1 hours ago

3,227

Author: Airdrop Reference, Source: Author Twitter @AirdropDaii

One day in 2030, when BlackRock's Bitcoin ETF surpassed the S&P 500 Index Fund, Wall Street traders suddenly realized: the thing they once ridiculed as a "dark web toy" is now controlling the throat of global capital.

But all the twists began in 2025—that year, when the price of Bitcoin broke through $250,000 in the hunt for institutional whales, but no one could tell who it belonged to. On-chain data shows that more than 63% of the circulating supply is locked into institutional custody addresses, and the exchange's Bitcoin liquidity is exhausted to only support three-day trading volume.

The above is fantasy, let’s go back to the present first.

A large amount of funds are continuing to flow out of Bitcoin ETFs, and Bitcoin once fell below 80,000. There are two main explanations for this phenomenon: First, it is that Trump in the United States launched a tariff war; second, the capital side is because 56% of short-term holders - hedge funds - closed positions.

However, analysts believe that it is currently in the "distribution stage" of the Bitcoin bull market.

The "distribution phase" of the Bitcoin bull market usually refers to the fact that before and after the price peaks in the later stage of the bull market, the big investors ("whale") began to gradually sell their chips, transferring Bitcoin from early holders to new investors entering the market. This stage means that the market will shift from a crazy rise to the top area, which is a key link in the bull and bear transformation.

If you don’t keep it a secret, give the answer first, the current market liquidity structure has changed.

OG retail investors and OG whales are playing sellers;

Institutional whales and new retail investors entering through ETFs become the main buyers.

In the cryptocurrency field, "OG" is the abbreviation of "Original Gangster" (also often interpreted as "Old Guard"), specifically refers to the earliest participants, pioneers or core groups that have been persisted in the Bitcoin field.

In a word, old money is withdrawing, new money is entering. Institutions dominate the new money.

Below we will give you a detailed analysis from the aspects of market structure, current cycle characteristics, institutional and retail investors' roles, cycle timelines, etc.

1. Typical market structure: whales allocate to retail investors at the end of the bull market.The typical bull market of bitcoin shows that whales distribute chips to retail investors, that is, early large holders sell coins at a high price to retail investors who enter the market later.

In other words, retail investors often take over the market at high levels in a fanatic atmosphere, while the "smart money" whales take the opportunity to ship in batches at high prices and realize profits. This process has been staged many times in the historical cycle:

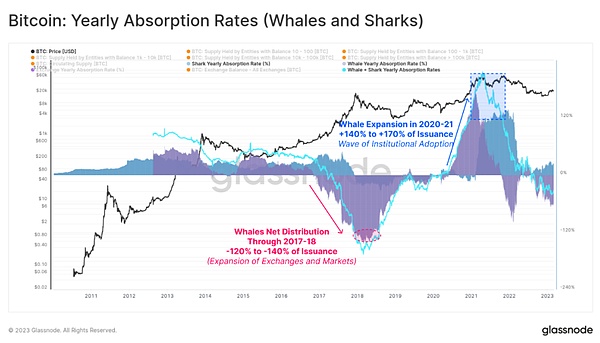

For example, when the bull market approached its peak in 2017, the net decrease in the balance of Bitcoin held by whales, indicating that a large number of chips were transferred from whales.The reason for moving out is that a large amount of new demand poured into the market at that time, providing sufficient liquidity for whales to distribute their positions. For details, see: The Shrimp Supply Sink: Revisiting the Distribution of Bitcoin Supply.

Overall, the market structure at the end of the traditional bull market can be summarized as: early-stage big investors gradually sold off, market supply increased, and retail investors bought and took over a large number of buys and took over, driven by FOMO sentiment (fear of missing out). This distribution behavior is often accompanied by signs such as increasing Bitcoin inflows on exchanges and moving old coins on chains, indicating that the market is about to reach its peak.

2. Characteristics of this bull market: new structural changesThe current allocation stage of this bull market (2023-2025 cycle) is different from the past, especially reflected in the behavior of retail investors and institutional investors.

