19 mins ago

8,817

Core view

"American Exceptionism" originated. "American exceptionalism" represents a type of view that the United States' economy, and dollar assets have unique advantages, allowing it to continue to outperform other markets in the global cycle. This view will be strengthened in 2023-2024. Behind the outstanding performance of US dollar assets, the advantages of US economic, and technological development are indeed reflected. 1) Economy: The US economy maintains rapid growth above the pre-epidemic level, and is immune to the scar effect after the epidemic. 2): The US fiscal stimulus "exceptionally" breaks through traditional constraints and continues to become an important support for the economy. The Federal Reserve maintains high interest rates, but effectively avoids economic and financial risks caused by high interest rates. 3) Technology: The leadership in the US technology field is highlighted in the new round of artificial intelligence (AI) development and catalyzed the strong performance of US stocks. 4) "Trump Deal": Trump's election once strengthened the "American exceptionalism", which made investors more confident in the US economy and dollar assets.

"American Exceptionism" reversal. From January to February this year, US stocks underperformed Hong Kong and European stocks, and the US dollar index fell back, and the capital market seemed to have traded "USD exception theory" ineffective. 1) Economy: The most intuitive signal is that US economic data has unexpectedly weakened and concerns about stagflation have risen sharply. Judging from the Citigroup Economic Surprise Index, recent U.S. economic data has been the most disappointing stage since Trump was elected. As of February 28, the GDPNow model's prediction value turned negative. 2) Trump's new policy: Trump's tariffs amplify economic uncertainty and aggravate concerns about stagflation. Trump streamlines the aggressive actions of institutions hinder Congressional budget negotiations and also implies economic downturn risks. The issue of spending and tariff reductions is closely linked to future tax cuts, reflecting the deep-seated contradiction that the U.S. fiscal difficulties are difficult to balance. The difficulty of the US expansionary fiscal implementation in the future may be higher than expected, which will conceal the US economic prospects. 3) Technology: DeepSeek breaks through the US technology monopoly expectations and catalyzes the adjustment of US stocks. In addition, Europe may also benefit from the reshaping of this technological competitive landscape.

There is still room for global asset reconfiguration. The recent rapid reversal of the "American Exceptionism" reflects the risk of excessive concentration of global funds on US dollar assets over the past two years or even longer. Since Trump took office, the economic uncertainty of the United States has risen sharply, and the direction of the United States may not be as strong as expected. The difficulty of US fiscal balance and the negative effects that may have on the economy in the pursuit of balance deserve further attention. The pattern of Sino-US and global economic and trade, science and technology and geopolitical games has also undergone important changes. Under these changes, investors may re-examine the difficult-to-false long-term narrative of the “U.S. exception” and adjust their regional allocation strategies. This process may be difficult to "one step"In place, it may take a longer process. We believe that there is still a lot of room for global asset allocation. Since 2025, the stock market (especially Hong Kong stocks), European stocks, etc. have outperformed the US stock market, but it has far failed to make up for the huge gap between the performance of US stocks since 2020 (the impact of the new crown). The gap between AI and technology development between China and the United States is not significant. Considering the growth of the market, the valuation of high-quality companies in A-shares and Hong Kong stocks still has a lot of room for growth compared with US stocks.

Risk warning: Trump's fiscal expansion exceeded expectations, the Federal Reserve's interest rate cut exceeded expectations, and the United States' economic and trade restrictions on non-US regions exceeded expectations, etc.

From 2023 to 2024, "American Exceptionism" has become a major main line of global asset allocation, that is, US stocks continue to outperform non-US stock markets, and the US dollar remains strong. This reflects the advantages of US economic and technological development, and Trump's election once strengthened its investment confidence in US dollar assets. However, since 2025, US stocks have underperformed non-US stock indexes such as Hong Kong and European stocks, and the US dollar index has also weakened. At present, the economic uncertainty of the United States has risen sharply since Trump took office, and the US economy may not be as strong as before. The difficulty of US fiscal balance and the negative effects that may have on the economy in the pursuit of balance deserve further attention. The pattern of Sino-US and global economic, trade, technology, and geopolitical games has also undergone important changes. We believe that the investment theme of "Reversal of US Exceptionism" has not yet ended, and there is still a lot of room for global asset allocation.

