56 mins ago

6,746

Article source: ASXN; Translated by: Golden Finance xiaozou

It has been a week since the Unit protocol was launched, and Hyperliquid's daily net inflow of Bitcoin has continued to be positive. As of this writing, more than 500 BTCs have flowed in, worth approximately $50 million. It is expected that the holdings of BTC on Hyperliquid will exceed 1,000 by the end of the month. In this article, we will dig into all aspects of the Unit protocol and understand how Unit introduces these native assets into Hyperliquid.

1. PrefaceUnit is a protocol based on lock-and-mint cross-chain system, designed to support the issuance of non-native assets on the Hyperliquid chain. Its main function is to allow users to deposit and withdraw assets such as Bitcoin, Ethereum and Solana directly on Hyperliquid.

The architecture of this protocol is built around two core components: the Guardian Network and the Agent System. The Guardian Network consists of node operators distributed on each support blockchain, processing deposits and withdrawals through a leader-based consensus mechanism. The proxy component is responsible for implementing core protocol functions, managing the MPC TSS wallet, and distributing private key shards to multiple parties, thereby enhancing security by eliminating single point of failure.

Unit allows users to trade non-Hyperliquid native spot tokens through the lock-minting system. Users can deposit assets at a specified address generated by the Guardian Network, which will mint spot assets of equivalent value on the Hyperliquid chain after verifying the transaction.

Unit and Hyperliquid are symbiotic. Unit acts as a critical infrastructure that enables Hyperliquid to expand from perpetual futures trading to the spot market. This expansion is crucial because it enables Hyperliquid to provide a complete trading ecosystem where users can trade spot and derivatives simultaneously on a single platform.

So Unit is particularly important for Hyperliquid. According to an analysis of major centralized exchanges (discussed in detail below), spot trading volumes in major assets such as Bitcoin and Ethereum usually account for about 18% of perpetual futures trading volume. This suggests that Unit integration may significantly increase Hyperliquid's transaction volume. In addition, the ability to provide spot trading opens up new possibilities for complex trading strategies such as capital rate arbitrage and Delta neutral strategies.

The architecture of this protocol emphasizes security and reliability through multi-layer verification. Transactions are processed through deterministic state machines to ensure that results are predictable and auditable.

The consensus mechanism requires 2 of the 3 guardians to agree on key operations (currently), while MPCThe wallet system enhances security by distributing key management to multiple parties. These security measures are further enhanced by the use of encrypted communications between secure enclaves and network operators.

Essentially, Unit is crucial to the future development of Hyperliquid, enabling it to compete with centralized exchanges more effectively and efficiently while maintaining its advantages in decentralization and self-custody. Understanding Hyperliquid's framework is crucial to understanding how Unit can effectively integrate CLOB and EVM systems for spot asset issuance.

2. Overview of HyperliquidHyperliquid is a sustainable trading protocol based on its own L1, designed to replicate the user experience of a centralized exchange while providing a fully on-chain order book and a decentralized exchange. Trading spot, derivatives and pre-listed markets.

In May 2024, Hyperliquid announced plans to support native EVMs, enabling direct compatibility with Ethereum smart contracts, wallets and bridges. Although Hyperliquid runs its own network and the Rust-based virtual machine, Hyperliquid L1, the system specializes in handling sustainable transactions and lacks the programmability and versatility of the EVM.

EVM integration will establish symbiotic relationships between these systems. Hyperliquid will run two different virtual machines on a consensus layer HyperBFT. Hyperliquid L1 will continue to manage core transaction features, including perpetual and spot order books, while EVM will serve as a standalone layer for auxiliary applications that prioritize flexibility over performance.

The enhanced EVM will be integrated with native Hyperliquid L1 components including HIP-1 assets, spot trading, perpetual trading and DeFi primitives to enable seamless value transfer between atomic composition and environment.

With the launch of EVM, Hyperliquid will be expanded into a more general chain, requiring strong cross-chain capabilities to support transactions, custody, lending and DeFi applications of non-native assets. The diversification pool of high-liquidity assets such as BTC, SOL and ETH is crucial to DeFi capabilities. Unit meets this need by allowing users and institutions to cross-chain non-native assets to Hyperliquid EVM for DeFi integration and transactions.

In order to build a sustainable DEX (decentralized exchange) that can match the speed and user experience of CEX (centralized exchange), Hyperliquid designed a high-performance Layer 1 blockchain from scratch. The L1 uses a Proof of Stake (PoS) model combined with Hyperliquid's proprietary HyperBFT consensus algorithm to provide low latency and high throughput. Several core components of the L1 architecture are crucial to implementing CEX-level UI/UX, speed, and transaction throughput.

The perpetual platform has achieved widespread success with trading volumes from 360,000 traders exceeding $888 billion. In recent weeks, the platform's average daily trading volume exceeded US$1.45 billion, accounting for 70% of DeFi derivatives trading volume. Creating a new perpetual market on Hyperliquid L1 is very simple, and the only prerequisite is the ability to reference the appropriate oracle price source to keep the perpetual futures consistent with the index price. This allows Hyperliquid to act at an extremely fast speed when adding a sustainable market to its platform. However, the non-native spot market on Hyperliquid presents entirely new challenges involving a large number of security and user experience considerations. Unit aims to solve these problems.