2.1 This cycle has unprecedented institutional participation

The launch of spot Bitcoin ETFs and listed companies' large-scale purchase of coins has made the market participants more diverse, and it is no longer just retail investors to promote the market. The addition of institutional funds has brought about a deeper fund pool and more stable demand, which is directly reflected in the fact that the market volatility has decreased compared to the past. According to analysis, the maximum drawdown in the current bull market is significantly smaller than in the past cycle, and the high-point pullback usually does not exceed 25%-30%, which is attributed to the intervention of institutional funds that has stabilized the volatility.

At the same time, the market maturity has increased, the price increase has decreased cycle by cycle, and the trend has become more stable. This can also be seen from indicators such as the growth rate of realized cap: this round of market value has only expanded a small part of the previous peak, indicating that the fanaticism has not been fully released (see: ThinkingAhead for details)

Realized cap is an important indicator to measure market capital inflows. Unlike traditional market cap (MarketCap), the realized market cap is not simply multiplied by the current price by the circulating supply, but considers the price of each bitcoin at the last transaction on the chain. Therefore, it can better reflect the scale of funds actually invested in the market.

Of course, the above indicators may also indicate that the market is entering a more mature and stable development stage.

2.2 Retail investors are also more rational and diverse in this round of behavior. On the one hand, senior retail investors (individual investors who have experienced multiple cycles) are relatively cautious and lock in profits earlier after a certain increase, which is different from the previous situation where retail investors chased the rise to the top.

For example, data at the beginning of 2025 showed that small-scale coin holders (retail investors) netted about 6,000 BTC (about 625 million US dollars) to the exchange in January and started cashing out in advance. During the same period, whales only had a small net inflow of about 1,000 BTC, basically remained unchanged. This disagreement means that many retail investors agreeIn order to reach the peak in stages, we chose to make a profit, while whales (that are regarded as "smart funds") remained silent, obviously looking for higher profit margins.

On the other hand, the newly entered retail investors' investment enthusiasm is still accumulating. Indicators such as Google Trends show that public attention once fell and "reset" after the price hit a new high, and there has not yet been a peak of national fanaticism at the end of previous cycles. This implies that the current bull market may not have entered the final fanatic stage yet and the market's upward potential remains.

2.3 Institutional behavior has become one of the important characteristics of this round

The last bull market from 2020 to 2021 was the first time that a large number of institutions and listed companies entered the market. At that time, whales held a currency increase - new "big investors" such as institutions bought in large quantities, and Bitcoin flowed from retail investors to these whale accounts.

This trend continues in the current cycle: large institutions purchase Bitcoin through channels such as OTC over-the-counter markets, trust funds or ETFs, making traditional whales no longer a net seller, delaying the arrival of the distribution stage to a certain extent. This makes the distribution of this bull market more ease and diversified, rather than the past model of simply taking over by retail investors: the depth and breadth of the market are increased, and new funds are enough to digest the chips thrown by long-term holders.

Glassnode report points out that a large amount of wealth has been or is shifting from long-term holders to new investors, which is a sign that the Bitcoin market will mature - long-term holders have achieved record profits (up to US$2.1 billion in a single day), and new investors have enough demand to take over these sellers. For details, see Bitcoin sees wealth shift from long-term holdersto new investors-Glassnode

It can be seen that the interaction between retail investors and institutions in this bull market has created a more resilient market environment.

3. Changes in roles between institutions and retail investorsThe following discusses the impact of OG retail investors and institutions on liquidity

As the evolution of the market participant structure, the roles of institutions and retail investors in the distribution stage have also changed significantly.

CryptoQuant CEO Ki Young Ju summarized this round of distribution model as: "old-level" retail investors (OG retail investors) + original whale > new retail investors (through ETFs, MSTRs and other channels) + new whale (institution).