1. The origin of "American Exceptionalism"

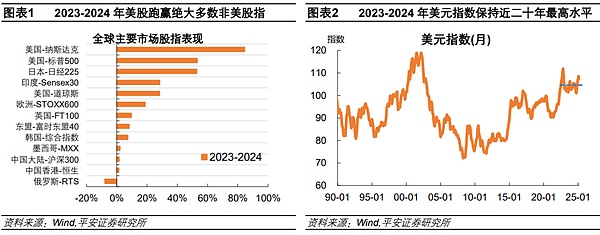

For investors, "American Exceptionalism" represents a type of view, that is, the economy of the United States, He US dollar assets have unique advantages, allowing them to continue to outperform other markets in the global cycle. This view was strengthened in 2023-2024. From 2023 to 2024, the US S&P 500 index and the Nasdaq Composite Index rose by 53.2% and 84.5% respectively, performing better than most non-US stock indexes. At the same time, the US dollar index rose from around 103 to around 108, an increase of about 5%, and the volatility center has remained at around 104 in the past two years, roughly at the highest level in nearly 20 years. Behind the outstanding performance of US dollar assets, the advantages of the US economy, technology development are indeed reflected.

The US economy maintains rapid growth above the pre-epidemic level, and "exceptionally" is immune to the scar effect after the epidemic. Since 2023, the global economy has basically digested the impact of the new crown epidemic and entered the "normal state"However, the US economy showed significant resilience and exceeded expectations in this stage, showing the characteristics of "superior success". From 2023 to 2024, the US real GDP maintained a rapid growth of 2.8-2.9% for two consecutive years, while the actual GDP growth of Europe and Japan was only around 1% during the same period. More importantly, the US economic growth rate in the past two years not only recovered rapidly, but even exceeded the average level (2.6%) in 2015-2019 before the epidemic. In contrast, the economic growth rate of Europe, Japan, emerging markets and developing economies is generally lower than the pre-epidemic level, showing varying degrees of "scar effect".

The US fiscal stimulus "exceptionally" breaks through traditional constraints and continues to become an important support for the economy. After the outbreak of the epidemic, the US fiscal strength far exceeded other countries, which was influenced by modern monetary theory (MMT) ideas, or the flexibility and autonomy given by the US dollar's international reserve currency status. According to IMF statistics, the scale of fiscal support for the US to deal with the impact of the new crown from 2020 to 2021 reached 25.5% of GDP, far exceeding the average level of 11.7% of developed economies, and 5.7% of the average level of emerging markets. Among them, the fiscal "spending money" to residents has formed over US$2 trillion in excess savings, and continued to support residents' consumption from 2022 to 2024. After 2022, most of the world will The fiscal deficit began to balance, but according to the IMF, as of 2024, the US deficit ratio still expanded by 3.7 percentage points to 7.6% compared with 2022, while the eurozone deficit ratio narrowed by 0.4 percentage points to 3.1% during the same period.

The Federal Reserve maintained high interest rates and effectively avoided the economic and financial risks caused by high interest rates. On the premise that the US economy maintains resilience, the US currency Maintaining higher interest rates than other regions, the higher returns of US dollar assets have attracted global capital inflows. Moreover, the market was worried that high interest rates may trigger an economic recession, which is reflected in the alarm issued by the deep inversion of US bond interest rates. However, the damage to the US economy by high interest rates has not been shown. One of the reasons is that the United States effectively blocked the financial risks caused by high interest rates. Faced with the regional banking crisis in March 2023, the Federal Reserve and the Treasury Department rescued banks as soon as possible, and the Federal Reserve temporarily expanded its balance sheet by about 400 billion US dollars, which quickly restored the financial market to stability. Judging from the Chicago Fed Financial Condition Index, since the regional banking crisis, the US financial system has actually tended to be loose.