3. Hyperliquid protocol mechanismBefore exploring the design and trends in the CEX field, we first need to understand the core components of Hyperliquid and how they operate in the sustainable and native spot markets:

(1) Order Book and Clearing Center

L1 status includes margin and matching engine data to ensure the complete transparency of the exchange. A key feature of Hyperliquid is that the L1 state also maintains an order book for each asset, which operates in a similar way to the order book on a centralized exchange, where orders are matched based on price-time priority.

The order book interacts with the clearing center, which manages all positions and margin verifications. When a new order is placed, margin verification will be conducted, and the margin of the slapped party will be checked again when the order matches, ensuring that the margin system can remain consistent even after the oracle price fluctuates after the order is placed.

The deposit is initially counted into the cross margin balance of the address, and by default, the position is opened in the cross margin mode. However, segregated margins are also available, allowing users to allocate specific margins to a single position, thereby reducing the liquidation risk of that position without affecting other positions. Likewise, the Spot Clearing Center manages the spot user status at each address, including token balances and any freezes.

(2) Oracle pricing

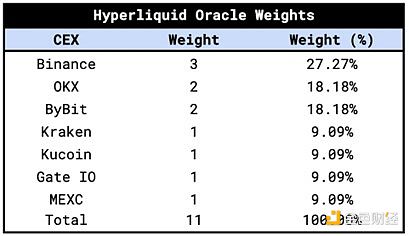

Hyperliquid uses custom built oracles as part of the chain consensus to ensure that the exchange's price is also Accurate. The validator updates the spot oracle price every 3 seconds, which are used to calculate the capital interest rate and mark price. Marking prices are essential for margin calculations, liquidation and triggering take-profit/stop-loss orders, and it is determined by combining oracle prices with the 150-second exponential moving average (EMA) of the difference between Hyperliquid mid-price and oracle prices. . To ensure accuracy, oracle prices are based on the weighted median spot prices of major exchanges including Binance, OKX, Kraken, Bybit, and Kucoin. The final oracle price is further optimized by staking weights of the verifier.

This system provides an unbiased and hasElastic price estimates, independent of Hyperliquid's internal market. In the event of extreme volatility or interruption of CEX data, the price protection mechanism is activated, relying on the median of the best bid, best offer and final trading price until normal conditions are restored.

(3) Maintenance Margin

Users can set leverage to any integer between 1 and the maximum asset leverage (3 times-50 times). The margin required to open a position is calculated as position size * Mark price / leverage.

For cross margin positions, the initial margin is locked and cannot be withdrawn, while the isolation position allows adjustment of margin after opening the position. The unrealized profit and loss of cross margin positions automatically contributes to the margin of the new position, while for isolated positions, the unrealized profit and loss increase the margin of the existing position. Users can increase leverage without closing positions, but leverage is only checked when opening positions.

If the unrealized profit and loss of a position is negative, possible operations include partial or complete closing of positions, increasing margin (for isolated positions), or depositing into USDC (for cross margin positions).

(4) Clearing

The liquidation of Hyperliquid is based on the marked price, which integrates the external CEX price and the order book status of Hyperliquid. This approach ensures clearing is more reliable and less susceptible to manipulation than relying solely on a single instantaneous order book price.

When a trader's position is unfavorable to it, resulting in an account equity below the maintenance margin, a liquidation event will be triggered.

4. Native Spot MarketOn April 16, the Hyperliquid team expanded its ecosystem to include native spot assets and its perpetual order book. HIP-1: Hyperliquid spot deployment creates native token standards on L1, similar to the ERC20 standard on Ethereum. HIP-1 allows deployment of limit-provisioned interchangeable tokens, as well as native on-chain order books. The first token introduced using this standard is PURR, a cat-themed meme coin deployed by the Hyperliquid team.

The token is deployed on the chain, and there are 5 steps in total, requiring the deployer to make 5 transactions on L1. These transactions will specify the following:

• Name: Human readable, up to 6 characters, no unique constraints.

• weiDecimals: The conversion rate from the minimum integer unit of the token to the human interpretable floating point number. For example, weiDecimals for ETH on the EVM network = 18, and weiDecimals for BTC on the Bitcoin network = 8.

• szDecimals: The minimum number of tradable decimal places on the spot order book. In other words, the token batch size on all spot order books will be 10 ** (weiDecimals - szDecimals). Requires szDecimals + 5 <= weiDecimals.

• Maximum Supply: Maximum and initial supply. Supply volumes may decrease over time due to spot order book fees or future destruction mechanisms.

• initialWei: Optional Genesis Balance specified by the transaction sender. This may include multi-signature vaults, initial cross-chain casting, etc.

• anchorTokenWei: The transaction sender can specify an existing HIP-1 token to receive the Genesis balance in proportion.

• hyperliquidityInit: Hyperliquidity parameter used to initialize USDC spot pairs. See the HIP-2 section for more details.

The user can transfer USDC from the perpetual sub-account to their spot account to trade any HIP-1 assets. All spot markets are traded with USDC and since they are native spot tokens, they are stored on Hyperliquid L1.

