39 mins ago

6,814

Author: YettaS Source: X, @YettaSing

The biggest feeling of going to Consensus HK this time is that VC is too It's hard, and it's not an exaggeration to say that the miserable is everywhere, which is in a strong contrast with the Marshals P. Some VCs cannot raise the next round of funds, some VCs are half gone, some VCs switch to strategic investors and no longer invest independently, and some VCs even consider issuing Meme to raise funds...

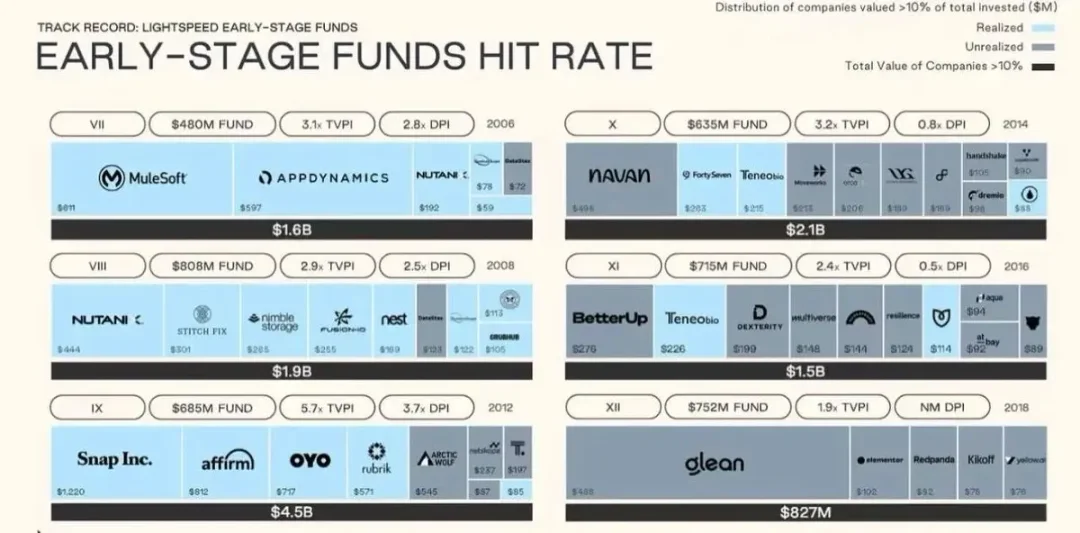

< p style="text-align: left;">Many VC peers have also chosen to leave, some join the project party, and some transform into KoL. It seems that these are more cost-effective choices. In the changing situation, everyone is looking for a new way to survive. And I am also thinking, what is wrong with VC? How to break the deadlock?First of all, we have to admit that both in China and the United States, VC as an investment asset class, the best times have passed. The figure below is the return data of several Lightspeed funds. The best fund invested in Snap, Affirm, and OYO in 2012 and achieved the return of DPI 3.7X (DPI is the multiple of allocated returns, and does not rely on valuation, and measures actual exit. Of course, the return on funds is incomparable to buying BTC directly, and even making a return on capital has become a problem since 2014.

VC has also gone through a similar trajectory. Relying on the demographic dividend, the mobile Internet and consumer Internet have grown rapidly, giving birth to hundreds of billions of enterprises such as Alibaba, Meituan, and Byte. 2015 was the last highlight moment. Subsequently, supervision became stricter, liquidity tightened, industry dividends declined, industrial cycle changes faced growth bottlenecks, and IPO exit channels were restricted, resulting in a sharp decline in the return rate of VC institutions and a large number of practitioners left the market.

Crypto VC is no exception. With the changes in the macro environment, the evolution of market structure and the decline in capital returns, VCs are facing huge survival dilemmas.

It's all about cost and liquidityIn the past, the value chain of VC investment was clearly visible: the project party carried innovative ideas, and VC provided strategic support and resources, KoL amplifies the market voice at critical moments and finally completes value discovery at CEX. We provide different values at different stages and bear different risks, which is the same asMatching returns, this is a "relatively fair" value chain.

For example, as VCs, the value we provide is never as simple as investing a sum of money in the early stage. How to help project parties connect with key resources in the ecosystem as soon as possible to promote business development, provide timely suggestions when market trends suddenly change, help project parties adjust their strategies, and even help build core teams. Moreover, in order to make a long-term binding with the project party, we will not talk about when we can TGE. Even after TGE, we will generally face a year of lockdown and 2-3 years of vesting. To a large extent, we all hope to be with the project party. Go and play a PVE non-zero sum game.