The United States' leading in the field of technology isThe new round of artificial intelligence (AI) development has become prominent and catalyzed the strong performance of US stocks. Since the launch of ChatGPT in November 2022, the rapid breakthrough and wide application of AI technology have undoubtedly been the key driving force for the strengthening of US stocks. In our report "Analysis of the Three Major Risks of US Stocks: Valuation, Concentration, and Macro", we discussed in detail the causes of high concentration of US stocks. Benefiting from AI themes and excellent profit-making ability, while the market value of leading U.S. stock companies has also increased, their share in global stock markets is also increasing. According to Goldman Sachs statistics, the market value of the top ten companies in the United States in 2024 has exceeded 20% of the world's global market value, setting a record high since the 1970s. This round of US stock technology wave is inseparable from the United States' continued investment in technology research and development, especially in the field of AI. According to OECD data, from 2021 to 2023, the United States invested about US$200 billion in venture capital (VC) in the field of AI, far exceeding other regions, with less than US$100 billion in the same period, while Europe was less than US$50 billion.

Trump's election once strengthened the "American exceptionalism", which made investors more confident in the US economy and dollar assets. Trump's logic of "America First" is believed to be able to further support economic growth through tax cuts, deregulation, etc., while tariffs and trade protection may further enhance the competitiveness of American companies, attract capital inflows, and form a "Trump cycle" similar to the "Reagan cycle" (refer to the report "From the "Reagan cycle" to the "Trump cycle": Unchange and Change"). During Trump's first term, the S&P 500's annualized yield was as high as 14.1%, ranking second in previous presidency since 1960, only Clinton. According to Ipsos' poll a month before the election, the public believes that Trump will surpass Biden Harris on all economic issues (including employment, inflation, stock performance, etc.).

2. The reversal of "American Exceptionism"

From January to February 2025, US stocks underperformed Hong Kong and European stocks, the US dollar index fell back, and the capital market seemed to have traded "US dollar exception theory" ineffective. Since the beginning of this year (as of February 28), the S&P 500 index of the U.S. stock market has only risen by 1.2%, while the Nasdaq has turned 2.4%. At the same time, stock indexes in Europe and other regions performed well, among which the Hang Seng Technology Index and the European STOXX600 Index rose by 24.6% and 10.4% respectively. The dollar exchange rate has also been under certain pressure. Since February (as of the 25th), the dollar index has fallen from above 108 to the year-on-year low of 106.3, a drop of 2%. During the same period, the euro, yen and pound sterling have been against the United States.The yuan rose 1.6%, 5.5% and 1.2% respectively.

First of all, the most intuitive signal is that the US economic data has unexpectedly weakened and concerns about stagflation have risen sharply. Economic data such as US retail sales (-0.9% month-on-month, expected -0.2%), Markit service industry PMI (49.7, expected 53), existing home sales (annualized 4.08 million, expected 4.12 million) released since February are almost unremarkable. The US Citigroup Economic Accident Index has been declining since late January this year and has turned negative after mid-February, which means that the recent economic data performance has been the most disappointing stage since Trump was elected. At the same time, the latest inflation data are generally higher than expected, such as the US core CPI (0.4% month-on-month, expected 0.3%) in January, core PPI (3.6% year-on-year, expected 3.3%), etc. As of February 28, the GDPNow model forecast showed that the US GDP turned negative to -1.5% in the first quarter of 2025. If GDP increased negatively this quarter on a negative month-on-month basis, this will be the first time since the first quarter of 2022 (the outbreak of the Russian-Ukrainian conflict).