These spot markets performed very well after the HYPE token generation event (TGE), both in terms of returns and trading volume. Since its launch, the average daily trading volume of the HYPE/USDC pair has been $240.3 million, incurring considerable fees for the platform and permanently destroying HYPE.

However, currently, the spot assets that can be tradable on Hyperliquid are very limited, and only tokens launched through the auction mechanism and deployed directly to Hyperliquid L1 can be traded. Looking at the spot ecosystem, we found that HYPE currently accounts for 90.3% of the total circulating market value of trading tokens, accounting for more than 85% of the daily trading volume.

In order for the Hyperliquid spot market to accelerate growth, it is necessary to be able to trade non-native assets such as Bitcoin, Ethereum and Solana on exchanges. This will greatly increase the volume of spot transactions processed by Hyperliquid and provide users with a decentralized, self-custodial way to trade core crypto assets while providing traders with interesting unlocks across collateral and margin utilization.

5. CEX Industry OverviewAs we all know, in the traditional stock market, derivative trading volume usually far exceeds the spot market trading volume. Derivatives provide leverage for traders, allowing them to control greater exposure with smaller capital, while also providing speculative and hedging tools that require less upfront investment and greater flexibility, such as shorting and Combining complex strategies. When we look at the US market (such as NYSE, CME), the derivative trading volume may be 10-20 times the trading volume of the spot market.

This fact also applies in the crypto space, and we see average trading volumes for perpetual futuresIt is 3.69 times the spot trading volume. However, the spot market is very important for the following reasons:

• Price Discovery- Spot price is the benchmark for all derivative products, including futures, options and perpetual swaps. Spot prices are used to calculate index prices to ensure that perpetual futures and other derivatives are consistent with actual market value.

• Liquidity- They enhance liquidity, which is crucial for price stability and efficient market operation.

• Settlement- Many derivative contracts (such as futures delivered in physical form) require actual delivery of Bitcoin, which is done through the spot market.

• Hedging/arbitrage-- Traders use the spot market to hedge the risk of derivative positions and minimize exposure to price fluctuations. Arbitrageurs rely on price differences between spot and derivatives markets to maintain market efficiency.

• DeFi-- A spot order book with non-native primary crypto assets will enable seamless interaction with HyperEVM for collateral lending projects or Ethena-style decentralized stablecoins, etc.

• Long-term Holding-- The spot market is crucial for long-term investors who prefer to hold actual Bitcoin as a store of value rather than speculating positions in derivatives.

• Capital Efficiency--Using cross-collateral and introducing currency-priced margins will enable traders and market makers to achieve significantly higher capital efficiency.

• Real oracle pricing-- Binance is currently the benchmark for the “fair price” of most crypto assets (especially major assets), thanks to its deep liquidity and market makers in the market dominance in. Therefore, Binance pricing plays a crucial role in ensuring efficiency across exchange markets. Price discovery has been made primarily on Binance. However, this is the first opportunity to move fair pricing and price discovery to a fully decentralized exchange.

We can now explore how Unit introduces these native assets into Hyperliquid, understanding the protocol mechanism and user workflow.

6. Protocol mechanism(1) Asset issuance and bridging

Usually, when we consider cross-chain and cross-network bridging, we will think of two different types of bridging. The first type involves the issuance of non-native assets, where users or institutions issue assets on non-native chains. This process introduces new non-native assets, requiring underwriters to manage risks and handle asset custody by locking/destructing on the source chain and issuing/mining on the target chain. Common implementations include:

• Lock-and-mint systems: Assets are locked in smart contracts on the native chain and cast on the target chain.

• Burn-and-mint systems: Assets are destroyed on the native chain and cast on the target chain. This approach usually requires new tokens or asset standards.

The second category is bridge based on intents, which functions more like cross-chain transactions, where users sell assets on one chain and buy assets on another chain.

Unit allows users to deposit and withdraw non-native spot assets to Hyperliquid through a lock-casting-based system. Deposits and withdrawals are processed by the Guardian/Agent network.

(2) Transaction Process

When a user deposits non-native spot assets into Hyperliquid through Unit, the Guardian Network generates or allocates a deposit address. For example, for SOL deposits, the Guardian Network creates or provides an existing SOL deposit address on the Solana blockchain. Each deposit address generated by the Guardian network is permanently and uniquely bound to a specific Hyperliquid address. Any future transfers to this deposit address will always be credited to the same destination address on Hyperliquid.

The user transfers his spot assets to the designated deposit address. Once the transaction is completed, the Guardian Network mints an equivalent native asset on the Hyperliquid chain and transfers it to the user's wallet. This transfer transaction requires verification by the Hyperliquid network. Importantly, Unit does not collect income from deposits or withdrawals. The only fee associated with the operation is the fee required to process transactions on their respective native networks.

For withdrawals, the process is the same as deposits, except that the Guardian Network creates a withdrawal address, and the user specifies a target address to receive the assets it withdraws.

The following is an example of a user depositing and withdrawing native SOL to/from Hyperliquid:

Deposit:

1. Address Generation: Guardian Network Generation Or assign a dedicated SOL deposit address and provide it to the user.

2. Transfer: The user sends SOL from his external wallet to the provided deposit address.

3. Verification: The Guardian network monitors the transaction until it is completed.

4) Settlement: Guardian Network signs spot transfers of deposit amounts, Hyperliquid Network verifies transactions, and credits the equivalent native SOL to the user's Hyperliquid wallet.

