ratio and increase the central bank's re-lending to financial institutions. No matter which currency operation direction the central bank adopts, it is to "maintain a reasonable abundance of liquidity."

This Central Economic Work Conference clearly proposed that "moderate easing should be implemented."The currency of the economy conveys a clear direction of monetary operation to the economic system, that is, through more abundant liquidity supply, lower market interest rates, boost market confidence, and improve expectations. But this does not mean that the currency has abandoned the principle of "stable", because "loose currency" must be "moderate" rather than excessive easing or flooding, and still requires that "the growth of social financing scale and money supply match the expected targets of economic growth and total price level."

It should be noted that the Central Economic Work Conference proposed that "the implementation of moderate easing currency" is not a fundamental change in the monetary position. In fact, in the past few years, the People's Bank of China has been adopting relatively loose currency in order to maintain a reasonable level of liquidity. . First, since 2015, the central bank has reduced the statutory deposit reserve ratio more than 20 times. The statutory deposit reserve ratio of large commercial banks has dropped from the original high of 21.5% to 9.5% now, and the deposit reserve ratio of small and medium-sized commercial banks has dropped from the original high of 19.5% to the current 6.5%. The reduction of the reserve requirement alone has released more than 10 trillion yuan of liquidity that was frozen. Secondly, the central bank provides liquidity to the market through various re-lending tools, which is reflected in the central bank's balance sheet. The central bank's claims for deposit-related financial institutions have increased from less than 2.5 trillion yuan at the end of 2014 to more than 17.4 trillion yuan at the end of September 2024, an increase of nearly 15 trillion yuan in less than 10 years. Third, although the central bank has not adjusted the benchmark interest rate of deposits and loans since 2015, it has been continuously lowered in the central bank's monetary operation. Interest rates directly drive the market interest rate downward. For example, the loan market quotation rate (LPR) fell from 5.76% in 2014 to 3.1% at the current level, and the weighted average interest rate of RMB loans in financial institutions fell from 6.96% at the end of June 2014 to 3.67%, down more than 300 basis points. Corresponding to the sharp drop in loan interest rates, the bond market interest rate has also ushered in the longest downward cycle since the reform and opening up, and the 10-year treasury bond yield fell from around 3.88% at the beginning of December 2017 to less than 1.8%. In short, the continuous decline in bond market yield reflects the fact that liquidity and currency have always been relatively loose.

So, in currency When a loose attitude has been adopted, why should we clearly propose "to implement moderately loose currency"? Fundamentally speaking, this is a macroeconomic need. When diagnosing the macroeconomic situation in my country, the Central Economic Work Conference pointed out that "my country's economic operation still faces many difficulties and challenges, mainly due to insufficient demand, some enterprises have difficulties in production and operation, people's employment and income increase, and there are still many risks and hidden dangers. ”

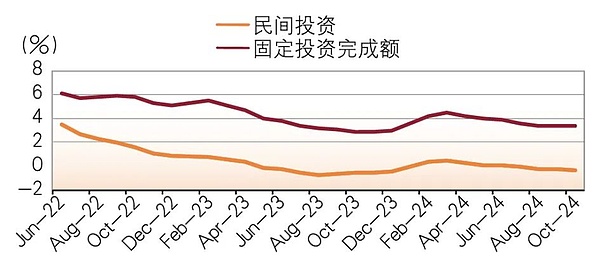

First, investment and consumption demand are weak. FixedAsset investment has been at a low level after the epidemic, and since 2023, the growth rate of fixed asset investment has been below 5%. In particular, private fixed asset investment has been extremely weak. Since December 2022, the growth rate of private fixed asset investment has been lower than 1%, and since May 2023, the growth rate of private fixed investment has shown negative growth in most months (see Figure 1). Due to insufficient private investment needs, investment has to be relied on to stabilize growth and investment, which not only increases the pressure on fiscal expenditure at all levels, but also increases the debt burden. Final consumption is also very weak. In the early stages after the end of the epidemic, although the total retail sales of consumer goods rebounded for a while, it did not last long and showed a relatively weak trend. In December 2022, that is, when the epidemic control was relaxed, the growth rate of total retail sales of consumer goods was -0.2%, rebounded to 9.3% in May 2023, and has since declined all the way, and has dropped below 4% after June 2024.

Figure 1 The completion amount of fixed asset investment and the growth rate of private investment

Source: compiled by Wind

Second, secondly, prices are sluggish. Since October 2022, PPI has continued to grow negatively for 26 months, and the PPI has been below -2.5% in the past three months (September to November 2024). Although the performance of CPI is slightly stronger than PPI, it has been hovering around 0 for 17 months, significantly lower than the global major 2% inflation target (see Figure 2). Because of this, Central Bank Governor Pan Gongsheng said in October 2024 that "promoting a reasonable rebound in prices will be an important consideration." Due to the continued sluggish price levels, more flexible space has been created for further implementation of moderate easing currencies.