In other words, retail investors and whales that have experienced early cycles are gradually selling, and the takeover not only includes retail investors in the traditional sense, but also ordinary investors entering the market through investment tools such as ETFs, as well as new institutional funds that play the role of whales.

This diversified participation pattern is completely different from the traditional single-line distribution model of "whale → retail investors".

In this cycle, OG retail investors (individual coin holders who entered the market in the early stage) may hold a considerable amount of Bitcoin, and they choose to cash out and leave the market at the high stage of the bull market, providing the market with some selling pressure and liquidity.

Similarly, OG whales (early large players) will ship in batches and cash out profits several times or even dozens of times. Correspondingly, institutional whales, as a new buyer, absorbed these selling pressures in large quantities. They bought through channels such as custodial accounts and ETFs, and Bitcoin flowed from old wallets to custodial wallets of these institutions.

In addition, some traditional retail investors now also hold Bitcoin indirectly through ETFs and listed company stocks (such as MicroStrategy's stocks), which can be regarded as a new form of "retail investor takeover".

This role change has had a profound impact on market liquidity and price trends.

3.1 More Bitcoins are leaving the exchange

On the one hand, OG holders' selling behavior usually leaves obvious on-chain footprints: increasing changes in old wallets, large-scale transfers flock to exchanges, etc.

For example, in this bull market, some long-term unmoved wallets have been observed to become active, and transferring coins to the exchange for sale is a sign that old holders have begun to allocate chips. KiYoung Ju pointed out that OG players' activities will be reflected through on-chain and exchange data, while the flow of "paper bitcoin" (such as ETF shares, Bitcoin-related stocks) will only be reflected as on-chain records of the custodial wallet at settlement. In other words, the purchase of institutional funds mostly occurs off-market or through custody, and the direct chain reflects the increase in the address balance of the custodian, rather than the direct flow of traditional exchanges.

The current exchange's Bitcoin balance is 2.22 million, which is also a reaction to this feature.

3.2 New whales and new retail investors are more resilient

On the other hand, institutional investors, as new whales, not only provide huge buying support, but also enhance the market's acceptance and liquidity depth under the pressure of selling.

Unlike when retail investors were easily panic and stampedeed in the past, institutional funds tend to be more inclined to buy at low prices and allocate them for a long time. When the market pulls back, the intervention of these professional funds can often support the bottom and stabilize the price. For example, some analysts pointed out that the reduction in volatility in this bull market is attributed to institutional participation: when retail investors sell, institutions are willing to take over to ensure market liquidity, so that the price retracement is much smaller than in the past.

Although the launch of Bitcoin ETFs has brought a large amount of incremental funds to the market, some ETF holders (such as hedge funds) may use arbitrage trading as their main purpose, so their funds are liquid. The recent large outflow of ETF funds shows that some institutional funds are only conducting short-term arbitrage rather than holding them completely for a long time. Bitcoin has recently fallen below 80,000. The pressure on the capital side comes from hedge fund arbitrage strategies to close positions.

However, new retail investors have shown strong resilience. They did not sell panic in every adjustment, but were willing to continue holding BitcoinThe short-term holder indicator shows stronger resistance to declines.

In general, the interaction between OG retail investors + OG whales and new institutional whales + new retail investors has formed a unique supply and demand pattern in the current market:

Early holders provide liquidity, institutions and new buyers absorb chips, making the distribution process in the later stage of the bull market more stable and traceable.

4. Cycle timeline: historical trends and this bull market outlookFrom historical data, the Bitcoin market presents a pattern of about four years and a cycle, each round includes a complete cycle of bear market-bull market-transition. This is highly correlated with the Bitcoin block reward halving event: After the halving occurs, the output of the new currency sharply declines, and a sharp price increase (bull market) will often occur in the next 12-18 months, and then enters a bear market adjustment near the high point.

4.1 History

Review the timelines of several major bull markets:

The first halving occurred at the end of 2012, after which Bitcoin price peaked in December 2013 about 13 months later;

The second halving in 2016 was halved, and the bull market peaked in December 2017 about 18 months later;

The third halving in May 2020, and about 17-18 months later, at the end of 2021, Bitcoin experienced two peaks of nearly $70,000.