Withdrawal:

1. Target Address Settings: The user provides his external SOL target address to which the withdrawn funds will be sent.

2. Address Generation: The Guardian Network generates a Hyperliquid withdrawal address and provides it to the user.

3. Transfer: The user sends his Hyperliquid SOL to the provided withdrawal address.

4. Verification: The Guardian Network monitors the Hyperliquid transaction until it is completed.

5) Settlement: Guardian Network signs and broadcasts SOL transactions to Solana Network, Funding NotesEnter the destination address specified by the user.

Unit consists of two core components:

• Guardian Network: The network of operators running nodes on each chain, processing deposits through Unit and withdrawals.

• Agent: Core protocol implementation, including basic logic and MPC TSS wallet, distributes private key shards to multiple parties instead of using a single private key.

This protocol relies on nodes and indexers to verify transaction inclusions, as well as a compliance layer.

(3) Guardian Network

Guardian Network is a distributed operator network that runs nodes on each chain and processes deposits and withdrawals through Unit. These operators also run a proxy that implements core Unit protocol functionality.

The Guardian Network operates through a leader-based consensus mechanism. The designated leader coordinates the Guardian and performs the state transition function to manage the transaction process, while the other Guardians act as validators. These Verifier Guardians (Followers) monitor signature requests from leaders, verify them independently, and return signatures to leaders.

All Guardians must run nodes and indexers on every chain that supports Unit deposits and withdrawals. Leaders have additional responsibility, including running a relay server to coordinate MPC operations with other guardians (verifiers/followers).

The relay server acts as a messaging mechanism only and does not introduce additional encryption assumptions or security risks. Importantly, there is no key material on the relay server, and even if it is compromised, it will not affect the security of the private key or signature operation.

In addition, the guardian jointly maintains the circuit breaker policy and can automatically pause the operation if suspicious or malicious activity is detected. This emergency protection allows the network to stop processing before resolving security issues, providing an additional layer of protection to prevent attacks.

(4) Agent

Agent is a core protocol implementation, including basic logic and MPC TSS wallets, distributes private key shards to multiple parties, rather than using a single private key.

Each guardian must run an independent proxy instance that participates in 2/3 of the MPC settings. This setting will be expanded in the future.

Agent instance consists of four key components:

• Chain Service

• Process Manager

• Consensus Service

• Wallet Manager

(5) Chain Service

Channel Service provides chain-specific interfaces for monitoring and tracking network activities and transaction management. Through these interfaces, the Guardian can track user deposits and related transactions, verify when the transaction is completed, confirm the necessary transaction verification, and manage transaction construction, signature and broadcast on their respective blockchains.

(6) Process Manager

The process manager uses a deterministic state machine to transfer cross-chain assets. The deterministic state machine in this context refers to the system only at a timeOne state, and each state transition is completely predictable based on the current state and input. They allow the protocol to ensure that each transfer follows a predetermined path.

For example, when/if BTC is transferred to HYPE, the transfer can only be in one state at a time (such as AWAITING_DEPOSIT, CONFIRMING_BITCOIN, or MINTING_HYPE), when a Bitcoin deposit address is detected in the AWAITING_DEPOSIT state, it will Always predictably switch to the CONFIRMING_BITCOIN state to wait for network acknowledgment. Especially for Bitcoin deposits, the protocol requires two block confirmations on the Bitcoin network before the transaction is considered to be completed and the settlement process continues.

The system implements strict audit measures, all state transitions are stored and recorded, creating a comprehensive audit trail for increased transparency. The chain-specific verification process ensures the finality of cross-chain transactions through each specialized verification mechanism that supports blockchain.

Process Manager validates transactions (by checking deposit and withdrawal addresses and transaction/payload parameters), ensuring the correct transaction sequence, coordinating with consensus services and monitoring asset transfers.

(7) Consensus Service

Consensus Service ensures that the Guardians reach consensus on protocol operations, deposits and withdrawals, and enables the agreement to be synchronized between the Guardians. It adopts a leader-based model where the leader must complete the transaction process while the other guardians act as validators/followers. There will be a single leader initially – the final agreement will implement the leader election process. In addition, consensus services require two-thirds of the guardians to reach a consensus on critical network operations.

This protocol adopts rate-limited endpoints to prevent denial of service attacks and includes circuit breakers that can stop operations when the guardian is threatened.

(8) Wallet Manager The wallet manager generates a key through MPC settings and adopts a threshold signature scheme, and neither party can access the complete private key. Instead of using a single private key, the system splits the private key into multiple parts and spreads it on different parties or devices. In addition to storing and generating keys, the MPC settings allow the guardian to sign transactions and manage cross-chain addresses. MPC settings are executed in secure enclaves—particularly AWS Nitro Enclave.

MPC operations are performed in safe enclaves to enhance runtime security. Secret sharing uses native KMS ("Key Management Service") functionality for encrypted storage, while all communications between network operators are protected through end-to-end encryption channels.

