19 mins ago

5,787

Author: XinGPT; Source: SevenUp DAO

TLDR: Let's talk about the conclusion first: It is possible in theory, but it is very small in reality

The leverage ratio is not high, the debt maturity is long, and there is no obvious debt repayment pressure in the short term

The premise of a financial crisis is that the value of Bitcoin is at an extremely low level for a long time, and the probability of occurrence is low;

Founder Michael Saylor has 46.8% voting rights, which can avoid the early redemption clauses in preferred stock debts and firmly grasp the company's operating direction

1. MicroStrategy's Bitcoin holdings and strategies

MicroStrategy has transformed from a traditional software company to the world's largest Bitcoin holding company. As of the end of 2024, the company held a total of about 471,107 Bitcoins. The total cost of these Bitcoins is about $27.97 billion, with an average purchase cost of about $62,500 per coin, while the market value of these Bitcoins is about $41.79 billion by the end of 2024.

MicroStrategy's Bitcoin investment is achieved through bond issuance and additional stock issuance. Its management (represented by co-founder Michael Saylor) regards Bitcoin as the company's main reserve asset, constantly buying more Bitcoin through external financing rather than relying on the cash flow of its own business.

MicroStrategy mainly raises funds to purchase Bitcoin through four channels:

using its own funds to purchase

is not the main source of funds. MicroStrategy uses no more than 500 million funds to purchase Bitcoin.

Issuing convertible seniorNotes

In order to buy more Bitcoin, MicroStrategies began to use the issuance of convertible bonds to raise funds to buy coins.

Convertible priority bonds are financial instruments that allow investors to convert bonds into corporate stocks under certain conditions. This type of bond is characterized by low interest rates, even zero, and setting conversion prices higher than the current stock price. Investors are willing to buy such bonds mainly because they provide downside protection (i.e., the principal and interest that the bonds can recover when they mature) and potential returns when the stock price rises. The interest rates of several convertible bonds issued by micro-strategy are mostly between 0% and 0.75%, indicating that investors are actually confident that the stock price of MSTR is rising and hope to convert bonds into stocks to earn more profits.

Issuing SeniorSecured Notes

In addition to convertible priority bonds, MicroStrategy has also issued a priority bond of $489 million with an interest rate of 6.125% due in 2028.

Prior-secured bonds are collateralized bonds with lower risk than convertible priority bonds, but these bonds only have fixed interest returns. The batch of priority bonds issued by MicroStrategy have chosen to repay in advance.

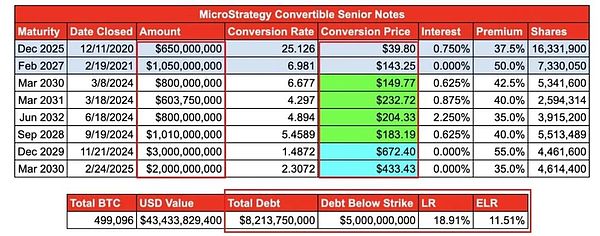

The following figure shows the current debt situation of the current MicroStrategy:

At-the-Market Equityofferings

MicroStrategies issue additional stocks to purchase Bitcoin, without debt, but issuing stocks dilute existing shareholders' equity. The reason why the existing shareholders agree to this additional issuance method is that MicroStrategies proposes a new indicator, BTC Yield, That is, the earnings per share are the ratio of Bitcoin holdings to the total diluted share capital. In other words, during the rising market, by issuing additional stock financing to purchase Bitcoin, although the proportion of shares held by users has decreased, the content of Bitcoin per share has increased. Overall, the amount of Bitcoin held by users may also increase.

For example, the BTC Yield of MicroStrategy in 2024 is 74%, which means that the number of Bitcoin per share increases by 74%, while the current BTC Yield in 2025 is 6.9%, with the goal of reaching 15% by the end of the year

2. Short-term impact of the decline in Bitcoin price vs. Long-term impact

1. Short-term impact:

Declining Bitcoin price will directly affect MicroStrategy's financial performance. Accounting rules require companies to make impairment losses when the price falls, but they cannot directly reflect returns when the price rises.

For example, when Bitcoin plummeted in 2022, the company made a provision of $197 million in impairment losses in the fourth quarter, resulting in quarterly losses. When Bitcoin rebounded in 2023, the company reduced its impairment losses due to accounting treatment, and even made profits at one point.

At present, the company does not have a Bitcoin pledge loan, so the fluctuations in the short term will not cause the risk of margin addition. However, the stock price is highly correlated with Bitcoin. The decline in Bitcoin often causes the share price of MicroStrategy to fall simultaneously, which in turn affects the company's financing ability.

2. Long-term impact:

2. Long-term impact:

If Bitcoin enters a long-term bear market, the company may face serious financing pressure. MicroStrategy's software business is currently small, with revenue of only about $500 million in 2024 and is still losing money, so it cannot accumulate a large amount of cash through its own business to cover debts or continue to buy Bitcoin.

The company's current operating model is highly dependent on the capital market. If Bitcoin is sluggish for a long time, investors may reduce their financing support for MicroStrategy, or require higher financing costs.