However, in the current market environment, the core contradiction lies in the extremely lack of liquidity, intensified market game, and the VC model is unsustainable.

Changes in capital flows: Where does VC's dilemma come from?The main driving force of this bull market is the strong entry of US Bitcoin spot ETFs and institutional investors. However, the transmission path of funds has undergone major changes:

Institutional funds mainly flow to BTC, BTC ETFs and even Index, but will never spread to the wider counterfeit market;

Lack of real technology/product innovation support, altcoins are difficult to maintain high valuations.

This directly causes the VC model to be highly FUD in the current market environment. Retail investors believe that VCs enjoy unfair advantages, can obtain chips at a lower cost, and grasp key market information. This information asymmetry leads to the collapse of market trust and further depletion of liquidity. In the PvP environment, retail investors require "absolute fairness". In contrast, the strategies of secondary funds will not have a strong opposition to market sentiment, because retail investors can also enter the market with the same chips, after all, they have given absolutely fair opportunities.

The current overwhelming Fud against VC is a counterattack from "absolute fairness" to "relative fairness" in the face of liquidity shortage.

The rise of Meme's financing modelIf I last regarded Meme as a cultural phenomenon, then this time, we need to regard it as a new financing method. The core value of this financing method lies in the

Participation mechanism: Retail investors can track information through on-chain data and obtain early chips under a relatively fair pricing mechanism;

Lower entry threshold: DeFi Summer During this period, we supported numerous solo devs who rely on product innovation to drive value capture. Now, the Meme model further lowers the threshold, allowing developers to "have assets first, then products."

This logic itself has no problem. Looking back, many public chains perform TGE without a mature ecosystem or main network. Why can’t Meme use the same method to attract enough attention first and then promote product development?

Essentially, the evolution of the path of "asset first, product later" is the sweeping of the entire financial ecology by the wave of populist capitalism. The prevalence of attention economy, catering to the public's desire to get rich quickly, breaking the monopoly of traditional financial institutions, moving down the capital threshold, and information openness and transparency are all unstoppable trends in the new era of populism. GameStop The evolution of fundraising methods from retail investors to Wall Street, from ICO to NFT to Meme, are all financial versions of the times.

So I say, Crypto is just a microcosm of this era.

VC's role in the new modelNo financing model is perfect . The biggest problem with this financing model is that the signal-to-noise ratio is extremely low, which brings unprecedented trust challenges -

The signal-to-noise ratio is extremely low: fair launch The cost of asset issuance is extremely low, and a large amount of garbage will fill it.

Insufficient information transparency: For high liquidity Meme projects, everyone in the market can enter early, which means whether the project has been built for a long time has become Not that important, what is important is how to make a profit in the game.

Soar in trust costs: high liquidity means high game. The first day of circulation means that we have no mechanism to bind interests with Founder to achieve long-term win-win results. Everyone will become opponents at any time and become each other's exit liquidity. This trust structure is dangerous and unsustainable.

I'm veryAgree with the differences in mindset written by @yuyue_chris:

People who play Meme think: narrative> chip structure~ community or emotion> product technology;

People who play Meme think: narrative> bargaining structure~ community or emotion> product technology; p>

Primary market believes: narrative> Product technology ~ chip structure> Community or emotions;

Meme Mode is essentially a darker on-chain world than VC mode. Due to the lack of product and technical support, "absolute fairness" is often just a cover. Look at Libra. Every carefully planned public favorable thing from the cabals behind the market ultimately makes us the targets of precise harvest. They can always predict your predictions, and in a highly game-oriented environment, the real long-term Builder becomes difficult to distinguish.

I don't think VC will disappear because the world is full of huge information asymmetry and trust asymmetry. For example, a cooperative resource like ARC cannot be one. A normal Dev can be obtained.

But in the face of such a wave of populist capitalism, it is absolutely unrealistic for VCs to simply use information asymmetry to make money while lying down as simple as in the past. It is never easy to adapt to change, especially when the market paradigm is completely reconstructed, and the effective methodologies in the past are quickly eliminated. The rise of Meme financing is not accidental, but the result of deeper liquidity changes and reshaping of trust mechanisms.

When Meme's high liquidity and short-term game thinking encounters the long-term support and value empowerment of VCs, how to find a balance between the two is Problems that VCs must face now. On the one hand, Primitive is very grateful that he has the freedom and flexibility to deal with market changes, but it is not easy to recognize structural changes and change his investment strategy.

But no matter how the market changes, there is one thing that remains unchanged-the one that really determines long-term value are those who have vision, have super execution ability, and are willing to continue Excellent founder of construction.