7. The future of Hyperliquid spotIntroducing native spot assets in a way that requires no trust and decentralization is the evolution of on-chain transactions and the ultimate goal of crypto trading. Unit will enable any user around the world to buy and sell native crypto assets while enjoying the excellent user experience brought by self-hosted and Hyperliquid high-performance order book. To quote Satoshi Nakamoto: "I think this is our first attempt at a decentralized, untrustworthy system," I would like to add that its user experience is comparable to that of a centralized competitor.

(1) How to truly unify the single-site trading experience in spot trading? The trading venues that provide spot and derivatives markets provide a more unified trading experience that can improve capital efficiency (support cross margin), risk and order management, and trading opportunities (especially basis trading and capital rate arbitrage):

1) Position and order management have a single source of position, meaning that users do not have to reconcile positions between multiple exchanges. Complex order types are easier to manage, orders are easier to cancel, modify and manage, and traders experience lower latency by not having to deal with multiple exchanges.

In addition, traders simply need to learn and integrate an API, which simplifies order management, key management and further reduces complexity.

2) Capital Efficiency and Cross Margin Users can use their spot positions as collateral for futures positions to reduce the total capital required and improve capital efficiency. In an EVM environment, this can also allow users/traders to earn profits while holding spot positions as collateral – and allow traders to gain futures exposure without having to sell.

The exchange usually considers the entire portfolio (spot + futures) when calculating margin requirements, where long spot positions can offset short futures positions in margin calculations. This reduces the total collateral required compared to having a separate account on different exchanges.

3) Arbitrage Opportunities With two markets on a platform, users can more effectively utilize the price differences between spot and futures markets, reduce transaction costs, and eliminate the need to transfer funds between exchanges.

For basis trading, when a price difference occurs, traders can quickly execute the two legs of the transaction on a single exchange without transferring funds between platforms. Furthermore, the lower transaction costs of trading on an exchange make it profitable to capture smaller spreads.

For capital rate arbitrage, including cash and arbitrage trading, traders can maintain spot positions while shorting perpetual futures, allowing them to collect funds while keeping Delta neutral. Having two positions on the same exchange significantly simplifies position management and monitoring.

Marking becomes more effective when operating both spot and futures markets on an exchange. Traders can provide liquidity in both markets while conducting real-time arbitrage between order books. A unified inventory view makes position management more efficient, and spot positions can be used as support for futures market making activities.

When trading spot and futures at one exchange, instantaneous arbitrage opportunities can be more efficiently captured. Traders can quickly deal with short-term price misalignment between these markets without worrying about delays in cross-exchange transfers. A single fee structure reduces the minimum profit spread for these transactions, while a unified execution environment ensures a better turnover rate.

4) Lower transaction costs Most exchanges offer fee discounts based on total transaction volume. Integrating spot and futures trading on one platform helps to reach higher volume levels, thus providing better rates for users and traders.

5) Simplified Accounting and Tax Reports Having all transactions on one platform makes it easier to track positions, calculate profits and losses, and prepare tax documents.

6) Trading volume impact

From the perspective of trading volume, the introduction of the native spot market is expected to immediately increase Hyperliquid's daily trading volume, thereby Increase the costs it incurs. By analyzing the spot to perpetual futures trading volume ratios of leading centralized exchanges such as Binance, Bybit and OKEx, we found that spot trading volume accounts for an average of about 27.02% of perpetual futures trading volume. While this highlights a stronger preference for perpetual futures trading, it may also be affected by the difference between the number of listed spot markets and the number of perpetual markets.

If Hyperliquid can list on a non-Hyperliquid native spot market with a similar number to perpetual futures, it is reasonable to increase its trading volume by at least 25%. This is Unit's long-term goal, however, we expect the launch of non-Hyperliquid native assets to be incremental, starting with BTC, ETH and SOL, as it takes considerable preparation time to build infrastructure to support a variety of assets.

If we only look at the BTC and ETH spot and perpetual futures trading volumes on some of the largest CEXs, we will find that spot trading volume accounts for approximately 10-20% of perpetual futures trading volume. By weighted average of trading volume, we found that spot trading volumes of BTC and ETH accounted for approximately 18% of perpetual futures trading volume.

So, if Unit increases spot BTC and ETH trading on Hyperliquid, we expect the total BTC and ETH trading volume on Hyperliquid to increase by at least 18% (i.e. BTC Hyperliquid Perpetual Futures 18% of the transaction volume).

The average daily trading volume of Hyperliquid's BTC perpetual market has been 21,413 BTC in the past month. Assuming the current spot to perpetual futures trading volume ratio remains at 18%, this means that the BTC volume in the Hyperliquid spot market (BTC/USDC) will immediately increase by about 3,854.34 BTC/day, about $350 million at the current price.

Similarly, Hyperliquid's ETH perpetual market has recorded an average daily volume of 550,136 ETH in the past month. At the same 18% ratio, we estimate that the daily trading volume of Hyperliquid's ETH spot market may reach about 99,024 ETH, whenThe previous price is calculated at about $272 million.

Although this method compares spot and perpetual futures trading volumes on centralized exchanges and briefly compares the current status of Hyperliquid's perpetual futures trading volumes, it fails to recognize Hyperliquid's cross-collateralization and Margin utilization may not be completely equivalent to Binance and other functions. The next section will explore how integrating native spot assets on Hyperliquid has a doubling effect on perpetual and spot trading volumes.