It is speculated that the fourth halving in April 2024 may trigger a new bull market, with its peak likely to occur within one to one and a half years after the halving, that is, about the second half of 2025, and the final distribution stage will usher in (the end of the bull market).

Of course, the cycle is not a mechanical repetition, and changes in the market environment and participant structure may affect the duration and peak of this bull market.

4.2 Optimism

Some analysts believe that the macro environment, supervision and market maturity will have an important impact on this cycle.

For example, Grayscale's research team pointed out in a report at the end of 2024 that the current market is only the medium-term stage of a new cycle. If the fundamentals (user adoption, macro environment, etc.) remain good, the bull market may continue until 2025 or even longer. They stressed that the newly launched spot Bitcoin ETFs have broadened the channels for capital entry, and the bright future of the US regulatory environment (such as Trump's new potential impact) may further boost crypto market valuation.

This means that this bull market is expected to be longer than in the past cycle, and the rise may cross the traditional time window.

On the other hand, there are also views on-chain data that support a long bull market. For example, the growth of real capital inflows (RealizedCap) in this cycle mentioned above has not yet reached half of the previous round high, indicating that the market fanaticism has not been fully released. Some analysts therefore predict that the final high of this bull market may be far beyond the previous round, and the highs are expected to be raised to$150,000 or more.

4.3 Conservative

However, there are also opinions that the vertex will appear within 2025.

CryptoQuant's Ki Young Ju expects that the final distribution phase of the Bitcoin bull market (several OG holders and institutions are concentrated to ship the final takeover funds) will occur within 2025. His judgment is based on the early distribution phase that has entered and the observed influx of new retail funds, and believes that there is no need to turn short before the final shipment is completed.

Comprehensive historical models and current indicators, it can be inferred that this bull market is likely to come to an end in the second half of 2025. By then, as prices reach a temporary peak, all kinds of holders will accelerate the distribution of chips to complete the final distribution process.

Of course, the exact time and height are difficult to predict, but judging from the length of the cycle (about 1.5 years after halving) and market signs (retail crazy degree, institutional funding trends, etc.), 2025 may become a key year.

5. ConclusionWhen Bitcoin transforms from geek toys into a trillion-level strategic asset, this bull market may reveal a cruel truth: the essence of the financial revolution is not to eliminate old money, but to reconstruct the genetic chain of global capital with new rules.

The "distribution stage" at this moment is actually the coronation ceremony of Wall Street's official takeover of the crypto world. When OG Whale handed over the chips to BlackRock, this is not a prelude to the collapse, but a march of the reconstruction of the global capital map - Bitcoin is evolving from the myth of retail investors to a "digital strategic reserve" on the institutional balance sheet.

The irony of the matter is that when retail investors are still calculating the "top escape password", the Blackstones have already written Bitcoin into the balance sheet template for 2030.

The ultimate question in 2025: Is this the pinnacle of cycle reincarnation, or is it the pain of the birth of a new financial order? The answer is hidden in the cold chain data - the transfer record of every OG wallet is adding bricks to BlackRock's custody addresses; the net inflow of each ETF is rewriting the definition right of "store of value".

A piece of advice for investors who travel through the cycle: The biggest risk is not to miss the opportunity, but to interpret the rules of the game in 2025 with the cognitive cognition of 2017. When the "coin holding address" becomes the "institutional custody account", when the "halving narrative" becomes the "derivative of Fed interest rate decisions", this century-long handover has long exceeded the scope of bull and bear.

History is always repeated, but what appears this time is not the tears of retail investors, but the never-ending on-chain transfers of institutional vaults.

This institutional trend may be analogous to the evolution of the Web1.0 era - the mutual interaction between geeks at the beginningConnecting to the Internet eventually fell into the hands of FAANG (Facebook, Apple, Amazon, Netflix and Google).

The cycle of history is always full of black humor.