Secondly, Trump's tariffs amplify economic uncertainty and aggravate concerns about stagflation. Recently, the U.S. Economic Uncertainty Index (EPU) has risen sharply to its highest level since the COVID-19 pandemic, and is significantly higher than Trump's first term from 2016 to 2019. On the one hand, the intensity and rhythm of tariffs have been repeated. The tariffs announced in the early days of Trump's office did not exceed expectations, such as the initial imposition of 10% tariffs on China rather than the 50-60% promised during the campaign; and there is room for negotiation and maneuver, such as the first batch of tariffs on Canada and Mexico postponed. However, in the near future, negotiations between the United States and trading partners seem to have made limited progress. Trump threatened to implement tariffs on Canada and Mexico as scheduled on March 4, and threatened to further impose 25% tariffs on the EU, and increase additional tariffs on China from 10% to 20%. On the other hand, tariffs strengthen the risk of stagflation. According to the latest estimates of PIIE, Trump's imposition of 25% tariffs on Canada and Mexico and 10% tariffs on China (no countermeasures are considered), may weaken US GDP growth by about 0.3 percentage points in the next few years and push up US inflation by 0.5 percentage points in 2025. Michigan survey showed that inflation expectations for U.S. residents rose significantly, while consumer confidence dropped significantly, highlighting the impact of tariffs on stagflation expectations.

Again, Trump's aggressive actions in streamlining institutions have hindered Congressional budget negotiations and also implicitlyEconomic downturn risk. The "Efficiency Department" (DOGE) led by Musk has taken action vigorously in the past month, including large-scale staff cuts, "invalid spending", and suspension of foreign aid. As of February 21, DOGE's official website announced that since Trump took office, the department has helped save $55 billion in federal spending, and more than 200,000 federal employees have been fired. On the one hand, these actions increase the difficulty and risk of closing the Congressional budget negotiations. The short-term spending bill passed in December 2024 will expire on March 14, 2025. If the U.S. Congress cannot pass a new appropriation bill or reach a budget agreement, the U.S. will be shut down. Currently, the Democrats are opposed to Trump's radical cuts in institutions and projects, making it more difficult for Congress to negotiate. On the other hand, sudden reductions in spending and employees may threaten the resilience of the U.S. economy and jobs. In recent years, the direct pull of US spending on GDP growth has increased significantly, and the sector's contribution to US employment growth has increased significantly. From 2023 to 2024, the contribution of US spending to GDP by about 0.6 percentage points year-on-year, 0.4 percentage points higher than the average from 2015 to 2019. In the past year (as of January 2025), the average monthly increase in non-farm employment in the U.S. sector was 36,000, twice that in 2019. Finally, the issue of spending cuts and tariff imposition is closely linked to future tax cuts, reflecting the deep-seated contradiction that the U.S. fiscal difficulty in balancing. From 2018 to 2019, Trump's tariffs did not have a significant impact on the US economy and US stocks, mainly due to the implementation of the 2017 tax cut bill. But this round of situations are different. The pressure on fiscal balance in the United States has risen sharply. Trump tries to "open source" through tariffs, plus "save expenditure" through spending, creating space for subsequent tax cuts. However, at present, there is great uncertainty in the scale of tariffs and expenditure reductions, which makes the space for subsequent tax cuts less certain. Once tax cuts are blocked, the "Trump cycle" may be discounted or ended early, and the US stock market and the US dollar will also lose their original support.

Look deeper, the U.S. fiscal policy may face a major turn during Trump's term. In fact, the fiscal outlook for the United States is full of uncertainty. On the one hand, Trump's push for tax cuts will inevitably bring pressure on income reduction and deficit expansion. According to Tax Foundation, Trump's tax cuts are expected to increase the deficit by about 700 billion yuan each year from 2026 to 2029. Radical tariffs (20% global tariff + 50% tariff on China) bring in revenue of US$330-380 billion per year, which will eventually trigger an annual deficit growth of more than US$300 billion and an annual deficit ratio rises by about 1 percentage point. On the other hand, Trump's new Treasury Secretary elected to 2028The budget deficit ratio will be reduced to the target of 3% in the year. The latest forecast from CBO in January 2025 shows that the US deficit ratio is expected to be 5.2-6.2% from 2025 to 2028, which is significantly higher than Becente's target. Regardless of whether Becente can successfully achieve the goal of deficit ratio decline, it can be considered at least that the path to fiscal balance in the United States is very difficult, and the difficulty of implementing the US expansionary fiscal in the future may be higher than expected, which will conceal the US economic prospects.