7) Collateral and margin impact When opening a position, the default setting is cross margin, maximizing capital efficiency by sharing collateral between all other cross margin positions. Currently, perpetual contracts on the platform use a single main margin method: USDT-denominated linear contracts use USDC as margin. In this setup, the oracle price is based on USDT, while the collateral is held at USDC. This approach effectively balances liquidity and accessibility.

For assets whose main liquidity sources are denominated in USDC, the oracle price is also based on USDC. Currently, the only perpetual contracts denominated in USDC are PURR-USD and HYPE-USD, both of which use the Hyperliquid spot market as their most liquid oracle source.

Hyperliquid can achieve functional equality with CEX in terms of collateral and margin mechanisms in the following ways: use spot positions and user's perpetual positions to achieve cross margin; margin collateral is not limited to USDC.

Adding non-Hyperliquid native spot assets and these two margin mechanisms will enable coin-price perpetual trading. The underlying crypto spot assets (such as Bitcoin) will be used as margin and settlement currency. In these contracts, traders must provide crypto assets as collateral, and all profits and losses are settled in the same crypto assets. This structure is particularly attractive to investors who firmly believe in the long-term value appreciation of their spot positions. By using spot bitcoin as collateral for perpetual positions – rather than converting to stablecoins – traders can take advantage of the profits and losses generated by these positions to effectively increase their crypto asset holdings and enhance their long-term portfolio. Additionally, currency standard contracts enable long-term holders to hedge price declines without liquidating their assets or converting them into fiat or stablecoins.

The popularity of coin-primary derivatives is obvious when examining relative open contracts for stablecoin margin and coin-primary products on major exchanges including Binance, OKEx, Bybit, Deribit and Huobi . As of this writing, the perpetual open contract for stablecoin margin is 220k BTC (>$20.04 billion), while the open contract for coin standard products is 71k BTC ($7.54 billion).

Open positions in Bitcoin standard contracts over the past yearAbout the company remains stable, accounting for 35% to 45% of open positions in Bitcoin stablecoin margin contracts. This stable demand highlights the market's demand for currency-prime derivatives. Against this backdrop, Hyperliquid's introduction of currency-primary derivatives may significantly increase open contracts, liquidity and trading volume. If we assume similar open contract and volume ratios observed by centralized exchanges, Hyperliquid may increase by about 40% on both indicators, significantly enhancing its market depth and activity.

Although open contracts of coin standard contracts remain stable, we usually see that they exist in only a few tokens, usually large assets such as BTC and ETH, sometimes BNB and TRX, and a few Large-cap assets are used for orphan instances (e.g., SHIB/DOGE pairs).

Major exchanges such as Binance, OKX and Bybit have developed complex risk models over the years to assess collateral value based on the following factors:

• Liquidity: Assets are sold in large quantities ease of time

• Historical volatility: price fluctuation amplitude

• Market depth: slippage in large-scale transactions

• Market value and trading volume< /p>

Large market assets such as BTC and ETH usually receive preferential trading conditions (higher LTV) due to their superior liquidity characteristics and price stability. Sub-primary assets such as BNB, although maintaining significant market capitalization, are limited by more conservative parameters (lower LTV) due to their higher volatility indicators, lower market depth and trading volume.

Although assets like BNB are included as quoted assets in the currency standard market, the adoption rate is limited. For example, the USD perpetual contract showed strong trading volume on Avalanche (433.1M), while the USDT perpetual contract showed the highest adoption rate in Sui (7.8B) and Tron (25.4B) trading. USDC perpetual contracts always show lower trading volumes across all assets.

The trading volume is significantly smaller - Solana leads with a BNB trading volume of 690.3K, while its total USD stablecoin trading volume is 12.5B, followed by Sui (3.2M vs 12.7B total), Tron ( 20M vs 50.7B total) and Avalanche (155.2K vs 834.5M total). This accounts for less than 0.0002% of all asset trading activities, indicating that the market has extremely limited interest in the current form of BNB currency standard contracts.

(2) Funding Arbitrage

Adding spot trading introduces several unique opportunities for users. Specifically, including non-native Hyperliquid spot assets will allow seamless execution of futures basis trading. For example, users can go long for spot Bitcoin and short for BTC perpetual contracts, with the capital rate being positivePayment is collected every hour. Enabling this strategy in a decentralized and self-hosted environment may attract a large amount of transaction volume to the platform, while also helping to regulate funding rates and promote more effective market dynamics.

In addition, if Hyperliquid enables cross-collateralization and coin-prime contracts, users can use their spot BTC positions as collateral while shorting the perpetual contract. This setup will significantly reduce the liquidation risk of its short hedging, as collateral value and profit and loss of short positions will largely offset each other, providing a more stable and secure hedging mechanism.

1) Fund Arbitrage Treasury Hyperliquid can introduce the ability to trade spot HIP-1 and selected non-native spot assets directly from the vault, possibly starting with an approved asset whitelist. This feature will pave the way for a fully on-chain, verifiable Delta neutral fund arbitrage treasury, providing traders and investors with new levels of transparency and efficiency.