Figure 2 CPI and PPI

Source: According to Wind

Third, the growth rate of corporate profits continues to decline. Data from the Bureau of Statistics shows that from January to November 2024, in addition to foreign-owned enterprises and Hong Kong, Macao and Taiwan-invested enterprises barely maintaining positive growth, the total profits of state-owned enterprises and joint-stock enterprises decreased significantly. The profit growth rate of their controlled enterprises was -8.2%, and joint-stock enterprises was -5.2%. Although the profit growth rate of private enterprises was not as large as the previous two, it was also -1.3%.growth. Corresponding to the continued decline in corporate profit growth rate, the capacity utilization rate of industrial enterprises has also declined significantly (see Figure 3). The capacity utilization rate in the third quarter of 2024 was only 74.6%, which means that more than 25% of the capacity is idle. In fact, the 2023 Central Economic Work Conference pointed out that "some industries have overcapacity." The continued decline in profit growth rate and excessively high production capacity will inevitably further have an adverse impact on the confidence of enterprises, which is one of the important factors for weak private investment.

Figure 3 Profit growth rate of industrial enterprises of different ownerships from January to November 2024

Source: Bureau of Statistics

Fourth, the real estate industry is still in deep adjustment. In the past few years, although a number of projects have been introduced to support the development of the real estate industry, the decline in the real estate industry has not been fundamentally reversed, and the real estate industry is still in deep adjustment. From April 2022 to November 2024, the amount of real estate development investment completed has been negative for 30 consecutive months, and the negative growth trend has not only not converged, but has also deteriorated slightly. From May to November 2024, the growth rate of real estate development investment completion exceeded -10%, and from September 2023 to April 2024, it was between -9% and -9.8% (see Figure 4). The decline in real estate construction area and real estate sales area are more likely to decline than the real estate development investment. Since 2024, the growth rate of real estate construction area has been below -10%. Although the decline in sales area growth rate has narrowed, it is still in the range of -15% to -20%. In particular, the growth rate of real estate sales area is in the range of -25% to -32%, which puts real estate development companies under tremendous pressure on capital turnover (see Figure 5).

Figure 4 Real estate development investment growth rate

Source: compiled by Wind

Figure 5 Real estate sales area growth rate

Source: compiled by Wind

Source: compiled by Wind

02 Possible measures for the central bank to implement moderate easing of currency

The Central Economic Work Conference pointed out: "Give full play to the dual functions of total monetary tools and structure, and reduce reserve requirement ratios in a timely manner... Explore and expand the central bank's macro-prudential and financial stability functions, innovate financial tools, and maintain financial market stability. "This points out the general operation method of moderately loose currency.

First, continue to reduce the statutory deposit reserve ratio. Although the central bank has reduced the statutory deposit reserve ratio more than 20 times, there is still a large room for downgrade. In fact, the central banks of many developed economies around the world have now abolished the statutory deposit reserve system, even if the statutory deposit reserve system is still retained. , the statutory reserve ratio is also very low. There are many reasons for this. For example, the capital adequacy supervision implemented by all commercial banks has imposed constraints on the credit of commercial banks. Even if the deposit reserve ratio cannot be determined, commercial banks cannot expand their credit unlimitedly. In addition, multiple crises have also shown that the statutory reserve ratio is difficult to ensure that commercial banks in liquidity difficulties can obtain sufficient liquidity and repayment methods in a timely manner, and ultimately have to rely on the central bank's lender mechanism to provide assistance. Now, the statutory reserve ratio of large commercial banks is 9.5%, and the 6.5% of small and medium-sized commercial banks. In the future, commercial banks still have at least 4.5 percentage points of room for reduction in reserve requirements. This is because the deposit money absorbed by large commercial banks in my country and the total amount of credit provided by large commercial banks account for the vast majority of the proportion.

Secondly, the total amount of central bank loans is combined with structural tools. Between the expansion of the total amount of central bank loans and the reduction of the statutory reserve ratio, moderately loose currencies should give priority to continuing to lower the statutory reserve ratio. As the interest rate paid by the central bank to financial institutionsExtremely low, increasing the opportunity cost of commercial banks, and commercial banks will inevitably pass on the costs to borrowers. Although reducing the fiat reserve ratio is a priority instrument option for moderately easing currencies, the role of central bank loans is still very important. The central bank will still increase the total supply of liquidity through re-lending, and at the same time use various structural monetary tools to guide the allocation of credit resources of financial institutions. However, some companies need to be prevented from arbitrage using preferential interest rates in structured currencies.