In addition, DeepSeek breaks through the US technology monopoly expectations and catalyzes the adjustment of US stocks. Since DeepSeek became popular on January 27 (as of February 28), Chinese and American technology stocks have performed sharply, with the Hang Seng Technology Index rising by about 20% (highest increase of 28%), and the Nasdaq Index falling by about 6%. The rapid development of AI technology has shortened the technological gap between the world and the United States. Investors have begun to suspect that the high investment in the AI field and the containment of competitors in the United States may not necessarily allow American companies to maintain global leadership and monopoly. As the US RAND commented, the DeepSeek-R1 (DS) model quickly ranks among the world's top language models, fundamentally representing the failure of the United States' efforts to curb AI progress, especially by limiting chip sales. In addition, Europe may also benefit from the reshaping of this competitive landscape. Since January 27 (as of February 28), Germany's TecDAX technology index has risen 3% (highest increase of 6%). Articles from the Center for Strategic Research in the United States (CSIS) pointed out that the success of DS may inspire and guide European AI startups. European companies can learn from similar models and develop similar miniaturization and low-cost models, combining European companies' advantages in privacy, security and regulatory compliance to develop AI products and services that are more competitive than American companies.

3. There is still room for global asset re-allocation

The recent rapid reversal of the "American Exceptionism" reflects the risk of excessive concentration of global funds on US dollar assets in the past two years or even longer. Since Trump took office, the economic uncertainty of the United States has risen sharply, and the direction of the United States may not be as strong as expected. The difficulty of US fiscal balance and the negative effects that may have on the economy in the pursuit of balance deserve further attention. The pattern of Sino-US and global economic and trade, science and technology and geopolitical games has also undergone important changes. Under these changes, investors may re-examine the long-term narrative of "US exception", which is currently difficult to falsify, and adjust their regional allocation strategies. This process may be difficult to "get it in one step", and it is even moreIt can take a long process.

We believe that at least from the perspective of global stock market performance, there is still a lot of room for global asset re-allocation. Since 2025, the stock market (especially Hong Kong stocks), European stocks and others have outperformed the US stock market, but they are far from making up for the huge gap between the performance of the US stock market since 2020 (the impact of the new crown). Since 2020 (as of February 28, 2025), the U.S. Nasdaq Index and the S&P 500 Index have still risen by 113% and 84%, the European STOXX600 Index has risen by 35%, the Hang Seng Technology Index has only risen by 26%, and the Shanghai and Shenzhen 300 Index and the Hang Seng Index have fallen by 3% and 16%.

From the valuation point of view, taking the Chinese and US stock markets as an example, as of February 28 this year, the ratio of the Shanghai and Shenzhen 300 Index to the S&P 500 Index PE was only 0.46, lower than the average level of 2015-2019. At the same time, the PE of the Hang Seng Technology Index is only about 23-25 times, which is significantly lower than the Nasdaq Index by 34-37 times; it should be noted that for most of the time from 2021 to 2022, the former's valuation was significantly higher than the latter, and at its highest was twice that of the latter. Considering that the gap between AI and technology development between China and the United States is not significant, and the market's growth potential, the valuations of high-quality companies in A-shares and Hong Kong stocks still have a lot of room for growth compared with US stocks.

Risk warning: Trump's fiscal expansion exceeded expectations, the Fed's interest rate cut exceeded expectations, the United States' economic and trade restrictions on non-US regions exceeded expectations, etc.