2) Reverse Fund Arbitrage The implementation of EVM can unlock the reverse fund arbitrage strategy during the period when the Hyperliquid perpetual contract fund rate is negative. Users can deposit USDC into the lending market on the EVM—or if Hyperliquid introduces a native lending mechanism, on L1—borrow spot assets and short on the spot order book. At the same time, they can go long on perpetual contracts, allowing them to pay with funds generated by negative fund rates.

3) Structured Products and Tokenized Vaults The platform has the potential to attract large volumes and open contracts through structured products such as Ethena's Delta neutral stablecoin. It is worth noting that Shoku has proposed to designate Hyperliquid as a “qualified place for its partial hedging stream”, which could significantly boost open contracts and trading volume, as Ethena’s USDe stablecoin has grown to $5.9 billion in TVL. In addition, several other teams are actively developing similar structured products, further expanding the opportunity.

The launch of EVM is also expected to bring new practicality to the vault through asset tokenization. Fund treasury, HLP treasury and user-created treasury can be tokenized to be traded and exchanged on HyperEVM. This innovation could trigger the development of DeFi strategies surrounding leveraging tokenized vaults, unlocking greater flexibility and opportunities for users to within the ecosystem.

(3) Market Maker At present, most top market makers utilize major brokerage firms such as FalconX, which support cross-exchange cross-margin and mortgage. This approach allows for high capital efficiency, increase transaction volume and improve transaction pricing that they can provide. When Hyperliquid enables collateral for spot assets, open contracts, liquidity and trading volume may be significantly increased as market making in spot and perpetual markets becomes more capital-efficient. Users can also benefit from smaller spreads as a result.

(4) Options After integrating spot and futures markets, it makes sense for Hyperliquid to integrate options trading (or build options trading protocols on top of Hyperliquid/HyperEVM) because they already have a CLOB for trading— —Although decentralized options trading volume is underperforming in the crypto space compared to giants such as Deribit.

Introduction to the spot market will help Hyperliquid's options trading by improving capital efficiency and execution speed. Additionally, it will allow traders to use the spot market for Delta hedging options and enable real-time settlement.

On the other hand, options can be completely built on perpetual futures (such as Deribit's model), because market makers can use perpetual futures instead of spot for perfect hedging, and settlement can be made through perpetual futures The market is based on cash. Given that the dominant crypto option venues (Deribit, OKX, Binance) all operate perfectly without spot stock, the market has developed around cash settlement derivatives, and most crypto option market making infrastructure and systems have revolved around futures/perpetual Hedging construction. Although the crypto derivatives market has evolved to derivatives around cash settlement, some traders prefer spot markets over futures markets, especially if they may wish to gain exposure to their underlying assets.

1) Spot Delta hedging Delta hedging options do not require a spot market. Traders can choose to use futures/derivative contracts instead of spot exposure for Delta hedging, and may even be in an advantage position as they can use less capital (via leverage). Nevertheless, the spot market may be helpful, as some traders prefer them and can benefit from the capital efficiency brought about by spot market integration.

Delta refers to the degree to which option prices respond to changes in underlying assets every 1 dollar. For example, if the Delta of the option is 0.5, when the underlying asset changes by $1, its price will theoretically change by $0.50. For Delta hedging, you take the opposite position in the underlying asset to offset this risk. For call longs with Delta of 0.5, you will short the underlying asset of 0.5 units. For short calls with 0.5 Delta, you will be long for 0.5 units of underlying assets.

For example, if a user sells 1 BTC call option with a Delta of 0.6, they can buy 0.6 BTC immediately for spot Delta hedging. If the price goes up and Delta becomes 0.7, they can buy an additional 0.1 BTC to keep Delta neutral and can be constantly adjusted according to market changes.

The spot market allows traders to use collateral between spot and option positions, reducing the demand for excess margin. In addition, if Delta changes due to price changes, prefers hedging through the spot marketUsers can immediately perform hedging adjustments in the spot market without having to route orders through external locations, reducing slippage and execution risks.

2) Real-time spot settlement Although encrypted options are usually settled in cash through the derivatives market, having spot assets on the platform can achieve the option of "physical" settlement, that is, actually delivering spot assets when exercising rights. • For call options: The platform can transfer the underlying spot assets from the seller to the buyer • For put options: The platform can execute spot sales at the strike price

(5) HL volume growth model estimates Hyperliquid is introducing Bitcoin The additional volume that may be processed after spot trading with Ethereum is challenging for several reasons. First, direct comparison of CEX spot trading volume with perpetual futures trading volume fails to take into account the product differences between Hyperliquid and traditional CEX platforms, and the current position of Hyperliquid in its development roadmap. We consider Hyperliquid as being in its early stages; for the moment, it still lacks key features—such as margin and cross-collateral—which are essential to provide a comparable experience to platforms like Binance, especially for market makers and volume/ Liquidity.

However, we can develop a simple model to estimate the trading volume of Hyperliquid after adding spot BTC and ETH as well as coin standard positions and cross-collateralization. This can be achieved by analyzing the current spot to perpetual futures trading volume ratio on CEX.