Third, increase the purchase of treasury bonds in open market operations. Unlike the central banks in other developed economies that hold a large amount of treasury bonds, the proportion of treasury bonds held by the central bank in my country accounts for extremely low levels of their total assets, which is actually not conducive to the central bank's guidance on market interest rates and their expected management through currency operations. In 2024, the central bank of my country began to try again to conduct inventory bonds on treasury bonds through the open market, but the scale was very small and had a limited impact on the total liquidity. In order to better implement moderately loose currencies, the central bank should increase the buying-out transaction of treasury bonds in open market operations. Given that my country's treasury bond balance and GDP are relatively low, if necessary in the future, the central bank may even consider purchasing a portion of provincial general bonds with low credit risks as a supplement to the central bank's treasury bond operations in the open market to better manage the total liquidity.

Finally, as a researcher, the author has always advocated that the deposit and loan benchmark interest rate should be abolished. The benchmark interest rate for deposits and loans has not been adjusted since 2015. In fact, LPR has long replaced the deposit and loan benchmark interest rate set by the central bank and has become the new interest rate benchmark for commercial bank loans. In currency operations, the central bank is also guiding the seven-day reverse repurchase rate to become the main interest rate, but at the same time, it still retains the remains of the planned economy, which is inconsistent with the market-oriented reform of the economy. While the market interest rate has experienced a very long downward cycle in the past five years, and both the loan interest rate and the bond market yield are at the lowest level since the reform and opening up, it is inappropriate to continue to retain the deposit and loan benchmark interest rate level nine years ago. It neither reflects the changes in the liquidity situation of the macro economy and financial markets, nor conveys monetary intentions.

03Possible impact of moderately easing currencies

No doubt, moderately easing currencies will have some positive impacts on the macroeconomic and financial markets. It will first change the reserve structure of commercial banks. The release of central banks and the added liquidity will affect the supply of loanable funds. Enough liquidity will put market interest rates generally at low levels for the next period of time. In other words, it has entered the era of ultra-low interest rates, which is both the result of loose currency and the macro economy.natural consequence of economic operation. Given that the bond market interest rates and deposit and loan interest rates are already at extremely low levels, this may lead to a readjustment of the financial asset structure of institutional investors and residents. In this sense, moderately loose currency will be conducive to the realization of the goal of "stabilizing the stock market" proposed by the Central Economic Work Conference.

In addition, the RMB exchange rate will respond necessary to changes in economic fundamentals and international environment. After Trump re-entered the White House, exports faced tariff pressure again, and hedging tariff risks objectively requires a certain degree of exchange rate depreciation. At the same time, the continued downward interest rate has further widened the interest rate gap between China and the United States, which will also put pressure on the RMB exchange rate. Of course, exchange rate fluctuations may in turn restrain changes in market interest rate levels, because exchange rate depreciation may certainly promote exports, but it will also weaken the competitiveness of currencies, which is in a certain degree of conflict with the need for a "strong currency" in the construction of a financial power.

However, loose currencies also face some challenges. First of all, the total amount of money and liquidity is already very abundant. As of the end of November 2024, the balance of broad currency M2 has been nearly 312 trillion yuan, and the ratio to GDP has exceeded 200%, making it the economy with the largest total currency in the world. This itself shows that the difficulties and challenges facing the economy are not the result of insufficient money supply. We clearly see that although the broad currency M2 still maintains significant positive growth, the current deposit balance of non-financial enterprises is continuing to decline, which shows that the currency demand held by enterprises based on business motivation is insufficient. Secondly, at the end of 2023, the macro leverage ratio has reached about 350%. The debt pressure faced today is closely related to the debt risks in some places to some extent to the past currency and credit expansion. Therefore, moderately loose currencies must weigh credit expansion and future credit risks. Third, the difficulties and challenges facing the economy are due to the internal laws of economic development, especially the economic difficulties brought about by the deep adjustment of the real estate industry, which are the result of changes in the supply and demand pattern of the real estate market and the qualitative change in the industrial cycle. It is impossible to expect the real estate industry to enter the era of rapid expansion in about 20 years after the new millennium through moderately loose currency. At the same time, the adverse impact of global trade and geopolitical environment changes seems to take a long time to digest.

Moderately loose currency is just a stopgap measure. In order to achieve the goals of "stabilizing growth" and "stabilizing investment", while implementing moderately loose currency, it is also necessary to improve the market economic system through deepening reforms to enhance confidence.This is the confidence of private entrepreneurs in the future, which makes them dare to invest, invest with confidence and invest with confidence. This requires that in practice, we truly "equally protect the legitimate rights and interests of enterprises of all types of ownership in accordance with the law" and ensure that enterprises of all types of ownership can compete fairly without discrimination. To this end, departments at all levels need to fully understand the laws of the operation and competition of the socialist market economy, learn to better deal with the market economy, put "power in the cage of the system", and power serves fair competition in the market, rather than overtaking market competition.

In addition, in order to improve the effectiveness of moderately loose currency, it is necessary to better integrate with the global economy.