If the price of Bitcoin is below the company's average purchase price for a long time, the book value of MicroStrategy's Bitcoin assets will continue to be lower than the actual cost, which may affect investor confidence and further increase the pressure on the stock price.

Because the company's management highly believes in the long-term value of Bitcoin, even if the financial situation isAs the situation worsens, companies are unlikely to take the initiative to sell Bitcoin, but will maintain operations through new debt or equity financing. But if financing is blocked, you may be forced to adjust your strategy.

3. Key financial data analysis

1. Bitcoin holdings and valuation:

As of the end of 2024, the book value of Bitcoin held by MicroStrategy was approximately US$23.9 billion (after impairment was set aside), but approximately US$41.79 billion was calculated based on market prices.

Due to the accounting standards adopted by the company, if the price of Bitcoin falls below $30,000, the company will have to make further impairments, which may exacerbate the stock price pressure.

2. Debt level: MicroStrategy's current total debt is approximately US$8.2 billion, mainly convertible bonds, with a low coupon, and even 0%.

Of course: Expired in December 2025: US$650 million, coupon interest of 0.75%. Expired in February 2027: US$1.05 billion, coupon rate 0%. Expired in December 2029: US$3 billion, coupon rate 0%.

The short-term debt risk is lower because some convertible bonds have conversion prices lower than current share prices, and these bonds are more likely to be converted into stocks rather than requiring cash payments. But if Bitcoin prices continue to be sluggish in the future and MicroStrategy's share price falls below the conversion price, bondholders may demand cash repayment, which will increase the company's cash flow pressure.

3. Cash flow and liquidity:

In 2024, the company's operating business had a net outflow of US$53 million, and it had only US$46.8 million in cash reserves, which means that MicroStrategy has almost no cash buffer.

At the end of 2024, the company raised US$15.1 billion through additional stock issuance, but if the stock price falls, the company's future financing capabilities may be affected.

In 2025, the company also issued an additional batch of preferred shares with a dividend yield of 10% (previously estimated 8%), indicating that the financing cost has begun to rise.

4. Profitability:

The company's own software business revenue growth has stagnated, with software revenue falling by 3% year-on-year in 2024, and the software business contributed only about US$500 million in the whole year.

The company relies on book returns brought by Bitcoin investment, but due to the impact of impairment rules, the financial report profit fluctuates greatly and cannot form a stable profit model.

In the future, if the price of Bitcoin does not continue to rise, the company may be in a loss-making state for a long time, further increasing financing pressure.

IV. Correlation between stock price and Bitcoin

In the past few years, the correlation between MicroStrategy's stock price and Bitcoin price reached 0.7~0.8, almost becoming a Bitcoin leveraged ETF.

At the end of 2024, Bitcoin hit a record high (nearly $100,000), and MicroStrategy's stock price soared to more than $500. But then Bitcoin pulled back, and the company's stock price plummeted by 50% in a short period of time.

The current market valuation of MicroStrategy is usually higher than its net value of Bitcoin, and some investors are willing to pay a premium to indirectly invest in Bitcoin through MSTR. But if the price of Bitcoin falls, this premium may disappear, and even trade below the net value.

V. The possibility of bankruptcy or financial crisis

left;">In the short term, MicroStrategy still has strong debt repayment ability, but if Bitcoin enters a long-term bear market, it may cause financial difficulties.

Asset vs. Liability Ratio: Currently publicThe company holds $41.79 billion in Bitcoin, far higher than $8.2 billion in debt, and has less short-term debt repayment pressure. But if the price of Bitcoin falls to 12,000 to 15,000 US dollars, the company's Bitcoin assets will be lower than the total debt, and technical bankruptcy may occur at this time.

Debt maturity risk: US$650 million in 2025 may be resolved through equity conversion, but more than US$4 billion in debt will expire from 2027 to 2029. If Bitcoin is still at a low level by then, MicroStrategy may have difficulty refinancing through additional shares or new debts that may require selling Bitcoin to repay debts.

Management Position: Michael Saylor controls 46.8% of the voting rights, which can prevent companies from selling Bitcoin or changing their strategies. But if the price of Bitcoin falls below a certain tipping point, the company may be forced to take urgent measures, including selling some of its Bitcoin, restructuring debts, and even considering bankruptcy protection.

As shown in the figure below, the convertible bond terms stipulate that a significant change has occurred in the company, and investors can ask the company to repay its debts 12-18 months in advance, but the definition of "significant change" mainly refers to the decision of the company's shareholders to liquidate. Most of the voting rights of the company's shareholders are in the hands of Michael Saylor

6. Conclusion:

MicroStrategy is still financially stable at present, but if the price of Bitcoin declines for a long-term and profound, its high leverage strategy may lead to serious financial pressure. The fate of a company depends entirely on the future trend of Bitcoin – if Bitcoin is sluggish for a long time, MicroStrategy may fall into a debt crisis or even go bankrupt; but if Bitcoin continues to rise, the company will maintain strong growth.