First, we look at the average daily BTC perpetual futures trading volume on Hyperliquid and apply 18 we calculated previously from the BTC and ETH spot to perpetual futures trading volume ratios for Binance, Bybit and OKEx %spot/perpetual futures ratio. This will generate an additional 3,854 BTC daily trading volume for the BTC spot market, 99,024 ETH daily trading volume for the ETH spot market, with an annualized additional trading volume of US$231 billion. However, we expect this to be the "final state" and it will take considerable preparation time as people gradually adopt native assets, market makers are familiar with the system, and Hyperliquid launches cross margin and coin standard positions.

1) FTX Growth Case Study – Using altcoins, in-app margin/lending Despite failures, FTX has a margin system that users can use effectively within the app Spot altcoins, margin and lending – this drives the growth of the platform. Overall, FTX introduces two interesting margin mechanisms: a unified margin system and an automatic cross-margin system, both of which are committed to increasing exchange trading volume and improving market depth.

Unified margin method puts all assets into a single collateral pool, rather than a separate wallet. When traders hold USD, BTC and ETH, they can bring all of these assets togetherUsed as collateral for any position. This eliminates the problem of funds being stuck in different wallets or locked into specific transactions.

The cross margin system extends this by applying the same risk calculations to spot and futures positions. Instead of setting different margin requirements for each trading type, the system looks at the total position value. For example, a short position of 2 BTC is a position of $30,000 when the price of Bitcoin is $15,000, whether in spot or futures. Margin requirements comply with the standard calculation: the initial margin is [(1.1/collateral weight)-1] multiplied by the position size, and the maintenance margin is [(1.03/collateral weight)-1].

The automation of this system increases marketing activities. Automatic cross-margin system handles lending and collateral without the need for manual management by traders. When someone places an order or wants to withdraw money, the system calculates the required borrowing, executes the borrowing order, and updates the collateral requirements immediately. If a trader with $50,000 wants to sell 1 BTC without it, the system will automatically borrow BTC and manage new positions (+$65,000, -1 BTC).

This automation has led to an increase in transaction volume. When traders can use their assets as collateral to earn borrowing income at the same time, they are more likely to keep their assets on the platform and trade actively. This creates a feedback loop: more deposits increase the size of the lending pool, thereby supporting more transactions, attracting more market makers and increasing transaction volume.

The improvement of capital efficiency can also drive the growth of trading volume. By using a single mortgage pool and an automated lending mechanism, traders can use their capital more actively. They can trade in multiple markets without transferring funds, and the system will continue to optimize their margin usage efficiency.

These mechanisms work together and are expected to increase asset trading volume and market depth. When unified margin and automatic cross margin reduce trading friction, it often leads to more transactions. Better liquidity and borrowing returns can attract more traders, and more traders usually mean greater trading volume. This model of growing transaction volume and market participation helps assets develop a more mature and active market.

2) What role does spot trading play in truly realizing an integrated trading experience?

Trading platforms that provide both spot and derivatives markets can provide a more unified trading experience, which can improve capital efficiency (support cross margin), risk and order management, and trading opportunities (especially basis trading and capital rate arbitrage):

• There is a single source of real position in position and order management, which means that users do not need to reconcile positions between multiple exchanges. Complex order types are easier to manage, order cancellation, modification and management are easier to order, and traders do not need to deal with multiple exchanges, so the delay is lower.

In addition, traders only need to learn and integrate an API, which simplifies order management, key management, and further reducesLow complexity.

• Capital Efficiency and Cross Margin Users can use their spot positions as collateral for futures positions, thereby reducing the total capital required and improving capital efficiency. In an EVM environment, this also allows users/traders to earn profits while holding spot positions as collateral and to gain futures exposure without selling spot stock.

The exchange usually considers the entire portfolio (spot + futures) when calculating margin requirements. In margin calculation, spot long positions can offset futures short positions. This reduces the total collateral required compared to having a separate account on different exchanges.

• Arbitrage opportunities have two markets on one platform, allowing users to more effectively utilize the price differences between spot and futures markets, reduce transaction costs without the need to transfer funds between exchanges .

For basis trading, when a price difference occurs, traders can quickly execute the two legs of the transaction on a single exchange without delay due to capital transfers between platforms. Furthermore, the lower transaction costs associated with trading on an exchange make it profitable to capture smaller spreads.

For capital rate arbitrage, including cash and arbitrage trading, traders can hold spot positions while shorting perpetual futures, thereby collecting funds for payment while keeping delta neutral. Holding these two positions on the same exchange significantly simplifies position management and monitoring.

Marketing becomes more effective when operating both spot and futures markets on a single exchange. Traders can provide liquidity in both markets while conducting real-time arbitrage between order books. A unified inventory view makes position management more efficient, and spot positions can be used as support for futures market making activities.

When trading spot and futures at one exchange, it is more effective to capture lightning arbitrage opportunities. Traders can quickly deal with short-term price misalignment between these markets without worrying about delays in cross-exchange transfers. A single fee structure reduces the minimum profit spread for these transactions, while a unified execution environment ensures a better turnover rate.

• Lower transaction costs Most exchanges offer fee discounts based on total transaction volume. Integrating spot and futures trading on one platform helps to reach higher volume levels, thus providing users and traders with better rates.

• Simplified Accounting and Tax Reporting All transactions on one platform make it easier to track positions, calculate profits and losses, and prepare tax documents.